UK Skin Care Market Report: Trends, Growth and Forecast (2025-2030)

By Product (Body Care, Facial Care, Hand Care, Skin Care Sets/Kits), By Category (Premium, Mass), By Gender (Men, Women, Unisex), By End User (Adults, Teenagers, Children), By Packaging (Tubes, Bottles, Jars, Others), By Sales Channel (Online, Offline) ... Read more

|

Major Players

|

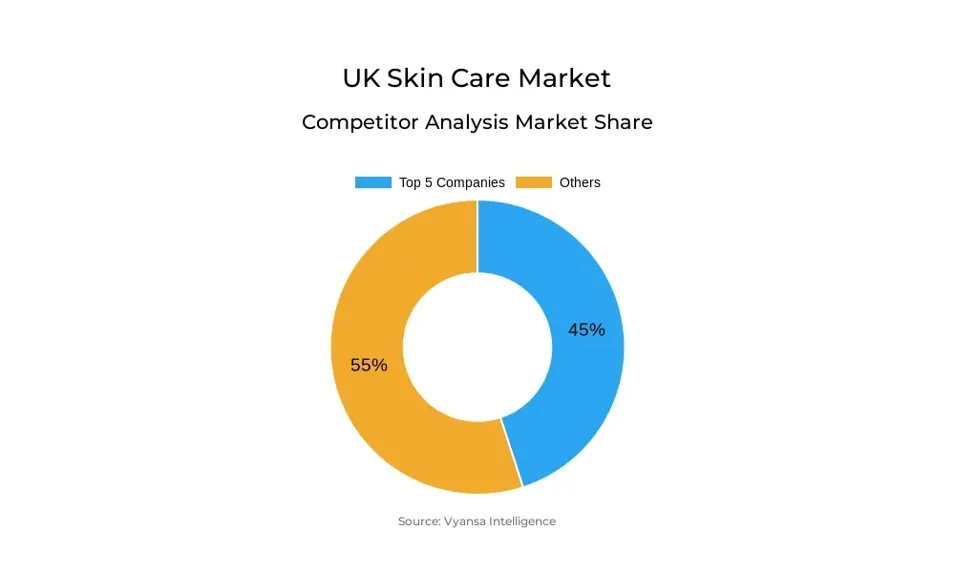

UK Skin Care Market Statistics, 2025

- Market Size Statistics

- Skin Care in UK is estimated at $ 5.98 Billion.

- The market size is expected to grow to $ 6.6 Billion by 2030.

- Market to register a CAGR of around 1.66% during 2025-30.

- Product Shares

- Facial Care grabbed market share of 70%.

- Competition

- More than 20 companies are actively engaged in producing Skin Care in UK.

- Top 5 companies acquired 45% of the market share.

- Clarins UK Ltd, Elemis Ltd, Procter & Gamble UK Ltd, L'Oréal (UK) Ltd, Boots UK Ltd etc., are few of the top companies.

- Sales Channel

- Retail Ecommerce grabbed 53% of the market.

UK Skin Care Market Outlook

UK skin care market is poised to record stable growth between 2025 and 2030 underpinned by sustained consumer interest and slow economic recovery. As the inflationary pressure abates, consumers are anticipated to be price-sensitive in their expenditures, prioritizing products that deliver guaranteed benefits. Anti-ageing products will drive category growth, particularly as younger generations of consumers, such as Gen Z and Millennials, actively pursue preventative remedies. Meanwhile, treatments and moisturisers will be staple categories, based on their wide product ranges and multi-beneficial credentials.

Loyalty among consumers is likely to hold up well with brands promising both affordability and effectiveness. Mid-range brands such as CeraVe, The Inkey List, and Weleda are likely to perform well, attracting value-conscious consumers in search of science-led solutions. Yet, competition is likely to heat up, particularly between premium and private label brands. Brands will have to spend on sustainable packaging, creative advertising, and more engaging formulations to maintain market share. The rising trend of skin care sets and multi-tasking products will also influence consumer behavior, as consumers seek easy routines and more value.

Digital platforms will maintain dominance in retail, but brick-and-mortar stores, particularly beauty experts, are gaining traction through private offerings and new store launches. Social media impact, particularly from platforms such as TikTok, will continue to be a major force behind product discovery and brand fame. Brands such as Summer Fridays and Sol De Janeiro, with their balance of innovation and social strength, will be likely to drive purchases beyond conventional category requirements.

