US Phytonutrients Market Report: Trends, Growth and Forecast (2026-2032)

By Type (Carotenoids, Flavonoids, Polyphenols, Phytosterols/Plant Sterols, Specialty Phytonutrients (Curcumin, Organosulfur Compounds, Phytoestrogens), Others), By Functional Positioning (Antioxidant Support, Eye Health, Heart Health, Immune Support, Cognitive Health, Skin Health, Gut/Metabolic Health, Healthy Aging), By Regulatory Use Case (Dietary Supplement Ingredient, Conventional Food Ingredient, Functional Beverage Ingredient, Natural Colorant, Cosmetic Active, Feed/Animal Nutrition Ingredient), By Delivery Technology (Standard Extract Powder, Oil Suspension/Oleoresin, Water-Dispersible Format, Microencapsulated/Beadlet, Emulsified/Liposomal, Ready-to-Blend Premix), By Source (Fruits & Vegetables, Grains & Cereals, Legumes & Pulses, Herbs & Spices, Oilseeds, Others), By Form (Dry/Powder, Liquid, Others), By Sales Channel (Retail Online (Brand-Owned Websites, Third-Party E-commerce Marketplaces, Online Health & Wellness Stores), Retail Offline (Supermarkets & Hypermarkets, Pharmacies & Drug Stores, Specialty Health & Nutrition Stores)), By End-use Industry (Food & Beverages, Nutraceuticals & Dietary Supplements, Pharmaceuticals, Cosmetics & Personal Care, Animal Nutrition, Others), By Region (West, Midwest, South, North, Northeast) ... Read more

|

Major Players

|

US Phytonutrients Market Statistics and Insights, 2026

- Market Size Statistics

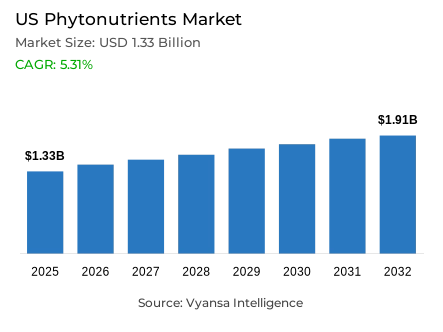

- Phytonutrients market size in US was valued at USD 1.33 billion in 2025 and is estimated at USD 1.4 billion in 2026.

- The market size is expected to grow to USD 1.91 billion by 2032.

- Market to register a CAGR of around 5.31% during 2026-32.

- Type Shares

- Carotenoids grabbed market share of 25%.

- Competition

- More than 10 companies are actively engaged in producing phytonutrients in US.

- Top 5 companies acquired around 40% of the market share.

- Sabinsa, OmniActive Health Technologies, Euromed USA, ADM, Kalsec etc., are few of the top companies.

- End-use Industry

- Nutraceuticals & dietary supplements grabbed 35% of the market.

US Phytonutrients Market Outlook

The US phytonutrients market was valued at USD 1.33 billion in 2025, establishing a commercially stable and health-consumption-driven foundation within one of the world's most active functional ingredient and preventive nutrition ecosystems. Projected to advance from USD 1.40 billion in 2026 to USD 1.91 billion by 2032, the sector registers a CAGR of 5.31% across the forecast horizon. This steady and structurally supported expansion trajectory reflects the sustained relevance of plant-based bioactive ingredients across health-focused product development, where preventive nutrition priorities, wellness-oriented consumption patterns, and ingredient-led formulation investment continue to support commercial expansion across the country. Growth is anchored in durable consumer health behavior rather than trend-driven purchasing cycles, giving this market a commercial resilience that sustains consistent ingredient demand across diverse application verticals and economic conditions.

The type architecture defining this market's commercial structure is anchored in carotenoid-based ingredients. Carotenoids command approximately 25% of total type market share, reflecting the consistent and deeply embedded formulation preference for naturally derived compounds whose broad application compatibility, established health associations, and wide consumer recognition make them the reference ingredient category across supplement, food, and functional product development contexts. This type concentration confirms that US phytonutrient buyers continue to prioritize ingredient categories whose commercial credibility and application breadth create natural and durable demand advantages over less established phytonutrient alternatives across wellness-focused procurement and formulation decisions.

The end-use architecture reinforces the structural centrality of nutraceuticals and dietary supplements as the category's dominant demand channel. Nutraceuticals and Dietary Supplements account for approximately 35% of total end-use industry market share, reflecting the foundational role of supplement-led applications in connecting phytonutrient ingredient demand with everyday wellness, preventive nutrition, and health-oriented consumer purchasing behavior. The NIH Office of Dietary Supplements documentation that approximately one-half of US adults and one-third of children and adolescents use dietary supplements confirms the national consumption scale that sustains consistent ingredient procurement demand across the supplement formulation and product development ecosystem.

