Chile Room Air Conditioners Market Report: Trends, Growth and Forecast (2026-2032)

By Product Type (Split Air Conditioners (Up to 9,000 BTU/h, 9,001-12,000 BTU/h, 12,001-18,000 BTU/h, 18,001-24,000 BTU/h, Above 24,000 BTU/h), Window Air Conditioners (Up to 9,000 BTU/h, 9,001-12,000 BTU/h, 12,001-18,000 BTU/h, 18,001-24,000 BTU/h, Above 24,000 BTU/h), Others), By Technology (Inverter, Non-Inverter), By Price (Up to USD 300, USD 301 to USD 600, USD 601 to USD 1,000, Above USD 1,000), By End User (Residential (Individual Households, Apartments/Condominiums, Vacation/Secondary Homes), Commercial (Offices, Retail Stores/Showrooms, Hospitality, Healthcare Facilities, Educational Institutions, Small Commercial Establishments, Others)), By Sales Channel (Retail Online (Brand-Owned Websites/D2C, E-Commerce Marketplaces), Retail Offline (Exclusive Brand Stores, Multi-Brand Electronics & Appliance Stores, Specialty Stores, Hypermarkets/Supermarkets, Home Improvement Stores, Dealer/Distributor Network, Direct Sales/Institutional Sales, Local Independent Retailers)), By Refrigerant Type (R-32, R-410A, R-290, R-454B, Others), By Connectivity (Smart/Connected, Conventional/Non-Smart), By Energy Efficiency (1 Star, 2 Star, 3 Star, 4 Star, 5 Star) ... Read more

|

Major Players

|

Chile Room Air Conditioners Market Statistics and Insights, 2026

- Market Size Statistics

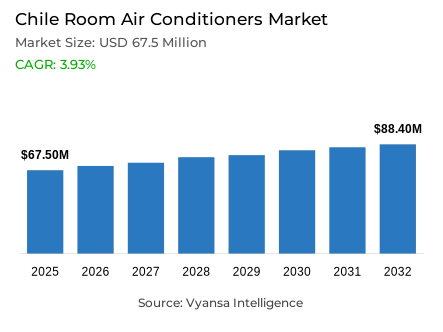

- Room air conditioners market size in Chile was valued at USD 67.5 million in 2025 and is estimated at USD 69.8 million in 2026.

- The market size is expected to grow to USD 88.4 million by 2032.

- Market to register a CAGR of around 3.93% during 2026-32.

- Product Type Shares

- Split air conditioners grabbed market share of 65%.

- Competition

- More than 10 companies are actively engaged in producing room air conditioners in Chile.

- Top 5 companies acquired around 55% of the market share.

- Anwo SA, Gree Electric Appliances Inc of Zhuhai, Ursus Trotter SA, Midea Group Co Ltd, TCL Corp etc., are few of the top companies.

- Technology

- Inverter grabbed 80% of the market.

Chile Room Air Conditioners Market Outlook

Chile room air conditioners market size was valued at USD 67.5 million in 2025 and is projected to grow from USD 69.8 million in 2026 to USD 88.4 million by 2032, exhibiting a CAGR of 3.93% during the forecast period. The outlook remains steady, supported by warmer climate conditions, a large residential base, and continued preference for efficient room cooling solutions across the country.

A key factor supporting demand is the rise in warmer than normal conditions. Chile’s mean temperature reaches 13.2°C in 2024, which is 0.4°C above the 1991-2020 normal, while 12 of 13 stations analyzed show positive anomalies. Chile’s official heatwave system also defines a heatwave as three or more consecutive days above an extreme threshold. This keeps room air conditioners relevant for households looking for direct and room specific cooling during stronger warm spells.

The outlook also benefits from the country’s broad household base and housing pipeline. Chile’s 2024 Census records 7,642,716 dwellings and 6,596,527 households, while 61.1% of households live in owner occupied homes and 26.2% live in rented housing. In addition, the 2025 Housing Subsidy Program covers 196,233 housing solutions, and the Emergency Housing Plan has already delivered 214,588 homes, with 127,428 more under execution, creating fresh scope for room air conditioners in move ins and first installations.

