US Paediatric Consumer Health Market Report: Trends, Growth and Forecast (2026-2032)

By Product Type (Paediatric Analgesics (Paediatric Acetaminophen, Paediatric Aspirin, Paediatric Combination Products Analgesics, Paediatric Dipyrone, Paediatric Ibuprofen, Paediatric Naproxen), Paediatric Cough, Cold and Allergy Remedies (Paediatric Allergy Remedies, Paediatric Cough/Cold Remedies), Paediatric Digestive Remedies (Paediatric Diarrhoeal Remedies, Paediatric Indigestion and Heartburn Remedies, Paediatric Laxatives, Paediatric Motion Sickness Remedies), Paediatric Dermatologicals, Nappy (Diaper) Rash Treatments, Paediatric Vitamins and Dietary Supplements), By Dosage Form (Liquid Syrups, Chewable Tablets, Drops, Powders/Sachets, Gummies, Topical Creams & Ointments), By Age Group (Infants & Toddlers (0-3 Years), Children (4-12 Years), Adolescents (13-18 Years)), By Treatment Type (Acute Treatment, Chronic Condition Management, Genetic & Rare Disease Management), By Sales Channel (Retail Online (Online Pharmacies, E-commerce Platforms, Brand Websites), Retail Offline (Hospital Pharmacies, Retail Pharmacies / Drugstores, Supermarkets & Hypermarkets, Specialty Baby Stores)), By Region (West, Midwest, South, North, Northeast) ... Read more

|

Major Players

|

US Paediatric Consumer Health Market Statistics and Insights, 2026

- Market Size Statistics

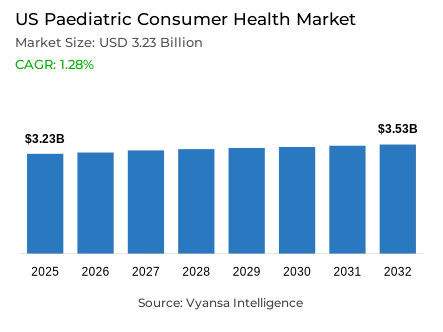

- Paediatric consumer health market size in US was valued at USD 3.23 billion in 2025 and is estimated at USD 3.32 Billion in 2026.

- The market size is expected to grow to USD 3.53 billion by 2032.

- Market to register a CAGR of around 1.28% during 2026-32.

- Product Type Shares

- Paediatric cough, cold and allergy remedies grabbed market share of 30%.

- Competition

- More than 20 companies are actively engaged in producing paediatric consumer health in US.

- Top 5 companies acquired around 35% of the market share.

- Haleon US Inc, Walgreen Co, MRO Maryruth LLC, McNeil Consumer & Specialty Pharmaceuticals, Bayer Corp etc., are few of the top companies.

- Sales Channel

- Retail offline grabbed 70% of the market.

US Paediatric Consumer Health Market Outlook

The US Paediatric consumer health market was valued at 3.23 billion US dollars in 2025 and is expected to grow from 3.32 billion US dollars in 2026 to 3.53 billion US dollars in 2032, with a compound annual growth rate of 1.28% during the forecast period. The category is recording modest growth, with the market increasing in value rather than recording widespread volume acceleration. The 2025 market is characterised by varied performance, with stronger commercial progress in vitamins, dietary supplements, and digestive care, although the more mature paediatric pain segment continues to suffer from a lack of product innovation and increasing pressure from private label.

Category trends are increasingly driven by parents’ preferences for branded products and cleaner product formulations. The greater range of drug-free and free-from products available is helping brands stand out in a competitive retail environment, especially if parents associate these characteristics with safe and reassuring use for their children. This is driving products associated with prevention, hydration, nutrition, digestive health, and wellness, as opposed to products associated with symptom relief.

Category trends are also being driven by changes in illness patterns and retail channels. A harsher cough, cold, and flu season in early 2025 is helping to stabilise the paediatric cough, cold, and allergy remedy category, which holds 30% of the total product type share. At the same time, the retail landscape is evolving, with retail online becoming a more dynamic way for consumers to discover products and repurchase, although retail offline still holds 70% of the total sales and is integral to the trust-based purchasing behavior associated with this category.