The future outlook is defined by four converging structural forces whose combined commercial impact creates a phytonutrients market of steady and well-grounded expansion momentum. The CDC's documentation that 76.4% of US adults, representing approximately 194 million people, reported one or more chronic conditions in 2023, while 51.4% reported multiple chronic conditions, confirms the health burden scale that sustains persistent consumer demand for nutrition-linked and preventive wellness ingredients. The USDA's Dietary Guidelines for Americans 2025 to 2030 delivering its first direct consumer advice in 25 years, centered on whole-food consumption, strengthens the commercial relevance of plant-linked ingredients whose naturally derived positioning aligns with evolving clean-label and food-connected wellness preferences. The US Census Bureau's documentation of the population aged 65 and older rising 3.1% to 61.2 million in 2024, now representing 18.0% of the national population, confirms the aging demographic expansion that is progressively broadening the addressable consumer base for healthy aging, long-term nutrition support, and active wellness products. These converging forces define a commercial environment that consistently rewards phytonutrient suppliers with strong carotenoid portfolio depth, supplement application expertise, and naturally positioned ingredient credentials over the forecast period.

US Phytonutrients Market Growth Driver

Chronic Condition Prevalence Sustains Preventive Nutrition Ingredient Demand

The broad and institutionally documented prevalence of chronic health conditions across the US adult population represents the primary structural driver of phytonutrient demand. This health burden functions as a persistent consumer wellness imperative that sustains consistent demand for plant-based bioactive ingredients associated with preventive nutrition, daily health support, and long-term wellness management across supplement and functional product formulation contexts. This disease burden-driven demand dynamic transcends discretionary spending fluctuations, reflecting a durable health behavior orientation whose purchasing volume generation is structurally anchored in the widespread consumer motivation to support everyday wellness through ingredient-led nutrition products.

The quantitative evidence validating this chronic condition-driven demand dynamic is documented with precision by the CDC. A total of 76.4% of US adults, representing approximately 194 million people, reported one or more chronic conditions in 2023, while 51.4%, or approximately 130 million adults, reported multiple chronic conditions. This broad health burden confirms the national scale of preventive wellness motivation that sustains consistent consumer demand for phytonutrient-based formulations across supplement and nutrition-focused product categories. The age-stratified dimension of this health profile is equally commercially significant, with 59.5% of young adults, 78.4% of midlife adults, and 93.0% of older adults reporting at least one chronic condition in 2023. These figures confirm a health landscape of sufficient breadth and demographic reach to sustain structural phytonutrient ingredient demand growth over the forecast period.

US Phytonutrients Market Challenge

Scientific Complexity and Evidence Gaps Constrain Consumer Confidence

The expanding scale of the US dietary supplement product universe combined with persistent scientific uncertainty around ingredient mechanisms, efficacy, and safety represents the most consequential structural challenge confronting phytonutrient suppliers. This evidence gap creates systematic consumer trust, product differentiation, and health claim credibility constraints that moderate adoption velocity and raise the communication investment threshold for ingredient-led brand positioning across a market whose product density makes standing out with scientific credibility progressively more difficult. In a commercial environment where phytonutrient product breadth is expanding faster than clear consumer understanding, the ability to communicate ingredient value with evidence-supported precision becomes a primary competitive differentiator.

The structural depth and consumer reach of this scientific complexity challenge are quantified with precision by the NIH Office of Dietary Supplements. The US dietary supplement space now encompasses more than 100,000 products, confirming the scale of the commercial environment within which phytonutrient suppliers must compete for formulation inclusion and consumer-facing brand credibility. The NIH Office of Dietary Supplements further documents that while approximately one-half of US adults and one-third of children and adolescents use dietary supplements, scientific questions remain open regarding mechanisms, metabolism, efficacy, safety, and effects on health outcomes. This combination of broad consumer usage and persistent evidence uncertainty creates a market environment where ingredient suppliers whose clinical research investment and transparent health communication capabilities exceed those of less evidence-supported competitors will capture disproportionate formulator trust and brand partnership value over the forecast period.

Unlock Market Intelligence

Explore the market potential with our data-driven report

US Phytonutrients Market Trend

Whole-Food Nutrition Messaging Strengthens Plant-Derived Ingredient Positioning

The progressive institutionalization of whole-food and naturally derived nutrition guidance across US federal dietary policy represents the defining structural trend reshaping phytonutrient ingredient positioning, product development priorities, and consumer communication strategies across the market. This whole-food nutrition trend is moving the commercial conversation around plant-based ingredients beyond isolated compound supplementation into the domain of food-connected, naturally positioned wellness solutions whose alignment with official dietary guidance creates a credibility and communication advantage for ingredient suppliers whose sourcing and positioning narratives reflect real-food consumption values.

