Europe Laboratory Information Management System Market Report: Trends, Growth and Forecast (2026-2032)

By Product Type (Clinical Operations LIMS (Hospital Laboratory LIMS, Physician Office Laboratory LIMS, Routine Diagnostics Laboratory LIMS), High-Throughput Testing LIMS (Independent Laboratory LIMS, Commercial Laboratory LIMS, Reference Laboratory LIMS, Multi-site Laboratory Network LIMS), Public Health & Reporting LIMS (Public Health Laboratory LIMS, Surveillance-linked Laboratory LIMS, Reference Network Laboratory LIMS), Research & Repository LIMS (Academic Research Laboratory LIMS, Translational Research Laboratory LIMS, Biobank & Repository LIMS), Regulated QA/QC LIMS (Pharmaceutical Laboratory LIMS, Biotechnology Laboratory LIMS, Food Testing Laboratory LIMS, Environmental Testing Laboratory LIMS, Forensic Laboratory LIMS)), By Workflow Type (Accessioning-to-Result Management (Sample Registration, Sample Tracking, Test Assignment, Result Entry & Release), Instrument-Integrated Workflow Management (Analyzer Connectivity, Automated Data Capture, Bidirectional Instrument Communication), Quality-Controlled Laboratory Workflow (Quality Control Management, Quality Assurance Workflow, Exception & Deviation Handling), Traceability & Repository Workflow (Chain-of-Custody Tracking, Storage & Retrieval Management, Biobank Sample Lifecycle Tracking), Interoperability & Reporting Workflow (External System Connectivity, Standards-based Data Exchange, Regulatory & Public Health Reporting)), By Deployment Model (Controlled Environment Deployment, Scalable Digital Deployment, Mixed Infrastructure Deployment), By End-User Cluster (Care Delivery Laboratories (Hospital Laboratories, Health-System Laboratories, Physician Office Laboratories, Community & Decentralized Testing Laboratories), Commercial Testing Laboratories (Independent Laboratories, Commercial Laboratories, Reference Laboratories), Government & Public Health Laboratories (Public Health Laboratories, Central Reference Laboratories, Disease Surveillance Laboratories), Research & Translational Laboratories (Academic Laboratories, Research Institutes, Biobanks, Clinical Research Support Laboratories), Regulated Scientific & Industrial Laboratories (Pharmaceutical Laboratories, Biotechnology Laboratories, Food Safety Laboratories, Environmental Laboratories, Forensic Laboratories)), By Purchase Model (Perpetual License, Subscription License, Usage-Based Model, Hybrid Commercial Model), By Country (Germany, UK, Netherlands, Switzerland, France, Italy, Spain, Rest of Europe) ... Read more

|

Major Players

|

Europe Laboratory Information Management System Market Statistics and Insights, 2026

- Market Size Statistics

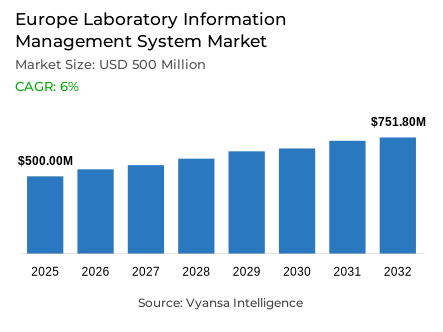

- Laboratory information management system market size in Europe was valued at USD 500 million in 2025 and is estimated at USD 530 million in 2026.

- The market size is expected to grow to USD 751.8 million by 2032.

- Market to register a CAGR of around 6% during 2026-32.

- Product Type Shares

- Clinical operations lims grabbed market share of 35%.

- Competition

- More than 10 companies are actively engaged in producing laboratory information management system in Europe.

- Top 5 companies acquired around 40% of the market share.

- Autoscribe Informatics, Clinisys, Sapio Sciences, LabWare, LabVantage Solutions etc., are few of the top companies.

- Workflow Type

- Interoperability & Reporting Workflow grabbed 30% of the market.

