Germany 120mm Tank Ammunition Market Report: Trends, Growth and Forecast (2026-2032)

By Ammunition Type (APFSDS (Armor-Piercing Fin-Stabilized Discarding Sabot), HEAT (High-Explosive Anti-Tank), HE (High-Explosive), MP/Multi-Purpose, Programmable/Smart Ammunition, Training/Practice Rounds), By Tank Platform Compatibility (NATO Standard 120mm (Smoothbore), Non-NATO/Other 120mm Systems), By End User (Army/Land Forces, Defense Contractors, Training & Testing Institutions), By Guidance Type (Unguided, Programmable/Airburst, Precision-Guided) ... Read more

|

Major Players

|

Germany 120mm Tank Ammunition Market Statistics and Insights, 2026

- Market Size Statistics

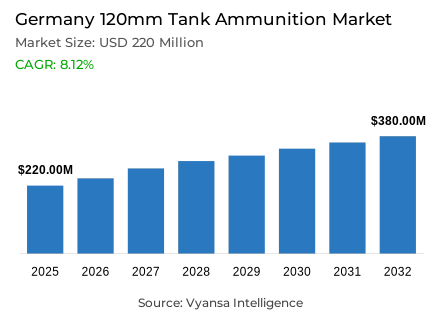

- 120mm tank ammunition market size in Germany was estimated at USD 220 million in 2025.

- The market size is expected to grow to USD 380 million by 2032.

- Market to register a CAGR of around 8.12% during 2026-32.

- Ammunition Type Shares

- Apfsds (armor-piercing fin-stabilized discarding sabot) grabbed market share of 50%.

- Competition

- More than 5 companies are actively engaged in producing 120mm tank ammunition in Germany.

- Top 1 companies acquired the maximum share of the market.

- Rheinmetall etc., are few of the top companies.

- Guidance Type

- Unguided grabbed 70% of the market.

Germany 120mm Tank Ammunition Market Outlook

Germany's 120mm tank ammunition market was valued at USD 220 million in 2025 and is projected to reach USD 380 million by 2032, growing at a CAGR of around 8.12% during 2026-32. This steady expansion is backed by Germany's record defence budget of €86.37 billion in 2025 and a significant contract for 105 Leopard 2 A8 tanks worth approximately €2.9 billion, both of which directly drive demand for training and combat ammunition stocks.

Procurement arrangements are adapting to facilitate this demand. The Bundeswehr has adopted multi-year framework contracts, and Rheinmetall has reported an order for 120mm ammunition worth several hundred million euros within a framework contract ceiling of approximately €4 billion. This allows industry to better understand production quantities, although capacity expansions are limited by the slow pace of permitting, as evidenced by Rheinmetall's Sardinia plant being held back for several years by regulatory hurdles before eventual approval.

Breaking down by ammunition type, APFSDS ammunition leads demand at 50%, due to its importance in destroying current armour and maintaining tank crews' skills through realistic gunnery training. The overall European rearmament cycle, with EU defence expenditure reaching €343 billion in 2024, also generates further multi-national demand that German manufacturers of 120mm tank ammunition can tap into via collective NATO procurement arrangements, such as a €200 million NSPA call-off contract in early 2026.

For guidance systems, unguided ammunition leads with a 70% market share due to their logistical simplicity, storage convenience, and compatibility with NATO smoothbore standardization. Although guided ammunition is available, their premium price makes them less economical for mass storage, ensuring that unguided ammunition remains firmly at the forefront of Germany's replenishment requirements.

Germany 120mm Tank Ammunition Market Growth DriverDefence Funding Pushes Armour Re-Stocking

Germany’s defence spending is rising in a way that directly supports larger ammunition buys and stock rebuilding. In the 2025 federal budget process, the Bundestag reports total defence spending of €86.37 billion, the highest level so far, with major procurements also financed via the Bundeswehr special fund. This larger, committed funding base keeps training and readiness cycles active, which lifts recurring demand for 120mm tank rounds.

Armour modernisation reinforces that pull. The Federal Ministry of Defence signs a contract for 105 Leopard 2 A8 tanks with costs of around €2.9 billion, financed through the special fund and the regular defence budget. More modern Leopard fleets require both combat loads and steady live-fire training stocks, pushing consistent ordering of 120mm ammunition. Sources: German Bundestag and BMVg.

