UK Anti-Aging Products Market Report: Trends, Growth and Forecast (2026-2032)

By Product Type (Creams & Moisturizers, Serums, Sunscreens/SPF Day Creams, Exfoliators/Peels, Masks, Targeted Treatments/Spot Correctors), By Claim/Benefit Type (Wrinkle & Fine-Line Reduction, Firming/Lifting Appearance, Hydration/Plumping, Brightening/Age-Spot Correction, Barrier Repair/Sensitive Mature Skin, Sun Protection/Photoaging Prevention), By Sales Channel (Retail Offline (Supermarkets/Hypermarkets, Pharmacy/Drugstores, Specialty Beauty Stores, Department Stores, Brand Exclusive Stores, Clinics/Salons/Spas, Other Offline Retail), Retail Online (Brand-Owned Websites, E-commerce Marketplaces, Online Beauty Retailers, Online Pharmacy Platforms, Social Commerce Platforms, Quick Commerce/On-Demand Delivery Platforms, Other Online Retail)), By Ingredient Platform (Retinoids, Hyaluronic Acid, Niacinamide, Vitamin C, Peptides, AHAs/BHAs, Ceramides, Botanical/Natural Actives, Others), By Consumer Age Group (18–34 Years, 35–54 Years, 55 Years & Above), By End User (Women, Men, Unisex), By Price Tier (Mass, Premium), By Regions (England, Wales, Scotland, Northern Ireland) ... Read more

|

Major Players

|

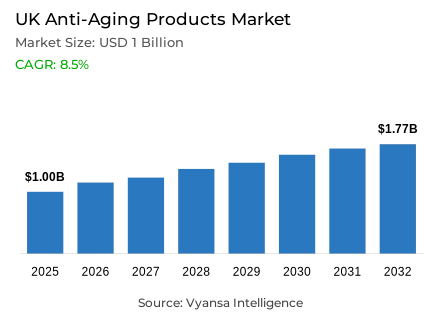

UK Anti-Aging Products Market Statistics and Insights, 2026

- Market Size Statistics

- Anti-aging products market size in UK was valued at USD 1 billion in 2025 and is estimated at USD 1.09 billion in 2026.

- The market size is expected to grow to USD 1.77 billion by 2032.

- Market to register a CAGR of around 8.5% during 2026-32.

- Product Type Shares

- Creams & moisturizers grabbed market share of 30%.

- Competition

- More than 10 companies are actively engaged in producing anti-aging products in UK.

- Top 5 companies acquired around 15% of the market share.

- DECIEM Beauty Group Inc., ELEMIS Limited, TROPIC SKINCARE LIMITED, The Estee Lauder Companies Inc., L'Oreal S.A. etc., are few of the top companies.

- Claim/Benefit Type

- Wrinkle & fine-line reduction grabbed 25% of the market.

UK Anti-Aging Products Market Outlook

Valued at USD 1 billion in 2025, the UK anti-aging products market is advancing from USD 1.09 billion in 2026 toward USD 1.77 billion by 2032, representing 8.5% compound annual growth rate throughout the forecast window. This market expansion reflects steady growth supported by rising consumer demand for skincare solutions addressing visible skin maintenance, daily nourishment, and targeted appearance-focused benefits. Market momentum remains underpinned by extended life expectancy driving sustained engagement with appearance-led skincare, digital-first consumer behavior reshaping product discovery patterns, and stable pensioner income supporting premium mature-skin positioning.

Extended life expectancy establishes foundational market driver sustaining consumer investment in appearance-focused anti-aging products and long-term skin-maintenance routines throughout extended consumer lifespans. Evidence from Office for National Statistics reveals life expectancy at age 65 in UK during 2022 to 2024 stands at 21.2 years for females and 18.7 years for males, establishing extended engagement with appearance-led skincare needs. This longevity directly supports market growth through heightened consumer focus on daily support in hydration, firmness, and visible skin maintenance across broader age span. Population aged 90 years and over rises to 625,000 in 2024, while centenarians reach 16,600, establishing demographic shift supporting steadier demand for products positioned around mature-skin care and long-term wrinkle management throughout UK market.

