China Childrenswear Market Report: Trends, Growth and Forecast (2026-2032)

By Product Type (Apparel (Baby and Toddler Wear, Boys Apparel, Girls Apparel), Footwear (Boys Footwear, Girls Footwear), Accessories (Boys Accessories, Girls Accessories), Others), By Age Group (Infant/Toddler (Below 2 years), Kids/Children (2 - 14 years)), By Price Category (Mass, Premium), By Sales Channel (Retail Offline, Retail Online) ... Read more

|

Major Players

|

China Childrenswear Market Statistics and Insights, 2026

- Market Size Statistics

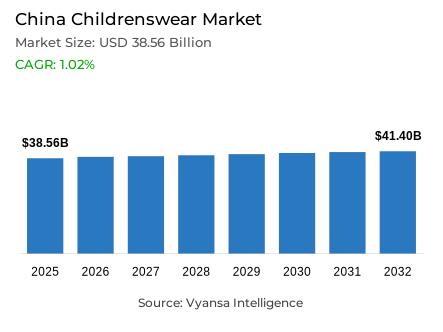

- Childrenswear in China is estimated at USD 38.56 billion in 2025.

- The market size is expected to grow to USD 41.4 billion by 2032.

- Market to register a cagr of around 1.02% during 2026-32.

- Product Type Shares

- Apparel grabbed market share of 75%.

- Competition

- Childrenswear in China is currently being catered to by more than 20 companies.

- Top 5 companies acquired around 10% of the market share.

- Nike (China) Inc; 361 Degrees International Ltd; Roly China Group Co Ltd; Semir Group Co Ltd; Anta (China) Co Ltd etc., are few of the top companies.

- Sales Channel

- Retail offline grabbed 60% of the market.

China Childrenswear Market Outlook

China Childrenswear market was worth around USD 38.56 billion in 2025 it is expected to reach around USD 41.4 billion by 2032, registering a CAGR of 1.02% between 2026 and 2032. Though the recovery in the aftermath of the pandemic has been sluggish, with deteriorating end-user sentiment, childrenswear continues to perform better amongst various apparel types. This is due to its necessity factor, coupled with an acceleration in the purchase of quality offerings. Despite weakening demands due to reduced birth rates and spending, premiumization has been robust because of the focus on comfort, safety, and fabrics.

The market is very fragmented, and the top five companies together hold only about 10% market value share. Domestic players such as Balabala are catering to the shift by introducing functional and outdoor-inspired ranges, and sportswear brands like 361 Degrees Kids and Xtep Kids are also increasing their foothold. Their approach to flexibility and quality has been appealing to younger end user who look for resilient and trendy enough ranges in order to engage in outdoor and school functions. The apparel category leads the total market sales of childrenwear.

The Retail offline occupies around 60% of share, thanks to a strong following of departmental and specialized retail outlets. Still, retail online is gaining popularity because of convenience and a wider range of available goods. Online brands utilize online marketing and collaborations with influencers to target fashion-savvyend user. It further expands a competitive setting.

The key drivers for the market will be the rising acceptance of outdoor wear and Chinoiserie-type children’s wear, which will be the result of cultural pride and sophistication. Safety norms, especially for babies and toddlers, will also remain at the top of the list, which will seeend user opting for quality and certified fabrics. All these factors will combine to ensure the China children’s wear market develops steadily.

China Childrenswear Market Growth DriverGrowing Demand for Functional Outdoor Children’s Wear: The functional outdoor

China increasing participation in outdoor and recreational activities is acting as a key driver for rising demand for functional and durable childrenswear. End user have become very active as a whole, taking part in outdoor activities such as trekking, camping, and biking. This has led to an increase in the need for high-performance clothing. The Chinese National Garment Association states that the growth of outdoor childrenwear sales rose by over 14% in 2024, registering the sharpest growth within the kids’ wear genre. End user have become keen to acquire clothing that provides protection from UV rays, waterproofing, ventilation, and temperature regulation capabilities, especially in northern China where the average temperature during winters dips below -10°C.

The likes of The North Face Kids, Anta, and Balabala are now extending the autumn/winter category to encompass resilient and water-resistant garments to cater to year-round needs. The increased focus on comfort, safety, and utility is a reflection of the shifting lifestyle observed within Chinese families, as functional outdoor kids' wear has now emerged as a major driver within the market.

China Childrenswear Market ChallengeFalling Birth Rate Reduces Baby and Toddler Wear Demand

The China childrenwear market is increasingly shaped by a persistently declining birth rate, which is constraining the size of the core end-user base and exerting downward pressure on long-term demand growth. An analysis of the data provided by the National Bureau of Statistics of China indicates that the birth rate in the Chinese market declined to 9.02 million in 2023, showing a 6% year-over-year drop to register the lowest rate in over seven decades. As such, the continuously declining birth rate in the Chinese market has resulted in the reduced demand of babies and toddlers clothing.