- Country

- Germany leads with a 20% share of the Europe market.

Europe Laboratory Information Management System Market Outlook

Europe laboratory information management system market was valued at USD 500 million in 2025 and is projected to advance from USD 530 million in 2026 to USD 751.8 million by 2032, registering a CAGR of 6% across the forecast period. This steady and institutionally supported expansion reflects a structurally sound growth environment within the Europe laboratory information systems market, where accelerating laboratory digitalisation, rising structured data management requirements, and growing expectations around workflow traceability across healthcare and research settings are collectively reshaping how laboratories across the continent define and deliver operational performance. Growth is anchored not in isolated technology adoption but in a region-wide shift toward more connected, compliant, and data-disciplined laboratory ecosystems driven by both national and supranational health data governance agendas.

Product demand is led by Clinical Operations LIMS, which commands 35% of the overall market within the product type segment. This position reflects sustained and broadly distributed institutional reliance on platforms that govern routine operations, structured sample handling, and day-to-day record management with measurable consistency across European laboratory environments. As laboratories become more process-driven and compliance-oriented, the future of laboratory informatics across the region is being defined by systems that embed operational control and audit-ready documentation directly into core testing workflows rather than treating digital capability as a peripheral function.

Workflow demand is shaped with equal commercial significance by the Interoperability and Reporting Workflow segment, which holds 30% of the total market. This prominence reflects the rising institutional priority placed on platforms that connect results, instruments, and internal systems without introducing delays or duplication into laboratory data flows. Across the region, lab data analytics and reporting tools are being deployed with growing frequency as laboratories recognise that reporting connectivity and structured data exchange have become foundational rather than optional capabilities within modern laboratory informatics environments.

Country concentration further reinforces the regional market structure, with Germany leading the European market at a 20% share that firmly positions it as the most commercially influential national market in the region. This concentration keeps regional demand closely aligned with healthcare digitalisation investment and operational modernisation programmes advancing most actively in Western and Central Europe. Taken together, clinical operations product leadership, interoperability workflow dominance, and Germany's anchor position collectively define a market trajectory that is commercially stable, regulatory-reform responsive, and well-supported through 2032.

Europe Laboratory Information Management System Market Growth Driver

eHealth Expansion Mechanically Drives Laboratory Data Management Demand

The rapid and measurable expansion of electronic health data access across Europe is creating a structurally significant and broadly distributed demand driver for laboratory information management platforms across the continent. As per data published by the European Commission, the EU-27 composite eHealth score reached 83% in 2024, rising by 4 percentage points from the prior year, while 23 Member States reported that between 80% and 100% of their national populations are technically able to access electronic health records through available national services. This scale of connected health record access directly enlarges the volume of laboratory-linked data that must be captured, structured, and reported through compliant digital systems, making laboratory workflow automation software a practical operational necessity rather than a discretionary infrastructure investment across European laboratory networks.

Provider connectivity gains are reinforcing this demand pressure from the supply side of the health system. According to statistics released by the European Commission, public healthcare providers reached 79% connectivity in 2024 while private providers reached 59%, with 16 Member States improving their maturity scores during the same period. As more providers across Europe connect and begin sharing structured health data across care settings, laboratories face higher reporting intensity, larger interoperability workloads, and more exacting data quality expectations that mechanically accelerate adoption of integrated laboratory management platforms capable of meeting these demands consistently across multi-site and multi-system operating environments.

Europe Laboratory Information Management System Market Challenge

Data Availability Gaps and Compliance Escalation Slow Uniform Deployment

Persistent unevenness in health data availability and provider connectivity across European member states is creating a structurally complex and commercially meaningful implementation challenge for laboratory informatics providers seeking uniform regional deployment. Based on data from the European Commission, timely data availability reached 99% for identification data and 98% for personal information in 2024, but fell to only 26% for medical images and 55% for medical devices and implants, revealing significant gaps in the connected data landscape that make full-scale multi-source regulatory compliance software for labs implementation considerably more difficult in environments where laboratory workflows depend on complete and consistent upstream data feeds.

