Global Pet Veterinary Diet Market Report: Trends, Growth and Forecast (2026-2032)

By Pet Type (Dogs, Cats, Others), By Product Type (Renal Care Diets, Digestive Care Diets, Urinary Care Diets, Weight Management Diets, Diabetes Care Diets, Dermatology Diets, Mobility & Joint Care Diets, Cardiac Care Diets, Recovery & Critical Care Diets, Dental & Oral Care Diets, Others), By Food Form (Dry Food, Wet Food, Semi-Moist Food, Therapeutic Treats, Others), By Prescription Type (Prescription Veterinary Diets, Non-Prescription Therapeutic Diets), By Sales Channel (Veterinary Clinics & Hospitals, Specialty Pet Stores, Online Prescription Channels, Brand-Owned Websites, Others), By Region (North America, South America, Europe, Middle East & Africa, Asia Pacific) ... Read more

|

Major Players

|

Global Pet Veterinary Diet Market Statistics and Insights, 2026

- Market Size Statistics

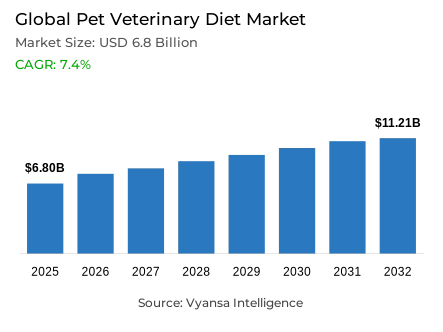

- Pet veterinary diet market size in Global was valued at USD 6.8 billion in 2025 and is estimated at USD 7.3 billion in 2026.

- The market size is expected to grow to USD 11.21 billion by 2032.

- Market to register a CAGR of around 7.4% during 2026-32.

- Product Type Shares

- Renal care diets grabbed market share of 25%.

- Competition

- More than 20 companies are actively engaged in producing pet veterinary diet.

- Top 5 companies acquired around 25% of the market share.

- Dechra Pharmaceuticals, Affinity Petcare, Monge, Royal Canin, Hill’s Pet Nutrition etc., are few of the top companies.

- Prescription Type

- Prescription veterinary diets grabbed 65% of the market.

- Region

- North America leads with a 45% share of the global market.

Global Pet Veterinary Diet Market Outlook

Backed by rising demand for condition-specific pet nutrition, the Global Pet Veterinary Diet Market was valued at USD 6.8 billion in 2025 and is projected to grow from USD 7.3 billion in 2026 to USD 11.21 billion by 2032, at a CAGR of 7.4%. Demand is shaped by diagnosis-led feeding across renal, urinary, digestive, dermatology, diabetes, mobility, cardiac, recovery, and dental care needs across regulated veterinary channels, where diet selection increasingly follows condition assessment, feeding guidance, and monitoring needs.

Renal Care Diets lead the Product Type category with 25% share, reflecting sustained use of kidney-support formulas that require controlled nutrients, digestibility, palatability, and veterinarian recommendation. These products are selected for chronic feeding continuity rather than taste, convenience, or ordinary premium positioning. Their role keeps product demand aligned with formulation depth, structured owner adherence, continuous availability, feeding acceptance, and clear transition guidance across authorized veterinary channels and clinical routines.

Prescription Veterinary Diets hold 65% share under Prescription Type, showing that professional recommendation remains central to adoption. These products move through a clinical purchase pathway, where veterinarians explain the condition, guide transition, define feeding quantity, and monitor response. This keeps prescription pet food linked with clinical need, controlled access, refill discipline, owner understanding, diet suitability, and ongoing nutrition supervision across chronic-use categories.

North America leads with 45% share, supported by mature veterinary care networks, specialty retail, prescription refill systems, and online prescription channels. APPA reports USD 158 billion in U.S. pet industry spending in 2024, including USD 68.3 billion for pet food and treats and USD 41.0 billion for veterinary care and product sales. Through 2032, therapeutic pet diets remain tied to structured feeding continuity, prescription-channel discipline, condition-led product usage, authorized refill access, and sustained diet adherence across chronic care routines and regulated prescription-led nutrition pathways in major pet care systems worldwide.

