Egypt Colour Cosmetics Market Report: Trends, Growth and Forecast (2026-2032)

By Category (Eye Make-Up (Eye Liner/Pencil, Eye Shadow, Mascara, Others), Facial Make-Up (BB/CC Creams, Blusher/Bronzer/Highlighter, Foundation/Concealer, Powder, Others), Lip Products (Lip Gloss, Lip Liner/Pencil, Lipstick, Others), Nail Products (Nail Polish, Nail Treatments/Strengthener, Polish Remover, Others), Colour Cosmetics Sets/Kits), By Price (Premium, Mass), By Gender (Men, Women, Unisex), By Packaging Type (Travel/Mini Size, Standard Size, Professional/Salon Size), By Form (Creams/Gels, Lotions, Sprays, Solid, Others), By Nature (Organic, Inorganic), By Sales Channel (Retail Offline, Retail Online) ... Read more

|

Major Players

|

Egypt Colour Cosmetics Market Statistics and Insights, 2026

- Market Size Statistics

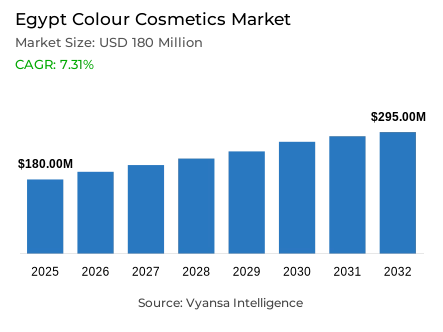

- Colour cosmetics market size in Egypt was estimated at USD 180 million in 2025.

- The market size is expected to grow to USD 295 million by 2032.

- Market to register a CAGR of around 7.31% during 2026-32.

- Category Shares

- Facial make-up grabbed market share of 35%.

- Competition

- More than 20 companies are actively engaged in producing colour cosmetics in Egypt.

- Top 5 companies acquired around 50% of the market share.

- Abu Shakra Trading Ltd, Univest Group, Azadea Group, L'Oréal Egypt LLC, Luna Cosmetics Co SAE etc., are few of the top companies.

- Sales Channel

- Retail offline grabbed 80% of the market.

Egypt Colour Cosmetics Market Outlook

The Egypt colour cosmetics market is experiencing a major shift as it faces economic difficulties and a changing trend of consumer spending. The market is estimated at USD 180 million in 2025, and USD 295 million in 2032, which is a compound annual growth rate (CAGR) of about 7.31% between 2026 and 2032. Despite the substantial price increases and currency devaluation causing a drop in volume in 2024, the category will recover due to the deep-rooted cultural connection to makeup and the sheer power of social media platforms like Instagram and Tik Tok on Generation Z.

The main drivers of growth are currently innovation and affordability. International executives, including L'Oréal, are weighing necessary price changes with advertising campaigns and new product launches, like the Maybelline Sunkisser blusher. At the same time, local producers, such as Luna Cosmetics, are becoming essential as they offer affordable alternatives that mirror the global trends. This increase in local production is particularly noteworthy because the lack of foreign currency limits access to imported high-end brands, thus pushing consumers to mass-market substitutes.

The demand of multifunctional and versatile products is likely to grow significantly during the forecast period. Egyptian consumers are increasingly demanding value in the form of multi-use products, including lipstick-blush sticks, which simplify the beauty process and reduce the total expenses. Lip products are expected to be the most active sub-category, and seasonal shades and simple colours are expected to be prioritized. In addition, an increasing population and increased exposure to beauty education through online tutorials will further drive experimentation and product knowledge.

sales channel is changing with the digital platforms threatening traditional retail. Although offline retail controlled 80% of the market through beauty experts and physical outlets, retail online is experiencing dynamic growth. Competitive pricing, exclusive deals, and home delivery are offered on online platforms by third-party services like Instashop and Talabat Mart. With the market moving towards 2032, the digital strategy and focus on mass-market affordability will be critical in maintaining the positive trend in the industry.