The compliance burden is simultaneously escalating as formal regulatory frameworks mature across the region. As indicated by authoritative sources at the European Commission, the European Health Data Space Regulation was officially published on 5 March 2025 and entered into force on 26 March 2025, introducing strict interoperability and security criteria alongside a pre- and post-market compliance framework for electronic health record systems across EU member states. For laboratory informatics vendors and their institutional clients, this regulatory development extends validation cycles, increases documentation requirements, and raises the cost of initial deployment, creating a more demanding entry environment that favours well-capitalised providers offering enterprise LIMS solutions with comprehensive compliance architecture built into their platform foundations.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Europe Laboratory Information Management System Market Trend

EHDS Implementation Is Establishing Interoperability as the Mandatory Operating Standard

A defining and commercially consequential structural trend is reshaping laboratory data infrastructure requirements across Europe as the European Health Data Space Regulation moves from legislative enactment toward phased technical implementation across all EU member states. Evidence drawn from public data released by the European Commission confirms that the EHDS Regulation entered into force on 26 March 2025, establishing a harmonised legal and technical framework for electronic health record systems that laboratories operating across European jurisdictions will be required to align with across a structured and time-bound implementation roadmap. This legislative momentum is directly accelerating digital transformation in laboratories across the continent by raising the minimum interoperability and data exchange standard that all connected laboratory reporting systems must meet to remain compliant within the evolving European health data governance architecture.

The commercial urgency of this trend is intensified by the specific inclusion of laboratory outputs within the EHDS implementation timeline. In line with findings from the European Commission, the exchange of medical images, laboratory results, and hospital discharge reports is required to be operational across all EU member states by March 2031, creating a defined and non-negotiable compliance deadline that is already influencing procurement decisions among forward-planning laboratory managers and health system administrators. Laboratories that invest in SaaS LIMS platforms with native interoperability capability are better positioned to manage this transition efficiently, reducing future migration costs and avoiding the operational disruption associated with late-stage system replacement under regulatory pressure.

Europe Laboratory Information Management System Market Opportunity

EU-Funded Digital Health Buildout Creates a Direct Commercial Runway

Substantial and actively disbursed EU public funding directed at European Health Data Space implementation is creating a commercially significant and well-timed opportunity for laboratory informatics providers positioned to capture procurement demand generated by publicly supported digital health infrastructure projects across the continent. As per official figures from the European Health and Digital Executive Agency, 68 EU4Health projects are already supporting EHDS implementation with total EU funding of EUR 105,206,061, including three key projects specifically preparing the technical groundwork for full-scale cross-border health data exchange. Each funded interoperability project generates downstream procurement requirements for sample lifecycle management solutions, structured data capture platforms, and compliant reporting software across the laboratory networks that these projects connect and serve.

The opportunity is expanding further as new funding commitments extend the EHDS implementation support infrastructure into 2026 and beyond. Data compiled from internationally recognised public authorities at the European Health and Digital Executive Agency confirms that two new contracts were signed under the 2025 EU4Health work programme on 9 April 2026 to support EHDS implementation and the application of future related regulations across member states. As public capital continues to flow into European health data infrastructure, laboratories and health networks across the continent gain stronger institutional capacity and clearer procurement mandates to invest in compliant, interoperable, and cloud adoption in lab informatics ready platforms, progressively expanding the addressable software deployment base across the European market through the forecast period.

Europe Laboratory Information Management System Market Country Analysis

By Country

- Germany

- UK

- Netherlands

- Switzerland

- France

- Italy

- Spain

- Rest of Europe

Germany holds the most commercially influential position within the Europe laboratory information management system market, commanding a 20% share that firmly establishes it as the leading national market in the regional landscape and the primary driver of demand concentration across the broader European LIMS industry. This leadership is underpinned by the country's active investment in healthcare digitalisation infrastructure, its well-developed pharmaceutical and biotechnology research ecosystem, and its formal regulatory modernisation agenda, all of which are generating sustained and institutionally driven demand for integrated laboratory informatics platforms that consistently exceeds the adoption pace of other European national markets. Within the country-level LIMS market analysis framework for the region, Germany represents the clearest and most commercially well-defined benchmark for platform adoption, procurement decision-making, and competitive vendor positioning across Europe.