Digital-first consumer behavior and online shopping growth reshape UK anti-aging products market toward convenient discovery and repeat purchasing through digital channels. Published data from Ofcom indicates 95% of UK population aged 16 and over has internet access at home in 2025, with adults spending average 4 hours 30 minutes online daily, enabling continuous skincare product research and comparison. Analysis from Office for National Statistics reveals online sales values rise 14.7% in January 2026 compared with January 2025, with online share of total retail sales standing at 28.2%, supporting stronger movement toward online-led launches and premium skincare selling. Digital infrastructure enables anti-aging product discovery through social platforms, ingredient education, and direct online comparison before purchase driving consumer preference for clearly substantiated benefit claims.

Market segmentation demonstrates pronounced consumer preference for practical formats and performance-focused benefit positioning. Creams and moisturizers command 30% market share through alignment with daily-use routines delivering consistent hydration and visible skin-support benefits, while wrinkle and fine-line reduction claims account for 25% of demand reflecting consumer prioritization of measurable outcomes. This UK anti-aging products market structure indicates consumers increasingly select familiar formats supporting routine application while demanding clear efficacy claims addressing visible aging concerns, enabling brands to deliver targeted benefits through accessible daily-use products maintaining strong retail visibility and competitive positioning.

UK Anti-Aging Products Market Growth Driver

Longer Lives Keep Demand Expanding

Extended life expectancy creates sustained demand for UK anti-aging products addressing visible aging concerns and long-term skin-maintenance needs throughout extended consumer lifespans. Statistics from Office for National Statistics confirm life expectancy at age 65 in UK during 2022 to 2024 stands at 21.2 years for females and 18.7 years for males, establishing extended engagement window with appearance-led skincare across mature demographics. This longevity directly translates into heightened market relevance for anti-aging skincare emphasizing daily support in hydration, firmness, and visible wrinkle reduction addressing persistent aging concerns over decades. Older population growth at top age brackets supports steadier demand for products positioned around mature-skin care and nourishment.

Expanding ultra-aged population segments create structural demand driver sustaining UK anti-aging products market expansion throughout forecast period. Published records from Office for National Statistics reveal number of people aged 90 years and over rises to 625,000 in 2024, while centenarians reach 16,600, establishing demographic concentration requiring specialized anti-aging skincare addressing advanced aging concerns. This demographic expansion supports market opportunity for brands positioning products around long-term wrinkle management, daily comfort, and age-specific skincare benefits serving consumers managing multiple aging concerns simultaneously. Extended lifespan and growing ultra-aged populations establish durable commercial foundation supporting sustained category relevance independent of cyclical economic factors.

UK Anti-Aging Products Market Challenge

Claims Scrutiny Raises Launch Complexity

Anti-aging market faces substantial compliance burden from stringent advertising standards and claims substantiation requirements affecting marketing communication strategies for UK brands. Official records from Advertising Standards Authority and Committee of Advertising Practice (CAP) indicate they scan nearly 60 million online ads annually, resolve over 40,000 complaints, and secure amendment or removal of 22,383 ads, establishing rigorous enforcement environment. This regulatory intensity makes anti-aging messaging significantly harder because brands must support language around repair, lifting, and visible line reduction with stronger evidence substantiation. Compliance load directly impacts market communication strategies, requiring enhanced documentation and clinical validation of product benefit claims throughout product development and marketing cycles.

Product notification requirements and formulation substance restrictions create additional regulatory burden affecting market entry timelines and portfolio expansion activities. Evidence from Office for Product Safety and Standards indicates every cosmetic product available to consumers in Great Britain must be notified to Office for Product Safety and Standards (OPSS), with non-notification leading to unlimited fines in England and Wales or up to £5,000 in Scotland and Northern Ireland, plus up to three months imprisonment. Analysis from UK legislation reveals further cosmetic substance restrictions came into force on 31 January 2025, with transitional deadlines running through 20 October 2025 and 2 March 2026. This regulatory environment slows product launches and increases execution risk for brands attempting rapid innovation cycles and market expansion in UK anti-aging products category.

Unlock Market Intelligence

Explore the market potential with our data-driven report

UK Anti-Aging Products Market Trend

Digital Discovery Moves to the Front

Consumer purchasing behavior demonstrates pronounced shift toward digital-first product discovery, comparison, and repeat purchasing supported by universal internet access and sustained online engagement. Market data from Ofcom indicates 95% of UK population aged 16 and over has internet access at home in 2025, with adults spending average 4 hours 30 minutes online daily, establishing comprehensive digital connectivity enabling continuous skincare research. This digital dominance keeps anti-aging products increasingly tied to social discovery, reviews, ingredient education, and direct online comparison before purchase, reshaping competitive advantage toward brands establishing authentic digital presence and transparent benefit positioning. Internet accessibility supports faster awareness for new anti-aging product launches and enables consumer empowerment through ingredient research and product comparison.