Buyer preference remains centered on efficient and stable cooling products. Split air conditioners hold 65% share, reflecting strong demand for fixed room cooling systems, while inverter technology accounts for 80% share, showing the importance of better control over electricity use. At the same time, electricity cost sensitivity remains relevant, as regulated household electricity tariffs rise by an average 7.1% from July 1, 2025, while annual inflation stands at 2.4% in February 2026, keeping room air conditioners tied to both comfort needs and operating cost awareness.

Chile Room Air Conditioners Market Growth DriverRising Heat Strengthens Everyday Cooling Need

Hotter conditions are a key driver for room air conditioners in Chile. The Chilean Meteorological Directorate’s 2024 annual climate report shows that the country’s mean temperature reaches 13.2°C in 2024, which is 0.4°C above the 1991-2020 normal, while 12 of 13 stations analyzed record positive anomalies. This indicates that warmer than normal conditions are becoming widespread rather than isolated.

These temperature conditions keep indoor cooling relevant for more households, especially during stronger warm spells. Chile’s official heatwave monitoring system also defines a heatwave as three or more consecutive days above an extreme daily threshold, showing that prolonged heat events are a real and measurable climate pattern. For room air conditioners, this supports demand from homes seeking direct and room specific comfort.

Chile Room Air Conditioners Market ChallengeElectricity Tariff Resets Keep Cost Sensitivity High

A major challenge is electricity cost sensitivity. Chile’s Ministry of Energy states that regulated household electricity tariffs register an average national increase of 7.1% from July 1, 2025, following the tariff normalization process. For room air conditioners, this directly affects expected running costs, which are important in household purchase decisions.

This pressure remains relevant even when general inflation is more moderate. Chile’s National Statistics Institute (INE) reports that the Consumer Price Index rises 2.4% year on year in February 2026. Even with lower inflation, higher power bills can still make consumers more careful about buying and operating cooling appliances, especially in price sensitive households.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Chile Room Air Conditioners Market TrendLarge Household Base Supports Residential Cooling Demand

An important trend is the growing relevance of household led cooling demand. Chile’s 2024 Census records 7,642,716 dwellings and 6,596,527 households, showing a broad installed base where room level cooling products can fit naturally. The same census also shows that 61.1% of households live in owner occupied housing, while 26.2% live in rented housing, which points to a wide residential user base across ownership types.

This housing profile supports the everyday role of room air conditioners in residential spaces. Whether households own or rent, the large number of occupied dwellings creates a strong base for compact and room specific cooling products that can be adopted without requiring whole building climate control systems.

Chile Room Air Conditioners Market OpportunityHousing Programs Open Fresh Installation Scope

A strong opportunity comes from Chile’s public housing pipeline. The Ministry of Housing and Urbanism (MINVU) states that its 2025 Housing Subsidy Program is authorized for UF 107,517,556, equivalent to 196,233 housing solutions nationwide. In addition, MINVU reports that the Emergency Housing Plan has already delivered 214,588 homes by August 2025, with 127,428 more under execution.

These figures expand the addressable base for room air conditioners linked to move ins, first installations, and home setup. As more subsidized and publicly supported housing units enter delivery or construction, brands gain wider room to target households at the point when essential comfort appliances are being added.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Chile Room Air Conditioners Market Segmentation Analysis

By Product Type

- Split Air Conditioners

- Up to 9,000 BTU/h

- 9,001-12,000 BTU/h

- 12,001-18,000 BTU/h

- 18,001-24,000 BTU/h

- Above 24,000 BTU/h

- Window Air Conditioners

- Up to 9,000 BTU/h

- 9,001-12,000 BTU/h

- 12,001-18,000 BTU/h

- 18,001-24,000 BTU/h

- Above 24,000 BTU/h

- Others

The segment with the highest share under the product type category is split air conditioners, which grab 65% of the market. This leading position shows that buyers in Chile continue to prefer fixed room cooling solutions that offer stronger and more reliable daily performance than less permanent alternatives.