Egypt Colour Cosmetics Market Growth Driver

Influencer-Led Beauty Education Accelerating Trial Cycles and Repeat Make-Up Purchases

The trend fueling the increase of beauty education on online platforms is the shift of beauty education to online platforms, from 2026 to 2032. Makeup has been a prominent cultural phenomenon in Egypt, and Generation Z is closely associated with Instagram trends. The increased supply of "advice on how to use beauty products" contributes to product awareness, and makes wearing colour cosmetics a low-effort approach to staying trendy, regardless of the home's focus on essentials. Online beauty education has been a resounding success in reducing the barriers to trial and encouraging repurchasing through the use of engagement and trends.

This effect is supported by the level of digital penetration as of May 2025, Egypt has 116.79 million mobile subscriptions and 87.32 million data-and-voice mobile broadband subscriptions, as per the Ministry of Communications and Information Technology (MCIT) and the National Telecommunications Regulatory Authority (NTRA). Such connectivity enables brands to amplify trend cycles by partnering with creators and short-form educational content, which maintains engagement and purchase intent. The digital infrastructure supports advanced influencer-marketing plans, real-time sharing of trends, and community development that underpin category growth. The overlap of high cultural affinity to makeup and high mobile penetration provides good conditions to digitally-enabled beauty education, which leads to trial, loyalty, and long-term category growth.

Egypt Colour Cosmetics Market Challenge

Inflation and Currency Depreciation Eroding Discretionary Spend and Premium Availability

The major challenge that the category will face is affordability. Frequent price rises and severe post-devaluation corrections force households to prioritize necessities, pushing colour cosmetics to the category of non-necessities. Retailers and manufacturers face complicated trade-offs: continuing to raise prices to cover costs can destroy the customer base, but heavy discounting destroys margins, and sourcing imported high-quality products is becoming more difficult. This crisis of affordability puts structural limits on the growth of the category and on premium positioning strategies.

The continuation of this pressure is explained by official macro-economic data. In October 2025, the Central Bank of Egypt (CBE) registered an annual urban headline consumer price index (CPI) inflation rate of 12.5%. The official exchange rates of the CBE pegged the U.S. dollar at EGP 46.7848 (purchase) / 46.9183 (sale) on February 11, 2026, significantly increasing the prices of imported inputs and finished goods in local currency. The currency depreciation increases inflation, creating two-fold pressures on prices and profitability. The combination of high inflation and weak currency creates long-term affordability issues that limit discretionary purchasing power and limit the possibility of volume growth in the economically stressed consumer market in Egypt.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Egypt Colour Cosmetics Market Trend

Value-Engineered Beauty Routines Shifting Demand Toward Multi-Use and Smaller Pack Formats

The concept of value engineering in beauty routines is a definite market trend in 2026–32. Consumers are responding to economic pressure by buying smaller pack sizes, buying multi-use products, and increasing the time between purchases. As a result, the category shifts to a more deliberate experimentation, where the budget is a factor and practicality and versatility are as important as colour and finish. Value optimisation, therefore, emerges as the dominant procurement model, which essentially transforms the consumption behaviour and product-selection standards among demographic groups.

This behaviour is supported by the wider pricing environment. According to the CBE site, headline inflation stands at 11.9% and core inflation at 11.2% on February 11, 2026, which continues to maintain austere day-to-day budgets and increases the sensitivity of shoppers to promotions and perceived value. In this case, products that provide several advantages in one product are the most compatible with the do more with less attitude. The value-first trend is a strategic change in the aspirational buying to functional optimisation, which requires brands to prove their utility, versatility, and affordability. This creates opportunities of multipurpose formulations, smaller, more convenient formats, and open value communication that can sustain cost-conscious beauty routines.

Egypt Colour Cosmetics Market Opportunity

Local Mass Brands Scaling Faster as Import Constraints Tighten and Value Demand Deepens

The primary opportunity lies in the expansion of domestic, mass-market brands that offer trend-driven products at price points accessible to Egyptian consumers. Limitation of foreign currency restricts the supply of imported high-end products and consumers are seeking cheaper local products. Therefore, domestic producers have great opportunities to imitate international designs, perfect recipes, and maintain shelf space without the same exposure to imports, thus stealing market share of international competitors with the same limitations.