The policy specificity and consumer communication significance of this whole-food nutrition trend are documented with authority by the USDA Food and Nutrition Service and the USDA Economic Research Service. The Dietary Guidelines for Americans 2025 to 2030 deliver direct consumer advice for the first time in 25 years, with the central message being a straightforward call to eat real food, confirming that federal dietary guidance is actively reinforcing the commercial relevance of naturally derived and plant-linked ingredient positioning across health product development. The USDA Economic Research Service's documentation that approximately 90% of Americans eat too few vegetables and 80% do not consume enough fruit confirms the structural produce intake gap that creates consistent consumer receptivity to plant-derived wellness ingredients positioned as accessible bridges to improved daily nutrition. As whole-food consumption messaging deepens its influence on consumer health purchasing behavior, phytonutrient suppliers whose ingredient narratives authentically reflect plant-origin and food-connected values will attract disproportionate formulator and consumer preference over the forecast period.

US Phytonutrients Market Opportunity

Aging Population Expansion Creates a Structurally Larger Wellness Demand Base

The rapid and institutionally documented expansion of the US older adult population represents the phytonutrients market's most structurally significant demand growth opportunity. This demographic shift provides a large, geographically distributed, and progressively more health-engaged consumer cohort whose healthy aging, long-term nutrition support, and active wellness management priorities create expanding commercial demand for phytonutrient ingredients across supplement, functional food, and specialty nutrition product formulation contexts. This aging demographic opportunity is distinguished from general population wellness demand by its structural durability and its capacity to generate consistent baseline purchasing volume that compounds independently of broader consumer discretionary spending cycles.

The quantitative foundation of this aging demographic opportunity is established with precision by the US Census Bureau. The population aged 65 and older rose 3.1% to reach 61.2 million in 2024, now representing 18.0% of the total national population, confirming that the demographic shift toward an older, more health-management-oriented national consumer base is advancing at a pace whose commercial implications for phytonutrient ingredient demand are both immediate and structurally compounding. The national median age reaching a record 39.1 years in 2024 further confirms that the aging demographic demand dynamic is not limited to the 65-and-older cohort but reflects a broader national population maturation whose wellness purchasing priorities are progressively elevating commercial demand for ingredients associated with sustained health support, vitality management, and preventive nutrition. Suppliers combining carotenoid portfolio depth, aging-specific formulation expertise, and supplement channel distribution strength will capture disproportionate value from this structurally significant opportunity over the forecast period.

Unlock Market Intelligence

Explore the market potential with our data-driven report

US Phytonutrients Market Segmentation Analysis

By Type

- Carotenoids

- Flavonoids

- Polyphenols

- Phytosterols/Plant Sterols

- Specialty Phytonutrients

- Curcumin

- Organosulfur Compounds

- Phytoestrogens

- Others

The segment with highest market share under the Type is Carotenoids, accounting for approximately 25% of the total market. This leading position reflects the deep structural alignment between carotenoid ingredient characteristics and the specific formulation requirements of the US market's most commercially active wellness product developers, where broad application compatibility, established consumer health associations, and wide recognition across supplement, food, and functional product contexts make carotenoids the reference phytonutrient type across ingredient procurement and product development decisions. With one-quarter of total market value concentrated within a single type category, Carotenoids define the commercial priorities, ingredient sourcing frameworks, and formulation innovation agenda of the US phytonutrients market, establishing the health positioning benchmarks and application breadth standards against which all competing phytonutrient type categories are evaluated.

The structural leadership of Carotenoids is further sustained by the ingredient's inherent versatility across the full spectrum of wellness product development contexts, from daily supplement formulations through functional food and beverage applications to specialty nutrition products targeting specific health management priorities. As the USDA's Dietary Guidelines for Americans 2025 to 2030 strengthen the commercial relevance of food-connected, naturally derived wellness ingredients, carotenoids' plant-origin positioning and broad consumer familiarity create a natural alignment with the clean-label and whole-food-associated product development direction that is reshaping formulation investment priorities across the US health ingredient landscape. The segment's structural dominance as the market's primary type revenue contributor and formulation innovation focal point is expected to consolidate over the forecast period.