This preference also fits the country’s heat profile. The Chilean Meteorological Directorate reports that the national mean temperature reaches 13.2°C in 2024, which is 0.4°C above the 1991-2020 normal, while 12 of 13 stations show positive anomalies. In such conditions, demand naturally leans toward room air conditioner formats that can provide more stable and effective cooling.

By Technology

- Inverter

- Non-Inverter

The segment with the highest share under the technology category is inverter, which grabs 80% of the market. This shows that buyers increasingly value technology that supports steadier cooling and better control over electricity use in daily operation. In Chile, this makes inverter based room air conditioners the dominant technology choice.

This leadership also aligns with the country’s cost environment. Chile’s Ministry of Energy says regulated household electricity tariffs rise by an average 7.1% from July 1, 2025, while INE reports 2.4% annual inflation in February 2026. In this setting, technologies associated with better operating efficiency become more attractive for households managing both comfort and monthly utility costs.

List of Companies Covered in Chile Room Air Conditioners Market

The companies listed below are highly influential in the Chile room air conditioners market, with a significant market share and a strong impact on industry developments.

- Anwo SA

- Gree Electric Appliances Inc of Zhuhai

- Ursus Trotter SA

- Midea Group Co Ltd

- TCL Corp

- Samsung Corp

- Hisense Group

- Mar del Sur Ltda

- LG Corp

Market News & Updates

- LG Corp, 2026:

On February 1, 2026, LG published its “Enfoque Categoría 2026” update on LG Chile’s HVAC platform, highlighting the residential rollout of DUALCOOL AI Air and stating that for 2026 it is reinforcing solutions for customers, partners, and installers across the region; the company says the line uses AI Air to automatically adjust airflow and operation based on indoor conditions, while LG ThinQ connectivity enables remote control, voice commands, and energy-use monitoring, and the same 2026 update also notes the expansion of lighter commercial single-split systems using lower-GWP R-32 refrigerant. For the Chile air conditioners market, this is a significant verified product-and-strategy development because it signals LG is pushing smarter, more energy-aware residential cooling products through its Chile-facing channel while also aligning with environmental efficiency trends, which can raise competition in premium inverter AC and accelerate consumer interest in connected cooling solutions.

- Samsung Corp, 2025:

On September 9, 2025, ANWO announced an official strategic commercial alliance with Samsung for Chile’s air-conditioning industry, stating that ANWO’s nationwide technical coverage will be combined with Samsung’s latest HVAC technologies and that the partnership will broaden the portfolio of advanced solutions available in the Chilean market; the announcement also quotes Samsung Chile’s HVAC product manager saying the alliance is a significant step in developing Samsung’s commercial air-conditioning category in Chile and strengthening its presence in a competitive segment. For the Chile air conditioners market, this is one of the most material verified updates in the company set because it directly improves Samsung’s local route to market, service reach, and project execution capability through a leading Chilean climatization specialist, which should support wider adoption and stronger brand visibility in both project-led and broader cooling applications.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Chile Room Air Conditioners Market Policies, Regulations, and Standards

- Chile Room Air Conditioners Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Chile Room Air Conditioners Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold in Thousand Units

- Market Segmentation & Growth Outlook

- By Product Type

- Split Air Conditioners- Market Insights and Forecast 2022-2032, USD Million

- Up to 9,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- 9,001-12,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- 12,001-18,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- 18,001-24,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- Above 24,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- Window Air Conditioners- Market Insights and Forecast 2022-2032, USD Million

- Up to 9,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- 9,001-12,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- 12,001-18,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- 18,001-24,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- Above 24,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Split Air Conditioners- Market Insights and Forecast 2022-2032, USD Million

