Finland 155mm Artillery Shells Market Report: Trends, Growth and Forecast (2026-2032)

By Shell Type (High-Explosive (HE\HE-FRAG) Shell, Smoke Shell, Illumination Shell, Training/Practice Shell, Other Special-Purpose Shell), By Guidance (Unguided, Precision-Guided), By Range Class (Standard Range, Extended Range, Assisted Range (Base Bleed, Rocket-Assisted (RAP))), By Operational Use (Training Consumption, Routine Peacetime Stockpile Replenishment, Active Conflict Replenishment\Urgent Operational Demand, Strategic Reserve\Surge Inventory Build), By Artillery Platform Type (Towed Howitzers, Self-Propelled Howitzers, Truck-Mounted Howitzers) ... Read more

|

Major Players

|

Finland 155mm Artillery Shells Market Statistics and Insights, 2026

- Market Size Statistics

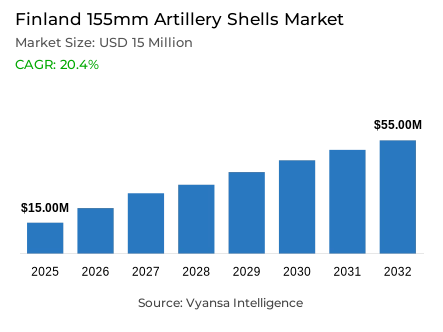

- 155mm artillery shells market size in Finland was estimated at USD 15 million in 2025.

- The market size is expected to grow to USD 55 million by 2032.

- Market to register a CAGR of around 20.4% during 2026-32.

- Shell Type Shares

- High-explosive (he/he-frag) shell grabbed market share of 65%.

- Competition

- 155mm artillery shells in Finland is currently being catered to by more than 10 companies.

- Top 5 companies acquired around 80% of the market share.

- Elbit Systems, General Dynamics Ordnance & Tactical Systems, Thales, Nammo, Rheinmetall etc., are few of the top companies.

- Guidance

- Unguided grabbed 85% of the market.

Finland 155mm Artillery Shells Market Outlook

The Finland 155mm artillery shells market was valued at approximately USD 15 million in 2025 and is projected to reach USD 55 million by 2032, registering a strong CAGR of around 20.4% during 2026-32. This robust growth is anchored in Finland's significantly elevated defence budget, with the 2026 national budget introducing EUR 6 billion in new procurement authorities and linking nearly EUR 3 billion in expenditure to 2026 alone. Combined EU and national investments of roughly EUR 56.5 million are further strengthening domestic manufacturing capacity to meet both national readiness goals and NATO interoperability requirements.

On the supply side, upstream energetics remain the most critical bottleneck. Nitrocellulose, propelling powder, and explosive-grade compounds are scarce inputs that constrain how fast production can scale. EU-backed grants-EUR 22.5 million to Nammo Lapua and EUR 10 million to Nammo Vihtavuori-are helping address these gaps, though regulatory complexity means capacity ramp-ups take time. A separate EUR 90 million agreement with the European Commission to supply Ukraine via the European Peace Facility adds a steady additional demand layer, creating a dual-demand dynamic that is reshaping production planning across the supply base for 155mm artillery shells.

From a product perspective, demand remains heavily concentrated in High‑Explosive variants, which command approximately 65% of total procurement volumes. They are the most preferred stockpiling option due to their versatility in operations which include suppression, neutralisation and training missions. Unguided rounds dominate even more decisively, capturing around 85% of procurement, driven by cost efficiency and logistical simplicity compared with precision‑guided alternatives.

Looking ahead, continued government investment, EU coordination, and a formalised export commitment to Ukraine position Finnish producers for sustained expansion through 2032, establishing the country as an increasingly capable hub for European ammunition supply and defence manufacturing.

