Europe Biofungicides Market Report: Trends, Growth and Forecast (2026-2032)

By Source (Microbial, Botanical), By Species (Bacillus, Trichoderma, Pseudomonas, Streptomyces, Saccharomyces, Aureobasidium, Coniothyrium, Others), By Form (Wettable Powder, Aqueous Solution, Granules, Powder, Liquid), By Mode of Application (Foliar Spray, Soil Treatment, Seed Treatment, Post-Harvest Treatment, Root Dipping, Drip Irrigation, Sprinkler Irrigation, Others), By Crop Type (Fruits and Vegetables, Cereals and Grains, Oilseeds and Pulses, Turf and Ornamentals, Plantation Crops, Nursery Crops, Others), By Country (Germany, The UK, France, Italy, Spain, The Netherlands, Rest of Europe) ... Read more

|

Major Players

|

Europe Biofungicides Market Statistics and Insights, 2026

- Market Size Statistics

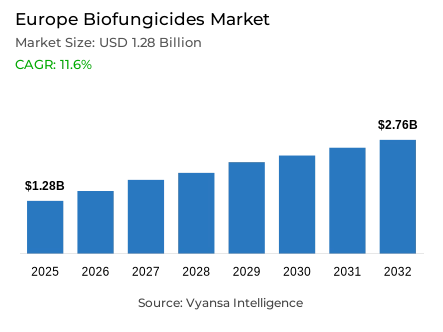

- Biofungicides market size in Europe was valued at USD 1.28 billion in 2025 and is estimated at USD 1.43 billion in 2026.

- The market size is expected to grow to USD 2.76 billion by 2032.

- Market to register a CAGR of around 11.6% during 2026-32.

- Source Shares

- Microbial grabbed market share of 80%.

- Competition

- More than 10 companies are actively engaged in producing biofungicides in Europe.

- Top 5 companies acquired around 35% of the market share.

- Lallemand Plant Care, CBC (Europe) Srl, Andermatt Group AG, Bayer AG (Bayer CropScience), BASF SE (BASF Agricultural Solutions) etc., are few of the top companies.

- Species

- Bacillus grabbed 35% of the market.

- Country

- France leads with a 30% share of the Europe market.

Europe Biofungicides Market Outlook

The Europe Biofungicides Market is valued at USD 1.28 Billion in 2025 and is projected to reach USD 2.76 Billion by 2032, growing at a CAGR of 11.6% during 2026-2032. Covering microbial and botanical biological fungicides, the market serves field crops, horticulture, vineyards, greenhouse production, and organic farming. The Europe Biofungicides Industry is moving from niche crop protection toward structured integration within sustainable plant disease management programs and export-oriented farming systems.

Policy support for biological plant protection is strengthening adoption conditions across the Europe Biofungicides Market. European Commission guidance states that micro-organisms used as biocontrol agents provide alternatives to chemical plant protection products and may be used in organic agriculture. This improves regulatory alignment for microbial biofungicides, supports Integrated Pest Management, and gives growers additional tools where residue management, soil health, and disease resistance control influence procurement decisions across the Europe Biofungicides Industry.

Crop protection demand remains anchored in high-value agricultural production and disease-sensitive specialty crops. In 2024, the European Commission reported that EU fresh fruit and vegetable production accounted for 13.4% of total EU agricultural production, with 63.8 million tonnes of vegetables, including pulses, and 40.8 million tonnes of fruits and nuts produced. The Europe Biofungicides Market gains from this base, while the Europe Biofungicides Industry expands foliar, seed treatment, and soil-applied disease-control solutions.

The 2026 trajectory is defined by regulatory simplification, supplier innovation, and broader commercialization of biological crop protection products. The Europe Biofungicides Market benefits as policymakers and industry groups push faster authorization for biocontrol, while suppliers position microbial actives for vineyards, cereals, sunflower, horticulture, and protected cultivation. The Europe Biofungicides Industry is therefore shifting toward stronger product pipelines, differentiated technical support, wider grower advisory capacity, field validation, partner-led commercialization, and expanded distribution access across EU farming systems across member states.

Europe Biofungicides Market Growth Driver

Sustainable Agriculture Expansion Is Strengthening Biological Fungicide Adoption

Organic farming expansion and residue-control expectations are increasing demand for microbial disease-management products across conventional and certified systems. The Europe Biofungicides Market gains stronger adoption visibility as growers use biological fungicides to reduce chemical dependency, support IPM programs, and protect disease-sensitive crops without weakening compliance with residue, soil-health, and sustainability requirements. This demand pattern is strongest in horticulture, vineyards, protected cultivation, and export-linked produce where preventive disease management affects buyer acceptance and export market access.