Lastly, K-Beauty and J-Beauty growth will continue to fuel innovation in the UK market. These foreign brands provide value luxury and exclusive ingredients, encouraging local brands to adapt. In a crowded dermocosmetics space, only those with robust differentiation, including scientific validity or health expert endorsements, will continue to grow in the long term.

UK Skin Care Market Challenge

UK shoppers are becoming increasingly discerning about their skin care buys, opting for bespoke regimens and evidence of efficacy. Therefore, areas such as anti-agers and simple moisturisers are expanding at a higher rate than body care. Yet, continued cost consciousness ensures mid-priced lines providing efficacy at value prices—e.g., CeraVe and The Inkey List—are attracting buyers. This represents significant challenges for private label and premium brands alike as they each try to hold their share.

Increasing trend towards multi-functional and hybrid products is also changing the scenario. Consumers are streamlining routines by often substituting multiple products with those that provide conjoint benefits, such as moisturisers or lip balms with sun protection factor. In addition, colour cosmetics players are making a foray into skin care by employing active ingredients, which adds to competition. Premium brands now need to concentrate more on innovation, sustainability, and quality marketing to remain competitive.

UK Skin Care Market Trend

The UK skincare market is seeing increasing demand for global beauty brands, particularly K-Beauty and J-Beauty. They are building traction as they possess innovative ingredients and value luxury appeal at budget-friendlier prices. Consumers are becoming more attracted to quality products offered at affordable prices. Brands such as COSRX and Laneíge have experienced high sales growth, with Boots UK stating that a Korean skin care product was sold every 30 seconds from October through to January 2025. The products made up over a tenth of the retailer's Everyday Skincare sales.

This demand is set to continue in the next few years as more international brands move into the UK market and build out their distribution. Meanwhile, domestic brands are learning from their international counterparts, especially in product formulation and positioning, in order to stay competitive amidst the changing beauty scene.

Unlock Market Intelligence

Explore the market potential with our data-driven report

UK Skin Care Market Opportunity

The dermocosmetics business has still been expanding steadily, although some top brands experienced a slowdown in value growth in 2024. This was primarily because more players were entering the market, hence increased competition in the niche. UK cost-conscious consumers continue to prioritize product performance, and this resulted in the high performance of brands such as Medik8, which provide science-backed formulas and professional-strength solutions.

In the future, competition within dermocosmetics is likely to increase even more by way of new product launches and well-considered positioning. To remain at the forefront, brands will have to emphasize establishing trust and credibility. Lending support from health care professionals to recommend products or the establishment of an engaged online community may be prime means of differentiation in a congested arena. These will be crucial for brands that seek to drive long-term growth within the developing UK skin care environment.

| Report Coverage | Details |

|---|---|

| Market Forecast | 2025-30 |

| USD Value 2024 | $ 5.98 Billion |

| USD Value 2030 | $ 6.6 Billion |

| CAGR 2025-2030 | 1.66% |

| Largest Category | Facial Care segment leads with 70% market share |

| Top Challenges | Evolving Consumer Demands and Intensifying Brand Competition |

| Top Trends | Rising Popularity of International Beauty Brands Driven by K-Beauty |

| Top Opportunities | Rising Scope for Differentiation Amid Growing Competition |

| Key Players | Clarins UK Ltd, Elemis Ltd, Procter & Gamble UK Ltd, L'Oréal (UK) Ltd, Boots UK Ltd, Estée Lauder Cosmetics Ltd, Beiersdorf UK Ltd, Unilever UK Ltd, L'Occitane Ltd, Johnson & Johnson Ltd and Others. |

Unlock Market Intelligence

Explore the market potential with our data-driven report

UK Skin Care Market Segmentation Analysis

The most market-share dominated segment under the sales channel is retail e-commerce. In 2024, it represented more than half of the overall value sales of the UK skin care market. It was boosted in popularity by its extensive product range, especially from up-and-coming and indie brands. People liked buying online because websites like Amazon offered competitive prices, which were especially appealing to frequent buyers.

Beauty specialist shops also had robust growth within this time. Space NK and Rituals, among others, increased their store presence, helping drive this segment's performance. Space NK, for example, launched seven new stores throughout the UK in 2024 and added exclusive ranges. The South Korean brand Then I Met You introduced in Space NK during July 2024, followed by The Inkey List in April 2025, demonstrating ongoing desire for specialist retailing experiences.