Local businesses are significantly advantaged by scale and reach. The United Nations Population Fund (UNFPA) estimates that the total population of Egypt in 2025 was 118.4 million, which gives local manufacturers a large domestic market to develop volume and brand recognition effectively. Low-cost education and community building: according to MCIT/NTRA data, mobile-internet users constituted 74.77% of mobile subscriptions by May 2025, enabling affordable digital marketing and direct consumer interaction. The local brand opportunity is enhanced by the size of the population, digital infrastructure, and import restrictions. Local manufacturers with trend sensitivity, stable quality and low prices are well placed to gain growing market share by localised manufacturing, effective sales channel and digitally-enabled brand development in the economically limited but demographically vast consumer base in Egypt.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Egypt Colour Cosmetics Market Segmentation Analysis

By Category

- Eye Make-Up

- Eye Liner/Pencil

- Eye Shadow

- Mascara

- Others

- Facial Make-Up

- BB/CC Creams

- Blusher/Bronzer/Highlighter

- Foundation/Concealer

- Powder

- Others

- Lip Products

- Lip Gloss

- Lip Liner/Pencil

- Lipstick

- Others

- Nail Products

- Nail Polish

- Nail Treatments/Strengthener

- Polish Remover

- Others

- Colour Cosmetics Sets/Kits

The segment has the highest share around the category in the Egypt colour cosmetics market, where Facial Make-Up grabbed a market share of 35%. This segment serves as the essential foundation for all beauty routines, leading to high usage frequency across different consumer groups. Current trends in contouring, highlighting, and the desire for flawless coverage have solidified its leading position. As consumers prioritize base products that offer durability and skin-enhancing features, facial makeup remains the largest contributor to the overall category value.

Innovation in this segment is increasingly focused on versatility and affordability to combat economic pressures. Brands are introducing formulations that cater to specific Egyptian skin needs while maintaining competitive pricing. Although economic instability has forced some consumers to buy smaller sizes, the "base" nature of facial makeup ensures it remains a non-discretionary part of the makeup kit. This 35% share is expected to hold steady as local brands innovate with high-quality, budget-friendly foundations and concealers.

By Sales Channel

- Retail Offline

- Retail Online

The segment has the highest share around the Sales Channel is Retail Offline, which grabbed 80% of the market. Beauty specialists and traditional brick-and-mortar stores remain the dominant destinations for Egyptian shoppers, who value the ability to test products and receive in-person advice. This offline dominance is supported by the extensive sales channel networks of major players like L'Oréal and Luna Cosmetics, ensuring that makeup remains physically accessible across various regions in Egypt, even as economic conditions fluctuate.

While offline retail maintains the majority share, it is increasingly being influenced by digital trends. Traditional stores are now integrating online strategies to compete with the rising popularity of retail online and third-party delivery apps. The 80% market share highlights that for the majority of Egyptian consumers, the physical shopping experience remains the primary way to purchase cosmetics. However, the convenience of the offline channel is being enhanced by service providers who bridge the gap between physical shelves and home delivery.

List of Companies Covered in Egypt Colour Cosmetics Market

The companies listed below are highly influential in the Egypt colour cosmetics market, with a significant market share and a strong impact on industry developments.

- Abu Shakra Trading Ltd

- Univest Group

- Azadea Group

- L'Oréal Egypt LLC

- Luna Cosmetics Co SAE

- Misr Cosmetics Co SAE

- Coty Inc

- MAC for Promoting Commercials Business

- Avon Cosmetics Egypt

- Flormar Co

Competitive Landscape

Egypt colour cosmetics market is characterised by volume decline amid price inflation exceeding 40%, intensifying competition around affordability and distribution. L’Oréal Egypt retains leadership through a broad brand portfolio spanning Maybelline to Yves Saint Laurent, leveraging strong retail reach, influencer partnerships, and CSR initiatives, though facing pricing pressures and availability constraints. Local player Luna Cosmetics competes aggressively on price and promotions, while Cosnova, with Catrice and Essence, is the most dynamic challenger, capitalising on affordable positioning and wide distribution. Beauty specialists remain the core channel, but e-commerce and third-party delivery platforms are reshaping access and price transparency. Key differentiation opportunities lie in mass positioning, multifunctional products, localised innovation, and digitally driven engagement targeting Gen Z consumers.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. Egypt Colour Cosmetics Market Policies, Regulations, and Standards

