UK Contact Lenses and Solutions Market Report: Trends, Growth and Forecast (2026-2032)

By Product Type (Contact Lenses (Standard Vision Correction Lenses, Myopia Control Lenses), Contact Lens Solutions), By Usage (Contact Lenses (Daily Disposable, Bi-Weekly, Monthly, Quarterly/Annual), Contact Lens Solutions (Daily-Use Care Solutions, Weekly/Periodic Deep-Clean Systems, Travel/Mini Packs)), By Material Type (Contact Lenses (Silicone Hydrogel, Hydrogel (Soft), Rigid Gas Permeable (RGP), Hybrid/Scleral/Specialty), Contact Lens Solutions (Multi-Purpose Solutions, Hydrogen Peroxide Systems, Saline Solutions, Enzymatic & Specialty Cleaners)), By Application (Contact Lenses (Spherical (Myopia/Hyperopia), Toric (Astigmatism), Multifocal (Presbyopia), Myopia Control, Cosmetic/Colored, Therapeutic/Medical), Contact Lens Solutions (Soft Lens Care, RGP Lens Care, Sensitive Eye/Preservative-Free Care)), By Sales Channel (Retail Offline (Optical Stores, Hospitals & Clinics, Others (Pharmacies, Beauty Centres, etc.)), Retail Online (Company-owned Portals, E-commerce Platforms)), By Pack Size (Contact Lenses (Trial Packs, Standard Packs, Bulk/Value Packs), Contact Lens Solutions (Up to 120 mL, 121–360 mL, Above 360 mL, Combo/Twin Packs)), By Region (England, Wales, Scotland, Northern Ireland) ... Read more

|

Major Players

|

UK Contact Lenses and Solutions Market Statistics and Insights, 2026

- Market Size Statistics

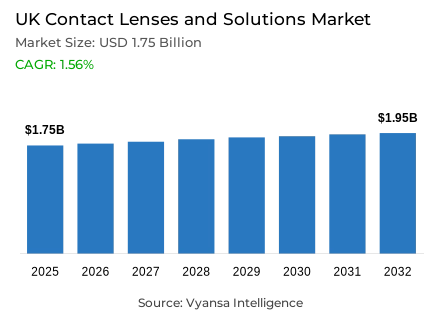

- Contact lenses and solutions market size in UK was estimated at USD 1.75 billion in 2025.

- The market size is expected to grow to USD 1.95 billion by 2032.

- Market to register a CAGR of around 1.56% during 2026-32.

- Product Type Shares

- Contact lenses grabbed market share of 80%.

- Competition

- More than 5 companies are actively engaged in producing contact lenses and solutions in UK.

- Top 5 companies acquired around 55% of the market share.

- Vistakon UK Ltd, Boots Opticians Ltd, Vision Express (UK) Ltd, Johnson & Johnson Ltd, Ciba Vision UK Ltd etc., are few of the top companies.

- Sales Channel

- Retail offline grabbed 65% of the market.

UK Contact Lenses and Solutions Market Outlook

The UK contact lenses and solutions market size was valued at USD 1.75 billion in 2025 and is projected to grow from USD 1.78 billion in 2026 to USD 1.95 billion by 2032. The rising prevalence of childhood myopia leads to growth in 2026. According to NHS Digital’s Health Survey for England (2022), eyesight problems remain among the most commonly reported long-standing conditions among children aged 5-15 years, while the Office for National Statistics (ONS, 2025) confirms that 98% of children aged 8-15 years use the internet daily, reinforcing sustained near‑vision use. The WHO (2025) and other health authorities have linked the development of myopia to increased screen time, which highlights the fundamental importance of corrective and management-based lenses. This environment continues to support steady uptake of contact lenses and solutions among digitally active households.

Nevertheless, the strain on household budgets remains a key issue. According to ONS (2025), around 26% of adults in early 2025 found it difficult to pay for essential living expenses, indicating sustained budget strain despite easing inflation. ONS (2025) retail data also point to cautious end user spending, where value sales are more often increasing than volume sales, indicating price sensitivity. This situation promotes price comparison and affordability among end users, which prevents quick premium growth.

