Canada Wallpaper Market Report: Trends, Growth and Forecast (2026-2032)

By Product Type (Vinyl Wallpaper, Non-Woven Wallpaper, Paper Wallpaper, Fabric Wallpaper, Others), By Application (Residential, Commercial), By Distribution Channel (Offline Retail, Online Retail, Specialty Stores, Direct Sales, Others) ... Read more

|

Major Players

|

Canada Wallpaper Market Statistics and Insights, 2026

- Market Size Statistics

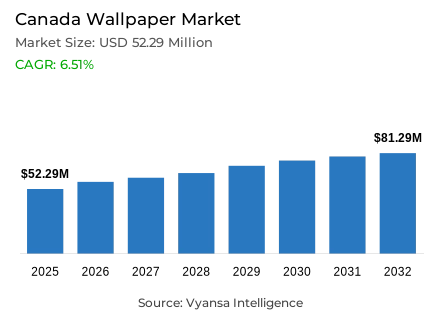

- Wallpaper market size in Canada was valued at USD 52.29 million in 2025 and is estimated at USD 56.28 million in 2026.

- The market size is expected to grow to USD 81.29 million by 2032.

- Market to register a CAGR of around 6.51% during 2026-32.

- Product Type Shares

- Vinyl wallpaper grabbed market share of 40%.

- Competition

- More than 10 companies are actively engaged in producing wallpaper in Canada.

- Top 5 companies acquired around 25% of the market share in 2026.

- Brewster Home Fashions, York Wallcoverings, Graham & Brown Ltd, Home Depot of Canada Inc. (The Home Depot), RONA inc. etc., are few of the top companies.

- Application

- Residential grabbed 75% of the market.

Canada Wallpaper Market Outlook

Canada wallpaper market is expanding as households use decorative wallcoverings for repainting cycles, accent-wall upgrades, rental-friendly décor, room personalization, and renovation-light interior refreshes. The market size was valued at USD 52.29 million in 2025 and is projected to grow from USD 56.28 million in 2026 to USD 81.29 million by 2032, registering a CAGR of 6.51% during the forecast period. Growth is supported by bedrooms, living rooms, kitchens, powder rooms, nurseries, home offices, and rental units where wallpaper offers visible design change without major remodeling.

Residential demand is the clear consumption base because households drive most decorative wall upgrades through moving events, small renovations, repainting decisions, and room-level personalization. Statistics Canada reported that residential building permit value reached CAD 86.6 billion in 2025, while multi-family permits reached CAD 57.0 billion, the second-highest level in the series. This matters because more apartments, condos, and renovated homes create more interior surfaces needing affordable visual updates. wallpaper fits this demand because it offers faster transformation than cabinetry, flooring, or structural renovation.

Vinyl wallpaper holds the leading 40% share under product type because Canadian buyers need durable, washable, moisture-tolerant, and easy-to-maintain wallcoverings. Home Depot Canada advises waterproof wallpaper for moisture or damp areas, supporting vinyl’s fit in kitchens, bathrooms, laundry areas, children’s rooms, and rental properties. Residential holds 75% share because household buyers use wallpaper for accent walls, children’s spaces, home offices, and quick design refreshes. This shows that the category is led by consumer décor decisions, DIY installation, online browsing, and home-improvement retail access.

The outlook remains positive because housing activity, retail access, and digital discovery support repeat decorative purchases through 2032. CMHC reported Canada’s housing starts trend at 258,010 units in May 2026, while year-to-date actual starts in centres above 10,000 people reached 93,644 units, up 3% from 2025. This matters because new and recently occupied homes create finishing and personalization demand. Statistics Canada also recorded CAD 4.3 billion in retail e-commerce sales in December 2025, showing that online retail helps consumers compare wallpaper designs, samples, prices, and installation formats.

Canada Wallpaper Market Growth Driver

Home Renovation Activity Strengthens Interior Demand

Home renovation and new housing activity are the primary demand driver because wallpaper is purchased when households refresh rooms, personalize newly occupied units, or upgrade interiors without heavy construction. Statistics Canada reported CAD 86.6 billion in residential building permits in 2025 and a record 308,600 dwelling units authorized for construction. These figures matter because each permitted unit creates future demand for wall finishing, décor upgrades, and rental personalization. Home renovation therefore supports peel-and-stick wallpaper, vinyl wallpaper, removable wallpaper, and other interior wallcoverings used for fast room transformation.

