Canada Water & Wastewater Pump Market Report: Trends, Growth and Forecast (2026-2032)

By Pump Type (Centrifugal Pumps (End Suction, Split Case, Vertical (Turbine, Axial Pump, Mixed Flow Pump), Submersible Pump), Positive Displacement Pumps (Progressing Cavity, Diaphragm, Gear Pump, Others)), By Application (Water, Wastewater), By End User (Industrial Water & Wastewater, Municipal Water & Wastewater) ... Read more

|

Major Players

|

Canada Water & Wastewater Pump Market Statistics and Insights, 2026

- Market Size Statistics

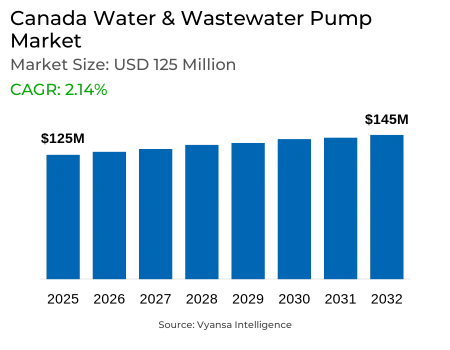

- Water & Wastewater Pump in Canada is estimated at $ 125 Million.

- The market size is expected to grow to $ 145 Million by 2032.

- Market to register a CAGR of around 2.14% during 2026-32.

- Pump Type Segment

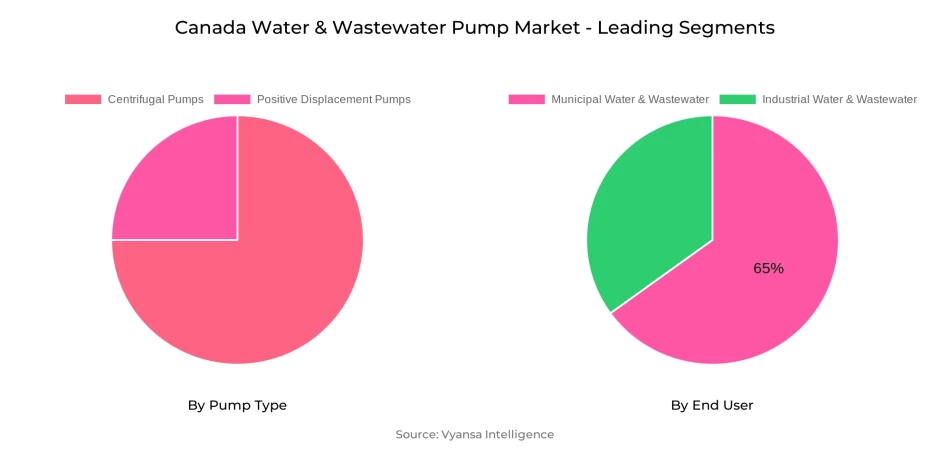

- Centrifugal Pumps continues to dominate the market.

- Competition

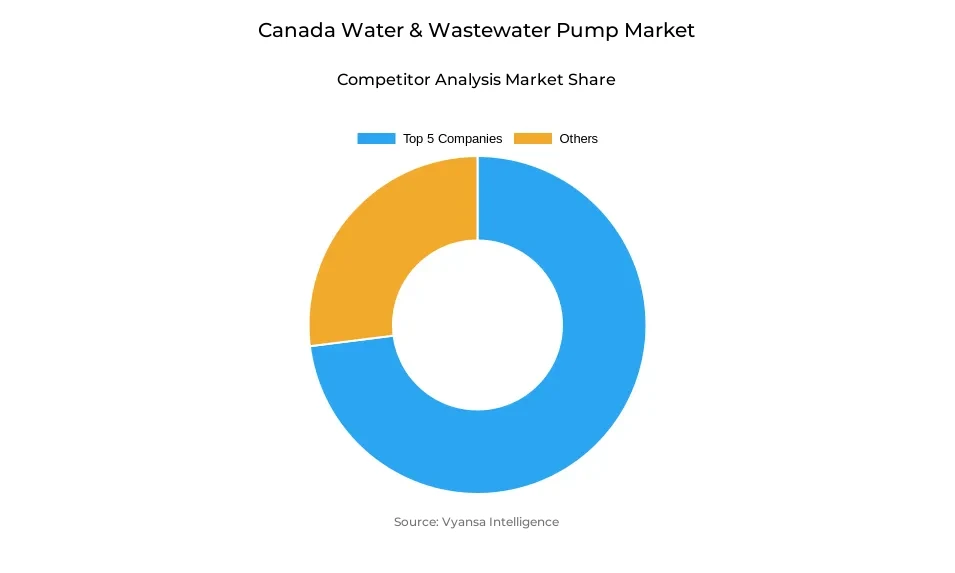

- More than 10 companies are actively engaged in producing Water & Wastewater Pump in Canada.