The main trend in 2026 is the incorporation of digital purchasing. According to ONS (2025), internet sales contributed approximately 27% to total UK retail sales, and over 95% of adults accessed the internet, reaffirming the importance of online repeat business. End users are increasingly using in-store eye tests and digital refills, preferring subscription and home delivery.

The main opportunity in 2026 is the development of innovation in the field of myopia control.National Institute of Health and Care Excellence (NICE,2025) states that the early treatment of progressive myopia is a priority, and the Life Sciences Vision Update (2025) by the UK Government emphasizes long-term investments in innovative medical equipment. Segmentation data show that contact lenses hold an 80% market share under product type, and retail offline contributes 65% under sales channel, indicating a continued need for professional consultation alongside the growing trend of digital repeat business.

UK Contact Lenses and Solutions Market Growth DriverRising Myopia Prevalence Among Children Drives Preventive Eye Care Demand

The increasing prevalence of myopia in children in England is a major demand driver in 2026. According to NHS Digital’s Health Survey for England, eyesight problems remain among the most commonly reported long-standing conditions among children aged 5–15 years. Furthermore, the UK Health Security Agency points out the increasing alarm about the early development of myopia as a result of excessive screen time. Demand is further supported by the increased awareness of parents about the need to use corrective and preventive eye-care solutions.

The Office for National Statistics (ONS, 2025) states that 98% of children aged 8–15 years use the internet daily, thereby solidifying the trend of near‑vision activity. Public-health organisations like the WHO globally have recognised the long-term use of digital devices as a significant contributor to the development of myopia. Myopia contact lenses that are comfort-oriented are directly benefiting by this paradigm shift in visual behaviour as parents are looking to find early solutions to the problem.

UK Contact Lenses and Solutions Market ChallengeCost-of-Living Pressures Constrain Premium Spending

In 2026, economic constraint is still a major factor. The Office for National Statistics (2025) confirms that, although inflation has been moderated in the recent past, economic budgets are strained by high prices in the previous years. In early 2025, around 26% of adults reported difficulty in paying for essential living expenses as stated by ONS Public Opinions and Social Trends. This situation continues the price sensitivity trend in discretionary expenditure in the health and personal care segment.

In addition, the ONS Retail Sales Bulletin (2025) indicates that end users remain cautious in their expenditure patterns. Value growth has been on the increase at a faster rate than volume growth in various retail industries, which points to cautious consumption habits. The use of contact-lenses is shifting towards the use of the private-label products and competitive pricing mechanisms thus limiting the high-price growth. As a result, the trend of restrained value growth is supported by price competition and sound spending habits.

Unlock Market Intelligence

Explore the market potential with our data-driven report

UK Contact Lenses and Solutions Market TrendShift Toward Online Purchasing of Replenishment Products

The trend of online buying is a force in eyewear buying in 2026. Based on the Office for National Statistics (2025), internet sales contributed approximately 27% of total retail sales in the UK in 2025, indicating a continued adoption trend. This paradigm shift allows the purchase of prescription-based products online after visiting the physical opticians.

The legal prescription release clause is becoming a more popular tool of price comparison among customers online. The ONS also indicates that over 95% of adults accessed the internet in 2025, signalling a continued high level of digital accessibility. The trend enables subscription, home delivery, and online discount stores to replenish sales and maintain the physical optician to perform eye tests and issue prescriptions.

UK Contact Lenses and Solutions Market OpportunityTechnological Innovation in Myopia Management Expands Clinical Scope

In 2026, there is a significant opportunity in technological advancements in the field of myopia control. National Institute of Health and Care Excellence (NICE, 2025) still advocates early intervention of progressive myopia among children. The increased professional acceptance reinforces the use of specialised corrective measures other than conventional glasses.

Moreover, UK university-funded and international research projects are still working on smart and sensor-enabled ophthalmic technologies. According to the UK Government Life Sciences Vision Update (2025), the country will continue to invest in innovative medical devices and digital health technologies. The developments present prospects of advanced contact-lens materials and innovations, especially in the control of myopia and comfort-enhanced designs to allow extended screen time.