Global Pet Veterinary Diet Market Growth Driver

Clinical Nutrition Demand Strengthens Therapeutic Adoption

Rising clinical feeding needs form the strongest driver, as dogs and cats increasingly require clinical pet nutrition for renal disease, urinary disorders, digestive sensitivity, obesity, diabetes, dermatology conditions, mobility decline, cardiac support, recovery feeding, and dental care. The demand pattern begins with a health concern, moves through veterinarian recommendation, and continues through feeding discipline, palatability, and repeat use. This keeps veterinary recommended diets connected with long-term care routines rather than discretionary wellness purchasing, expanding structured use of specialized formulas across veterinary clinics, specialty retailers, and authorized refill channels where clinical advice guides product selection and feeding continuity over time consistently.

FDA states that pet food ingredients must be safe and have an appropriate function in the product, while nutrient sources, flavorings, preservatives, and processing aids may require GRAS status or food additive approval for intended use. This formulation discipline is central to disease-specific pet nutrition, as renal, urinary, digestive, dermatology, and diabetes formulas depend on targeted nutrient systems. Product need therefore increases where veterinarians translate symptoms into feeding plans and owners require continuity, suitable formats, and reliable availability after diagnosis. This improves visibility across recurring-use care pathways while keeping product communication tied to clinical function, ingredient purpose, and claim discipline.

Global Pet Veterinary Diet Market Challenge

Premium Pricing Restricts Long-Term Diet Continuity

High product cost remains a key restraint, as premium veterinary nutrition requires specialized formulation, controlled nutrients, palatability work, claim discipline, veterinarian education, and prescription-linked distribution. Renal, urinary, digestive, dermatology, diabetes, and recovery formulas carry higher development and retail costs than standard maintenance products. Owners also manage veterinary visits, diagnostics, medicines, vaccines, grooming, and routine care expenses, making long-term feeding affordability a direct constraint on repeat purchasing across chronic-use diets. The restraint becomes sharper when continuous feeding extends over several months or years after diagnosis and household budget pressure increases across care episodes and visits repeatedly.

Compliance pressure increases the challenge, as therapeutic feeding depends on owners continuing the correct product without frequent mixing, substitution, or delayed refills. FDA reviews claims such as urinary tract health support and low magnesium, while inspections verify manufacturing practices that prevent contamination or adulteration. This raises responsibility for clinical claim substantiation, labeling accuracy, and product consistency. Palatability issues, prescription verification, and refill inconvenience can weaken veterinary diet compliance, limiting wider use among cost-sensitive owners and markets with lower clinic access. Clearer education, accessible pack options, reliable supply, and authorized refills help maintain diet continuity across treatment cycles and reduce avoidable interruption in prescribed feeding routines.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Global Pet Veterinary Diet Market Trend

Condition-Specific Diets Reshape Clinical Nutrition Use

The shift toward condition-specific pet diets is reshaping clinical nutrition use as formulas are organized across renal, urinary, digestive, dermatology, weight management, diabetes, mobility, cardiac, recovery, and dental nutrition. Each condition requires distinct formulation logic, feeding guidance, product texture, and claim discipline. This moves the category from broad therapeutic positioning toward deeper clinical segmentation and increases format management requirements across dry veterinary diet, wet food, therapeutic treats, and supplements designed for different feeding routines, pet acceptance patterns, chronic care requirements, species needs, life-stage tolerance, packaging requirements, and owner transition needs across daily feeding routines and adherence needs consistently worldwide.

Royal Canin identifies veterinary products for diagnosed urinary, renal, and gastrointestinal issues, while Purina positions its veterinary diets and supplements as advanced therapeutic nutrition prescribed by veterinarians for specific pet needs. Purina also cites more than 500 scientists and over 260 published probiotic research articles. These examples show how veterinary diet product development is increasingly linked with condition coverage, format suitability, and evidence-backed communication. The trend creates clearer differences in therapeutic portfolio depth across disease areas while keeping product development tied to clinical function, supply consistency, veterinarian education, feeding acceptance, label clarity, and nutrient adequacy expectations across clinical pet nutrition categories.

Global Pet Veterinary Diet Market Opportunity

Digital Refill Models Improve Prescription Continuity

Expansion of online prescription pet food is improving prescription continuity, as veterinary diets require authorized refills after the first clinic recommendation. A pet placed on renal, urinary, digestive, diabetes, weight-control, dermatology, or recovery nutrition may need repeated purchases over long care cycles. Veterinary e-commerce connects clinics, pet pharmacies, manufacturers, and owners through prescription validation, home delivery, refill reminders, and feeding education. This supports repeat purchase continuity while keeping product use linked with veterinary oversight, condition-specific feeding requirements, authorized access, owner adherence, and continued diet access.