Figures published by IFOAM Organics Europe show that EU farmland under organic production reached 18.1 million hectares in 2024, while organic producers increased to 438,447. This operating base strengthens the Europe Biofungicides Industry by expanding the addressable acreage for biological plant protection products, increasing distributor interest in microbial portfolios planning, and supporting procurement of inputs aligned with organic standards, certification expectations, crop rotation systems, and low-residue crop protection across key European farming clusters.

Europe Biofungicides Market Challenge

Authorization Complexity is Slowing Commercial Scale-Up

Lengthy authorization pathways continue to restrict the speed at which biological crop protection products reach growers. The Europe Biofungicides Market faces slower commercialization when microbial and biocontrol products must navigate complex active-substance evaluation, national product authorization, label expansion, and renewal requirements. This affects supplier launch planning and inventory decisions, increases dossier costs, and delays farmer and distributor access to disease-control options as chemical active substances come under tighter scrutiny across EU crop systems.

IBMA stated in 2026 that biocontrol remains regulated under EU Plant Protection Products Regulation (EC) No 1107/2009 together with chemical pesticides, leaving farmers waiting up to 10 years for new products compared with 2-3 years elsewhere. This bottleneck constrains the Europe Biofungicides Industry by slowing product turnover, limiting crop-label coverage, reducing channel confidence, delaying field adoption, and weakening near-term market participation for smaller microbial innovators that depend on predictable approval timelines and harmonized EU market access.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Europe Biofungicides Market Trend

New Biological Platforms are Expanding Technical Differentiation

Next-generation microbial and non-conventional biological actives are reshaping innovation priorities beyond traditional bacterial and fungal formulations. The Europe Biofungicides Market is moving toward broader biological platforms that combine preventive disease control, resistance management, and sustainability positioning. This trend strengthens differentiation for suppliers that can validate efficacy under European field conditions, integrate biologicals with conventional crop programs, and support grower confidence through technical advisory networks and localized agronomy support services.

Syngenta reported in November 2025 that Amoéba’s Willaertia magna-based biocontrol active substance received EU approval in June 2025 after EFSA scientific assessment and a European Commission decision, with product-specific authorizations in progress. This development supports technology diversification, broadens the innovation pipeline for cereals and field crops, seed treatment opportunities, and signals stronger commercial interest in biological fungicide platforms that can address resistance pressure, expand crop coverage, improve formulation strategies, improve registration readiness, strengthen distributor uptake, and support crop-protection sustainability goals.

Europe Biofungicides Market Opportunity

Arable and Specialty Crops Create Wider Commercial Openings

Underpenetrated arable and specialty-crop applications create a scalable opportunity for suppliers that can move biological fungicides beyond organic niches. The Europe Biofungicides Market can capture stronger demand when products are positioned for cereals, oilseeds, vineyards, greenhouse vegetables, and fruit crops with clear protocols for timing, compatibility, storage, and field performance. Distribution partnerships and grower training remain central to converting technical interest into recurring procurement, technical service contracts, and retailer-aligned spray programs and broader crop-label expansion.

The European Environment Agency reported in 2025 that EU organic farming covered 17.4 million hectares, or 10.8% of utilised agricultural area in 2023, against a 25% policy target for 2030. This gap supports the Europe Biofungicides Industry by creating room for input suppliers, registrants, and advisory providers to expand biological portfolios as organic conversion, IPM compliance, public procurement, residue reduction, and low-residue production targets advance across fresh produce, vineyards, cereals, and protected cultivation.

Europe Biofungicides Market Country Analysis

By Country

- Germany

- The UK

- France

- Italy

- Spain

- The Netherlands

- Rest of Europe

France leads by country with 30% share, supported by a large organic farming production base, high-value crop systems, vineyards, horticulture, and active registration activity for biological crop protection products. French demand is shaped by residue-sensitive production, export requirements, disease pressure in specialty crops and vineyards, and policy-linked movement toward lower chemical dependency. Its position also supports supplier launch sequencing because France often anchors wider EU access strategies and distributor-led grower trials.