At the broader regional level, Europe presents a commercially distinct and strategically compelling profile within the global LIMS market analysis landscape, shaped by the convergence of supranational regulatory reform through the EHDS, active EU-funded digital health infrastructure investment, and rising laboratory data governance expectations across a geographically diverse but institutionally coordinated group of national health systems. As Germany sustains its market leadership and neighbouring markets across Western, Northern, and Central Europe advance their own digitalisation programmes in response to EHDS implementation requirements, the European laboratory informatics market is consolidating its position as one of the most regulatory-reform-driven and institutionally well-supported LIMS adoption environments in the world heading into the next decade.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Europe Laboratory Information Management System Market Segmentation Analysis

By Product Type

- Clinical Operations LIMS

- Hospital Laboratory LIMS

- Physician Office Laboratory LIMS

- Routine Diagnostics Laboratory LIMS

- High-Throughput Testing LIMS

- Independent Laboratory LIMS

- Commercial Laboratory LIMS

- Reference Laboratory LIMS

- Multi-site Laboratory Network LIMS

- Public Health & Reporting LIMS

- Public Health Laboratory LIMS

- Surveillance-linked Laboratory LIMS

- Reference Network Laboratory LIMS

- Research & Repository LIMS

- Academic Research Laboratory LIMS

- Translational Research Laboratory LIMS

- Biobank & Repository LIMS

- Regulated QA/QC LIMS

- Pharmaceutical Laboratory LIMS

- Biotechnology Laboratory LIMS

- Food Testing Laboratory LIMS

- Environmental Testing Laboratory LIMS

- Forensic Laboratory LIMS

Clinical Operations LIMS holds the highest share within the product type category at 35%, reflecting sustained and institutionally embedded demand for platforms that govern routine testing activity, structured sample handling, and daily process documentation with operational precision across European laboratory environments. Laboratories across the continent are consistently selecting systems that improve internal coordination, reduce workflow inconsistency, and support structured execution across testing and record management functions in environments where compliance expectations and interoperability requirements are simultaneously rising. LIMS for pharmaceuticals industry and clinical diagnostics applications are both contributing meaningfully to the commercial depth of this segment, reinforcing its leadership position within the broader European product landscape.

Its sustained dominance signals a market-wide preference for systems that deliver active and embedded operational governance rather than supplementary digital capability. Clinical Operations LIMS is valued across European laboratory environments for its role in strengthening workflow discipline, supporting structured process execution, and enabling cleaner audit visibility across routine testing functions in both public health system and private research laboratory settings. As compliance obligations deepen and interoperability mandates approach their implementation deadlines, this segment is expected to retain its position as the primary product demand anchor throughout the forecast period.

By Workflow Type

- Accessioning-to-Result Management

- Sample Registration

- Sample Tracking

- Test Assignment

- Result Entry & Release

- Instrument-Integrated Workflow Management

- Analyzer Connectivity

- Automated Data Capture

- Bidirectional Instrument Communication

- Quality-Controlled Laboratory Workflow

- Quality Control Management

- Quality Assurance Workflow

- Exception & Deviation Handling

- Traceability & Repository Workflow

- Chain-of-Custody Tracking

- Storage & Retrieval Management

- Biobank Sample Lifecycle Tracking

- Interoperability & Reporting Workflow

- External System Connectivity

- Standards-based Data Exchange

- Regulatory & Public Health Reporting

The Interoperability and Reporting Workflow segment commands the highest share within the workflow type category at 30%, driven by growing laboratory demand for platforms that support structured data exchange, cleaner result communication, and more reliable reporting coordination across multi-system and multi-site health data environments throughout Europe. Laboratories are prioritising workflow platforms that reduce manual information handling, improve data movement accuracy across institutional boundaries, and meet the interoperability standards now being formally mandated under the EHDS regulatory framework, with laboratory data management and compliance requirements and cross-border reporting readiness both influencing platform selection decisions. Its lead position confirms that connected reporting capability and interoperability architecture are the primary workflow adoption drivers across the European LIMS market.