- Top 5 companies acquired the maximum share of the market.

- ITT, IDEX, Dover, Flowserve, Sulzer AG etc., are few of the top companies.

- End User

- Municipal Water & Wastewater grabbed 65% of the market.

Canada Water & Wastewater Pump Market Outlook

Canada's water assets are stressed with over one-third of its water mains being over 50 years old, resulting in high rates of pipeline failure and excessive water loss. Approximately $80 billion in replacement and upgrade is needed for aging drinking water, wastewater, and stormwater systems. These infrastructure shortages, along with rising populations and climate change-driven flooding, are driving robust demand for replacement pumps and high-tech pumps throughout the country. The Canadian Water & Wastewater Pump market stands at USD 125 million in 2025 and is projected to grow to USD 145 million by 2032.

Water and wastewater utilities in municipalities own the market share of 65%, fueled by ongoing replacement of aging infrastructure and increasing treatment demands. Government initiatives also gain strength, with Budget 2024 setting aside CAD 6 billion under the Canada Housing Infrastructure Fund for upgrading water and wastewater systems. Such developments require massive pump installations to guarantee reliability as well as adherence to more stringent efficiency standards.

Centrifugal pumps continue to be the top product type, with the highest market share, owing to their omnipresent applications across municipal systems, industrial processes, and HVAC operations. Single-stage centrifugal pumps are the most dominant, and multistage versions are increasingly being adopted to cater to high-pressure applications in oil & gas, mining, and water treatment. The market is also influenced by AI- and IoT-based smart pump solutions which enable energy-efficient operation, predictive maintenance, and leak detection, but adoption is limited due to high capital expenditure and lack of skilled resources.

Industrial water and wastewater use are becoming the fastest-growing end-use, driven by tighter environmental regulations and increasing demand in markets such as data centers, manufacturing, and energy. As municipalities continue to represent the biggest demand and industries insisting on new-generation solutions, Canada's pump market forecast remains optimistic, driven by infrastructure replacement, regulatory compliance, and uptake of new technologies.

Canada Water & Wastewater Pump Market Growth Driver

Aging Infrastructure Demands Urgent Modernization

Canada's water infrastructure is coming to a critical point as more than 33% of the water mains are older than 50 years, leading to around 260,000 breaks in water mains every year in the US and Canada. As per Statistics Canada, 86% of Canada's population is covered by municipal wastewater systems, with aging infrastructure needing around $80 billion to replace and improve. This infrastructure shortage is further aggravated by the reality that water loss in the distribution system stands at 15% today, much higher than the suggested 10% target.

Population growth drives rising demand while aging systems strain municipal utilities. Replacement costs for drinking water, wastewater and stormwater infrastructure in fair or very poor condition are estimated at more than $80 billion by the Federation of Canadian Municipalities. These aging infrastructure systems are compounded by the effects of climate change, as rising instances of flooding overwhelm treatment capacity and wreak havoc on already aging pipe systems. The pressing need for infrastructure upgrade drives high demand for replacement pumps and innovative pumping technologies throughout Canada's water industry.

Canada Water & Wastewater Pump Market Challenge

High Capital Investment Requirements Strain Adoption

Smart pump technology's adoption is hampered by a big financial hurdle since costs of installation are still much higher than conventional pumping systems. Smart water pumps need the incorporation of sophisticated sensors, IoT, and automated components that raise the capital outlay, and price-sensitive consumers can be discouraged by this in developing countries and small cities. This high up-front cost obstacle is added to by the difficulty of installing, maintaining, and debugging smart water pumps that necessitates skilled labor expertise.

