UK Digestive Remedies Market Report: Trends, Growth and Forecast (2026-2032)

By Product Type (Paediatric Digestive Remedies (Paediatric Diarrhoeal Remedies, Paediatric Indigestion & Heartburn Remedies, Paediatric Laxatives, Paediatric Motion Sickness Remedies), Diarrhoeal Remedies, IBS Treatments, Indigestion & Heartburn Remedies (Antacids, Antiflatulents, Digestive Enzymes, H2 Blockers, Proton Pump Inhibitors), Laxatives, Motion Sickness Remedies), By Age Group (Children & Adolescents (01-17 years), Adults (18-65 years), Geriatric (65+ years)), By Sales Channel (Retail Online, Retail Offline (Hospitals, Clinics, Pharmacies)), By Region (England, Wales, Scotland, Northern Ireland) ... Read more

|

Major Players

|

UK Digestive Remedies Market Statistics and Insights, 2026

- Market Size Statistics

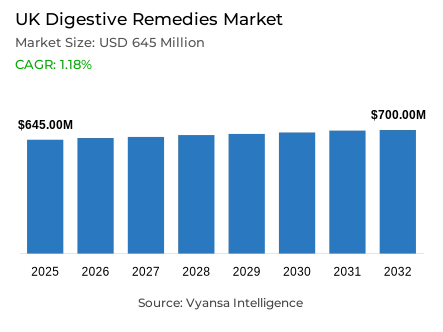

- Digestive remedies market size in UK was valued at USD 645 million in 2025 and is estimated at USD 655 million in 2026.

- The market size is expected to grow to USD 700 million by 2032.

- Market to register a CAGR of around 1.18% during 2026-32.

- Product Type Shares

- Indigestion & heartburn remedies grabbed market share of 65%.

- Competition

- More than 20 companies are actively engaged in producing digestive remedies in UK.

- Top 5 companies acquired around 60% of the market share.

- Rhone-Poulenc Rorer, Teva UK Ltd, Boots UK Ltd, Reckitt Benckiser Group Plc (RB), Bayer Plc etc., are few of the top companies.

- Sales Channel

- Retail offline grabbed 90% of the market.

UK Digestive Remedies Market Outlook

United Kingdom digestive remedies market was valued at USD 645 million in 2025 and is projected to grow from USD 655 million in 2026 to USD 700 million by 2032, exhibiting a CAGR of 1.18% over the forecast period. This is supported by rising consumer awareness of digestive health, growing attention to diet, and an increasing interest in self-medication and convenient over-the-counter remedies to common digestive discomfort. The UK consumers are increasingly taking charge of the treatment of mild symptoms like heartburn, indigestion, and irritable bowel syndrome, especially when the problems disrupt work, travel, or daily activities.

This trend underpins stable demand for digestive remedies, as individuals continue to favor quick and easy solutions that align with contemporary lifestyles. The category is also influenced by a wider concern about food quality, ingredients, and gut health, making digestive care a more frequent part of daily wellness choices. The demand of the product is focused on quick-acting relief. Within product type, indigestion and heartburn remedies represent 65% of the market, bolstered by frequent out‑of‑home eating, irregular meal timing, and the demand for user‑friendly products.

Concurrently, brands are enhancing digital engagement through online education, symptom support, and improved retail touchpoints, thereby enabling consumers to compare options and make more informed purchases throughout the digestive remedies category.

The retail format still offers strong sales support. Within the sales channel, retail offline accounts for 90% of the market, reflecting sustained consumer confidence in pharmacies and physical outlets for immediate access, expert advice, and repeat purchases. Also, product development to older adults and wider household application is broadening category relevance by offering simpler formats, weaker formulations, and more convenient packaging to take daily care of the digestive system.

UK Digestive Remedies Market Growth DriverDiet-Led Self-Care Keeps Quick Relief in Focus

Increasing attention to digestive health and everyday food choices continues to uphold digestive remedies within the United Kingdom. Consumers are increasingly self-treating mild symptoms and finding quick and easy remedies to heartburn, indigestion and irritable bowel syndrome, especially when the symptoms disrupt work, travel or daily activities. This is consistent with the larger primary-care behavior, with the community pharmacies playing a larger role in offering convenient self-care assistance.