Top Companies in UK Skin Care Market

The top companies operating in the market include Clarins UK Ltd, Elemis Ltd, Procter & Gamble UK Ltd, L'Oréal (UK) Ltd, Boots UK Ltd, Estée Lauder Cosmetics Ltd, Beiersdorf UK Ltd, Unilever UK Ltd, L'Occitane Ltd, Johnson & Johnson Ltd, etc., are the top players operating in the UK Skin Care Market.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. UK Skin Care Market Policies, Regulations, and Standards

4. UK Skin Care Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. UK Skin Care Market Statistics, 2020-2030F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in US$ Million

5.2. Market Segmentation & Growth Outlook

5.2.1.By Product

5.2.1.1. Body Care- Market Insights and Forecast 2020-2030, USD Million

5.2.1.1.1. Firming Body Care- Market Insights and Forecast 2020-2030, USD Million

5.2.1.1.2. General Purpose Body Care- Market Insights and Forecast 2020-2030, USD Million

5.2.1.2. Facial Care- Market Insights and Forecast 2020-2030, USD Million

5.2.1.2.1. Acne Treatments- Market Insights and Forecast 2020-2030, USD Million

5.2.1.2.2. Face Masks- Market Insights and Forecast 2020-2030, USD Million

5.2.1.2.3. Facial Cleansers- Market Insights and Forecast 2020-2030, USD Million

5.2.1.2.3.1. Liquid- Market Insights and Forecast 2020-2030, USD Million

5.2.1.2.3.2. Cream- Market Insights and Forecast 2020-2030, USD Million

5.2.1.2.3.3. Gel- Market Insights and Forecast 2020-2030, USD Million

5.2.1.2.3.4. Bar Cleansers- Market Insights and Forecast 2020-2030, USD Million

5.2.1.2.3.5. Facial Cleansing Wipes- Market Insights and Forecast 2020-2030, USD Million

5.2.1.2.4. Moisturisers and Treatments- Market Insights and Forecast 2020-2030, USD Million

5.2.1.2.4.1. Basic Moisturisers- Market Insights and Forecast 2020-2030, USD Million

5.2.1.2.4.2. Anti-Agers- Market Insights and Forecast 2020-2030, USD Million

5.2.1.2.5. Lip Care- Market Insights and Forecast 2020-2030, USD Million

5.2.1.2.6. Toners- Market Insights and Forecast 2020-2030, USD Million

5.2.1.3. Hand Care- Market Insights and Forecast 2020-2030, USD Million

5.2.1.4. Skin Care Sets/Kits- Market Insights and Forecast 2020-2030, USD Million

5.2.2.By Category

5.2.2.1. Premium- Market Insights and Forecast 2020-2030, USD Million

5.2.2.2. Mass- Market Insights and Forecast 2020-2030, USD Million

5.2.3.By Gender

5.2.3.1. Men- Market Insights and Forecast 2020-2030, USD Million

5.2.3.2. Women- Market Insights and Forecast 2020-2030, USD Million

5.2.3.3. Unisex- Market Insights and Forecast 2020-2030, USD Million

5.2.4.By End User

5.2.4.1. Adults- Market Insights and Forecast 2020-2030, USD Million

5.2.4.2. Teenagers- Market Insights and Forecast 2020-2030, USD Million

5.2.4.3. Children- Market Insights and Forecast 2020-2030, USD Million

5.2.5.By Packaging

5.2.5.1. Tubes- Market Insights and Forecast 2020-2030, USD Million

5.2.5.2. Bottles- Market Insights and Forecast 2020-2030, USD Million

5.2.5.3. Jars- Market Insights and Forecast 2020-2030, USD Million

5.2.5.4. Others- Market Insights and Forecast 2020-2030, USD Million

5.2.6.By Sales Channel

5.2.6.1. Online- Market Insights and Forecast 2020-2030, USD Million

5.2.6.2. Offline- Market Insights and Forecast 2020-2030, USD Million

5.2.7.By Competitors

5.2.7.1. Competition Characteristics

5.2.7.2. Market Share & Analysis

6. UK Body Care Market Statistics, 2020-2030F

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in US$ Million

6.2. Market Segmentation & Growth Outlook

6.2.1.By Product- Market Insights and Forecast 2020-2030, USD Million

6.2.2.By Category- Market Insights and Forecast 2020-2030, USD Million

6.2.3.By Gender- Market Insights and Forecast 2020-2030, USD Million

6.2.4.By End User- Market Insights and Forecast 2020-2030, USD Million

6.2.5.By Packaging- Market Insights and Forecast 2020-2030, USD Million

6.2.6.By Sales Channel- Market Insights and Forecast 2020-2030, USD Million

