US Diagnostic Labs Market Report: Trends, Growth and Forecast (2026-2032)

By Lab Type (Single/Independent Laboratories, Hospital-based Laboratories, Physician Office Laboratories, Others), By Testing Services (Physiological Function Testing, General & Clinical Testing, Esoteric Testing, Specialized Testing, Non-invasive Prenatal Testing, COVID-19 Testing, Others), By Disease (Cardiology, Oncology, Neurology, Orthopedics, Gastroenterology, Gynecology, Odontology, Others), By Revenue Source (Healthcare Plan, Out-of-Pocket, Public System), By Test Type (Pathology, Radiology), By End User (Referrals, Walk-ins, Corporate Clients), By Region (West, Midwest, South, North, Northeast) ... Read more

|

Major Players

|

US Diagnostic Labs Market Statistics and Insights, 2026

- Market Size Statistics

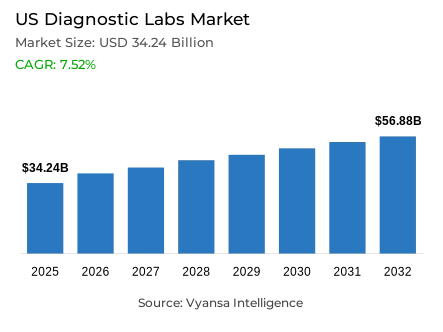

- Diagnostic labs market size in US was estimated at USD 34.24 billion in 2025.

- The market size is expected to grow to USD 56.88 billion by 2032.

- Market to register a CAGR of around 7.52% during 2026-32.

- Lab Type Shares

- Single/independent laboratories grabbed market share of 50%.

- Competition

- Diagnostic labs in US is currently being catered to by more than 15 companies.

- Top 5 companies acquired around 60% of the market share.

- Kaiser Permanente Laboratories, Cleveland Clinic Laboratories, Northwell Health Labs, Labcorp, Quest Diagnostics etc., are few of the top companies.

- Testing Services

- General & clinical testing grabbed 40% of the market.

US Diagnostic Labs Market Outlook

The United States diagnostic lab market is estimated to be worth USD 34.24 billion in 2025 and USD 56.88 billion in 2032, with a compound annual growth rate of about 7.52% between 2026 and 2032. This growth is propelled by the increasing burden of chronic disease, with an estimated 60% of the population affected and about 40% diabetic or pre-diabetic. Diseases such as diabetes, cardiovascular disease, and cancer require regular blood tests and screenings, significantly boosting laboratory volumes.

Approximately 70% of all medical decisions are based on laboratory test results, making diagnostics essential to modern healthcare delivery. U.S. facilities conduct billions of tests each year to support comprehensive care, while health agencies increasingly emphasize early detection and continuous monitoring.

Single-ownership and independent lab dominate the market with a 50% share. Quest Diagnostics and Labcorp together perform about one-quarter of all U.S. tests. General and clinical testing services represent the largest segment with a 50% share, driven by routine diagnostics across care settings.

Workforce shortages remain a major challenge, with vacancy rates between 7-11% and up to 25% in some regions. Rising retirements and slow workforce replenishment persist. To address this, nearly 90% of lab workers report a need for increased automation, and 91% see AI as essential to meeting patient-care demand and managing labor costs that account for 40-60% of operating budgets.

US Diagnostic Labs Market Growth Driver

Rising Chronic Disease Prevalence Accelerating Diagnostic Testing Requirements

The requirement for diagnostic lab work is largely fueled by the demand of an aging society with a high incidence of chronic diseases. At present, close to 60% of the total population is affected by at least one chronic disease, with 40% being diabetic or prediabetic, requiring constant monitoring of the condition. Chronic diseases such as diabetes, heart conditions, and cancers require constant blood tests as well as general screenings, thereby increasing the amount of lab tests. The management of diabetes on its own requires regular glucose checks and Hemoglobin A1c, which adds significant value to the total laboratory workloads. The importance of laboratory diagnostics in preventive-care systems is becoming more and more significant due to the growing focus of health agencies on early diagnosis and continuous monitoring of chronic diseases.