Royal Canin’s online store and subscription access, along with Purina’s professional and retail availability, show how digital channels reduce missed purchases without removing clinical guidance. Improved prescription pet food delivery, product education, and supply reliability reduce refill gaps and improve visibility across recurring-use categories. Digital refill data also supports inventory planning, pack-size decisions, and product availability across clinics, pharmacies, and authorized digital platforms. The expansion remains tied to refill continuity, authorized access, and sustained diet adherence across chronic nutrition routines, where interruptions can weaken feeding discipline and disrupt structured nutrition management. Authorized digital platforms also make refill timing, diet education, and product availability easier to coordinate without changing the veterinarian-led nature of product use overall.

Global Pet Veterinary Diet Market Regional Analysis

By Region

- North America

- South America

- Europe

- Middle East & Africa

- Asia Pacific

Mature veterinary infrastructure, specialty retail access, prescription refill systems, and high pet healthcare awareness position North America as the leading regional base, with 45% share of the Global Pet Veterinary Diet Market. The region benefits from clinic-led nutrition guidance, structured access to veterinary clinics and hospitals, pet pharmacies, specialty stores, and digital refill channels. APPA reports 95 million U.S. pet-owning households, supporting recurring nutrition demand where clinical recommendation and authorized access are well established. This regional structure improves visibility across prescription-led channels and links leadership with access quality, care continuity, and refill discipline.

Europe provides the strongest broadening base outside North America. FEDIAF reports 139 million pet-owning households, 299 million pets, EUR 29.2 billion in annual pet food sales, and 9.1 million tonnes of volume. This creates a large foundation for Europe pet veterinary diet market expansion as veterinary awareness, specialty retail, and therapeutic feeding education deepen. Continued use of online prescription pet diets and condition-led portfolios can support regional adoption through improved refill access and channel depth. The regional outlook remains tied to clinic access, authorized product availability, and sustained diet adherence across chronic care routines across mature and developing veterinary nutrition channels over the forecast period ahead.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Global Pet Veterinary Diet Market Segmentation Analysis

By Product Type

- Renal Care Diets

- Digestive Care Diets

- Urinary Care Diets

- Weight Management Diets

- Diabetes Care Diets

- Dermatology Diets

- Mobility & Joint Care Diets

- Cardiac Care Diets

- Recovery & Critical Care Diets

- Dental & Oral Care Diets

- Others

The leading Product Type segment is Renal Care Diets, holding 25% of the Global Pet Veterinary Diet Market. This leadership reflects the long-term nature of kidney support pet food, where controlled nutrients, digestibility, palatability, and daily feeding continuity shape use. Renal formulas differ from ordinary senior diets through protein quality, phosphorus control, sodium management, energy density, and acceptance needs, especially among cats and older pets. Their position is reinforced by veterinarian recommendation, chronic feeding duration, repeat refill behavior after diagnosis, and the need for continuous product availability in authorized channels and routine care settings across major markets.

Renal formulas need clear feeding directions, product identity, net quantity, ingredient communication, and storage protection to maintain owner adherence. Dry formats support routine use, while wet textures support hydration and acceptance for selective or older pets. Smaller packs can support trial feeding before longer use. This segment maintains long-term relevance as wet formats, dry options, transition guidance, and refill systems become more common for chronic kidney nutrition across authorized channels and veterinary-linked refill networks. The category sets a clinical benchmark for urinary, digestive, dermatology, mobility, diabetes, and recovery portfolios where formulation precision and sustained intake remain essential for diet acceptance and chronic-use stability.

By Prescription Type

- Prescription Veterinary Diets

- Non-Prescription Therapeutic Diets

The Prescription Veterinary Diets category leads under Prescription Type, holding 65% of the Global Pet Veterinary Diet Market. This position reflects the role of diagnosis, veterinarian recommendation, product authorization, owner education, and feeding follow-up in therapeutic nutrition. Owners may recognize symptoms, yet they often need professional guidance to distinguish renal, urinary, digestive, diabetes, dermatology, mobility, and weight management formulas. This purchase structure reduces selection uncertainty and keeps controlled access pet food aligned with clinical needs across repeat care cycles, where consistent feeding influences nutrition continuity, condition management, and owner understanding.