Unlock Market Intelligence

Explore the market potential with our data-driven report

UK Contact Lenses and Solutions Market Segmentation Analysis

By Product Type

- Contact Lenses

- Contact Lens Solutions

The category with the largest market share in relation to product type is contact lenses, with a market share of 80%. This shows that end users are more oriented to direct vision-correction solutions rather than ancillary care products. Contact lenses continue to be at the centre of demand in this category.

Solutions are a complementary category to replacement cycles, yet the growth momentum still lies within the lens products category itself. Continued development of material and comfort technology maintains the structural dominance of the contact-lens category in the product line, which forms the core of category performance.

By Sales Channel

- Retail Offline

- Retail Online

The category with the largest share in terms of sales channel is retail offline, commanding 65% market share. The prescription requirement that must be provided by the offline channel of optical retailing ensures that the channel remains dominant because the prescription has to be provided by the offline channel through offline consultations, thus reaffirming the necessity of the presence of opticians in the purchase process.

Even though digital platforms allow convenient repeat business, the initial fitting and professional advice is deeply entrenched in offline retail. The professionalism of professionals is appreciated by the customers, particularly in the case of first-time buyers and pediatric myopia control. Therefore, offline retail maintains its structural importance even though the repeat-business segment is gradually being digitalized.

List of Companies Covered in UK Contact Lenses and Solutions Market

The companies listed below are highly influential in the UK contact lenses and solutions market, with a significant market share and a strong impact on industry developments.

- Vistakon UK Ltd

- Boots Opticians Ltd

- Vision Express (UK) Ltd

- Johnson & Johnson Ltd

- Ciba Vision UK Ltd

- CooperVision UK Ltd

- Specsavers Optical Group Ltd

- Bausch & Lomb UK Ltd

Competitive Landscape

The competitive landscape of contact lenses and solutions in the UK in 2025 remains led by Johnson & Johnson Ltd, which holds a 19.3% value share, supported primarily by its Acuvue portfolio of daily disposable lenses. The brand benefits from strong consumer trust, widespread optician partnerships, and continued demand for premium, comfort-focused products. However, competition is intensifying. Ciba Vision UK Ltd ranks second with a 13.2% share, strengthening its position through product innovation such as the launch of PRECISION7 weekly lenses and continued expansion in daily disposable offerings. The market is characterised by established multinational players competing on technology, professional engagement, and portfolio breadth. At the same time, private label expansion by major optical retailers and growing price sensitivity among consumers are reshaping competitive dynamics, placing pressure on leading brands to balance innovation with value-driven positioning.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- UK Contact Lenses and Solution Market Policies, Regulations, and Standards

- UK Contact Lenses and Solution Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- UK Contact Lenses and Solution Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold in Thousand Units

- Market Segmentation & Growth Outlook

- By Product Type

- Contact Lenses- Market Insights and Forecast 2022-2032, USD Million

- Standard Vision Correction Lenses- Market Insights and Forecast 2022-2032, USD Million

- Myopia Control Lenses- Market Insights and Forecast 2022-2032, USD Million

- Contact Lens Solutions- Market Insights and Forecast 2022-2032, USD Million

- Contact Lenses- Market Insights and Forecast 2022-2032, USD Million

- By Usage

- Contact Lenses- Market Insights and Forecast 2022-2032, USD Million

- Daily Disposable- Market Insights and Forecast 2022-2032, USD Million

- Bi-Weekly- Market Insights and Forecast 2022-2032, USD Million

- Monthly- Market Insights and Forecast 2022-2032, USD Million

- Quarterly/Annual- Market Insights and Forecast 2022-2032, USD Million

- Contact Lens Solutions- Market Insights and Forecast 2022-2032, USD Million

- Daily-Use Care Solutions- Market Insights and Forecast 2022-2032, USD Million

- Weekly/Periodic Deep-Clean Systems- Market Insights and Forecast 2022-2032, USD Million