Germany 120mm Tank Ammunition Market ChallengePermitting Delays Limit Output Scaling

Scaling 120mm supply is constrained by slow permitting and capacity ramp-ups across the munitions industrial base. A recent Rheinmetall case shows the issue clearly: a €50 million munitions facility in Sardinia faces years of political and legal wrangling and only receives final approval after an environmental impact process, delaying when output can actually start and scale.

This matters for Germany because demand signals are large and time-sensitive. Rheinmetall states that the Bundeswehr places another 120mm tank-ammunition order worth “several hundred million euros” under a framework agreement whose ceiling is around €4 billion. When production expansions depend on lengthy approvals and local resistance, suppliers struggle to synchronise deliveries with replenishment plans, increasing schedule and availability risk even when budgets are available. Sources: Rheinmetall; Financial Times.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Germany 120mm Tank Ammunition Market TrendFramework Contracts and Pooled Buying Expand

Procurement is shifting toward multi-year frameworks with repeated call-offs, instead of one-off spot buys. Rheinmetall notes that the Bundeswehr’s latest 120mm order (covering combat and training rounds) sits under an existing framework, and that Germany expanded the contract ceiling to around €4 billion. This structure supports steady replenishment and gives industry clearer volumes to plan production, materials, and test capacity against.

At the alliance level, pooled procurement is becoming a practical channel for standardised 120mm rounds. In February 2026, Rheinmetall reports that NATO’s Support and Procurement Agency makes a first call-off worth around €200 million under a 2025 framework, with the Basic Contractual Instrument signed in July 2025. In practice, this normalises common specifications and faster ordering for NATO-standard tank ammunition. Sources: Rheinmetall; NSPA framework details.

Germany 120mm Tank Ammunition Market OpportunityEU Rearmament Lifts Cross-Border Orders

Europe’s broader rearmament cycle creates a larger, more predictable demand pool that Germany-based 120mm suppliers can tap. The European Defence Agency reports EU defence expenditure reaches €343 billion in 2024, a 19% rise versus 2023, and links the increase to record levels of equipment procurement. In 2026, this higher baseline keeps ammunition and spares procurement politically “funded and urgent,” not discretionary.

That environment opens commercial room for German prime contractors and sub-tier manufacturers to scale output with allied orders, not just national demand. Rheinmetall reports a first NATO Support and Procurement Agency call-off worth around €200 million under a 2025 framework for 120mm tank ammunition, serving multiple NATO countries. For German production lines and their supply chains, these multi-country call-offs translate into larger batch sizes and steadier planning for raw materials and qualification testing. Sources: EDA; Rheinmetall.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Germany 120mm Tank Ammunition Market Segmentation Analysis

By Ammunition Type

- APFSDS (Armor-Piercing Fin-Stabilized Discarding Sabot)

- HEAT (High-Explosive Anti-Tank)

- HE (High-Explosive)

- MP/Multi-Purpose

- Programmable/Smart Ammunition

- Training/Practice Rounds

The segment with the highest share under the Ammunition Type is APFSDS (Armor-Piercing Fin-Stabilized Discarding Sabot), holding 50% of demand. This dominance is practical: APFSDS is the “go-to” round for defeating modern armour, so it stays central to both doctrine-driven war-reserve planning and realistic gunnery training for heavy armour units.

APFSDS also fits how fleets are used day to day. Armoured formations train against hard targets and need consistent ballistic performance to keep crews qualified, which keeps repeat orders steady. Other 120mm round families support different mission sets, but they do not replace the need for a dedicated kinetic penetrator in high-threat scenarios. As a result, procurement baskets typically prioritise APFSDS first, and then balance inventories with complementary round types.

By Guidance Type

- Unguided

- Programmable/Airburst

- Precision-Guided

The segment with the highest share under the Guidance Type is Unguided, accounting for 70% of demand. Most 120mm tank rounds are designed to be fired as high-velocity, ballistic munitions from the main gun, so unguided solutions remain the default for both training and combat loads where crews need simple, repeatable handling.