By End-use Industry

- Food & Beverages

- Nutraceuticals & Dietary Supplements

- Pharmaceuticals

- Cosmetics & Personal Care

- Animal Nutrition

- Others

The segment with highest market share under the End-Use Industry is Nutraceuticals and Dietary Supplements, accounting for approximately 35% of the total market. This commanding position reflects the foundational role of supplement-led applications in providing the most direct and commercially established integration pathway for phytonutrient ingredients into consumer-facing wellness products whose daily health support, preventive nutrition, and ingredient-led value positioning sustain consistent and high-frequency procurement demand across both established and emerging product development contexts. With more than one-third of total market value anchored in nutraceutical and dietary supplement demand, this end-use segment defines the ingredient specification standards, health claim positioning frameworks, and commercial development priorities of the US phytonutrients market.

The structural leadership of Nutraceuticals and Dietary Supplements is being actively sustained by the broad and institutionally documented scale of national supplement consumption. The NIH Office of Dietary Supplements' documentation of the US dietary supplement space now encompassing more than 100,000 products confirms the commercial depth of the application environment within which phytonutrient ingredients compete for formulation inclusion and brand-level positioning. As consumers increasingly seek wellness products that address everyday health management, preventive nutrition, and long-term vitality support, the supplement channel's ability to deliver ingredient-specific health value through structured daily consumption routines creates a commercially resilient demand dynamic for carotenoid and broader phytonutrient ingredient integration. The segment's structural authority as the market's primary revenue anchor and ingredient demand driver is expected to deepen over the forecast period.

List of Companies Covered in US Phytonutrients Market

The companies listed below are highly influential in the US phytonutrients market, with a significant market share and a strong impact on industry developments.

- Sabinsa

- OmniActive Health Technologies

- Euromed USA

- ADM

- Kalsec

- Kemin Industries

- FutureCeuticals

- AIDP

- Kerry Group

- Givaudan

Market News & Updates

- OmniActive Health Technologies, 2025:

, OmniActive announced that the U.S. FDA acknowledged Lutemax Free Lutein for use in infant formula, and the company said this regulatory milestone opens a new category for its flagship lutein ingredient by giving infant-formula manufacturers a differentiated carotenoid source to support infant eye and brain development. For the U.S. phytonutrients market, this is a highly significant update because it expands lutein’s addressable market into one of the most tightly regulated nutrition segments and strengthens the commercial relevance of carotenoid-based phytonutrients in early-life nutrition

- Lycored, 2025:

Lycored announced at IFT FIRST in Chicago the debut of three superstable, nature-based color emulsions—including new yellow and orange shades positioned as replacements for Yellow 5 and 6—while also emphasizing that its lycopene-based red solutions can replace Red 3 and Red 40 across beverages, gummies, sauces, supplements, and fruit preparations. For the U.S. phytonutrients market, this is one of the clearest product-led developments because it directly connects carotenoid-based natural color systems with reformulation demand in the U.S. food and supplement industry, where brands are increasingly looking for stable plant-derived alternatives to synthetic dyes

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- US Phytonutrients Market Policies, Regulations, and Standards

- US Phytonutrients Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- US Phytonutrients Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Type

- Carotenoids- Market Insights and Forecast 2022-2032, USD Million

- Flavonoids- Market Insights and Forecast 2022-2032, USD Million

- Polyphenols- Market Insights and Forecast 2022-2032, USD Million

- Phytosterols/Plant Sterols- Market Insights and Forecast 2022-2032, USD Million

- Specialty Phytonutrients- Market Insights and Forecast 2022-2032, USD Million

- Curcumin- Market Insights and Forecast 2022-2032, USD Million

- Organosulfur Compounds- Market Insights and Forecast 2022-2032, USD Million

- Phytoestrogens- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Functional Positioning

- Antioxidant Support- Market Insights and Forecast 2022-2032, USD Million

- Eye Health- Market Insights and Forecast 2022-2032, USD Million

- Heart Health- Market Insights and Forecast 2022-2032, USD Million

- Immune Support- Market Insights and Forecast 2022-2032, USD Million

- Cognitive Health- Market Insights and Forecast 2022-2032, USD Million

- Skin Health- Market Insights and Forecast 2022-2032, USD Million

- Gut/Metabolic Health- Market Insights and Forecast 2022-2032, USD Million

- Healthy Aging- Market Insights and Forecast 2022-2032, USD Million

- By Regulatory Use Case

- Dietary Supplement Ingredient- Market Insights and Forecast 2022-2032, USD Million

- Conventional Food Ingredient- Market Insights and Forecast 2022-2032, USD Million

- Functional Beverage Ingredient- Market Insights and Forecast 2022-2032, USD Million