However, the overall outlook is one of continued selective but positive growth. The paediatric consumer health market continues to enjoy strong end-user demand for vitamins and supplements, especially where brands have been able to position themselves as offering clear benefit statements and attractive delivery systems combined with strong positioning of their ingredients as clean and safe. At the same time, the market is also having to contend with increasing issues of social media health misinformation, supplements and marketing to minors, and safety issues surrounding some of the actives used within the market. Therefore, brand and professional endorsement remain key areas of strength for brands to compete on within this market.

US Paediatric Consumer Health Market Growth DriverClean-Label and Drug-Free Formulations Are Strengthening Parental Confidence and Brand Preference

The most consistent and reliable growth drivers of the paediatric consumer health market in the US is the increasing preference of parents for drug-free and clearly branded formulations that they can feel safe and comfortable giving to their children. Value growth within the paediatric market is increasingly being driven by products that have been able to position themselves as safe and more in tune with the world of wellness and health.

The 2024 to 2025 flu season is considered a season of high severity as per the classification of the Centers for Disease Control and Prevention, and the season is expected to have 51 million cases of illness, 23 million medical visits, 710,000 hospitalizations, and 45,000 deaths recorded within the season. The high illness environment ensures that families are consistently engaged in pediatric remedy and supplement categories, and the cleaner and more naturally positioned formulations provide parents a stronger and more credible reason to choose the brand over the regular and less expensive options at the point of purchase.

US Paediatric Consumer Health Market ChallengeOnline Health Misinformation Is Elevating Reputational and Regulatory Risk Across the Category

A key challenge facing the US Paediatric consumer health market is the rising risk of children and teenagers being exposed to false, misleading, and potentially damaging health-related or supplement-related content across social media channels. In particular, the spread of false body image content, the misuse of laxatives, and exaggerated weight management practices are increasing the risk of paediatric-related products being misunderstood or misused by impressionable younger consumers. Accordingly, there is a notable reputational risk at play across the category, particularly with respect to the need for safe and effective safety communication, especially with respect to products that can be purchased directly over the counter without any professional guidance.

The regulatory environment with respect to the issue of health misinformation has taken a notably firm turn. New York has now become the first state in the country to ban the sale of weight loss or muscle-building supplements to minors. The legislation has already taken effect as of April 2024. Moreover, the FDA has confirmed that dietary supplements are not approved prior to marketing, except when the manufacturer introduces new ingredients. Accordingly, the above developments serve to highlight the structural weaknesses of the broader Paediatric Consumer Health Supplement category.

Unlock Market Intelligence

Explore the market potential with our data-driven report

US Paediatric Consumer Health Market TrendRetail Online Is Continuing to Reshape the Paediatric Product Discovery and Purchase Journey

A prominent and commercially relevant trend, as far as the US-based paediatric consumer health market is concerned, relates to the increasing role of retail online and omnichannel retail as a means of shaping the way families evaluate, consider, and ultimately purchase child health-related products. To be sure, the role of the pharmacy channel and the hypermarket channel remains highly relevant as a means of delivering health-related products, as these channels continue to be highly respected sources of relevant products. However, the role of retail online continues to grow as a commercially relevant channel, driven by the ability of these channels to offer convenience, a wide range of products, repeat purchase convenience, as well as fast delivery. In particular, the ability of retail online channels to play a more prominent role has the potential to greatly benefit the newly emerging wellness-based brand, as these companies must rely on digital channels, clean and uncluttered brand messages, as well as broad appeal across the broader health landscape, rather than the more traditional pharmacy channel.

According to the US Census Bureau, total retail online sales are predicted to reach 1,233.7 billion US dollars in 2025, with retail online sales increasing by 5.4% from the prior year, or 2024. In particular, retail online sales comprise 16.4% of total retail trade. In the fourth quarter of 2025, retail online sales totaled 316.1 billion US dollars, increasing by 5.3% from the same period of the prior year. These figures clearly demonstrate the increasing commercial relevance of retail online as a means of shaping the way families evaluate, consider, and ultimately purchase child health-related products, as the channel continues to gain commercially relevant ground, even as the offline channel maintains the highest percentage of total sales volume.