The results of laboratory tests are the basis of about 70% of all medical decisions, which is why the role of diagnostics in modern healthcare provision cannot be overestimated. Such a high dependency implies that as the prevalence of chronic diseases keeps increasing, clinicians will order more tests to make accurate diagnosis, choose the right therapy, and manage the disease. The result is a continued increase in laboratory testing volumes, and U.S. facilities currently conduct billions of tests each year to assist in holistic patient care. As a result, the chronic disease burden of the country is directly converted into increased use of diagnostic laboratory services, which makes it one of the key factors that contribute to the ongoing growth of the sector.

US Diagnostic Labs Market Challenge

Critical Laboratory Workforce Shortages Constraining Operational Capacity

The persistent lack of laboratory personnel is a major problem that endangers the efficiency and quality of services in the diagnostic market. Although the pandemic pressures have subsided, the average laboratory vacancy rates remain within the range of 7-11%, and some areas have reached 25%, which is significantly higher than historical levels. According to market surveys, despite the fact that staffing conditions have improved compared to the extreme shortages seen in 2020-2021, the level of vacancies is significantly higher than it was before the pandemic. This chronic shortage of workforce forces many lab to work understaffed, thus putting more workloads on the available technologists and may lead to longer turnaround times. Critical specialty areas, such as pathology and microbiology, are still reporting unfilled positions, which indicates ongoing recruitment and retention challenges despite heightened awareness of workforce issues.

To add to these difficulties, a growing tide of retirements is quickly draining the pool of seasoned laboratory workers at alarming rates. According to recent departmental surveys, 10 out of 17 laboratory departments indicate an increase in the rate of retirement, with experienced technicians leaving the workforce faster than new professionals can be trained to replace them. This brain drain, combined with a decline in the number of young professionals joining the profession, contributes greatly to the labor shortage. Experts in the market warn that, unless strategic intervention is undertaken, shortages may only increase, thus threatening the ability of lab to cope with the growing testing demand. In most facilities, recruitment of specialized technical positions often takes several months to a year, which highlights the significant challenge of workforce replenishment and makes talent development a top priority.

Unlock Market Intelligence

Explore the market potential with our data-driven report

US Diagnostic Labs Market Trend

Accelerated Adoption of Genetic Testing and Precision Diagnostics

There is a sharp change in the diagnostic laboratory environment towards genetic and high-complexity molecular testing procedures. In 2024, genetic tests have already reached an impressive 43% of all Medicare Part B laboratory expenditures, by far the highest percentage of all testing categories. This significant investment indicates a high rate of increase in DNA-based diagnostics, such as extensive cancer genomics and infectious-disease panels, which have become standard clinical instruments in modern patient care. Interestingly, the Medicare expenditure on conventional non-genetic tests like metabolic panels and complete blood counts has decreased over the past years, to as low as USD 4.8 billion in 2024, which is a clear indication of the changing test mix as precision medicine continues to push the laboratory service menus towards complex molecular analyses.

Behind this change is a proliferation of possible genetic testing opportunities made possible by the development of new technological capacities. Genetic test products are now available in an unprecedented variety of diagnostic lab, with more than 175,000 distinct genetic test products in the U.S. market as of 2025, ranging in application from oncology biomarkers to rare-disease diagnostics. Most of them are laboratory-developed tests (LDTs) developed internally, which have expanded significantly in complexity and clinical application. Regulatory bodies are also rethinking regulatory frameworks of LDTs due to their increased use and possible clinical risks. This influx of genetic testing is a classic example of a new era of diagnostics, with advanced molecular methods quickly becoming a staple of the overall laboratory service offerings.