Its commercial importance is expected to deepen further as EHDS implementation milestones approach and institutional readiness requirements become more formally defined across member states. As laboratories invest in platforms that treat structured reporting and cross-system data exchange as core and non-negotiable architectural capabilities, this segment is expected to strengthen its position as the most strategically significant and commercially active workflow category within the Europe laboratory information management system market through the forecast period.

Various Market Players in Europe Laboratory Information Management System Market

The companies mentioned below are highly active in the Europe laboratory information management system market, occupying a considerable portion of the market and shaping industry progress.

- Autoscribe Informatics

- Clinisys

- Sapio Sciences

- LabWare

- LabVantage Solutions

- Thermo Fisher Scientific

- STARLIMS

- Agilent Technologies

- CloudLIMS

- QBench

- SciSure

- Dassault Systèmes BIOVIA

Market News & Updates

- STARLIMS, 2026:

STARLIMS released Technology Platform TP 12.6. The update introduced a new browser-based mobility framework that allows mobile apps to run directly in the device browser, with support for camera use, QR barcode scanning, offline mode, and additional enhancements for performance, stability, and security.

- LabWare, 2025:

LabWare expanded its SaaS LIMS portfolio with LabWare ASSURE, adding a new cloud-based option alongside LabWare QAQC and LabWare GROW. The release was positioned for microbiology, food safety, and quality workflows, with configurable deployment for laboratories adopting subscription-based informatics systems.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Europe Laboratory Information Management System Market Policies, Regulations, and Standards

- Europe Laboratory Information Management System Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Europe Laboratory Information Management System Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product Type

- Clinical Operations LIMS- Market Insights and Forecast 2022-2032, USD Million

- Hospital Laboratory LIMS- Market Insights and Forecast 2022-2032, USD Million

- Physician Office Laboratory LIMS- Market Insights and Forecast 2022-2032, USD Million

- Routine Diagnostics Laboratory LIMS- Market Insights and Forecast 2022-2032, USD Million

- High-Throughput Testing LIMS- Market Insights and Forecast 2022-2032, USD Million

- Independent Laboratory LIMS- Market Insights and Forecast 2022-2032, USD Million

- Commercial Laboratory LIMS- Market Insights and Forecast 2022-2032, USD Million

- Reference Laboratory LIMS- Market Insights and Forecast 2022-2032, USD Million

- Multi-site Laboratory Network LIMS- Market Insights and Forecast 2022-2032, USD Million

- Public Health & Reporting LIMS- Market Insights and Forecast 2022-2032, USD Million

- Public Health Laboratory LIMS- Market Insights and Forecast 2022-2032, USD Million

- Surveillance-linked Laboratory LIMS- Market Insights and Forecast 2022-2032, USD Million

- Reference Network Laboratory LIMS- Market Insights and Forecast 2022-2032, USD Million

- Research & Repository LIMS- Market Insights and Forecast 2022-2032, USD Million

- Academic Research Laboratory LIMS- Market Insights and Forecast 2022-2032, USD Million

- Translational Research Laboratory LIMS- Market Insights and Forecast 2022-2032, USD Million

- Biobank & Repository LIMS- Market Insights and Forecast 2022-2032, USD Million

- Regulated QA/QC LIMS- Market Insights and Forecast 2022-2032, USD Million

- Pharmaceutical Laboratory LIMS- Market Insights and Forecast 2022-2032, USD Million

- Biotechnology Laboratory LIMS- Market Insights and Forecast 2022-2032, USD Million