Canadian municipalities are already faced with a presumed $80 billion infrastructure deficit and have a hard time justifying premium investment in sophisticated pumping technologies. Lack of trained personnel to operate these sophisticated systems also stands in the way of adoption and effective use across the country. The presence of cybersecurity threats related to IoT-connected smart pumps poses vulnerabilities that affect critical infrastructure, causing system failure and data loss and deterring businesses from adopting these technologies. These combined factors create substantial barriers to widespread smart pump adoption despite their long-term operational benefits.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Canada Water & Wastewater Pump Market Trend

Smart Technology Integration Revolutionizes Operations

IoT and AI-powered smart pumps are revolutionizing Canada's water management scenario, with the nation registering a 12.8% adoption rate as one of the leading countries promoting the use of smart IoT pumps in industrial and commercial domains. Such sophisticated systems allow for real-time performance tracking, predictive maintenance, and energy efficiency that cut the cost of operations drastically and increase the reliability of the system. Smart pumps combine sensors and weather information to optimize irrigation in an environmentally responsible manner, mitigating increasing concerns for groundwater depletion while aiding precision agriculture endeavors.

The global market for smart pumps is expected to expand at 12.2% CAGR, with centrifugal pumps fitted with sensor modules representing more than 50% of installations. Municipalities and industries in Canada are embracing AI-based diagnostics, cloud-enabled performance platforms, and automated control systems offering unparalleled system visibility. This technology revolution goes beyond simple monitoring to encompass leak detection, flow control, and automated compensation that facilitate sustainable water management in agricultural, municipal, and industrial applications. The combination of 5G connectivity and edge computing further augments these functions, providing constant high-speed connectivity even in far-flung locations.

Canada Water & Wastewater Pump Market Opportunity

Government Investment Fuels Market Expansion

The Canadian government's promise to modernize water infrastructure holds enormous prospects for growth in the pump market, with Budget 2024 setting aside CAD 6 billion in federal contributions over a period of ten years via the Canada Housing Infrastructure Fund for expediting construction and upgrading water and wastewater infrastructure. This huge investment specifically addresses housing-facilitating drinking water, wastewater, stormwater infrastructure that involves extensive pump installations and upgrades. Natural Resources Canada instituted energy efficiency standards for clean water pumps that took effect in January 2020, generating compliance-driven replacement demand for older, less efficient equipment.

Canadian industrial water treatment expenditure is forecast to grow 28% to 2030, spurred by high-tech and energy sector growth requiring sophisticated water management solutions. Provincial projects like the Alberta water conservation goals of mandating 170 liters per capita per day residential water use reduction by 2027 place further demands on effective pumping systems. This regulatory context, along with federal investment in infrastructure and provincial conservation requirements, creates a supportive context for growth of pump markets.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Canada Water & Wastewater Pump Market Segmentation Analysis

By Pump Type

- Centrifugal Pumps

- Positive Displacement Pumps

The most market-share-sizable pump type segment is Centrifugal Pumps, which remains the market leader. Centrifugal pumps retain their dominance because of extensive application in water supply systems, industrial fluid handling, air conditioning & heating systems, and oil & gas operations where high-volume routine fluid flow takes advantage of real-time flow control and variable speed drive capability.

The market for centrifugal pumps in Canada is anticipated to register a CAGR of 2.8% led by mining, oil and gas, and water treatment sectors that demand efficient fluid transfer solutions. Centrifugal technology dominates the market with its capability to deliver maximum flow rates and dynamic head to fluids along with energy-efficient operation through IoT sensors and auto-diagnosis. Single-stage centrifugal pumps specifically held 61.26% market share in 2022, while multistage variants represent the fastest-growing segment as industries demand higher pressure applications. This segmentation reflects the diverse operational requirements across Canada's industrial landscape, from oil sands production in Alberta to municipal water treatment facilities nationwide.

By End User

- Industrial Water & Wastewater

- Municipal Water & Wastewater

The End User segment with the largest market share is Municipal Water & Wastewater, which captured 65% of the market as per industry statistics. This is indicative of the imperative that municipal systems play in providing for Canada's population, as Statistics Canada indicates that 86% of Canadians are covered by municipal wastewater systems that involve significant pumping infrastructure. The top position of the municipal sector is due to continuous infrastructure replacement requirements, regulatory compliance demands, and population growth requiring increased water treatment capacity.

Industrial Water & Wastewater is the fastest growing end user segment with a CAGR of 2.58% fuelled by aggressive industrialization and strict environmental laws. Industrial applications such as data centers, manufacturing, and energy generation are heavily investing in cutting-edge water treatment systems to adhere to regulatory needs and enable sustainable processes. Canada's industrial water treatment industry is driving high demand for niche pumping solutions. This industrial expansion supplements the existing municipal sector, and each segment needs to have different pump specifications and performance requirements in order to fulfill their various operational demands.