- Travel/Mini Packs- Market Insights and Forecast 2022-2032, USD Million

- Contact Lenses- Market Insights and Forecast 2022-2032, USD Million

- By Material Type

- Contact Lenses- Market Insights and Forecast 2022-2032, USD Million

- Silicone Hydrogel- Market Insights and Forecast 2022-2032, USD Million

- Hydrogel (Soft)- Market Insights and Forecast 2022-2032, USD Million

- Rigid Gas Permeable (RGP)- Market Insights and Forecast 2022-2032, USD Million

- Hybrid/Scleral/Specialty- Market Insights and Forecast 2022-2032, USD Million

- Contact Lens Solutions- Market Insights and Forecast 2022-2032, USD Million

- Multi-Purpose Solutions- Market Insights and Forecast 2022-2032, USD Million

- Hydrogen Peroxide Systems- Market Insights and Forecast 2022-2032, USD Million

- Saline Solutions- Market Insights and Forecast 2022-2032, USD Million

- Enzymatic & Specialty Cleaners- Market Insights and Forecast 2022-2032, USD Million

- Contact Lenses- Market Insights and Forecast 2022-2032, USD Million

- By Application

- Contact Lenses- Market Insights and Forecast 2022-2032, USD Million

- Spherical (Myopia/Hyperopia)- Market Insights and Forecast 2022-2032, USD Million

- Toric (Astigmatism)- Market Insights and Forecast 2022-2032, USD Million

- Multifocal (Presbyopia)- Market Insights and Forecast 2022-2032, USD Million

- Myopia Control- Market Insights and Forecast 2022-2032, USD Million

- Cosmetic/Colored- Market Insights and Forecast 2022-2032, USD Million

- Therapeutic/Medical- Market Insights and Forecast 2022-2032, USD Million

- Contact Lens Solutions- Market Insights and Forecast 2022-2032, USD Million

- Soft Lens Care- Market Insights and Forecast 2022-2032, USD Million

- RGP Lens Care- Market Insights and Forecast 2022-2032, USD Million

- Sensitive Eye/Preservative-Free Care- Market Insights and Forecast 2022-2032, USD Million

- Contact Lenses- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- Optical Stores- Market Insights and Forecast 2022-2032, USD Million

- Hospitals & Clinics- Market Insights and Forecast 2022-2032, USD Million

- Others (Pharmacies, Beauty Centres, etc.)- Market Insights and Forecast 2022-2032, USD Million

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- Company-owned Portals- Market Insights and Forecast 2022-2032, USD Million

- E-commerce Platforms- Market Insights and Forecast 2022-2032, USD Million

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- By Pack Size

- Contact Lenses- Market Insights and Forecast 2022-2032, USD Million

- Trial Packs- Market Insights and Forecast 2022-2032, USD Million

- Standard Packs- Market Insights and Forecast 2022-2032, USD Million

- Bulk/Value Packs- Market Insights and Forecast 2022-2032, USD Million

- Contact Lens Solutions- Market Insights and Forecast 2022-2032, USD Million

- Up to 120 mL- Market Insights and Forecast 2022-2032, USD Million

- 121–360 mL- Market Insights and Forecast 2022-2032, USD Million

- Above 360 mL- Market Insights and Forecast 2022-2032, USD Million

- Combo/Twin Packs- Market Insights and Forecast 2022-2032, USD Million

- Contact Lenses- Market Insights and Forecast 2022-2032, USD Million

- By Region

- England

- Wales

- Scotland

- Northern Ireland

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Product Type

- Market Size & Growth Outlook

- UK Contact Lenses Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold in Thousand Units

- Market Segmentation & Growth Outlook

- By Usage- Market Insights and Forecast 2022-2032, USD Million

- By Material Type- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Pack Size- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- UK Contact Lens Solutions Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold in Thousand Units

- Market Segmentation & Growth Outlook

- By Usage- Market Insights and Forecast 2022-2032, USD Million

- By Material Type- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Pack Size- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Johnson & Johnson Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Ciba Vision UK Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- CooperVision UK Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Specsavers Optical Group Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Bausch & Lomb UK Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Vistakon UK Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Boots Opticians Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Vision Express (UK) Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Swisslens SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Johnson & Johnson Ltd

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Usage |

|

| By Material Type |

|

| By Application |

|

| By Sales Channel |

|

| By Pack Size |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.