European Environment Agency country information published in 2025 shows that France had 2,767,828 hectares under or converting to organic cultivation and 61,163 organic farms, equal to 14.4% of all farms. This operating base strengthens demand for biological fungicides by expanding certified acreage, improving grower familiarity with biological inputs, and reinforcing the country’s role as a high-priority commercialization, field-validation, label-expansion, and technical advisory market for microbial disease-control products across vineyards, arable crops, and protected horticulture.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Europe Biofungicides Market Segmentation Analysis

By Source

- Microbial

- Botanical

Microbial biofungicides lead by source because bacterial and fungal actives align closely with IPM, organic production, residue reduction, and preventive disease-control programs. The Europe Biofungicides Market records Microbial at 80% share, supported by grower preference for living active strains and microbial metabolites that colonize roots, seeds, foliage, and plant surfaces under variable field pressure. Their use supports soil-borne and foliar disease control while allowing integration with biological crop protection schedules and resistance-management programs.

European Commission information on micro-organisms states that more than 60 micro-organisms are currently approved in the EU after scientific risk assessment confirmed safe use in plant protection products. This approval base strengthens microbial segment planning by widening available active-substance options, supporting product registration confidence, improving distributor portfolio depth, and enabling suppliers to target organic agriculture, protected cultivation, specialty crops, and conventional IPM programs with biological disease-management alternatives that match residue expectations and retailer-driven sustainability and certification standards.

By Species

- Bacillus

- Trichoderma

- Pseudomonas

- Streptomyces

- Saccharomyces

- Aureobasidium

- Coniothyrium

- Others

Bacillus leads by species because Bacillus-based biofungicides offer spore-forming stability, root and seed colonization, antifungal metabolite activity, and compatibility with seed treatment, in-furrow, and foliar programs across European cropping systems. The Europe Biofungicides Market records Bacillus at 35% share, reflecting its strong fit for preventive plant disease management programs, storage resilience, application flexibility, and scalable formulation across high-value crops, oilseeds, cereals, and protected cultivation systems where early disease suppression shapes yield protection and input planning.

BASF announced in 2025 that Integral Pro received registration in France for sunflower and would be available EU-wide from the 2026 sowing season; the product uses Bacillus amyloliquefaciens MBI600 and field trials across the EU from 2022 to 2024 showed a 3.5 dt/hectare average yield increase versus untreated seeds. This strengthens Bacillus positioning by linking biological activity to measurable crop-performance outcomes, improving seed-company adoption, distributor confidence, and agronomic justification for premium microbial formulations.

Various Market Players in Europe Biofungicides Market

The companies mentioned below are highly active in the Europe biofungicides market, occupying a considerable portion of the market and shaping industry progress.

- Lallemand Plant Care

- CBC (Europe) Srl

- Andermatt Group AG

- Bayer AG (Bayer CropScience)

- BASF SE (BASF Agricultural Solutions)

- Syngenta Crop Protection AG

- Certis Belchim B.V.

- Koppert B.V.

- De Sangosse S.A.S.(Agronaturalis Ltd)

- UPL Europe Ltd

- Eden Research plc

- Gowan Company L.L.C.

Market News & Updates

- Eden Research plc, 2026:

Eden Research announced a Mevalone label extension in France in January 2026. The approval expanded Mevalone use on grapes for downy and powdery mildew control, subject to local restrictions. The update adds France-specific vineyard biofungicide access in one of Europe’s priority disease-management crop categories.

- Eden Research plc, 2025:

Eden Research announced a Syngenta distribution agreement for ornamental crops in December 2025. The agreement targets the EU and UK ornamental crop market, covering cut flowers, pot plants, trees, shrubs, and bulbs under the Syngenta-labelled Evelta biofungicide. The update expands Europe-specific biological fungal-disease protection into ornamental crop channels.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Europe Biofungicides Market Policies, Regulations, and Standards

- Europe Biofungicides Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Europe Biofungicides Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Volume in Metric Tonnes