Prescription diets also require balanced access. Products must remain linked with veterinary guidance, while refills need enough convenience to maintain feeding continuity. Online authorization, subscription refills, and direct-to-home delivery improve access without removing professional oversight. Pet pharmacy prescription diets and clinic-dispensed products therefore depend on transparency, product availability, palatability, and clear instructions. This structure supports disciplined usage and refill behavior across chronic care routines without shifting the category into uncontrolled self-selection. Better prescription-channel consistency reduces diet interruption and keeps product use aligned with veterinarian-led feeding plans, refill validation, and long-term adherence across chronic feeding schedules. The segment remains defined by professional oversight, structured refills, and clear diet instructions overall.

Market Players in Global Pet Veterinary Diet Market

These market players maintain a significant presence in the Global pet veterinary diet market and contribute to its ongoing evolution.

- Dechra Pharmaceuticals

- Affinity Petcare

- Monge

- Royal Canin

- Hill’s Pet Nutrition

- Purina Pro Plan Veterinary Diets

- Virbac

- Farmina Pet Foods

- VAFO Group

- SANYpet

- Vobra Special Petfoods

- VetExpert

- Happy Dog

- Rayne Clinical Nutrition

- General Mills / Blue Buffalo

Market News & Updates

- Hill’s Pet Nutrition, 2025:

Hill’s Pet Nutrition announced new and enhanced Prescription Diet products at VMX 2025. The update includes Prescription Diet formulas using ActivBiome+ technology and products designed to help veterinarians manage pets with multiple conditions. The launch expands Hill’s therapeutic nutrition portfolio across digestive, dermatology, kidney, and condition-specific veterinary diet applications.

- Virbac, 2025:

Virbac launched Vikaly in September 2025 as a medicated food for cats with chronic kidney disease. The product combines renal kibble with medication for proteinuria management in adult and senior cats. The launch adds a new therapeutic nutrition format to Virbac’s veterinary diet portfolio in Europe.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Global Pet Veterinary Diet Market Policies, Regulations, and Standards

- Global Pet Veterinary Diet Production (Thousand Ton) Trend 2022-2032

- Global Pet Veterinary Diet Production (Thousand Ton) Trend By Product Type

- Renal Care Diets

- Digestive Care Diets

- Urinary Care Diets

- Weight Management Diets

- Diabetes Care Diets

- Dermatology Diets

- Mobility & Joint Care Diets

- Cardiac Care Diets

- Recovery & Critical Care Diets

- Dental & Oral Care Diets

- Company Wise Production Plants and Statistics

- Installed Production Capacity

- Actual Production

- Planned Production Target

- Global Pet Veterinary Diet Production (Thousand Ton) Trend By Product Type

- Global Pet Veterinary Diet Pricing Analysis 2022-2032

- Global Pet Veterinary Diet Pricing Trend (USD/Ton) 2022-2032

- Global Pet Veterinary Diet Trend (USD/Ton) By Regions 2022-2032

- North America

- South America

- Europe

- Middle East & Africa

- Asia Pacific

- Global Feed Probiotics Pricing Trend (USD/Ton) By Product Type 2022-2032

- Renal Care Diets

- Digestive Care Diets

- Urinary Care Diets

- Weight Management Diets

- Diabetes Care Diets

- Dermatology Diets

- Mobility & Joint Care Diets

- Cardiac Care Diets

- Recovery & Critical Care Diets

- Dental & Oral Care Diets

- Global Pet Veterinary Diet Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Global Pet Veterinary Diet Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold (Thousand Tons)

- Market Segmentation & Growth Outlook

- By Pet Type

- Dogs- Market Insights and Forecast 2022-2032, USD Million

- Cats- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Product Type

- Renal Care Diets- Market Insights and Forecast 2022-2032, USD Million

- Digestive Care Diets- Market Insights and Forecast 2022-2032, USD Million

- Urinary Care Diets- Market Insights and Forecast 2022-2032, USD Million

- Weight Management Diets- Market Insights and Forecast 2022-2032, USD Million

- Diabetes Care Diets- Market Insights and Forecast 2022-2032, USD Million

- Dermatology Diets- Market Insights and Forecast 2022-2032, USD Million

- Mobility & Joint Care Diets- Market Insights and Forecast 2022-2032, USD Million

- Cardiac Care Diets- Market Insights and Forecast 2022-2032, USD Million

- Recovery & Critical Care Diets- Market Insights and Forecast 2022-2032, USD Million

- Dental & Oral Care Diets- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Food Form