While the actual spending amount of those having fewer offspring is higher, the number of end users is still shrinking. As end user brands in the 0-3 years age group are highly dependent on the retailers in this age category, now those retailers are moving towards marketing garments for school-going children. Even as the effect of premiumization is alleviating the concern for low fertility, this remains an issue that leads brands to focus on garments for pre-teen children.

Unlock Market Intelligence

Explore the market potential with our data-driven report

China Childrenswear Market TrendChinoiserie Style Kids Wear Popularity

The children wear market in China is experiencing a renewed cultural orientation, with Guochao-inspired apparel increasingly gaining acceptance among end users. End user are now showing interest in Chinoiserie patterns that combine elements of traditional Chinese designs and contemporary cuts. According to JD.com’s 2024 Fashion Report, Chinoiserie-type childrenswear and Hanfu-style clothing experienced a sales increase of 18% from last year, peaking during Lunar New Year and Mid-Autumn Festivals.

Balabala, Mini Peace, among other giants, launched lines of traditional Suzhou embroidery, Han elements, and Tang-cut clothing. Moreover, interaction levels exceeded 5 million views in relation to traditional kidswear in the beginning of 2024, as hosted by Xiaohongshu, indicating significant interest among end users. The current revival of culture and aestheticism indicates how domestic pride, together with innovations in fashion, is impacting end user behavior among contemporary families within China.

China Childrenswear Market OpportunityIncreasing Demand for Safe and Premium Quality Fabrics for Children's Wear

Growing emphasis on safety standards, product quality, and wearing comfort is creating a significant market opportunity within the childrenswear segment. Middle-class end user in urban areas are shifting towards clothing made of Class A-certified materials, which are in accordance with the China GB 31701 safety standard for infants textile products. The China Textile market Federation reported a surge of over 11% in the demand for organic cotton and non-toxic dyes in 2024. The growing demand is a result of increased interest in the use of safe and comfortable fabric materials.

Leading brands like PatPat and Balabala have already introduced OEKO-TEX® and GOTS certification in their materials this is expected to enhance the authenticity of their products. However, over the forecast period, with an increased focus on breathable, high-quality materials, innovations are expected in the market, leading to premiumization, with brands being differentiated based on higher standards of safety and sustainability.

Unlock Market Intelligence

Explore the market potential with our data-driven report

China Childrenswear Market Segmentation Analysis

By Product Type

- Apparel

- Baby and Toddler Wear

- Boys Apparel

- Girls Apparel

- Footwear

- Boys Footwear

- Girls Footwear

- Accessories

- Boys Accessories

- Girls Accessories

- Others

The segment with highest market share under product is apparel, as it constitutes the largest market share as far as market revenue is concerned. The major reason behind such high market dominance is the fact that garments are a basic need of kids, as they have a replacement cycle because kids are constantly growing. Even though the birth rate is declining, garments have a high demand asend user are concerned about comfort, quality, and safety. Moreover, the clothing category is continuously upgraded with the emergence of newer styles and innovations that fit the lifestyle changes.

However, the increasing interest in adventure and outdoor pursuits has increased the demand for sportswear and utility children clothing. At the same time, the developing fashion trend of Chinoiserie depicts the rising cultural sentiments of the people and is expected to retain the apparel category’s dominant market position in the forecast period.

By Sales Channel

- Retail Offline

- Retail Online

The segment with highest market share under sales channel is retail offline, taking a 60% market share. The retail offline channels have continued to lead, given that manyend user want to assess the quality, feel, and guise of the clothes before buying, most especially for kids. The department store, specialty store, and shopping mall have continued to be important platforms.

Retail offline has also been adapting to offering an interesting experience to end user by providing special collections and appealing to family shoppers. Big brands such as Balabala and Mini Peace have huge store outlets, thus increasing convenience and awareness. Though the growth rate of online platforms is very high, offline retail ensures authentic quality and thus secures dominance over the China Childrenswear Market.

List of Companies Covered in China Childrenswear Market

The companies listed below are highly influential in the China childrenswear market, with a significant market share and a strong impact on industry developments.