4. Egypt Colour Cosmetics Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. Egypt Colour Cosmetics Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in USD Million

5.2. Market Segmentation & Growth Outlook

5.2.1.By Category

5.2.1.1. Eye Make-Up- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.1. Eye Liner/Pencil- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.2. Eye Shadow- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.3. Mascara- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.4. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Facial Make-Up- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.1. BB/CC Creams- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.2. Blusher/Bronzer/Highlighter- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.3. Foundation/Concealer- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.4. Powder- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.5. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3. Lip Products- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.1. Lip Gloss- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.2. Lip Liner/Pencil- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.3. Lipstick- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.4. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.1.4. Nail Products- Market Insights and Forecast 2022-2032, USD Million

5.2.1.4.1. Nail Polish- Market Insights and Forecast 2022-2032, USD Million

5.2.1.4.2. Nail Treatments/Strengthener- Market Insights and Forecast 2022-2032, USD Million

5.2.1.4.3. Polish Remover- Market Insights and Forecast 2022-2032, USD Million

5.2.1.4.4. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.1.5. Colour Cosmetics Sets/Kits- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Price

5.2.2.1. Premium- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Mass- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Gender

5.2.3.1. Men- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Women- Market Insights and Forecast 2022-2032, USD Million

5.2.3.3. Unisex- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Packaging Type

5.2.4.1. Travel/Mini Size - Market Insights and Forecast 2022-2032, USD Million

5.2.4.2. Standard Size - Market Insights and Forecast 2022-2032, USD Million

5.2.4.3. Professional/Salon Size- Market Insights and Forecast 2022-2032, USD Million

5.2.5.By Form

5.2.5.1. Creams/Gels- Market Insights and Forecast 2022-2032, USD Million

5.2.5.2. Lotions- Market Insights and Forecast 2022-2032, USD Million

5.2.5.3. Sprays- Market Insights and Forecast 2022-2032, USD Million

5.2.5.4. Solid- Market Insights and Forecast 2022-2032, USD Million

5.2.5.5. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.6.By Nature

5.2.6.1. Organic- Market Insights and Forecast 2022-2032, USD Million

5.2.6.2. Inorganic- Market Insights and Forecast 2022-2032, USD Million

5.2.7.By Sales Channel

5.2.7.1. Retail Offline- Market Insights and Forecast 2022-2032, USD Million

5.2.7.2. Retail Online- Market Insights and Forecast 2022-2032, USD Million

5.2.8.By Competitors

5.2.8.1. Competition Characteristics

5.2.8.2. Market Share & Analysis

6. Egypt Eye Make-Up Colour Cosmetics Market Statistics, 2022-2032

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in USD Million

6.2. Market Segmentation & Growth Outlook

6.2.1.By Category- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Price- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By Gender- Market Insights and Forecast 2022-2032, USD Million

6.2.4.By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

6.2.5.By Form- Market Insights and Forecast 2022-2032, USD Million

6.2.6.By Nature- Market Insights and Forecast 2022-2032, USD Million

6.2.7.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

7. Egypt Facial Make-Up Colour Cosmetics Market Statistics, 2022-2032

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in USD Million

7.2. Market Segmentation & Growth Outlook

7.2.1.By Category- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Price- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By Gender- Market Insights and Forecast 2022-2032, USD Million

