UK Weight Management and Wellbeing Market Report: Trends, Growth and Forecast (2026-2032)

By Category (Meal Replacement Products (Shakes, Bars, Ready-to-Drink (RTD) Beverages, Powder Mixes), OTC Obesity Products (Fat Absorption Inhibitors, Appetite Suppressants, Metabolism Boosters), Supplement Nutrition Drinks, Slimming Teas, Weight Loss Supplements), By Application (Obesity Management, Diabetes-Associated Weight Control, Cardiovascular Risk Reduction, Post-Bariatric Surgery Weight Maintenance, General Fitness & Lifestyle Weight Control), By End User (Hospitals, Specialty & Bariatric Clinics, Weight Loss Centers, Homecare/Individual Consumers), By Sales Channel (Retail Offline (Pharmacies & Drug Stores, Supermarkets/Hypermarkets, Specialty Nutrition Stores), Retail Online (E-commerce Platforms, Brand-Owned Websites)), By Region (England, Wales, Scotland, Northern Ireland) ... Read more

|

Major Players

|

UK Weight Management and Wellbeing Market Statistics and Insights, 2026

- Market Size Statistics

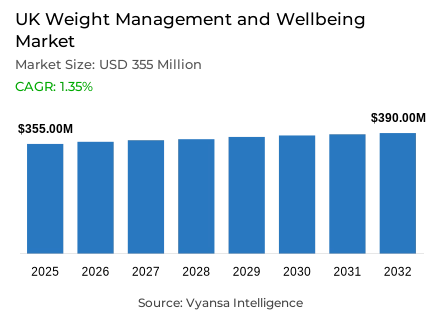

- Weight management and wellbeing market size in UK was valued at USD 355 million in 2025 and is estimated at USD 362.25 million in 2026.

- The market size is expected to grow to USD 390 million by 2032.

- Market to register a CAGR of around 1.35% during 2026-32.

- Category Shares

- Meal replacement products grabbed market share of 75%.

- Competition

- More than 20 companies are actively engaged in producing weight management and wellbeing in UK.

- Top 5 companies acquired around 70% of the market share.

- Class Delta Ltd, USN UK Ltd, PhD Nutrition Ltd, Huel Ltd, Glanbia Plc etc., are few of the top companies.

- Sales Channel

- Retail offline grabbed 65% of the market.

UK Weight Management and Wellbeing Market Outlook

The UK weight management and wellbeing market was valued at USD 355 million in 2025 and is projected to grow from USD 362.25 million in 2026 to USD 390 million by 2032, exhibiting a CAGR of approximately 1.35 % during the forecast period. The future looks promising with a stable yet average growth as the consumer preference towards healthier lifestyles, weight-control products, and convenient food remains to influence buying behaviour. Although the pricing pressures have been reduced compared to previous years, the demand is still supported by the increasing awareness of obesity and personal wellbeing.

The prevalence of obesity and changing dietary patterns still support the topicality of weight-management and wellbeing products in daily life. In England, 64.5% of adults aged 18+ were overweight or living with obesity in 2023/24, while 26.5% were living with obesity, according to the Office for Health Improvement and Disparities. Concurrently, only 31.3% of adults aged 16+ consume the recommended five portions of fruit and vegetables per day, highlighting persistent gaps in nutrition that reinforce the appeal of convenient and structured approaches to weight control.

Product innovation and convenient nutrition formats are shaping category performance. Meal replacement products hold the largest category share at around 75%, reflecting strong consumer demand for easy-to-use solutions that combine portion control with balanced nutrition. Within broader health routines, weight management and wellbeing solutions increasingly position themselves as functional products that support energy, fitness recovery, and daily wellness rather than focusing only on short-term weight loss.

Distribution dynamics also influence future performance. In UK, retail offline is still accounting for 65% of total sales, with the support of retailers such as supermarkets, pharmacies, and specialty stores that people trust for their ease of access and quality of products. At the same time, online retail is expanding as people are looking for more convenient ways to shop. This is another aspect that emphasizes the place of weight management and wellness solutions in the lifestyle and nutritional habits of the people in the UK.

UK Weight Management and Wellbeing Market Growth DriverRising Obesity Burden Keeps Demand Active

One of the key drivers that affects the UK weight management and wellbeing market is the high burden of excess weight. According to the Office for Health Improvement and Disparities (OHID) in its Obesity profile: May 2025 update, in 2023/24, 64.5% of adults aged 18 years and over in England were overweight or obese, increasing from 64.0% in 2022/23. According to the same update, 26.5% of adults had obesity.