US Paediatric Consumer Health Market OpportunityNaturally Positioned Supplements Represent the Strongest Available White Space

There is a clearly defined and commercially viable opportunity to be found within the space of paediatric vitamins and supplements, specifically as it relates to the promotion of ‘natural,’ ‘preventive,’ and ‘clean label’ health and wellbeing credentials. Parents are increasingly incorporating these types of products into the daily lives of their children to support the health of the digestive system, immune system, hydration levels, and quality of sleep, and many of them are doing so on the basis of the proposition that such products are more ‘gentle’ and ‘natural’ alternatives to more conventional pharmaceutical solutions.

The opportunity is best served through investment in higher levels of product credibility and professional alignment. The FDA has issued educational tools on the New Dietary Ingredient Notification process, aimed at improving the quality of dietary supplement notifications. The American Academy of Pediatrics has said, “Most healthy children get the nutrients they need from a healthy, well-balanced diet. In fact, vitamin supplements are rarely needed, except when a specific clinical need has been diagnosed. Parents should consult with a pediatrician before initiating vitamin supplements.” This provides a highly defined space, both commercially and from a position of credibility, for better-formulated, more clearly communicated, and pediatrician-recommended brands as opposed to the more general vitamin supplement category.

Unlock Market Intelligence

Explore the market potential with our data-driven report

US Paediatric Consumer Health Market Segmentation Analysis

By Product Type

- Paediatric Analgesics

- Paediatric Acetaminophen

- Paediatric Aspirin

- Paediatric Combination Products Analgesics

- Paediatric Dipyrone

- Paediatric Ibuprofen

- Paediatric Naproxen

- Paediatric Cough, Cold and Allergy Remedies

- Paediatric Allergy Remedies

- Paediatric Cough/Cold Remedies

- Paediatric Digestive Remedies

- Paediatric Diarrhoeal Remedies

- Paediatric Indigestion and Heartburn Remedies

- Paediatric Laxatives

- Paediatric Motion Sickness Remedies

- Paediatric Dermatologicals

- Nappy (Diaper) Rash Treatments

- Paediatric Vitamins and Dietary Supplements

The segment with the highest market share, as far as the Product Type segment of the market is concerned, is Paediatric Cough, Cold, and Allergy Remedies, which holds a 30% share of the total market. The reason for this leadership position lies in the simple, yet undeniable, truth that, as the pressures of illness increase, the need for fast access to relief from the symptoms of illness remains one of the most immediately relevant, as well as the most frequently occurring, reason why parents seek child health products.

The Centers for Disease Control and Prevention rate this flu season as high severity for the years 2024 and 2025, which includes an estimated 51 million illnesses, 23 million medical visits, and 710,000 hospitalizations for the flu season. This high rate of illness severity is why cough, cold, and allergy remedies maintain their position at number one in the total product type segment. Although vitamins, digestive aids, and clean label wellness products are making significant market inroads, this segment remains at the heart of this market segment because it continues to address critical and timely issues in children’s health that require immediate and unprejudiced decision-making.

By Sales Channel

- Retail Online

- Online Pharmacies

- E-commerce Platforms

- Brand Websites

- Retail Offline

- Hospital Pharmacies

- Retail Pharmacies / Drugstores

- Supermarkets & Hypermarkets

- Specialty Baby Stores

The segment that holds the highest market share in this segment is Retail Offline, which holds 70% market share in total market size. This segment remains at the top because children’s purchasing decisions are fundamentally trust-based in nature. Parents prefer to purchase children’s health-related products in familiar retail environments where they feel comfortable comparing brands, examining product packaging in more detail, and making decisions confidently and well-informed, aided by in-store pharmacy staff where necessary.

According to the US Census Bureau, retail online accounted for 16.4% of total retail sales in 2025. In addition, retail online sales for the fourth quarter of 2025 reached USD 316.1 billion. These figures prove that retail online is rapidly and significantly gaining traction in this market segment. However, they also prove that the vast majority of children’s consumer health-related purchases remain anchored in traditional retail environments where immediate product availability, brand familiarity, and reassurance of a trusted in-store purchasing experience remain at the heart of how most US families address children’s purchasing decisions.

List of Companies Covered in US Paediatric Consumer Health Market

The companies listed below are highly influential in the US paediatric consumer health market, with a significant market share and a strong impact on industry developments.