- Dry Food- Market Insights and Forecast 2022-2032, USD Million

- Wet Food- Market Insights and Forecast 2022-2032, USD Million

- Semi-Moist Food- Market Insights and Forecast 2022-2032, USD Million

- Therapeutic Treats- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Prescription Type

- Prescription Veterinary Diets- Market Insights and Forecast 2022-2032, USD Million

- Non-Prescription Therapeutic Diets- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Veterinary Clinics & Hospitals- Market Insights and Forecast 2022-2032, USD Million

- Specialty Pet Stores- Market Insights and Forecast 2022-2032, USD Million

- Online Prescription Channels- Market Insights and Forecast 2022-2032, USD Million

- Brand-Owned Websites- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Region

- North America

- South America

- Europe

- Middle East & Africa

- Asia Pacific

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Pet Type

- Market Size & Growth Outlook

- North America Pet Veterinary Diet Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold (Thousand Tons)

- Market Segmentation & Growth Outlook

- By Pet Type- Market Insights and Forecast 2022-2032, USD Million

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- By Food Form- Market Insights and Forecast 2022-2032, USD Million

- By Prescription Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Country

- The US

- Canada

- Mexico

- Rest of North America

- The US Pet Veterinary Diet Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold (Thousand Tons)

- Market Segmentation & Growth Outlook

- By Pet Type- Market Insights and Forecast 2022-2032, USD Million

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- By Food Form- Market Insights and Forecast 2022-2032, USD Million

- By Prescription Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Canada Pet Veterinary Diet Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold (Thousand Tons)

- Market Segmentation & Growth Outlook

- By Pet Type- Market Insights and Forecast 2022-2032, USD Million

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- By Food Form- Market Insights and Forecast 2022-2032, USD Million

- By Prescription Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Mexico Pet Veterinary Diet Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold (Thousand Tons)

- Market Segmentation & Growth Outlook

- By Pet Type- Market Insights and Forecast 2022-2032, USD Million

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- By Food Form- Market Insights and Forecast 2022-2032, USD Million

- By Prescription Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Market Size & Growth Outlook

- South America Pet Veterinary Diet Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold (Thousand Tons)

- Market Segmentation & Growth Outlook

- By Pet Type- Market Insights and Forecast 2022-2032, USD Million

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- By Food Form- Market Insights and Forecast 2022-2032, USD Million

- By Prescription Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Country

- Brazil

- Argentina

- Rest of South America

- Brazil Pet Veterinary Diet Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold (Thousand Tons)

- Market Segmentation & Growth Outlook

- By Pet Type- Market Insights and Forecast 2022-2032, USD Million

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- By Food Form- Market Insights and Forecast 2022-2032, USD Million

- By Prescription Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Argentina Pet Veterinary Diet Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold (Thousand Tons)

- Market Segmentation & Growth Outlook

- By Pet Type- Market Insights and Forecast 2022-2032, USD Million

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- By Food Form- Market Insights and Forecast 2022-2032, USD Million

- By Prescription Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Market Size & Growth Outlook

- Europe Pet Veterinary Diet Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold (Thousand Tons)

- Market Segmentation & Growth Outlook

- By Pet Type- Market Insights and Forecast 2022-2032, USD Million

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- By Food Form- Market Insights and Forecast 2022-2032, USD Million

- By Prescription Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Country

- Germany

- The UK

- France

- Italy

- Spain

- Rest of Europe

- Germany Pet Veterinary Diet Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold (Thousand Tons)

- Market Segmentation & Growth Outlook

- By Pet Type- Market Insights and Forecast 2022-2032, USD Million

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- By Food Form- Market Insights and Forecast 2022-2032, USD Million

- By Prescription Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- The UK Pet Veterinary Diet Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold (Thousand Tons)

- Market Segmentation & Growth Outlook

- By Pet Type- Market Insights and Forecast 2022-2032, USD Million

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- By Food Form- Market Insights and Forecast 2022-2032, USD Million

- By Prescription Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- France Pet Veterinary Diet Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold (Thousand Tons)

- Market Segmentation & Growth Outlook

- By Pet Type- Market Insights and Forecast 2022-2032, USD Million

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- By Food Form- Market Insights and Forecast 2022-2032, USD Million

- By Prescription Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Italy Pet Veterinary Diet Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold (Thousand Tons)

- Market Segmentation & Growth Outlook

- By Pet Type- Market Insights and Forecast 2022-2032, USD Million

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- By Food Form- Market Insights and Forecast 2022-2032, USD Million

- By Prescription Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Spain Pet Veterinary Diet Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold (Thousand Tons)