Finland 155mm Artillery Shells Market Growth DriverIncreasing Defence Budget Allocations and Front-Loaded Procurement Strategies

Finland's 2026 national budget proposal significantly elevates defence materiel procurement, introducing new procurement authorities totalling EUR 6 billion. Of this, EUR 4 billion is designated for the broader development of Defence Forces' materiel, while EUR 2 billion is specifically allocated to joint weapons systems-a category that directly encompasses ammunition procurement. This front-loaded fiscal strategy links nearly EUR 3.0 billion in expenditure to 2026 alone, sustaining high contracting intensity and ensuring a steady pipeline of 155mm shell orders for stock replenishment and operational readiness training, even as payments extend into subsequent fiscal years.

The deliberate structuring of procurement authorities in this manner reflects Finland's strategic intent to maintain wartime readiness while meeting NATO interoperability requirements. By committing procurement volumes early in the cycle, the Ministry of Defence enables domestic and allied suppliers to plan production capacity with greater certainty. This approach stabilises demand signals for 155mm artillery shell manufacturers and reduces lead-time volatility, positioning the Finland 155mm artillery shells market for sustained, predictable growth driven by government-mandated defence modernisation objectives.

Finland 155mm Artillery Shells Market ChallengeUpstream Supply Chain Bottlenecks in Propellant and Energetics Production

A critical structural constraint limiting the scalability of 155mm shell output in Finland lies not in shell machining capacity but in the availability of upstream energetics-primarily nitrocellulose, propelling powder, and explosive-grade compounds. This challenge is recognised at the European level, with the European Commission's ASAP work programme explicitly targeting these bottlenecks across member-state ammunition supply chains. The dependency on specialised chemical processes for producing propellant-grade materials creates significant lead-time and throughput limitations that cannot be resolved through investments in downstream manufacturing alone.

Finland's industry landscape reflects these pressures directly. Under EU-backed support frameworks, Nammo Vihtavuori has received EUR 10 million to expand nitrocellulose and powder output, while Nammo Lapua has been allocated EUR 22.5 million to increase 155mm shell capacity. Despite these injections, regulatory compliance requirements and the complexity of energetics processing continue to constrain the pace at which production can be ramped up. For end users relying on consistent ammunition deliveries, managing these chemical-processing bottlenecks remains the foremost operational and procurement challenge within the Finland 155mm artillery shells market.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Finland 155mm Artillery Shells Market TrendEU-Backed Financing Mechanisms and Frozen-Asset Procurement Models Reshaping Market Dynamics

A significant structural shift is emerging in how Finland's 155mm artillery shell procurement is financed and directed. Finland has formalised an agreement with the European Commission to supply Ukraine with heavy ammunition funded through the European Peace Facility, leveraging proceeds from frozen Russian sovereign assets. The agreement is valued at EUR 90 million and positions Finnish domestic suppliers as primary source manufacturers for these deliveries. This novel financing channel effectively generates an additional demand layer for Finnish production lines, independent of conventional national budget allocations.

This arrangement is reshaping production planning rhythms across the Finnish ammunition supply base. End users and procurement planners must now align manufacturing schedules with EU-mandated delivery windows and associated documentation standards, rather than operating solely within domestic scheduling frameworks. The result is a more regularised order cadence for NATO-standard 155mm shells, as local producers balance national replenishment mandates against EU-coordinated export commitments. This dual-demand dynamic is increasingly becoming a defining trend in the Finland 155mm artillery shells market, introducing new layers of compliance, coordination, and capacity optimisation.

Finland 155mm Artillery Shells Market OpportunityExpanding EU Grant Support and National Co-Investment Creating Scalable Capacity

Finland's ammunition manufacturing base stands at a strategically advantageous position, having secured the full amount applied for under the European Commission's ASAP grant programme. The Finnish Government has confirmed EUR 32.5 million in EU funding directed at ramping up domestic ammunition production, with Finnish industry benefiting from the entirety of the applied allocation-a signal of confidence in Finland's industrial readiness and project quality. This EU-backed funding is specifically oriented toward expanding shell manufacturing throughput and reinforcing critical input supply chains within the country.