- Market Segmentation & Growth Outlook

- By Source

- Microbial- Market Insights and Forecast 2022-2032, USD Million

- Botanical- Market Insights and Forecast 2022-2032, USD Million

- By Species

- Bacillus- Market Insights and Forecast 2022-2032, USD Million

- Trichoderma- Market Insights and Forecast 2022-2032, USD Million

- Pseudomonas- Market Insights and Forecast 2022-2032, USD Million

- Streptomyces- Market Insights and Forecast 2022-2032, USD Million

- Saccharomyces- Market Insights and Forecast 2022-2032, USD Million

- Aureobasidium- Market Insights and Forecast 2022-2032, USD Million

- Coniothyrium- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Form

- Wettable Powder- Market Insights and Forecast 2022-2032, USD Million

- Aqueous Solution- Market Insights and Forecast 2022-2032, USD Million

- Granules- Market Insights and Forecast 2022-2032, USD Million

- Powder- Market Insights and Forecast 2022-2032, USD Million

- Liquid- Market Insights and Forecast 2022-2032, USD Million

- By Mode of Application

- Foliar Spray- Market Insights and Forecast 2022-2032, USD Million

- Soil Treatment- Market Insights and Forecast 2022-2032, USD Million

- Seed Treatment- Market Insights and Forecast 2022-2032, USD Million

- Post-Harvest Treatment- Market Insights and Forecast 2022-2032, USD Million

- Root Dipping- Market Insights and Forecast 2022-2032, USD Million

- Drip Irrigation- Market Insights and Forecast 2022-2032, USD Million

- Sprinkler Irrigation- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Crop Type

- Fruits and Vegetables- Market Insights and Forecast 2022-2032, USD Million

- Cereals and Grains- Market Insights and Forecast 2022-2032, USD Million

- Oilseeds and Pulses- Market Insights and Forecast 2022-2032, USD Million

- Turf and Ornamentals- Market Insights and Forecast 2022-2032, USD Million

- Plantation Crops- Market Insights and Forecast 2022-2032, USD Million

- Nursery Crops- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Country

- Germany

- The UK

- France

- Italy

- Spain

- The Netherlands

- Rest of Europe

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Source

- Market Size & Growth Outlook

- Germany Biofungicides Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Volume in Metric Tonnes

- Market Segmentation & Growth Outlook

- By Source- Market Insights and Forecast 2022-2032, USD Million

- By Species- Market Insights and Forecast 2022-2032, USD Million

- By Form- Market Insights and Forecast 2022-2032, USD Million

- By Mode of Application- Market Insights and Forecast 2022-2032, USD Million

- By Crop Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- The UK Biofungicides Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Volume in Metric Tonnes

- Market Segmentation & Growth Outlook

- By Source- Market Insights and Forecast 2022-2032, USD Million

- By Species- Market Insights and Forecast 2022-2032, USD Million

- By Form- Market Insights and Forecast 2022-2032, USD Million

- By Mode of Application- Market Insights and Forecast 2022-2032, USD Million

- By Crop Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- France Biofungicides Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Volume in Metric Tonnes

- Market Segmentation & Growth Outlook

- By Source- Market Insights and Forecast 2022-2032, USD Million

- By Species- Market Insights and Forecast 2022-2032, USD Million

- By Form- Market Insights and Forecast 2022-2032, USD Million

- By Mode of Application- Market Insights and Forecast 2022-2032, USD Million

- By Crop Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Italy Biofungicides Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Volume in Metric Tonnes

- Market Segmentation & Growth Outlook

- By Source- Market Insights and Forecast 2022-2032, USD Million

- By Species- Market Insights and Forecast 2022-2032, USD Million

- By Form- Market Insights and Forecast 2022-2032, USD Million

- By Mode of Application- Market Insights and Forecast 2022-2032, USD Million

- By Crop Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Spain Biofungicides Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Volume in Metric Tonnes

- Market Segmentation & Growth Outlook

- By Source- Market Insights and Forecast 2022-2032, USD Million

- By Species- Market Insights and Forecast 2022-2032, USD Million

- By Form- Market Insights and Forecast 2022-2032, USD Million

- By Mode of Application- Market Insights and Forecast 2022-2032, USD Million

- By Crop Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- The Netherlands Biofungicides Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Volume in Metric Tonnes

- Market Segmentation & Growth Outlook

- By Source- Market Insights and Forecast 2022-2032, USD Million

- By Species- Market Insights and Forecast 2022-2032, USD Million

- By Form- Market Insights and Forecast 2022-2032, USD Million

- By Mode of Application- Market Insights and Forecast 2022-2032, USD Million

- By Crop Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Bayer AG (Bayer CropScience)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- BASF SE (BASF Agricultural Solutions)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Syngenta Crop Protection AG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Certis Belchim B.V.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Koppert B.V.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Lallemand Plant Care

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- CBC (Europe) Srl

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Andermatt Group AG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- De Sangosse S.A.S.(Agronaturalis Ltd)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- UPL Europe Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Eden Research plc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Gowan Company L.L.C.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Bayer AG (Bayer CropScience)

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Source |

|

| By Species |

|

| By Form |

|

| By Mode of Application |

|

| By Crop Type |

|

| By Country |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.