- Market Segmentation & Growth Outlook

- By Pet Type- Market Insights and Forecast 2022-2032, USD Million

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- By Food Form- Market Insights and Forecast 2022-2032, USD Million

- By Prescription Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Market Size & Growth Outlook

- Middle East & Africa Pet Veterinary Diet Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold (Thousand Tons)

- Market Segmentation & Growth Outlook

- By Pet Type- Market Insights and Forecast 2022-2032, USD Million

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- By Food Form- Market Insights and Forecast 2022-2032, USD Million

- By Prescription Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Country

- The UAE

- Saudi Arabia

- South Africa

- Egypt

- Rest of Middle East and Africa

- The UAE Pet Veterinary Diet Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold (Thousand Tons)

- Market Segmentation & Growth Outlook

- By Pet Type- Market Insights and Forecast 2022-2032, USD Million

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- By Food Form- Market Insights and Forecast 2022-2032, USD Million

- By Prescription Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Saudi Arabia Pet Veterinary Diet Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold (Thousand Tons)

- Market Segmentation & Growth Outlook

- By Pet Type- Market Insights and Forecast 2022-2032, USD Million

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- By Food Form- Market Insights and Forecast 2022-2032, USD Million

- By Prescription Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- South Africa Pet Veterinary Diet Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold (Thousand Tons)

- Market Segmentation & Growth Outlook

- By Pet Type- Market Insights and Forecast 2022-2032, USD Million

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- By Food Form- Market Insights and Forecast 2022-2032, USD Million

- By Prescription Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Egypt Pet Veterinary Diet Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold (Thousand Tons)

- Market Segmentation & Growth Outlook

- By Pet Type- Market Insights and Forecast 2022-2032, USD Million

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- By Food Form- Market Insights and Forecast 2022-2032, USD Million

- By Prescription Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Market Size & Growth Outlook

- Asia Pacific Pet Veterinary Diet Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold (Thousand Tons)

- Market Segmentation & Growth Outlook

- By Pet Type- Market Insights and Forecast 2022-2032, USD Million

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- By Food Form- Market Insights and Forecast 2022-2032, USD Million

- By Prescription Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Country

- China

- India

- Japan

- South Korea

- Australia

- Indonesia

- Rest of Asia Pacific

- China Pet Veterinary Diet Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold (Thousand Tons)

- Market Segmentation & Growth Outlook

- By Pet Type- Market Insights and Forecast 2022-2032, USD Million

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- By Food Form- Market Insights and Forecast 2022-2032, USD Million

- By Prescription Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Pet Veterinary Diet Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold (Thousand Tons)

- Market Segmentation & Growth Outlook

- By Pet Type- Market Insights and Forecast 2022-2032, USD Million

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- By Food Form- Market Insights and Forecast 2022-2032, USD Million

- By Prescription Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Japan Pet Veterinary Diet Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold (Thousand Tons)

- Market Segmentation & Growth Outlook

- By Pet Type- Market Insights and Forecast 2022-2032, USD Million

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- By Food Form- Market Insights and Forecast 2022-2032, USD Million

- By Prescription Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- South Korea Pet Veterinary Diet Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold (Thousand Tons)

- Market Segmentation & Growth Outlook

- By Pet Type- Market Insights and Forecast 2022-2032, USD Million

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- By Food Form- Market Insights and Forecast 2022-2032, USD Million

- By Prescription Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Australia Pet Veterinary Diet Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold (Thousand Tons)

- Market Segmentation & Growth Outlook

- By Pet Type- Market Insights and Forecast 2022-2032, USD Million

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- By Food Form- Market Insights and Forecast 2022-2032, USD Million

- By Prescription Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Indonesia Pet Veterinary Diet Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold (Thousand Tons)

- Market Segmentation & Growth Outlook

- By Pet Type- Market Insights and Forecast 2022-2032, USD Million

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- By Food Form- Market Insights and Forecast 2022-2032, USD Million

- By Prescription Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Royal Canin

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Hill’s Pet Nutrition

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Purina Pro Plan Veterinary Diets

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Virbac

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Farmina Pet Foods

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Dechra Pharmaceuticals

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Affinity Petcare

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Monge

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- VAFO Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- SANYpet

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Vobra Special Petfoods

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- VetExpert

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Happy Dog

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Rayne Clinical Nutrition

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- General Mills / Blue Buffalo

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Royal Canin

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Pet Type |

|

| By Product Type |

|

| By Food Form |

|

| By Prescription Type |

|

| By Sales Channel |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.