Online retail expansion and digital channel growth accelerate anti-aging products market shift toward e-commerce-led purchasing and direct consumer engagement. Published data from Office for National Statistics reveals online sales values rise 14.7% in January 2026 compared with January 2025, while online share of total retail sales stands at 28.2%, establishing pronounced digital dominance in retail landscape. This shift supports stronger movement toward online-led launches, replenishment buying, and premium skincare selling through digital channels across UK market. Digital platforms enable brands developing night repair creams, facial oils for mature skin, and anti-aging eye creams to establish direct consumer relationships bypassing traditional retail gatekeepers and capturing valuable first-party consumer data supporting targeted marketing and repeat purchase optimization.

UK Anti-Aging Products Market Opportunity

Silver Spending Opens Premium White Space

Strong opportunities emerge in premium mature-skin anti-aging product lines positioned for older households with stable income profiles and demonstrated purchasing power supporting premium positioning. Official records from Department for Work and Pensions indicate average weekly income for pensioner couples in UK stands at £634 in FYE 2023 to FYE 2025, while single pensioners record £322 per week, establishing sufficient household income supporting premium anti-aging product participation. This purchasing power creates meaningful opportunity for brands positioning UK anti-aging products around comfort, routine use, and higher-value skincare benefits addressing specific mature-skin concerns. Premium portfolio development targeting older consumers represents clear commercial opportunity where stable income and established consumer relationships support sustained purchasing of premium anti-aging creams and specialized skincare solutions.

Stable income flows across older consumer base and universal State Pension coverage strengthen business case for premium anti-aging market solutions targeting senior demographics. Evidence from Department for Work and Pensions reveals 98% of pensioners receive State Pension in both FYE 2022 and FYE 2025, establishing dependable income foundation supporting consistent consumer spending throughout retirement. This income stability supports market opportunity for premium lines built around hydration, repair, and age-specific skincare care, particularly where brands combine trusted claims, gentler formulations, and easier-to-follow routines for long-term use. Stable demographic income and predictable spending patterns enable brands developing premium anti-aging skincare to build sustainable business models targeting affluent older consumers prioritizing skincare quality and routine convenience.

Unlock Market Intelligence

Explore the market potential with our data-driven report

UK Anti-Aging Products Market Segmentation Analysis

By Product Type

- Creams & Moisturizers

- Serums

- Sunscreens/SPF Day Creams

- Exfoliators/Peels

- Masks

- Targeted Treatments/Spot Correctors

Creams and moisturizers command market leadership at 30% share within UK anti-aging products market, establishing dominant product type positioning through superior alignment with consumer preferences for practical daily-use formats. This market segment maintains leading position due to strong consumer preference for easy-to-apply, familiar formats integrating seamlessly into established morning and evening skincare routines emphasizing hydration and visible skin-support benefits. Cream and moisturizer formulations deliver accessible positioning supporting routine daily application while maintaining adequate performance for sustained wrinkle reduction and firmness support addressing broad consumer demographics seeking practical anti-aging solutions.

This market leadership position reflects consumers' continued selection of practical product types supporting daily use integration without specialized techniques or complexity. Creams and moisturizers support repeated morning and evening application, delivering hydration and anti-aging benefits within single accessible format supporting routine adherence and repeat purchase behavior. The 30% market share indicates this segment continues shaping UK anti-aging products demand, retail shelf presence, and launch priorities across the broader industry. Consumers continue preferring familiar formats combining nourishment and visible care without complicating routines, enabling manufacturers maintaining cream and moisturizer leadership to develop formulation innovation supporting category expansion through advanced delivery systems and clinically validated actives addressing mature-skin concerns.

By Claim/Benefit Type

- Wrinkle & Fine-Line Reduction

- Firming/Lifting Appearance

- Hydration/Plumping

- Brightening/Age-Spot Correction

- Barrier Repair/Sensitive Mature Skin

- Sun Protection/Photoaging Prevention

Wrinkle and fine-line reduction claims command market leadership at 25% share within UK anti-aging products market benefit segment, establishing categorical dominance reflecting consumer prioritization of measurable outcomes over generic age-care positioning. This market segment demonstrates consumers remain focused on visible and targeted skincare outcomes rather than relying exclusively on broad beauty positioning when selecting anti-aging products. Consumers across age groups expect anti-aging skincare demonstrating efficacy around wrinkle softening, fine-line reduction, and visible texture improvement supporting sustained engagement with products delivering measurable performance outcomes.