- By Technology

- Inverter- Market Insights and Forecast 2022-2032, USD Million

- Non-Inverter- Market Insights and Forecast 2022-2032, USD Million

- By Price

- Up to USD 300- Market Insights and Forecast 2022-2032, USD Million

- USD 301 to USD 600- Market Insights and Forecast 2022-2032, USD Million

- USD 601 to USD 1,000- Market Insights and Forecast 2022-2032, USD Million

- Above USD 1,000- Market Insights and Forecast 2022-2032, USD Million

- By End User

- Residential- Market Insights and Forecast 2022-2032, USD Million

- Individual Households- Market Insights and Forecast 2022-2032, USD Million

- Apartments/Condominiums- Market Insights and Forecast 2022-2032, USD Million

- Vacation/Secondary Homes- Market Insights and Forecast 2022-2032, USD Million

- Commercial- Market Insights and Forecast 2022-2032, USD Million

- Offices- Market Insights and Forecast 2022-2032, USD Million

- Retail Stores/Showrooms- Market Insights and Forecast 2022-2032, USD Million

- Hospitality- Market Insights and Forecast 2022-2032, USD Million

- Healthcare Facilities- Market Insights and Forecast 2022-2032, USD Million

- Educational Institutions- Market Insights and Forecast 2022-2032, USD Million

- Small Commercial Establishments- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Residential- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- Brand-Owned Websites/D2C- Market Insights and Forecast 2022-2032, USD Million

- E-Commerce Marketplaces- Market Insights and Forecast 2022-2032, USD Million

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- Exclusive Brand Stores- Market Insights and Forecast 2022-2032, USD Million

- Multi-Brand Electronics & Appliance Stores- Market Insights and Forecast 2022-2032, USD Million

- Specialty Stores- Market Insights and Forecast 2022-2032, USD Million

- Hypermarkets/Supermarkets- Market Insights and Forecast 2022-2032, USD Million

- Home Improvement Stores- Market Insights and Forecast 2022-2032, USD Million

- Dealer/Distributor Network- Market Insights and Forecast 2022-2032, USD Million

- Direct Sales/Institutional Sales- Market Insights and Forecast 2022-2032, USD Million

- Local Independent Retailers- Market Insights and Forecast 2022-2032, USD Million

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- By Refrigerant Type

- R-32- Market Insights and Forecast 2022-2032, USD Million

- R-410A- Market Insights and Forecast 2022-2032, USD Million

- R-290- Market Insights and Forecast 2022-2032, USD Million

- R-454B- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Connectivity

- Smart/Connected- Market Insights and Forecast 2022-2032, USD Million

- Conventional/Non-Smart- Market Insights and Forecast 2022-2032, USD Million

- By Energy Efficiency

- 1 Star- Market Insights and Forecast 2022-2032, USD Million

- 2 Star- Market Insights and Forecast 2022-2032, USD Million

- 3 Star- Market Insights and Forecast 2022-2032, USD Million

- 4 Star- Market Insights and Forecast 2022-2032, USD Million

- 5 Star- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Product Type

- Market Size & Growth Outlook

- Chile Split Air Conditioners Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold in Thousand Units

- Market Segmentation & Growth Outlook

- By Technology- Market Insights and Forecast 2022-2032, USD Million

- By Price- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Refrigerant Type- Market Insights and Forecast 2022-2032, USD Million

- By Connectivity- Market Insights and Forecast 2022-2032, USD Million

- By Energy Efficiency- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Chile Window Air Conditioners Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold in Thousand Units

- Market Segmentation & Growth Outlook

- By Technology- Market Insights and Forecast 2022-2032, USD Million

- By Price- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Refrigerant Type- Market Insights and Forecast 2022-2032, USD Million

- By Connectivity- Market Insights and Forecast 2022-2032, USD Million

- By Energy Efficiency- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Midea Group Co Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- TCL Corp

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Samsung Corp

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Hisense Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Mar del Sur Ltda

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Anwo SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Gree Electric Appliances Inc of Zhuhai

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Ursus Trotter SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- LG Corp

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Electrolux AB

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Midea Group Co Ltd

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Technology |

|

| By Price |

|

| By End User |

|

| By Sales Channel |

|

| By Refrigerant Type |

|

| By Connectivity |

|

| By Energy Efficiency |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.