- Haleon US Inc

- Walgreen Co

- MRO Maryruth LLC

- McNeil Consumer & Specialty Pharmaceuticals

- Bayer Corp

- Abbott Laboratories Inc

- Zarbee's Inc

- Unilever Group

- Walmart Inc

- CVS Health Corp

Competitive Landscape

The US paediatric consumer health market in 2025 is led by McNeil Consumer & Specialty Pharmaceuticals, whose trusted brands Tylenol, Motrin, Benadryl, and Desitin maintain strong positions across analgesics, cough and allergy remedies, and nappy rash treatments. Unilever Group is a key challenger in paediatric vitamins and dietary supplements, driven by SmartyPants and OLLY, which compete through appealing gummy formats, bold packaging, and benefit-led messaging. Competition is increasingly shaped by demand for clean-label, drug-free, and natural formulations, with brands such as Zarbee’s, Genexa, MaryRuth Organics, and Dr. Rydland’s Herbal Formula gaining attention. Hypermarkets, pharmacies, and e-commerce remain critical channels, while social media and personalised digital marketing are helping newer brands expand visibility and influence purchase decisions.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- United States Paediatric Consumer Health Market Policies, Regulations, and Standards

- United States Paediatric Consumer Health Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- United States Paediatric Consumer Health Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product Type

- Paediatric Analgesics- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Acetaminophen- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Aspirin- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Combination Products Analgesics- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Dipyrone- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Ibuprofen- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Naproxen- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Cough, Cold and Allergy Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Allergy Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Cough/Cold Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Digestive Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Diarrhoeal Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Indigestion and Heartburn Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Laxatives- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Motion Sickness Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Dermatologicals- Market Insights and Forecast 2022-2032, USD Million

- Nappy (Diaper) Rash Treatments- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Vitamins and Dietary Supplements- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Analgesics- Market Insights and Forecast 2022-2032, USD Million

- By Dosage Form

- Liquid Syrups- Market Insights and Forecast 2022-2032, USD Million

- Chewable Tablets- Market Insights and Forecast 2022-2032, USD Million

- Drops- Market Insights and Forecast 2022-2032, USD Million

- Powders/Sachets- Market Insights and Forecast 2022-2032, USD Million

- Gummies- Market Insights and Forecast 2022-2032, USD Million

- Topical Creams & Ointments- Market Insights and Forecast 2022-2032, USD Million

- By Age Group

- Infants & Toddlers (0-3 Years)- Market Insights and Forecast 2022-2032, USD Million

- Children (4-12 Years)- Market Insights and Forecast 2022-2032, USD Million

- Adolescents (13-18 Years)- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type

- Acute Treatment- Market Insights and Forecast 2022-2032, USD Million

- Chronic Condition Management- Market Insights and Forecast 2022-2032, USD Million

- Genetic & Rare Disease Management- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- Online Pharmacies- Market Insights and Forecast 2022-2032, USD Million

- E-commerce Platforms- Market Insights and Forecast 2022-2032, USD Million

- Brand Websites- Market Insights and Forecast 2022-2032, USD Million

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- Hospital Pharmacies- Market Insights and Forecast 2022-2032, USD Million

- Retail Pharmacies / Drugstores- Market Insights and Forecast 2022-2032, USD Million

- Supermarkets & Hypermarkets- Market Insights and Forecast 2022-2032, USD Million

- Specialty Baby Stores

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- By Region

- West

- Midwest

- South

- North

- Northeast

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Product Type

- Market Size & Growth Outlook

- United States Paediatric Analgesics Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Dosage Form- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- United States Paediatric Cough, Cold and Allergy Remedies Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Dosage Form- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- United States Paediatric Digestive Remedies Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Dosage Form- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- United States Paediatric Dermatologicals Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Dosage Form- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- United States Nappy (Diaper) Rash Treatments Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Dosage Form- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- United States Paediatric Vitamins and Dietary Supplements Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Dosage Form- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- McNeil Consumer & Specialty Pharmaceuticals

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Bayer Corp

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Abbott Laboratories Inc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Zarbee's Inc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Unilever Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Haleon US Inc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Walgreen Co

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- MRO Maryruth LLC

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Walmart Inc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- CVS Health Corp

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- McNeil Consumer & Specialty Pharmaceuticals

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Dosage Form |

|

| By Age Group |

|

| By Treatment Type |

|

| By Sales Channel |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.