This requirement is supported by official dietary data. The National Diet and Nutrition Survey (NDND) indicates that 72% of participants purchased food or beverages from the out‑of‑home sector within the preceding seven days, a figure that increases to 77% among adults aged 19 to 64. It further reveals that only 4% of adults meet the fibre recommendation, thereby sustaining the relevance of digestive discomfort in daily life.

UK Digestive Remedies Market ChallengePreventive Wellness Products Compete for Mild-Symptom Spend

Preventive gut‑health choices are exerting pressure on conventional digestive remedies in the United Kingdom. Consumers are increasingly questioning the quality, ingredients, and long-term health of food, leading some to choose probiotics, herbal products, or dietary changes instead of the usual over-the-counter solutions to mild digestive problems. This tendency is especially relevant in the context in which consumers perceive digestive care as a part of a more comprehensive lifestyle and nutrition program, and not a temporary therapeutic need.

This change of mindset is reflected in Food Standards Agency monitoring. Between April 2024 and March 2025, 86% to 88% of respondents indicated that food prices were a concern, while ultra‑processed food remained the second‑highest concern and ingredients and additives were included within the top five. In March 2025, 21% expressed additional concern regarding the affordability of food within the forthcoming month. Such more selective, prevention‑oriented behaviour may diminish momentum for conventional digestive remedies.

Unlock Market Intelligence

Explore the market potential with our data-driven report

UK Digestive Remedies Market TrendDigital-Led Engagement Is Changing Purchase Behaviour

The category is moving out of shelf visibility to greater digital interaction. Online education, symptom support, and digital touchpoints are becoming more widely used by brands and retailers to help consumers compare products and make purchase decisions faster. This is in line with the larger trend of convenience, and makes digestive care more accessible by means of connected retail and remote health advice as opposed to in-store discovery alone.

The power of this environment is depicted by official data. ONS reports that online sales comprised 28.3% of total retail sales in Great Britain in December 2025, up from 28.0% in November. NHS England further states that 99.9% of general practitioner practices had digital telephony in place by March 2025. This wider digital ecosystem supports app-based guidance, online advertising, and digital-first digestive health interaction.

UK Digestive Remedies Market OpportunityAge-Focused Innovation Creates More Room for Expansion

The focus on product development towards older adults and wider household application offers significant growth opportunities in the United Kingdom. The category currently has a broad age spectrum, and the demand can be expanded with the help of easy-to-swallow forms, more transparent dosing, milder formulations, and more convenient packaging to use at home. This provides brands with a chance to be more relevant in terms of daily digestive support as opposed to occasional symptom relief.

The importance of these factors is highlighted by ONS data. In 2024, 8.4 million individuals in the United Kingdom lived alone, of whom 51.1% were aged 65 years or older. The same bulletin indicates that 40.9% of women aged 65 and above also lived alone. This ageing and home-based consumer group underpins the need to have more readily available and easy to manage digestive care and justifies the need to have more age-specific product lines.

Unlock Market Intelligence

Explore the market potential with our data-driven report

UK Digestive Remedies Market Segmentation Analysis

By Product Type

- Paediatric Digestive Remedies

- Paediatric Diarrhoeal Remedies

- Paediatric Indigestion & Heartburn Remedies

- Paediatric Laxatives

- Paediatric Motion Sickness Remedies

- Diarrhoeal Remedies

- IBS Treatments

- Indigestion & Heartburn Remedies

- Antacids

- Antiflatulents

- Digestive Enzymes

- H2 Blockers

- Proton Pump Inhibitors

- Laxatives

- Motion Sickness Remedies

The segment commands the highest share within the product type category, with indigestion and heartburn remedies accounting for 65% of the market. This leadership is sustained by the fact that these products are used to treat some of the most common and acute digestive issues in the United Kingdom, especially after heavy meals, eating out, irregular meal timings, and lifestyle related discomfort. This segment remains at the center of regular purchases of digestive care due to its rapid action, high levels of familiarity, and ease of use.

This stance is supported by official dietary data. The NDNS indicates that 72% of participants purchased food or beverages from the out‑of‑home sector within the preceding seven days, and 23% recorded at least one eating occasion at a fast‑food or takeaway outlet. These practices increase the risk of acidity and post-meal pain, thus perpetuating the hegemony of indigestion and heartburn solutions.