This long-term pressure has led to high consumer demand of products that enable more organized and effective weight control. The aforementioned OHID release also indicates that only 31.3 % of adults aged 16+ consumed at least five portions of fruit and vegetables per day in, underscoring the need for convenient products that merge weight support with broader nutritional benefits.

UK Weight Management and Wellbeing Market ChallengeGLP-1 Medicines Raise the Competitive Pressure

The main issue is that the prescription-based competition, especially GLP-1 drugs, has risen at a very high rate, which has made consumers very picky about the conventional weight-loss products. According to the interim commissioning guidance published by National Health Service (NHS) England in March 2025, the total population of National Institute for Health and Care Excellence (NICE) eligible patients with tirzepatide is estimated to be 3.4 million individuals, which demonstrates the large pool of medically addressable people that has been created.

According to the same NHS England guidance, 220,000 people are to be accessed in the first three years of a staged rollout, and primary-care access funding will begin on 23 June 2025. The Medicines and Healthcare products Regulatory Agency (MHRA) guidance, revised on 5 February 2026, confirms that Wegovy and Mounjaro are still licenced, prescription-only weight management options, which further increases the burden of comparison on conventional supplements in terms of trust, efficacy, and relevance to consumers.

Unlock Market Intelligence

Explore the market potential with our data-driven report

UK Weight Management and Wellbeing Market TrendFunctional Nutrition Moves Beyond Pure Slimming

One of the key market trends is the shift of the simple weight-loss positioning to the wider daily wellness. Meal replacements and associated products are being promoted as nutrient-rich solutions that aid energy, fitness, recovery, digestive health, and overall wellbeing, as opposed to calories alone. This change is in line with the trend of health practices that are more sustainable and lifestyle friendly as outlined in the market content.

This trend is in line with the existing nutrition and activity trends in the UK. OHID reports that only 31.3 % of adults in England consume five portions of fruit and vegetables per day, while 22.0 % of adults were physically inactive in 2023/24. These loopholes make convenient, practical nutrition more relevant, especially when the consumer wants products that can be combined with daily wellness objectives rather than rigid short-term dieting.

UK Weight Management and Wellbeing Market OpportunityE-Commerce Expansion Creates a Stronger Route to Growth

One of the obvious opportunities lies in e-commerce and direct-to-consumer growth. The Office for National Statistics (ONS) reports that internet sales accounted for 27.4 % of total retail sales in Great Britain in 2025, and the ONS December 2025 retail sales bulletin shows the online share rising to 28.3 % in December 2025. This gives weight-management brands more room to scale visibility, assortment, repeat purchases, and subscription-based purchasing.

The route is further enticed by the fact that the delivery infrastructure in the UK is getting stronger. On 24 June 2025, a UK government press release stated that Amazon intended to spend GBP40 billion in the UK within the next three years, which would enhance the long-term environment by accelerating fulfilment, enhancing product availability, and expanding digital access to health and wellness products.

Unlock Market Intelligence

Explore the market potential with our data-driven report

UK Weight Management and Wellbeing Market Segmentation Analysis

By Category

- Meal Replacement Products

- Shakes

- Bars

- Ready-to-Drink (RTD) Beverages

- Powder Mixes

- OTC Obesity Products

- Fat Absorption Inhibitors

- Appetite Suppressants

- Metabolism Boosters

- Supplement Nutrition Drinks

- Slimming Teas

- Weight Loss Supplements

The first segment in this category is meal replacement products, which holds a significant 75% of the market share. This is also in line with the current trend in the lives of consumers, who are increasingly looking towards a product that is easy to consume and also meets the needs of a healthy diet, while also providing the advantage of weight management with little extra effort.

The success of this segment is also in line with the overall health scenario, as statistics on the website of the OHID indicate that in 2023/24, 64.5% of adults aged 18+ in England were overweight or obese, and only 31.3% of adults aged 16+ achieved the 5 a day fruit and vegetable guideline.

By Sales Channel

- Retail Offline

- Pharmacies & Drug Stores

- Supermarkets/Hypermarkets

- Specialty Nutrition Stores

- Retail Online

- E-commerce Platforms

- Brand-Owned Websites

In UK, retail offline is still accounting for 65% of total sales, with the support of retailers such as supermarkets, pharmacies, and specialty stores that people trust for their ease of access and quality of products.