US Diagnostic Labs Market Opportunity

Strategic Implementation of Automation and Artificial Intelligence Technologies

Automation and artificial intelligence are becoming strategic tools used by diagnostic lab to improve operational efficiency and reduce chronic staffing challenges. In a nationwide survey, almost 90% of laboratory professionals said their organizations need to increase automation capacity to handle the growing testing volume, and 91% said that implementing AI-driven solutions could help them fulfill unmet patient-care requirements. Repetitive processes, such as specimen sorting and centrifugation, can be automated, allowing lab to sustain high throughput capacity even when staff numbers are low. This automation does not only shorten turnaround times but also significantly minimizes the risk of human error during testing processes. These technologies are seen by laboratory professionals as essential operational support, with 95% confirming that automation directly improves patient-care quality.

The returns on investment in automation technologies are high in terms of operations in diagnostic facilities. Workflows that are supported by machines are effective in compensating for the lack of workforce by taking over labor-intensive tasks and leaving skilled technologists to focus on complex analyses and interpretation of results. Automated systems run 24/7 and maintain accuracy, which is beneficial in assisting lab to scale capacity during demand peaks like seasonal flu spikes. These systems also offer cost savings, since labor costs are estimated to be 40-60% of laboratory operating costs, and reduction of manual work is financially beneficial. Early adopters indicate that intelligent automation and AI algorithms are effective at automating processes from quality control to slide interpretation, enhancing productivity without compromising testing accuracy and positioning technology adoption as a leading opportunity to grow the laboratory sustainably.

Unlock Market Intelligence

Explore the market potential with our data-driven report

US Diagnostic Labs Market Segmentation Analysis

By Lab Type

- Single/Independent Laboratories

- Hospital-based Laboratories

- Physician Office Laboratories

- Others

Single/independent lab, encompassing national reference laboratory chains and numerous standalone facilities, command 50% of the U.S. diagnostic labs market, establishing this as the dominant segment overall. These lab service extensive networks of hospitals, clinics, and physician offices for routine testing requirements, with market leaders Quest Diagnostics and Labcorp together performing approximately one-quarter of all U.S. laboratory tests, illustrating this segment’s remarkable reach and processing volume. Their market prominence reflects broad accessibility and operational efficiency that healthcare providers increasingly depend upon for reliable diagnostic services.

The substantial market share held by independent lab reflects their exceptional accessibility and cost-effectiveness for end users across healthcare settings. Many outpatient providers and health systems rely extensively on these facilities for rapid, economically viable testing services outside traditional hospital settings. By leveraging advanced automation platforms and extensive logistics networks, independent lab can process substantial volumes of common tests rapidly to satisfy widespread demand. Their convenient patient access through numerous service centers combined with comprehensive test menus has firmly cemented independent lab’ leading market position.

By Testing Services

- Physiological Function Testing

- General & Clinical Testing

- Esoteric Testing

- Specialized Testing

- Non-invasive Prenatal Testing

- COVID-19 Testing

- Others

General & clinical testing services constitute the foundational backbone of U.S. diagnostic lab, accounting for 40% of the market and representing the largest share among all testing categories. This segment encompasses routine examinations including complete blood counts, comprehensive metabolic panels, and urinalysis, which serve as fundamental tools for diagnosing medical conditions and monitoring overall patient health status. Such tests are routinely ordered across primary care settings, specialty clinics, and hospital systems as standard medical practice, generating consistently high testing volumes.

The commanding market share of general clinical testing services is fundamentally driven by their broad medical necessity and high ordering frequency. Preventive health check-ups and chronic disease management protocols rely heavily on these baseline diagnostic tests, fueling steady nationwide demand. Advancements in automated analyzer technology have further enhanced efficiency, enabling lab to process high volumes rapidly and accurately. The ubiquity of general laboratory testing across all care settings solidifies this segment’s preeminent position.

List of Companies Covered in US Diagnostic Labs Market

The companies listed below are highly influential in the US diagnostic labs market, with a significant market share and a strong impact on industry developments.