- Natural Colorant- Market Insights and Forecast 2022-2032, USD Million

- Cosmetic Active- Market Insights and Forecast 2022-2032, USD Million

- Feed/Animal Nutrition Ingredient- Market Insights and Forecast 2022-2032, USD Million

- By Delivery Technology

- Standard Extract Powder- Market Insights and Forecast 2022-2032, USD Million

- Oil Suspension/Oleoresin- Market Insights and Forecast 2022-2032, USD Million

- Water-Dispersible Format- Market Insights and Forecast 2022-2032, USD Million

- Microencapsulated/Beadlet- Market Insights and Forecast 2022-2032, USD Million

- Emulsified/Liposomal- Market Insights and Forecast 2022-2032, USD Million

- Ready-to-Blend Premix- Market Insights and Forecast 2022-2032, USD Million

- By Source

- Fruits & Vegetables- Market Insights and Forecast 2022-2032, USD Million

- Grains & Cereals- Market Insights and Forecast 2022-2032, USD Million

- Legumes & Pulses- Market Insights and Forecast 2022-2032, USD Million

- Herbs & Spices- Market Insights and Forecast 2022-2032, USD Million

- Oilseeds- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Form

- Dry/Powder- Market Insights and Forecast 2022-2032, USD Million

- Liquid- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- Brand-Owned Websites- Market Insights and Forecast 2022-2032, USD Million

- Third-Party E-commerce Marketplaces- Market Insights and Forecast 2022-2032, USD Million

- Online Health & Wellness Stores- Market Insights and Forecast 2022-2032, USD Million

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- Supermarkets & Hypermarkets- Market Insights and Forecast 2022-2032, USD Million

- Pharmacies & Drug Stores- Market Insights and Forecast 2022-2032, USD Million

- Specialty Health & Nutrition Stores- Market Insights and Forecast 2022-2032, USD Million

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- By End-use Industry

- Food & Beverages- Market Insights and Forecast 2022-2032, USD Million

- Nutraceuticals & Dietary Supplements- Market Insights and Forecast 2022-2032, USD Million

- Pharmaceuticals- Market Insights and Forecast 2022-2032, USD Million

- Cosmetics & Personal Care- Market Insights and Forecast 2022-2032, USD Million

- Animal Nutrition- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Region

- West

- Midwest

- South

- North

- Northeast

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Type

- Market Size & Growth Outlook

- US Carotenoids Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Functional Positioning- Market Insights and Forecast 2022-2032, USD Million

- By Regulatory Use Case- Market Insights and Forecast 2022-2032, USD Million

- By Delivery Technology- Market Insights and Forecast 2022-2032, USD Million

- By Source- Market Insights and Forecast 2022-2032, USD Million

- By Form- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By End-use Industry- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- US Flavonoids Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Functional Positioning- Market Insights and Forecast 2022-2032, USD Million

- By Regulatory Use Case- Market Insights and Forecast 2022-2032, USD Million

- By Delivery Technology- Market Insights and Forecast 2022-2032, USD Million

- By Source- Market Insights and Forecast 2022-2032, USD Million

- By Form- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By End-use Industry- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- US Polyphenols Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Functional Positioning- Market Insights and Forecast 2022-2032, USD Million

- By Regulatory Use Case- Market Insights and Forecast 2022-2032, USD Million

- By Delivery Technology- Market Insights and Forecast 2022-2032, USD Million

- By Source- Market Insights and Forecast 2022-2032, USD Million

- By Form- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By End-use Industry- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- US Phytosterols/Plant Sterols Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Functional Positioning- Market Insights and Forecast 2022-2032, USD Million

- By Regulatory Use Case- Market Insights and Forecast 2022-2032, USD Million

- By Delivery Technology- Market Insights and Forecast 2022-2032, USD Million

- By Source- Market Insights and Forecast 2022-2032, USD Million

- By Form- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By End-use Industry- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- US Specialty Phytonutrients Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Functional Positioning- Market Insights and Forecast 2022-2032, USD Million

- By Regulatory Use Case- Market Insights and Forecast 2022-2032, USD Million

- By Delivery Technology- Market Insights and Forecast 2022-2032, USD Million

- By Source- Market Insights and Forecast 2022-2032, USD Million

- By Form- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By End-use Industry- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- ADM

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Kalsec

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Kemin Industries

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- FutureCeuticals

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- AIDP

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Sabinsa

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- OmniActive Health Technologies

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Euromed USA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Kerry Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Givaudan

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- ADM

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Type |

|

| By Functional Positioning |

|

| By Regulatory Use Case |

|

| By Delivery Technology |

|

| By Source |

|

| By Form |

|

| By Sales Channel |

|

| By End-use Industry |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.