Unguided rounds also stay attractive for logistics. They are easier to store, certify, and move at scale, and they align with NATO standardisation around 120mm smoothbore systems. While guided concepts exist in the wider land-munitions space, they typically add cost and integration complexity that is harder to justify for routine gunnery and bulk stockpiles. In practice, Germany’s buying mix keeps unguided rounds as the backbone, with specialised options playing a narrower role.

List of Companies Covered in Germany 120mm Tank Ammunition Market

The companies listed below are highly influential in the Germany 120mm tank ammunition market, with a significant market share and a strong impact on industry developments.

Market News & Updates

- Rheinmetall, 2026:

Rheinmetall’s first call-off under the NATO Support and Procurement Agency (NSPA) 120mm tank ammunition framework (structured as a “Basic Contractual Instrument” signed in July 2025) is valued at ~€200 million and-per Rheinmetall’s official release wording-covers 35,000 rounds of 120mm tank ammunition for multiple NATO end customers; for the Germany 120mm tank ammunition market, this is a concrete 2026 demand signal that reinforces Rheinmetall’s position as a primary large-calibre supplier within NATO procurement channels and supports higher utilization and prioritization of German-linked manufacturing/supply capacity for 120mm natures aligned to Leopard-class requirements.

- Rheinmetall, 2025:

In December 2025, the Bundeswehr placed another call-off with Rheinmetall for 120mm tank ammunition (combat and training) under its existing framework agreement, with the new order intake described as “several hundred million euros”; the same Rheinmetall release notes Germany’s broader framework expansion to ~€4 billion and the ability through 2030 to procure several hundred thousand 120mm x 570 cartridges, which in Germany’s 120mm market context materially increases procurement visibility and underwrites multi-year production planning, supplier contracting, and inventory rebuilding for Leopard 2 ammunition demand.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Germany 120mm Tank Ammunition Market Policies, Regulations, and Standards

- Germany 120mm Tank Ammunition Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Germany 120mm Tank Ammunition Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Ammunition Type

- APFSDS (Armor-Piercing Fin-Stabilized Discarding Sabot)- Market Insights and Forecast 2022-2032, USD Million

- HEAT (High-Explosive Anti-Tank)- Market Insights and Forecast 2022-2032, USD Million

- HE (High-Explosive)- Market Insights and Forecast 2022-2032, USD Million

- MP/Multi-Purpose- Market Insights and Forecast 2022-2032, USD Million

- Programmable/Smart Ammunition- Market Insights and Forecast 2022-2032, USD Million

- Training/Practice Rounds- Market Insights and Forecast 2022-2032, USD Million

- By Tank Platform Compatibility

- NATO Standard 120mm (Smoothbore)- Market Insights and Forecast 2022-2032, USD Million

- Non-NATO/Other 120mm Systems- Market Insights and Forecast 2022-2032, USD Million

- By End User

- Army/Land Forces- Market Insights and Forecast 2022-2032, USD Million

- Defense Contractors- Market Insights and Forecast 2022-2032, USD Million

- Training & Testing Institutions- Market Insights and Forecast 2022-2032, USD Million

- By Guidance Type

- Unguided- Market Insights and Forecast 2022-2032, USD Million

- Programmable/Airburst- Market Insights and Forecast 2022-2032, USD Million

- Precision-Guided- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Ammunition Type

- Market Size & Growth Outlook

- Germany APFSDS (Armor-Piercing Fin-Stabilized Discarding Sabot) Tank Ammunition Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Tank Platform Compatibility- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Guidance Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Germany HEAT (High-Explosive Anti-Tank) Tank Ammunition Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Tank Platform Compatibility- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Guidance Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Germany HE (High-Explosive) Tank Ammunition Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Tank Platform Compatibility- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Guidance Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Germany MP/Multi-Purpose Tank Ammunition Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Tank Platform Compatibility- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Guidance Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Germany Programmable/Smart Tank Ammunition Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Tank Platform Compatibility- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Guidance Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Germany Training/Practice Rounds Tank Ammunition Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Tank Platform Compatibility- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Guidance Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Rheinmetall

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Others

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Rheinmetall

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Ammunition Type |

|

| By Tank Platform Compatibility |

|

| By End User |

|

| By Guidance Type |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.