- Kaiser Permanente Laboratories

- Cleveland Clinic Laboratories

- Northwell Health Labs

- Labcorp

- Quest Diagnostics

- Mayo Clinic Laboratories

- ARUP Laboratories

- Bio-Reference Laboratories

- Ascension Clinical Laboratories

- Intermountain Healthcare Laboratories

Market News & Updates

- Quest Diagnostics, 2025:

Launched a novel blood test combining AB42/40 and p-tau217 biomarkers to help confirm Alzheimer’s disease pathology, using advanced mass spec and immunoassay technologies.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. US Diagnostic Labs Market Policies, Regulations, and Standards

4. US Diagnostic Labs Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. US Diagnostic Labs Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in USD Million

5.2. Market Segmentation & Growth Outlook

5.2.1.By Lab Type

5.2.1.1. Single/Independent Laboratories- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Hospital-based Laboratories- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3. Physician Office Laboratories- Market Insights and Forecast 2022-2032, USD Million

5.2.1.4. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Testing Services

5.2.2.1. Physiological Function Testing- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. General & Clinical Testing- Market Insights and Forecast 2022-2032, USD Million

5.2.2.3. Esoteric Testing- Market Insights and Forecast 2022-2032, USD Million

5.2.2.4. Specialized Testing- Market Insights and Forecast 2022-2032, USD Million

5.2.2.5. Non-invasive Prenatal Testing- Market Insights and Forecast 2022-2032, USD Million

5.2.2.6. COVID-19 Testing- Market Insights and Forecast 2022-2032, USD Million

5.2.2.7. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Disease

5.2.3.1. Cardiology- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Oncology- Market Insights and Forecast 2022-2032, USD Million

5.2.3.3. Neurology- Market Insights and Forecast 2022-2032, USD Million

5.2.3.4. Orthopedics- Market Insights and Forecast 2022-2032, USD Million

5.2.3.5. Gastroenterology- Market Insights and Forecast 2022-2032, USD Million

5.2.3.6. Gynecology- Market Insights and Forecast 2022-2032, USD Million

5.2.3.7. Odontology- Market Insights and Forecast 2022-2032, USD Million

5.2.3.8. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Revenue Source

5.2.4.1. Healthcare Plan- Market Insights and Forecast 2022-2032, USD Million

5.2.4.2. Out-of-Pocket- Market Insights and Forecast 2022-2032, USD Million

5.2.4.3. Public System- Market Insights and Forecast 2022-2032, USD Million

5.2.5.By Test Type

5.2.5.1. Pathology- Market Insights and Forecast 2022-2032, USD Million

5.2.5.2. Radiology- Market Insights and Forecast 2022-2032, USD Million

5.2.6.By End User

5.2.6.1. Referrals- Market Insights and Forecast 2022-2032, USD Million

5.2.6.2. Walk-ins- Market Insights and Forecast 2022-2032, USD Million

5.2.6.3. Corporate Clients- Market Insights and Forecast 2022-2032, USD Million

5.2.7.By Region

5.2.7.1. West

5.2.7.2. Midwest

5.2.7.3. South

5.2.7.4. North

5.2.7.5. Northeast

5.2.8.By Competitors

5.2.8.1. Competition Characteristics

5.2.8.2. Market Share & Analysis

6. US Single/Independent Laboratories Market Statistics, 2022-2032

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in USD Million

6.2. Market Segmentation & Growth Outlook

6.2.1.By Testing Services- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Disease- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By Revenue Source- Market Insights and Forecast 2022-2032, USD Million

6.2.4.By Test Type- Market Insights and Forecast 2022-2032, USD Million

6.2.5.By End User- Market Insights and Forecast 2022-2032, USD Million

6.2.6.By Region- Market Insights and Forecast 2022-2032, USD Million

7. US Hospital-based Laboratories Market Statistics, 2022-2032

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in USD Million

7.2. Market Segmentation & Growth Outlook

7.2.1.By Testing Services- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Disease- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By Revenue Source- Market Insights and Forecast 2022-2032, USD Million