- Food Testing Laboratory LIMS- Market Insights and Forecast 2022-2032, USD Million

- Environmental Testing Laboratory LIMS- Market Insights and Forecast 2022-2032, USD Million

- Forensic Laboratory LIMS- Market Insights and Forecast 2022-2032, USD Million

- Clinical Operations LIMS- Market Insights and Forecast 2022-2032, USD Million

- By Workflow Type

- Accessioning-to-Result Management- Market Insights and Forecast 2022-2032, USD Million

- Sample Registration- Market Insights and Forecast 2022-2032, USD Million

- Sample Tracking- Market Insights and Forecast 2022-2032, USD Million

- Test Assignment- Market Insights and Forecast 2022-2032, USD Million

- Result Entry & Release- Market Insights and Forecast 2022-2032, USD Million

- Instrument-Integrated Workflow Management- Market Insights and Forecast 2022-2032, USD Million

- Analyzer Connectivity- Market Insights and Forecast 2022-2032, USD Million

- Automated Data Capture- Market Insights and Forecast 2022-2032, USD Million

- Bidirectional Instrument Communication- Market Insights and Forecast 2022-2032, USD Million

- Quality-Controlled Laboratory Workflow- Market Insights and Forecast 2022-2032, USD Million

- Quality Control Management- Market Insights and Forecast 2022-2032, USD Million

- Quality Assurance Workflow- Market Insights and Forecast 2022-2032, USD Million

- Exception & Deviation Handling- Market Insights and Forecast 2022-2032, USD Million

- Traceability & Repository Workflow- Market Insights and Forecast 2022-2032, USD Million

- Chain-of-Custody Tracking- Market Insights and Forecast 2022-2032, USD Million

- Storage & Retrieval Management- Market Insights and Forecast 2022-2032, USD Million

- Biobank Sample Lifecycle Tracking- Market Insights and Forecast 2022-2032, USD Million

- Interoperability & Reporting Workflow- Market Insights and Forecast 2022-2032, USD Million

- External System Connectivity- Market Insights and Forecast 2022-2032, USD Million

- Standards-based Data Exchange- Market Insights and Forecast 2022-2032, USD Million

- Regulatory & Public Health Reporting- Market Insights and Forecast 2022-2032, USD Million

- Accessioning-to-Result Management- Market Insights and Forecast 2022-2032, USD Million

- By Deployment Model

- Controlled Environment Deployment- Market Insights and Forecast 2022-2032, USD Million

- Scalable Digital Deployment- Market Insights and Forecast 2022-2032, USD Million

- Mixed Infrastructure Deployment- Market Insights and Forecast 2022-2032, USD Million

- By End-User Cluster

- Care Delivery Laboratories- Market Insights and Forecast 2022-2032, USD Million

- Hospital Laboratories- Market Insights and Forecast 2022-2032, USD Million

- Health-System Laboratories- Market Insights and Forecast 2022-2032, USD Million

- Physician Office Laboratories- Market Insights and Forecast 2022-2032, USD Million

- Community & Decentralized Testing Laboratories- Market Insights and Forecast 2022-2032, USD Million

- Commercial Testing Laboratories- Market Insights and Forecast 2022-2032, USD Million

- Independent Laboratories- Market Insights and Forecast 2022-2032, USD Million

- Commercial Laboratories- Market Insights and Forecast 2022-2032, USD Million

- Reference Laboratories- Market Insights and Forecast 2022-2032, USD Million

- Government & Public Health Laboratories- Market Insights and Forecast 2022-2032, USD Million

- Public Health Laboratories- Market Insights and Forecast 2022-2032, USD Million

- Central Reference Laboratories- Market Insights and Forecast 2022-2032, USD Million

- Disease Surveillance Laboratories- Market Insights and Forecast 2022-2032, USD Million

- Research & Translational Laboratories- Market Insights and Forecast 2022-2032, USD Million