- Nike (China) Inc

- 361 Degrees International Ltd

- Roly China Group Co Ltd

- Semir Group Co Ltd

- Anta (China) Co Ltd

- Uniqlo China Co Ltd

- adidas Sports (China) Ltd

- Xtep International Holdings Ltd

- Inditex Group China

- Dongguan Pepco Clothes Industrial Co Ltd

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. China Childrenswear Market Policies, Regulations, and Standards

4. China Childrenswear Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. China Childrenswear Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in US$ Million

5.2. Market Segmentation & Growth Outlook

5.2.1.By Product Type

5.2.1.1. Apparel- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.1. Baby and Toddler Wear- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.2. Boys Apparel- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.3. Girls Apparel- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Footwear- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.1. Boys Footwear- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.2. Girls Footwear- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3. Accessories- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.1. Boys Accessories- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.2. Girls Accessories- Market Insights and Forecast 2022-2032, USD Million

5.2.1.4. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Age Group

5.2.2.1. Infant/Toddler (Below 2 years)- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Kids/Children (2 - 14 years)- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Price Category

5.2.3.1. Mass- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Premium- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Sales Channel

5.2.4.1. Retail Offline- Market Insights and Forecast 2022-2032, USD Million

5.2.4.2. Retail Online- Market Insights and Forecast 2022-2032, USD Million

5.2.5.By Competitors

5.2.5.1. Competition Characteristics

5.2.5.2. Market Share & Analysis

6. China Apparel Childrenswear Market Statistics, 2022-2032

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in US$ Million

6.2. Market Segmentation & Growth Outlook

6.2.1.By Age Group- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Price Category- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

7. China Footwear Childrenswear Market Statistics, 2022-2032

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in US$ Million

7.2. Market Segmentation & Growth Outlook

7.2.1.By Age Group- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Price Category- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

8. China Accessories Childrenswear Market Statistics, 2022-2032

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in US$ Million

8.2. Market Segmentation & Growth Outlook

8.2.1.By Age Group- Market Insights and Forecast 2022-2032, USD Million

8.2.2.By Price Category- Market Insights and Forecast 2022-2032, USD Million

8.2.3.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

9. Competitive Outlook

9.1. Company Profiles

9.1.1.Semir Group Co Ltd

9.1.1.1. Business Description

9.1.1.2. Product Portfolio

9.1.1.3. Collaborations & Alliances

9.1.1.4. Recent Developments

9.1.1.5. Financial Details

9.1.1.6. Others

9.1.2.Anta (China) Co Ltd

9.1.2.1. Business Description

9.1.2.2. Product Portfolio

9.1.2.3. Collaborations & Alliances

9.1.2.4. Recent Developments

9.1.2.5. Financial Details

9.1.2.6. Others

9.1.3.Uniqlo China Co Ltd

9.1.3.1. Business Description

9.1.3.2. Product Portfolio

9.1.3.3. Collaborations & Alliances

9.1.3.4. Recent Developments

9.1.3.5. Financial Details

9.1.3.6. Others

9.1.4.adidas Sports (China) Ltd

9.1.4.1. Business Description

9.1.4.2. Product Portfolio

9.1.4.3. Collaborations & Alliances

9.1.4.4. Recent Developments

9.1.4.5. Financial Details

9.1.4.6. Others

9.1.5.Xtep International Holdings Ltd

9.1.5.1. Business Description

9.1.5.2. Product Portfolio

9.1.5.3. Collaborations & Alliances

9.1.5.4. Recent Developments

9.1.5.5. Financial Details

9.1.5.6. Others

9.1.6.Nike (China) Inc

9.1.6.1. Business Description

9.1.6.2. Product Portfolio

9.1.6.3. Collaborations & Alliances

9.1.6.4. Recent Developments

9.1.6.5. Financial Details

9.1.6.6. Others

9.1.7.361 Degrees International Ltd

9.1.7.1. Business Description

9.1.7.2. Product Portfolio

9.1.7.3. Collaborations & Alliances

9.1.7.4. Recent Developments

9.1.7.5. Financial Details

9.1.7.6. Others

9.1.8.Roly China Group Co Ltd

9.1.8.1. Business Description

9.1.8.2. Product Portfolio

9.1.8.3. Collaborations & Alliances

9.1.8.4. Recent Developments

9.1.8.5. Financial Details

9.1.8.6. Others

9.1.9.Inditex Group China

9.1.9.1. Business Description

9.1.9.2. Product Portfolio

9.1.9.3. Collaborations & Alliances

9.1.9.4. Recent Developments

9.1.9.5. Financial Details

9.1.9.6. Others

9.1.10. Dongguan Pepco Clothes Industrial Co Ltd

9.1.10.1. Business Description

9.1.10.2. Product Portfolio

9.1.10.3. Collaborations & Alliances

9.1.10.4. Recent Developments

9.1.10.5. Financial Details

9.1.10.6. Others

10. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Age Group |

|

| By Price Category |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.