The driver is also supported by renovation price pressure, which encourages smaller decorative projects instead of major remodels. Statistics Canada’s Residential Renovation Price Index covers 37 renovation projects across 15 census metropolitan areas and includes contractor prices for materials, labour, equipment, overhead, and profit. This methodology shows why wallpaper can benefit from cost-sensitive remodeling activity: it avoids full contractor-led renovation while still improving room appearance. Peel-and-stick, pre-pasted, and removable formats reduce labour dependence, making DIY home improvement more accessible for Canadian homeowners and renters.

Canada Wallpaper Market Challenge

Housing Softness Pressures Decorative Spending

Housing softness is the main challenge because wallpaper demand depends on home turnover, new occupancy, renovation confidence, and discretionary décor spending. Statistics Canada reported that residential permit value fell CAD 1.0 billion to CAD 86.6 billion in 2025, while single-family construction intentions declined 7.0% to CAD 29.6 billion, the lowest annual level in the series. This matters because detached homes usually create larger wall-surface opportunities than smaller units. When single-family activity weakens, suppliers lose some demand from whole-home personalization, large renovation projects, and move-in redecorating cycles.

Affordability pressure also limits premium wallpaper purchases. Statistics Canada reported that Canada’s Consumer Price Index rose 2.8% year over year in April 2026, while annual average CPI increased 2.1% in 2025. These figures matter because decorative wallpaper competes with groceries, rent, utilities, mortgage payments, and renovation labour in household budgets. wallpaper remains relatively affordable, but consumers may delay luxury wallpaper, textured wallpaper, customized wallpaper, or designer products when purchasing power tightens. Retailers must balance premium décor products with entry-level rolls, peel-and-stick formats, promotions, and online comparison tools

Unlock Market Intelligence

Explore the market potential with our data-driven report

Canada Wallpaper Market Trend

DIY and Digital Discovery Reshape Buying

The strongest trend is DIY-friendly and digitally discovered wallpaper, especially peel-and-stick, removable, pre-pasted, waterproof, and 3D formats. Statistics Canada reported retail e-commerce sales of CAD 4.3 billion in December 2025, accounting for 6.1% of total retail trade, up from 5.8% in November. This matters because wallpaper is highly visual: consumers compare colors, textures, repeat patterns, room images, customer reviews, and installation formats online before buying. Digital discovery reduces showroom dependence and helps smaller brands reach homeowners, renters, interior designers, and DIY consumers.

Retailer product education reinforces this trend. Home Depot Canada says peel-and-stick wallpaper is self-adhesive, easy to apply, and removable without glue or water, making it suitable for renters or temporary décor changes. Its installation guide describes peel-and-stick application as a beginner project taking about three hours. This matters commercially because simpler installation expands the buyer base beyond professional decorators. Removable wallpaper reduces commitment risk, supports seasonal décor, enables accent-wall experimentation, and allows online retailers to sell samples, rolls, tools, and matching supplies directly to households.

Canada Wallpaper Market Opportunity

Multi-Family Housing Opens Design Scope

The strongest opportunity lies in multi-family housing, rental interiors, and small-space personalization. Statistics Canada reported that multi-family permits reached CAD 57.0 billion in 2025, the second-highest level in the series, while authorized dwelling units rose to a record 308,600. This matters because apartments and condos create concentrated demand for affordable interior finishes, especially accent walls, removable décor, washable wallpaper, and durable wallcoverings suited to compact rooms. wallpaper suppliers can target renters, landlords, property managers, and first-time buyers who want visible upgrades without permanent renovation or high labour costs.

CMHC adds another demand signal, reporting that year-to-date actual housing starts in centres with at least 10,000 people reached 93,644 units in May 2026, up 3% from the same period in 2025. This supports opportunity because each new unit eventually needs finishing, staging, occupancy personalization, or post-move décor spending. wallpaper brands can benefit by offering smaller roll sizes, waterproof vinyl products, coordinated colour collections, sample-based ordering, specialty stores, and e-commerce platforms. The best opportunity is recurring room refreshes across urban apartments, starter homes, student housing, and rental properties.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Canada Wallpaper Market Segmentation Analysis

By Product Type

- Vinyl Wallpaper

- Non-Woven Wallpaper

- Paper Wallpaper

- Fabric Wallpaper

- Others

The segment with the highest share under Product Type is Vinyl wallpaper, holding around 40% of the market. This leadership is commercially logical because vinyl wallpaper matches Canadian household needs for durability, cleanability, moisture tolerance, and design variety. Home Depot Canada advises waterproof wallpaper for moisture or damp areas, directly supporting vinyl use in kitchens, bathrooms, laundry rooms, basements, and rental units. The 40% share shows that buyers prioritize performance, not only pattern. In everyday homes, wallcoverings must survive wiping, children’s rooms, cooking moisture, hallway contact, and tenant turnover.