Complementing this EU support, the Ministry of Defence has separately allocated approximately EUR 24 million in national funding to increase domestic ammunition production. Together, these combined investments of nearly EUR 56.5 million create a well-capitalised platform for Finnish manufacturers to scale capacity in a structured, risk-managed manner. For end users across the Defence Forces and allied procurement programmes, this expansion translates into improved security of supply, reduced import dependency, and an enhanced ability to fulfil both domestic readiness requirements and EU-linked framework orders-establishing Finland as an increasingly capable hub within the broader European 155mm Artillery Shells Market.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Finland 155mm Artillery Shells Market Segmentation Analysis

By Shell Type

- High-Explosive (HE\HE-FRAG) Shell

- Smoke Shell

- Illumination Shell

- Training/Practice Shell

- Other Special-Purpose Shell

Within the Finland 155 mm artillery shells market, segmentation by shell type reveals a pronounced concentration in High‑Explosive (HE/HE‑FRAG) shell variants, which account for approximately 65% of the total market share. Such a leading role indicates the operational flexibility of HE rounds, which can serve a wide range of fire missions, including suppression, neutralisation, and immediate battlefield effect, without relying on specialised target conditions. Their interoperability with standard fuze families and standardised handling processes also increases their priority in procurement, since end users gain the advantage of less inventory complexity in both depots and active firing units.

The remaining 35% of the market share is distributed among mission‑specific variants such as smoke, illumination, and specialised payload rounds, which are procured in limited quantities for defined operational scenarios. Although these shell types are operationally necessary in some engagements, they do not dictate the volume-driven procurement cycles of HE rounds. The ammunition planners of Finland thus focus on HE/HE-FRAG to stockpile to provide contingency depth and to continue with day-to-day gunnery training on a large scale. This procurement philosophy—prioritising the broadest utility per round—is expected to sustain HE dominance as the leading shell type segment throughout the forecast period.

By Guidance

- Unguided

- Precision-Guided

Under the guidance segmentation for the Finland 155 mm artillery shells market, unguided rounds decisively lead, holding approximately 85% of the total market share. This commanding position stems from the fundamental role unguided ammunition plays in high‑volume, cost‑effective fire support operations. For area target engagements and large‑scale training exercises, unguided 155 mm shells offer significant advantages in cost‑per‑shot economics, logistical simplicity, and supply‑chain predictability. End users across Finnish artillery units prioritise these rounds to maintain high baseline readiness levels without incurring the procurement complexity or electronics dependency associated with precision-guided alternatives.

Guided 155 mm rounds, representing the remaining 15% of the market share, are maintained as a mission‑critical but operationally narrow layer of capability. They need to be closely integrated with sophisticated sensor platforms, fire-control software architectures, and specialised fuzing or guidance kits, which make them difficult to procure, logistically support, and maintain by end users. Inventory planners therefore treat guided munitions as a targeted complement to core unguided stockpiles rather than a primary procurement category. While growing investments in precision capabilities may incrementally shift this balance over the long term, unguided rounds are expected to retain their overwhelming share within the Finland 155 mm artillery shells market across the near‑to‑medium term horizon.

List of Companies Covered in Finland 155mm Artillery Shells Market

The companies listed below are highly influential in the Finland 155mm artillery shells market, with a significant market share and a strong impact on industry developments.