7.2.4.By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

7.2.5.By Form- Market Insights and Forecast 2022-2032, USD Million

7.2.6.By Nature- Market Insights and Forecast 2022-2032, USD Million

7.2.7.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

8. Egypt Lip Products Colour Cosmetics Market Statistics, 2022-2032

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in USD Million

8.2. Market Segmentation & Growth Outlook

8.2.1.By Category- Market Insights and Forecast 2022-2032, USD Million

8.2.2.By Price- Market Insights and Forecast 2022-2032, USD Million

8.2.3.By Gender- Market Insights and Forecast 2022-2032, USD Million

8.2.4.By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

8.2.5.By Form- Market Insights and Forecast 2022-2032, USD Million

8.2.6.By Nature- Market Insights and Forecast 2022-2032, USD Million

8.2.7.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

9. Egypt Nail Products Colour Cosmetics Market Statistics, 2022-2032

9.1. Market Size & Growth Outlook

9.1.1.By Revenues in USD Million

9.2. Market Segmentation & Growth Outlook

9.2.1.By Category- Market Insights and Forecast 2022-2032, USD Million

9.2.2.By Price- Market Insights and Forecast 2022-2032, USD Million

9.2.3.By Gender- Market Insights and Forecast 2022-2032, USD Million

9.2.4.By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

9.2.5.By Form- Market Insights and Forecast 2022-2032, USD Million

9.2.6.By Nature- Market Insights and Forecast 2022-2032, USD Million

9.2.7.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

10. Egypt Colour Cosmetics Sets/Kits Colour Cosmetics Market Statistics, 2022-2032

10.1. Market Size & Growth Outlook

10.1.1. By Revenues in USD Million

10.2. Market Segmentation & Growth Outlook

10.2.1. By Price- Market Insights and Forecast 2022-2032, USD Million

10.2.2. By Gender- Market Insights and Forecast 2022-2032, USD Million

10.2.3. By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

10.2.4. By Form- Market Insights and Forecast 2022-2032, USD Million

10.2.5. By Nature- Market Insights and Forecast 2022-2032, USD Million

10.2.6. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

11. Competitive Outlook

11.1. Company Profiles

11.1.1. L'Oréal Egypt LLC

11.1.1.1. Business Description

11.1.1.2. Product Portfolio

11.1.1.3. Collaborations & Alliances

11.1.1.4. Recent Developments

11.1.1.5. Financial Details

11.1.1.6. Others

11.1.2. Luna Cosmetics Co SAE

11.1.2.1. Business Description

11.1.2.2. Product Portfolio

11.1.2.3. Collaborations & Alliances

11.1.2.4. Recent Developments

11.1.2.5. Financial Details

11.1.2.6. Others

11.1.3. Misr Cosmetics Co SAE

11.1.3.1. Business Description

11.1.3.2. Product Portfolio

11.1.3.3. Collaborations & Alliances

11.1.3.4. Recent Developments

11.1.3.5. Financial Details

11.1.3.6. Others

11.1.4. Coty Inc

11.1.4.1. Business Description

11.1.4.2. Product Portfolio

11.1.4.3. Collaborations & Alliances

11.1.4.4. Recent Developments

11.1.4.5. Financial Details

11.1.4.6. Others

11.1.5. MAC for Promoting Commercials Business

11.1.5.1. Business Description

11.1.5.2. Product Portfolio

11.1.5.3. Collaborations & Alliances

11.1.5.4. Recent Developments

11.1.5.5. Financial Details

11.1.5.6. Others

11.1.6. Abu Shakra Trading Ltd

11.1.6.1. Business Description

11.1.6.2. Product Portfolio

11.1.6.3. Collaborations & Alliances

11.1.6.4. Recent Developments

11.1.6.5. Financial Details

11.1.6.6. Others

11.1.7. Univest Group

11.1.7.1. Business Description

11.1.7.2. Product Portfolio

11.1.7.3. Collaborations & Alliances

11.1.7.4. Recent Developments

11.1.7.5. Financial Details

11.1.7.6. Others

11.1.8. Azadea Group

11.1.8.1. Business Description

11.1.8.2. Product Portfolio

11.1.8.3. Collaborations & Alliances

11.1.8.4. Recent Developments

11.1.8.5. Financial Details

11.1.8.6. Others

11.1.9. Avon Cosmetics Egypt

11.1.9.1. Business Description

11.1.9.2. Product Portfolio

11.1.9.3. Collaborations & Alliances

11.1.9.4. Recent Developments

11.1.9.5. Financial Details

11.1.9.6. Others

11.1.10. Flormar Co

11.1.10.1.Business Description

11.1.10.2.Product Portfolio

11.1.10.3.Collaborations & Alliances

11.1.10.4.Recent Developments

11.1.10.5.Financial Details

11.1.10.6.Others

12. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Category |

|

| By Price |

|

| By Gender |

|

| By Packaging Type |

|

| By Form |

|

| By Nature |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.