Product development continues being shaped by outcome-driven requirements as manufacturers emphasize clear benefit communication and functional value throughout competitive UK anti-aging products market environments. Brands formulating wrinkle and fine-line reduction claims emphasize anti-aging serums, retinol-based skincare, and hyaluronic acid formulations addressing consumer expectations around targeted fine-line improvement and visible wrinkle softening. The 25% market share indicates this benefit segment continues influencing product claims, innovation priorities, and competitive positioning throughout UK anti-aging industry. Purchase decisions increasingly guided by clear functional value and direct performance expectations rather than broad beauty messaging alone, enabling manufacturers maintaining wrinkle and fine-line reduction claim leadership to develop product innovation capturing sustained demand through targeted benefit positioning and substantiated performance claims supporting category expansion throughout forecast period.

List of Companies Covered in UK Anti-Aging Products Market

The companies listed below are highly influential in the UK anti-aging products market, with a significant market share and a strong impact on industry developments.

- DECIEM Beauty Group Inc.

- ELEMIS Limited

- TROPIC SKINCARE LIMITED

- The Estee Lauder Companies Inc.

- L'Oreal S.A.

- The Procter & Gamble Company

- Unilever PLC

- Coty Inc.

- TEMPLESPA LIMITED

- No7 Beauty Company

Market News & Updates

- The Estée Lauder Companies Inc., 2026:

In April 2026, Estée Lauder announced new clinical results for Re-Nutriv. The company published two peer-reviewed anti-aging manuscripts. These validated Re-Nutriv’s sirtuin-targeting formulations and visible-age assessment model. The studies covered the Ultimate Diamond serum, soft crème, and eye crème. Estée Lauder’s official UK site also actively sells Re-Nutriv. This gives the innovation direct relevance for UK consumers. For the UK anti-aging products market, this strengthens science-led premium skincare. It also supports stronger product trust and premium category differentiation.

- No7 Beauty Company, 2025:

In April 2025, No7 launched its new Future Renew Night Serum. The company called it its most advanced night formulation. The serum combines No7’s super peptide blend with Lindera Strychnifolia. It also includes niacinamide, hyaluronic acid, and vitamin C. No7 said the product synchronizes with skin’s overnight repair cycle. The company also launched the Future Renew Peptide Cleanser. It added a new 75ml size for Future Renew Serum. For the UK anti-aging products market, this is significant. It expands a major domestic anti-aging franchise with fresh formats. It also strengthens competition in clinically positioned mass-premium skincare.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- UK Anti-Aging Products Market Policies, Regulations, and Standards

- UK Anti-Aging Products Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- UK Anti-Aging Products Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product Type

- Creams & Moisturizers- Market Insights and Forecast 2022-2032, USD Million

- Serums- Market Insights and Forecast 2022-2032, USD Million

- Sunscreens/SPF Day Creams- Market Insights and Forecast 2022-2032, USD Million

- Exfoliators/Peels- Market Insights and Forecast 2022-2032, USD Million

- Masks- Market Insights and Forecast 2022-2032, USD Million

- Targeted Treatments/Spot Correctors- Market Insights and Forecast 2022-2032, USD Million

- By Claim/Benefit Type

- Wrinkle & Fine-Line Reduction- Market Insights and Forecast 2022-2032, USD Million

- Firming/Lifting Appearance- Market Insights and Forecast 2022-2032, USD Million

- Hydration/Plumping- Market Insights and Forecast 2022-2032, USD Million

- Brightening/Age-Spot Correction- Market Insights and Forecast 2022-2032, USD Million

- Barrier Repair/Sensitive Mature Skin- Market Insights and Forecast 2022-2032, USD Million

- Sun Protection/Photoaging Prevention- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- Supermarkets/Hypermarkets- Market Insights and Forecast 2022-2032, USD Million