At the same time, online retail is expanding as people are looking for more convenient ways to shop. This is another aspect that emphasizes the place of weight management and wellness solutions in the lifestyle and nutritional habits of the people in the UK.

List of Companies Covered in UK Weight Management and Wellbeing Market

The companies listed below are highly influential in the UK weight management and wellbeing market, with a significant market share and a strong impact on industry developments.

- Class Delta Ltd

- USN UK Ltd

- PhD Nutrition Ltd

- Huel Ltd

- Glanbia Plc

- Nutricia Ltd

- LighterLife Fast Ltd

- Omega Pharma Ltd

- Herbalife (UK) Ltd

- Ideal Health Group Ltd

Competitive Landscape

The competitive landscape of weight management and wellbeing in the UK is led by major brands that are strongly positioned within the meal replacement segment, which continues to dominate overall category sales. Huel Ltd led the market in 2025 with a value share of 33, supported by its strong presence in meal replacements and a diversified portfolio that includes ready-to-drink products and bars. The company has strengthened its position through the expansion of its UK retail footprint and a robust direct-to-consumer channel, with products available in around 70% of UK supermarkets and more than 25,000 stores globally. Glanbia Plc follows with a value share of 20.2 through its Slim Fast brand, although its performance has remained relatively flat as consumer preferences shift towards pharmaceutical weight loss drugs such as Wegovy and Ozempic. In response to sustained underperformance, Glanbia announced plans to divest Slim Fast as part of a broader strategy to streamline operations.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- UK Weight Management and Wellbeing Market Policies, Regulations, and Standards

- UK Weight Management and Wellbeing Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- UK Weight Management and Wellbeing Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Category

- Meal Replacement Products- Market Insights and Forecast 2022-2032, USD Million

- Shakes- Market Insights and Forecast 2022-2032, USD Million

- Bars- Market Insights and Forecast 2022-2032, USD Million

- Ready-to-Drink (RTD) Beverages- Market Insights and Forecast 2022-2032, USD Million

- Powder Mixes- Market Insights and Forecast 2022-2032, USD Million

- OTC Obesity Products- Market Insights and Forecast 2022-2032, USD Million

- Fat Absorption Inhibitors- Market Insights and Forecast 2022-2032, USD Million

- Appetite Suppressants- Market Insights and Forecast 2022-2032, USD Million

- Metabolism Boosters- Market Insights and Forecast 2022-2032, USD Million

- Supplement Nutrition Drinks- Market Insights and Forecast 2022-2032, USD Million

- Slimming Teas- Market Insights and Forecast 2022-2032, USD Million

- Weight Loss Supplements- Market Insights and Forecast 2022-2032, USD Million

- Meal Replacement Products- Market Insights and Forecast 2022-2032, USD Million

- By Application

- Obesity Management- Market Insights and Forecast 2022-2032, USD Million

- Diabetes-Associated Weight Control- Market Insights and Forecast 2022-2032, USD Million

- Cardiovascular Risk Reduction- Market Insights and Forecast 2022-2032, USD Million

- Post-Bariatric Surgery Weight Maintenance- Market Insights and Forecast 2022-2032, USD Million

- General Fitness & Lifestyle Weight Control- Market Insights and Forecast 2022-2032, USD Million

- By End User

- Hospitals- Market Insights and Forecast 2022-2032, USD Million

- Specialty & Bariatric Clinics- Market Insights and Forecast 2022-2032, USD Million

- Weight Loss Centers- Market Insights and Forecast 2022-2032, USD Million

- Homecare/Individual Consumers- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- Pharmacies & Drug Stores- Market Insights and Forecast 2022-2032, USD Million

- Supermarkets/Hypermarkets- Market Insights and Forecast 2022-2032, USD Million

- Specialty Nutrition Stores- Market Insights and Forecast 2022-2032, USD Million

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- E-commerce Platforms- Market Insights and Forecast 2022-2032, USD Million

- Brand-Owned Websites- Market Insights and Forecast 2022-2032, USD Million

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- By Region

- England

- Wales

- Scotland

- Northern Ireland

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Category

- Market Size & Growth Outlook

- UK Meal Replacement Products Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- UK OTC Obesity Products Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- UK Supplement Nutrition Drinks Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- UK Slimming Teas Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- UK Weight Loss Supplements Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Huel Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Glanbia Plc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Nutricia Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- LighterLife Fast Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Omega Pharma Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Class Delta Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- USN UK Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- PhD Nutrition Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Herbalife (UK) Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Ideal Health Group Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Huel Ltd

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Category |

|

| By Application |

|

| By End User |

|

| By Sales Channel |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.