By Sales Channel

- Retail Online

- Retail Offline

- Hospitals

- Clinics

- Pharmacies

The segment commands the highest share within the sales channel category, with retail offline holding a 90% market share. This dominance stems from the fact that digestive remedies are frequently purchased for rapid relief, and UK consumers continue to value pharmacist advice, trusted brands, and immediate access when symptoms arise. Repeat purchases are also made through physical outlets especially when dealing with well-known products that are used to treat indigestion, constipation, diarrhoea, and IBS-related discomfort.

This strength is explained by the pharmacy network of England. According to NHS Business Services Authority (NHSBSA), 10,407 community pharmacies were in operation in England as of 31 March 2025, and 1.16billion prescription items were dispensed by community pharmacies in 2024-25. This scale reinforces the significance of offline healthcare retail and contributes to maintaining store‑led sales dominance for digestive remedies.

List of Companies Covered in UK Digestive Remedies Market

The companies listed below are highly influential in the UK digestive remedies market, with a significant market share and a strong impact on industry developments.

- Rhone-Poulenc Rorer

- Teva UK Ltd

- Boots UK Ltd

- Reckitt Benckiser Group Plc (RB)

- Bayer Plc

- Haleon Plc

- McNeil Healthcare (UK) Ltd

- Boehringer Ingelheim Ltd

- Pharmacia & Upjohn Cambridge Ltd

- Omega Pharma Ltd

Competitive Landscape

The competitive landscape of digestive remedies in the UK in 2025 was led by Reckitt Benckiser Group Plc, which maintained its top position in value share, supported by the strong performance of its Gaviscon brand and a broad portfolio including Senokot, Fybogel, and Guardium. The company benefited from strong brand equity, wide distribution across pharmacies, supermarkets and e-commerce, and continued investment in marketing and consumer education. Meanwhile, Haleon Plc strengthened its position, with Tums emerging as a highly dynamic brand driven by aggressive digital marketing and rising awareness of OTC antacids. Its wider portfolio, including Andrews and Ex-Lax, further supported its competitive presence. Despite the dominance of leading players, the market remained competitive, shaped by ongoing innovation, expanding e-commerce, and increasing alignment with wellness trends.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- UK Digestive Remedies Market Policies, Regulations, and Standards

- UK Digestive Remedies Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- UK Digestive Remedies Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product Type

- Paediatric Digestive Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Diarrhoeal Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Indigestion & Heartburn Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Laxatives- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Motion Sickness Remedies- Market Insights and Forecast 2022-2032, USD Million

- Diarrhoeal Remedies- Market Insights and Forecast 2022-2032, USD Million

- IBS Treatments- Market Insights and Forecast 2022-2032, USD Million

- Indigestion & Heartburn Remedies- Market Insights and Forecast 2022-2032, USD Million

- Antacids- Market Insights and Forecast 2022-2032, USD Million

- Antiflatulents- Market Insights and Forecast 2022-2032, USD Million

- Digestive Enzymes- Market Insights and Forecast 2022-2032, USD Million

- H2 Blockers- Market Insights and Forecast 2022-2032, USD Million

- Proton Pump Inhibitors- Market Insights and Forecast 2022-2032, USD Million

- Laxatives- Market Insights and Forecast 2022-2032, USD Million

- Motion Sickness Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Digestive Remedies- Market Insights and Forecast 2022-2032, USD Million

- By Age Group

- Children & Adolescents (01-17 years)- Market Insights and Forecast 2022-2032, USD Million

- Adults (18-65 years)- Market Insights and Forecast 2022-2032, USD Million

- Geriatric (65+ years)- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- Hospitals- Market Insights and Forecast 2022-2032, USD Million

- Clinics- Market Insights and Forecast 2022-2032, USD Million

- Pharmacies- Market Insights and Forecast 2022-2032, USD Million

- By Region

- England

- Wales

- Scotland

- Northern Ireland

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Product Type

- Market Size & Growth Outlook

- UK Paediatric Digestive Remedies Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- UK Diarrhoeal Remedies Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- UK IBS Treatments Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- UK Indigestion & Heartburn Remedies Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- UK Laxatives Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- UK Motion Sickness Remedies Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Reckitt Benckiser Group Plc (RB)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Bayer Plc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Haleon Plc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- McNeil Healthcare (UK) Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Boehringer Ingelheim Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Rhône-Poulenc Rorer

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Teva UK Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Boots UK Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Pharmacia & Upjohn Cambridge Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Omega Pharma Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Reckitt Benckiser Group Plc (RB)

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Age Group |

|

| By Sales Channel |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.