- Pharmacy/Drugstores- Market Insights and Forecast 2022-2032, USD Million

- Specialty Beauty Stores- Market Insights and Forecast 2022-2032, USD Million

- Department Stores- Market Insights and Forecast 2022-2032, USD Million

- Brand Exclusive Stores- Market Insights and Forecast 2022-2032, USD Million

- Clinics/Salons/Spas- Market Insights and Forecast 2022-2032, USD Million

- Other Offline Retail- Market Insights and Forecast 2022-2032, USD Million

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- Brand-Owned Websites- Market Insights and Forecast 2022-2032, USD Million

- E-commerce Marketplaces- Market Insights and Forecast 2022-2032, USD Million

- Online Beauty Retailers- Market Insights and Forecast 2022-2032, USD Million

- Online Pharmacy Platforms- Market Insights and Forecast 2022-2032, USD Million

- Social Commerce Platforms- Market Insights and Forecast 2022-2032, USD Million

- Quick Commerce/On-Demand Delivery Platforms- Market Insights and Forecast 2022-2032, USD Million

- Other Online Retail- Market Insights and Forecast 2022-2032, USD Million

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- By Ingredient Platform

- Retinoids- Market Insights and Forecast 2022-2032, USD Million

- Hyaluronic Acid- Market Insights and Forecast 2022-2032, USD Million

- Niacinamide- Market Insights and Forecast 2022-2032, USD Million

- Vitamin C- Market Insights and Forecast 2022-2032, USD Million

- Peptides- Market Insights and Forecast 2022-2032, USD Million

- AHAs/BHAs- Market Insights and Forecast 2022-2032, USD Million

- Ceramides- Market Insights and Forecast 2022-2032, USD Million

- Botanical/Natural Actives- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Consumer Age Group

- 18–34 Years- Market Insights and Forecast 2022-2032, USD Million

- 35–54 Years- Market Insights and Forecast 2022-2032, USD Million

- 55 Years & Above- Market Insights and Forecast 2022-2032, USD Million

- By End User

- Women- Market Insights and Forecast 2022-2032, USD Million

- Men- Market Insights and Forecast 2022-2032, USD Million

- Unisex- Market Insights and Forecast 2022-2032, USD Million

- By Price Tier

- Mass- Market Insights and Forecast 2022-2032, USD Million

- Premium- Market Insights and Forecast 2022-2032, USD Million

- By Regions

- England- Market Insights and Forecast 2022-2032, USD Million

- Wales- Market Insights and Forecast 2022-2032, USD Million

- Scotland- Market Insights and Forecast 2022-2032, USD Million

- Northern Ireland- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Product Type

- Market Size & Growth Outlook

- UK Creams & Moisturizers Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Claim/Benefit Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Ingredient Platform- Market Insights and Forecast 2022-2032, USD Million

- By Consumer Age Group- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Price Tier- Market Insights and Forecast 2022-2032, USD Million

- By Regions- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- UK Serums Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Claim/Benefit Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Ingredient Platform- Market Insights and Forecast 2022-2032, USD Million

- By Consumer Age Group- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Price Tier- Market Insights and Forecast 2022-2032, USD Million

- By Regions- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- UK Sunscreens/SPF Day Creams Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Claim/Benefit Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Ingredient Platform- Market Insights and Forecast 2022-2032, USD Million

- By Consumer Age Group- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Price Tier- Market Insights and Forecast 2022-2032, USD Million

- By Regions- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- UK Exfoliators/Peels Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Claim/Benefit Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Ingredient Platform- Market Insights and Forecast 2022-2032, USD Million

- By Consumer Age Group- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Price Tier- Market Insights and Forecast 2022-2032, USD Million

- By Regions- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- UK Masks Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Claim/Benefit Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Ingredient Platform- Market Insights and Forecast 2022-2032, USD Million

- By Consumer Age Group- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Price Tier- Market Insights and Forecast 2022-2032, USD Million

- By Regions- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- UK Targeted Treatments/Spot Correctors Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Claim/Benefit Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Ingredient Platform- Market Insights and Forecast 2022-2032, USD Million

- By Consumer Age Group- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Price Tier- Market Insights and Forecast 2022-2032, USD Million

- By Regions- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- L'Oreal S.A.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- The Procter & Gamble Company

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Beiersdorf AG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Unilever PLC

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- The Estee Lauder Companies Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Galderma S.A.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Laboratoires Pierre Fabre

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Coty Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Johnson & Johnson

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Shiseido Company Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- L'Oreal S.A.

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Claim/Benefit Type |

|

| By Sales Channel |

|

| By Ingredient Platform |

|

| By Consumer Age Group |

|

| By End User |

|

| By Price Tier |

|

| By Regions |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.