7. UK Facial Care Market Statistics, 2020-2030F

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in US$ Million

7.2. Market Segmentation & Growth Outlook

7.2.1.By Product- Market Insights and Forecast 2020-2030, USD Million

7.2.2.By Category- Market Insights and Forecast 2020-2030, USD Million

7.2.3.By Gender- Market Insights and Forecast 2020-2030, USD Million

7.2.4.By End User- Market Insights and Forecast 2020-2030, USD Million

7.2.5.By Packaging- Market Insights and Forecast 2020-2030, USD Million

7.2.6.By Sales Channel- Market Insights and Forecast 2020-2030, USD Million

8. UK Hand Care Market Statistics, 2020-2030F

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in US$ Million

8.2. Market Segmentation & Growth Outlook

8.2.1.By Category- Market Insights and Forecast 2020-2030, USD Million

8.2.2.By Gender- Market Insights and Forecast 2020-2030, USD Million

8.2.3.By End User- Market Insights and Forecast 2020-2030, USD Million

8.2.4.By Packaging- Market Insights and Forecast 2020-2030, USD Million

8.2.5.By Sales Channel- Market Insights and Forecast 2020-2030, USD Million

9. UK Skin Care Sets/Kits Market Statistics, 2020-2030F

9.1. Market Size & Growth Outlook

9.1.1.By Revenues in US$ Million

9.2. Market Segmentation & Growth Outlook

9.2.1.By Category- Market Insights and Forecast 2020-2030, USD Million

9.2.2.By Gender- Market Insights and Forecast 2020-2030, USD Million

9.2.3.By End User- Market Insights and Forecast 2020-2030, USD Million

9.2.4.By Packaging- Market Insights and Forecast 2020-2030, USD Million

9.2.5.By Sales Channel- Market Insights and Forecast 2020-2030, USD Million

10. Competitive Outlook

10.1. Company Profiles

10.1.1. L'Oréal (UK) Ltd

10.1.1.1. Business Description

10.1.1.2. Product Portfolio

10.1.1.3. Collaborations & Alliances

10.1.1.4. Recent Developments

10.1.1.5. Financial Details

10.1.1.6. Others

10.1.2. Boots UK Ltd

10.1.2.1. Business Description

10.1.2.2. Product Portfolio

10.1.2.3. Collaborations & Alliances

10.1.2.4. Recent Developments

10.1.2.5. Financial Details

10.1.2.6. Others

10.1.3. Estée Lauder Cosmetics Ltd

10.1.3.1. Business Description

10.1.3.2. Product Portfolio

10.1.3.3. Collaborations & Alliances

10.1.3.4. Recent Developments

10.1.3.5. Financial Details

10.1.3.6. Others

10.1.4. Beiersdorf UK Ltd

10.1.4.1. Business Description

10.1.4.2. Product Portfolio

10.1.4.3. Collaborations & Alliances

10.1.4.4. Recent Developments

10.1.4.5. Financial Details

10.1.4.6. Others

10.1.5. Unilever UK Ltd

10.1.5.1. Business Description

10.1.5.2. Product Portfolio

10.1.5.3. Collaborations & Alliances

10.1.5.4. Recent Developments

10.1.5.5. Financial Details

10.1.5.6. Others

10.1.6. Clarins UK Ltd

10.1.6.1. Business Description

10.1.6.2. Product Portfolio

10.1.6.3. Collaborations & Alliances

10.1.6.4. Recent Developments

10.1.6.5. Financial Details

10.1.6.6. Others

10.1.7. Elemis Ltd

10.1.7.1. Business Description

10.1.7.2. Product Portfolio

10.1.7.3. Collaborations & Alliances

10.1.7.4. Recent Developments

10.1.7.5. Financial Details

10.1.7.6. Others

10.1.8. Procter & Gamble UK Ltd

10.1.8.1. Business Description

10.1.8.2. Product Portfolio

10.1.8.3. Collaborations & Alliances

10.1.8.4. Recent Developments

10.1.8.5. Financial Details

10.1.8.6. Others

10.1.9. L'Occitane Ltd

10.1.9.1. Business Description

10.1.9.2. Product Portfolio

10.1.9.3. Collaborations & Alliances

10.1.9.4. Recent Developments

10.1.9.5. Financial Details

10.1.9.6. Others

10.1.10. Johnson & Johnson Ltd

10.1.10.1.Business Description

10.1.10.2.Product Portfolio

10.1.10.3.Collaborations & Alliances

10.1.10.4.Recent Developments

10.1.10.5.Financial Details

10.1.10.6.Others

11. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product |

|

| By Category |

|

| By Gender |

|

| By End User |

|

| By Packaging |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.