Top Companies in Canada Water & Wastewater Pump Market

The top companies operating in the market include ITT, IDEX, Dover, Flowserve, Sulzer AG, KSB, Xylem, Grundfos, Ebara, SPX Flow, etc., are the top players operating in the Canada Water & Wastewater Pump Market.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. Canada Water & Wastewater Pump Market Policies, Regulations, and Standards

4. Canada Water & Wastewater Pump Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. Canada Water & Wastewater Pump Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in US$ Million

5.2. Market Segmentation & Growth Outlook

5.2.1.By Pump Type

5.2.1.1. Centrifugal Pumps- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.1. End Suction- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.2. Split Case- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.3. Vertical- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.3.1. Turbine- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.3.2. Axial Pump- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.3.3. Mixed Flow Pump- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.4. Submersible Pump- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Positive Displacement Pumps- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.1. Progressing Cavity- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.2. Diaphragm- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.3. Gear Pump- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.4. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Application

5.2.2.1. Water- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Wastewater- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By End User

5.2.3.1. Industrial Water & Wastewater- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Municipal Water & Wastewater- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Competitors

5.2.4.1. Competition Characteristics

5.2.4.2. Market Share & Analysis

6. Canada Centrifugal Water & Wastewater Pump Market Statistics, 2020-2030F

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in US$ Million

6.2. Market Segmentation & Growth Outlook

6.2.1.By Pump Type- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Application- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By End User- Market Insights and Forecast 2022-2032, USD Million

7. Canada Positive Displacement Water & Wastewater Pump Market Statistics, 2020-2030F

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in US$ Million

7.2. Market Segmentation & Growth Outlook

7.2.1.By Pump Type- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Application- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By End User- Market Insights and Forecast 2022-2032, USD Million

8. Competitive Outlook

8.1. Company Profiles

8.1.1.Flowserve Corporation

8.1.1.1. Business Description

8.1.1.2. Product Portfolio

8.1.1.3. Collaborations & Alliances

8.1.1.4. Recent Developments

8.1.1.5. Financial Details

8.1.1.6. Others

8.1.2.Ebara Corporation

8.1.2.1. Business Description

8.1.2.2. Product Portfolio

8.1.2.3. Collaborations & Alliances

8.1.2.4. Recent Developments

8.1.2.5. Financial Details

8.1.2.6. Others

8.1.3.WILO SE

8.1.3.1. Business Description

8.1.3.2. Product Portfolio

8.1.3.3. Collaborations & Alliances

8.1.3.4. Recent Developments

8.1.3.5. Financial Details

8.1.3.6. Others

8.1.4.Sulzer Limited

8.1.4.1. Business Description

8.1.4.2. Product Portfolio

8.1.4.3. Collaborations & Alliances

8.1.4.4. Recent Developments

8.1.4.5. Financial Details

8.1.4.6. Others

8.1.5.Grundfos Holding A/S

8.1.5.1. Business Description

8.1.5.2. Product Portfolio

8.1.5.3. Collaborations & Alliances

8.1.5.4. Recent Developments

8.1.5.5. Financial Details

8.1.5.6. Others

8.1.6.Xylem Inc.

8.1.6.1. Business Description

8.1.6.2. Product Portfolio

8.1.6.3. Collaborations & Alliances

8.1.6.4. Recent Developments

8.1.6.5. Financial Details

8.1.6.6. Others

8.1.7.KSB SE & Co. KGaA

8.1.7.1. Business Description

8.1.7.2. Product Portfolio

8.1.7.3. Collaborations & Alliances

8.1.7.4. Recent Developments

8.1.7.5. Financial Details

8.1.7.6. Others

8.1.8.Kirloskar Brothers Limited (KBL)

8.1.8.1. Business Description

8.1.8.2. Product Portfolio

8.1.8.3. Collaborations & Alliances

8.1.8.4. Recent Developments

8.1.8.5. Financial Details

8.1.8.6. Others

8.1.9.Franklin Electric

8.1.9.1. Business Description

8.1.9.2. Product Portfolio

8.1.9.3. Collaborations & Alliances

8.1.9.4. Recent Developments

8.1.9.5. Financial Details

8.1.9.6. Others

8.1.10. Pentair PLC

8.1.10.1. Business Description

8.1.10.2. Product Portfolio

8.1.10.3. Collaborations & Alliances

8.1.10.4. Recent Developments

8.1.10.5. Financial Details

8.1.10.6. Others

9. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Pump Type |

|

| By Application |

|

| By End User |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.