Vinyl also benefits from retailer merchandising because it is easier to explain through functional claims such as washable, removable, textured, waterproof, or peel-and-stick. Home Depot Canada highlights wallpaper options including pre-pasted, peel-and-stick, removable, waterproof, and 3D products, showing how retailers segment demand by application need. This matters because many consumers choose wallpaper without professional guidance. Clear product labels reduce hesitation and improve conversion. Vinyl’s leadership therefore reflects both material performance and retail simplicity across home improvement stores, online retail, and specialty stores.

By Application

- Residential

- Commercial

The segment with the highest share under Application is Residential, holding around 75% of the market. This dominance reflects how wallpaper is mainly purchased for homes rather than large commercial specifications. Residential buyers use wallcoverings for accent walls, bedrooms, nurseries, living rooms, home offices, powder rooms, hallways, and rental upgrades. Statistics Canada reported CAD 86.6 billion in residential building permits in 2025, confirming that housing remains the largest built-environment base linked to interior finishing demand. The 75% share shows that household taste, DIY adoption, and online browsing shape revenue.

Residential leadership is reinforced by household-scale installation needs. Home Depot Canada describes peel-and-stick wallpaper as easy to apply and remove without glue or water, while its installation guide classifies the task as beginner level. This matters because residential customers often prefer products that avoid contractors, downtime, dust, and large budgets. wallpaper fits room-by-room decision making: one child’s wall, one rental entryway, one powder room, or one home-office backdrop can drive purchase. The segment’s strength therefore comes from frequent small projects, not only new builds.

List of Companies Covered in Canada Wallpaper Market

The companies listed below are highly influential in the Canada wallpaper market, with a significant market share and a strong impact on industry developments.

- Brewster Home Fashions

- York Wallcoverings

- Graham & Brown Ltd

- Home Depot of Canada Inc. (The Home Depot)

- RONA inc.

- Sherwin Williams Canada Inc. (Sherwin-Williams)

- Amazon.com.ca ULC (Amazon.ca)

- Wayfair LLC (Wayfair)

- Dundee Deco

- Koroseal Interior Products LLC (Metro Wallcoverings)

Market News & Updates

- Graham & Brown Ltd, 2026:

Graham & Brown launched its official 80th anniversary wallpaper collection. The collection reimagines eight archive designs in contemporary styles and was released alongside the company’s 80th birthday. The update adds a heritage-led wallpaper range for residential décor buyers seeking refreshed classic patterns.

- York Wallcoverings, 2025:

York Wallcoverings introduced Patina as its 2026 Color of the Year. The update features a dedicated Patina wallpaper selection, including botanical, textured, metallic, and abstract designs. The release adds a trend-led color collection for residential wallpaper and interior decoration projects.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Canada Wallpaper Market Policies, Regulations, and Standards

- Canada Wallpaper Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Canada Wallpaper Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Meter Square

- Market Segmentation & Growth Outlook

- By Product Type

- Vinyl Wallpaper- Market Insights and Forecast 2022-2032, USD Million

- Non-Woven Wallpaper- Market Insights and Forecast 2022-2032, USD Million

- Paper Wallpaper- Market Insights and Forecast 2022-2032, USD Million

- Fabric Wallpaper- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Application

- Residential- Market Insights and Forecast 2022-2032, USD Million

- Commercial- Market Insights and Forecast 2022-2032, USD Million

- By Distribution Channel

- Offline Retail- Market Insights and Forecast 2022-2032, USD Million

- Online Retail- Market Insights and Forecast 2022-2032, USD Million

- Specialty Stores- Market Insights and Forecast 2022-2032, USD Million

- Direct Sales- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Product Type

- Market Size & Growth Outlook

- Canada Vinyl Wallpaper Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Meter Square

- Market Segmentation & Growth Outlook

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Distribution Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Canada Non-Woven Wallpaper Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Meter Square

- Market Segmentation & Growth Outlook

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Distribution Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Canada Paper Wallpaper Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Meter Square

- Market Segmentation & Growth Outlook

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Distribution Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Canada Fabric Wallpaper Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Meter Square

- Market Segmentation & Growth Outlook

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Distribution Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Home Depot of Canada Inc. (The Home Depot)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- RONA inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Sherwin Williams Canada Inc. (Sherwin-Williams)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Amazon.com.ca ULC (Amazon.ca)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Wayfair LLC (Wayfair)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Brewster Home Fashions

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- York Wallcoverings

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Graham & Brown Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Dundee Deco

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Koroseal Interior Products, LLC (Metro Wallcoverings)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Home Depot of Canada Inc. (The Home Depot)

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Application |

|

| By Distribution Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.