7.2.4.By Test Type- Market Insights and Forecast 2022-2032, USD Million

7.2.5.By End User- Market Insights and Forecast 2022-2032, USD Million

7.2.6.By Region- Market Insights and Forecast 2022-2032, USD Million

8. US Physician Office Laboratories Market Statistics, 2022-2032

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in USD Million

8.2. Market Segmentation & Growth Outlook

8.2.1.By Testing Services- Market Insights and Forecast 2022-2032, USD Million

8.2.2.By Disease- Market Insights and Forecast 2022-2032, USD Million

8.2.3.By Revenue Source- Market Insights and Forecast 2022-2032, USD Million

8.2.4.By Test Type- Market Insights and Forecast 2022-2032, USD Million

8.2.5.By End User- Market Insights and Forecast 2022-2032, USD Million

8.2.6.By Region- Market Insights and Forecast 2022-2032, USD Million

9. Competitive Outlook

9.1. Company Profiles

9.1.1.Labcorp

9.1.1.1. Business Description

9.1.1.2. Service Portfolio

9.1.1.3. Collaborations & Alliances

9.1.1.4. Recent Developments

9.1.1.5. Financial Details

9.1.1.6. Others

9.1.2.Quest Diagnostics

9.1.2.1. Business Description

9.1.2.2. Service Portfolio

9.1.2.3. Collaborations & Alliances

9.1.2.4. Recent Developments

9.1.2.5. Financial Details

9.1.2.6. Others

9.1.3.Mayo Clinic Laboratories

9.1.3.1. Business Description

9.1.3.2. Service Portfolio

9.1.3.3. Collaborations & Alliances

9.1.3.4. Recent Developments

9.1.3.5. Financial Details

9.1.3.6. Others

9.1.4.ARUP Laboratories

9.1.4.1. Business Description

9.1.4.2. Service Portfolio

9.1.4.3. Collaborations & Alliances

9.1.4.4. Recent Developments

9.1.4.5. Financial Details

9.1.4.6. Others

9.1.5.Bio-Reference Laboratories

9.1.5.1. Business Description

9.1.5.2. Service Portfolio

9.1.5.3. Collaborations & Alliances

9.1.5.4. Recent Developments

9.1.5.5. Financial Details

9.1.5.6. Others

9.1.6.Kaiser Permanente Laboratories

9.1.6.1. Business Description

9.1.6.2. Service Portfolio

9.1.6.3. Collaborations & Alliances

9.1.6.4. Recent Developments

9.1.6.5. Financial Details

9.1.6.6. Others

9.1.7.Cleveland Clinic Laboratories

9.1.7.1. Business Description

9.1.7.2. Service Portfolio

9.1.7.3. Collaborations & Alliances

9.1.7.4. Recent Developments

9.1.7.5. Financial Details

9.1.7.6. Others

9.1.8.Northwell Health Labs

9.1.8.1. Business Description

9.1.8.2. Service Portfolio

9.1.8.3. Collaborations & Alliances

9.1.8.4. Recent Developments

9.1.8.5. Financial Details

9.1.8.6. Others

9.1.9.Ascension Clinical Laboratories

9.1.9.1. Business Description

9.1.9.2. Service Portfolio

9.1.9.3. Collaborations & Alliances

9.1.9.4. Recent Developments

9.1.9.5. Financial Details

9.1.9.6. Others

9.1.10. Intermountain Healthcare Laboratories

9.1.10.1. Business Description

9.1.10.2. Service Portfolio

9.1.10.3. Collaborations & Alliances

9.1.10.4. Recent Developments

9.1.10.5. Financial Details

9.1.10.6. Others

10. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Lab Type |

|

| By Testing Services |

|

| By Disease |

|

| By Revenue Source |

|

| By Test Type |

|

| By End User |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.