- Elbit Systems

- General Dynamics Ordnance & Tactical Systems

- Thales

- Nammo

- Rheinmetall

- Nexter (KNDS)

- BAE Systems

- Eurenco

- MSM Group

Market News & Updates

- Nammo, 2025:

Nammo stated that Sweden, Denmark, Finland, and Norway signed an agreement with Nammo covering “ammunition deliveries, production and services” across peace, crisis, and war conditions, signaling a structural shift toward long-term Nordic security-of-supply frameworks rather than ad-hoc buys; for Finland’s 155mm ecosystem, this materially reduces supply-risk because it ties Finnish demand to a multi-country industrial planning cycle and to Nammo’s Finland footprint—where Nammo notes ongoing capability build-out (e.g., a new primer factory at Vihtavuori) and manufacturing specialization supporting artillery/mortar-related components—thereby improving availability and lead-time resilience for domestically supported artillery ammunition value chains.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Finland 155mm Artillery Shells Market Policies, Regulations, and Standards

- Finland 155mm Artillery Shells Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Finland 155mm Artillery Shells Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Shell Type

- High-Explosive (HE\HE-FRAG) Shell- Market Insights and Forecast 2022-2032, USD Million

- Smoke Shell- Market Insights and Forecast 2022-2032, USD Million

- Illumination Shell- Market Insights and Forecast 2022-2032, USD Million

- Training/Practice Shell- Market Insights and Forecast 2022-2032, USD Million

- Other Special-Purpose Shell- Market Insights and Forecast 2022-2032, USD Million

- By Guidance

- Unguided - Market Insights and Forecast 2022-2032, USD Million

- Precision-Guided - Market Insights and Forecast 2022-2032, USD Million

- By Range Class

- Standard Range - Market Insights and Forecast 2022-2032, USD Million

- Extended Range - Market Insights and Forecast 2022-2032, USD Million

- Assisted Range- Market Insights and Forecast 2022-2032, USD Million

- Base Bleed- Market Insights and Forecast 2022-2032, USD Million

- Rocket-Assisted (RAP)- Market Insights and Forecast 2022-2032, USD Million

- By Operational Use

- Training Consumption- Market Insights and Forecast 2022-2032, USD Million

- Routine Peacetime Stockpile Replenishment- Market Insights and Forecast 2022-2032, USD Million

- Active Conflict Replenishment\Urgent Operational Demand- Market Insights and Forecast 2022-2032, USD Million

- Strategic Reserve\Surge Inventory Build- Market Insights and Forecast 2022-2032, USD Million

- By Artillery Platform Type

- Towed Howitzers- Market Insights and Forecast 2022-2032, USD Million

- Self-Propelled Howitzers- Market Insights and Forecast 2022-2032, USD Million

- Truck-Mounted Howitzers- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Shell Type

- Market Size & Growth Outlook

- Finland High-Explosive (HE\HE-FRAG) Shells Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Guidance- Market Insights and Forecast 2022-2032, USD Million

- By Range Class - Market Insights and Forecast 2022-2032, USD Million

- By Operational Use - Market Insights and Forecast 2022-2032, USD Million

- By Artillery Platform Type - Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Finland Smoke Shells Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Guidance- Market Insights and Forecast 2022-2032, USD Million

- By Range Class - Market Insights and Forecast 2022-2032, USD Million

- By Operational Use - Market Insights and Forecast 2022-2032, USD Million

- By Artillery Platform Type - Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Finland Illumination Shells Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Guidance- Market Insights and Forecast 2022-2032, USD Million

- By Range Class - Market Insights and Forecast 2022-2032, USD Million

- By Operational Use - Market Insights and Forecast 2022-2032, USD Million

- By Artillery Platform Type - Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Finland Training/Practice Shells Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Guidance- Market Insights and Forecast 2022-2032, USD Million

- By Range Class - Market Insights and Forecast 2022-2032, USD Million

- By Operational Use - Market Insights and Forecast 2022-2032, USD Million

- By Artillery Platform Type - Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Nammo

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Rheinmetall

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Nexter (KNDS)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- BAE Systems

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Eurenco

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Elbit Systems

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- General Dynamics Ordnance & Tactical Systems

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Thales

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- MSM Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Nammo

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Shell Type |

|

| By Guidance |

|

| By Range Class |

|

| By Operational Use |

|

| By Artillery Platform Type |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.