- Academic Laboratories- Market Insights and Forecast 2022-2032, USD Million

- Research Institutes- Market Insights and Forecast 2022-2032, USD Million

- Biobanks- Market Insights and Forecast 2022-2032, USD Million

- Clinical Research Support Laboratories- Market Insights and Forecast 2022-2032, USD Million

- Regulated Scientific & Industrial Laboratories- Market Insights and Forecast 2022-2032, USD Million

- Pharmaceutical Laboratories- Market Insights and Forecast 2022-2032, USD Million

- Biotechnology Laboratories- Market Insights and Forecast 2022-2032, USD Million

- Food Safety Laboratories- Market Insights and Forecast 2022-2032, USD Million

- Environmental Laboratories- Market Insights and Forecast 2022-2032, USD Million

- Forensic Laboratories- Market Insights and Forecast 2022-2032, USD Million

- Care Delivery Laboratories- Market Insights and Forecast 2022-2032, USD Million

- By Purchase Model

- Perpetual License- Market Insights and Forecast 2022-2032, USD Million

- Subscription License- Market Insights and Forecast 2022-2032, USD Million

- Usage-Based Model- Market Insights and Forecast 2022-2032, USD Million

- Hybrid Commercial Model- Market Insights and Forecast 2022-2032, USD Million

- By Country

- Germany

- UK

- Netherlands

- Switzerland

- France

- Italy

- Spain

- Rest of Europe

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Product Type

- Market Size & Growth Outlook

- Germany Laboratory Information Management System Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- By Workflow Type- Market Insights and Forecast 2022-2032, USD Million

- By Deployment Model- Market Insights and Forecast 2022-2032, USD Million

- By End-User Cluster- Market Insights and Forecast 2022-2032, USD Million

- By Purchase Model- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- UK Laboratory Information Management System Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- By Workflow Type- Market Insights and Forecast 2022-2032, USD Million

- By Deployment Model- Market Insights and Forecast 2022-2032, USD Million

- By End-User Cluster- Market Insights and Forecast 2022-2032, USD Million

- By Purchase Model- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Netherlands Laboratory Information Management System Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- By Workflow Type- Market Insights and Forecast 2022-2032, USD Million

- By Deployment Model- Market Insights and Forecast 2022-2032, USD Million

- By End-User Cluster- Market Insights and Forecast 2022-2032, USD Million

- By Purchase Model- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Switzerland Laboratory Information Management System Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- By Workflow Type- Market Insights and Forecast 2022-2032, USD Million

- By Deployment Model- Market Insights and Forecast 2022-2032, USD Million

- By End-User Cluster- Market Insights and Forecast 2022-2032, USD Million

- By Purchase Model- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- France Laboratory Information Management System Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- By Workflow Type- Market Insights and Forecast 2022-2032, USD Million

- By Deployment Model- Market Insights and Forecast 2022-2032, USD Million

- By End-User Cluster- Market Insights and Forecast 2022-2032, USD Million

- By Purchase Model- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Italy Laboratory Information Management System Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- By Workflow Type- Market Insights and Forecast 2022-2032, USD Million

- By Deployment Model- Market Insights and Forecast 2022-2032, USD Million

- By End-User Cluster- Market Insights and Forecast 2022-2032, USD Million

- By Purchase Model- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Spain Laboratory Information Management System Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- By Workflow Type- Market Insights and Forecast 2022-2032, USD Million

- By Deployment Model- Market Insights and Forecast 2022-2032, USD Million

- By End-User Cluster- Market Insights and Forecast 2022-2032, USD Million

- By Purchase Model- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- LabWare

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- LabVantage Solutions

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Thermo Fisher Scientific

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- STARLIMS

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Agilent Technologies

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Autoscribe Informatics

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Clinisys

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Sapio Sciences

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- CloudLIMS

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- QBench

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- SciSure

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Dassault Systèmes BIOVIA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- LabWare

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Workflow Type |

|

| By Deployment Model |

|

| By End-User Cluster |

|

| By Purchase Model |

|

| By Country |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.