UAE Sleep Aids Market Report: Trends, Growth and Forecast (2026-2032)

By Product (Single Ingredient (Doxylamine Succinate, Diphenhydramine, Melatonin), Combination Ingredient (Diphenhydramine + Acetaminophen, Other Antihistamine-Based Combinations), Herbal & Traditional Sleep Aids (Valerian root, Passionflower, Chamomile, Kava, Multi-Herbal Sleep Blends)), By Sleep Disorder (Insomnia, Sleep Apnea, Restless Legs Syndrome, Narcolepsy, Sleep Walking, Others), By Age Group (Young to Mid Adults (25-44 Years), Middle-Aged Adults (45-64 Years), Geriatric Population (65+ Years)), By Sales Channel (Retail Online, Retail Offline), By End User (Homecare/Individual Consumers, Hospitals, Sleep Centers & Clinics), By Formulation (Tablets, Gummies, Capsules, Liquid, Sublingual), By Region (Dubai, Abu Dhabi, Sharjah, Northern Emirates) ... Read more

|

Major Players

|

UAE Sleep Aids Market Statistics and Insights, 2026

- Market Size Statistics

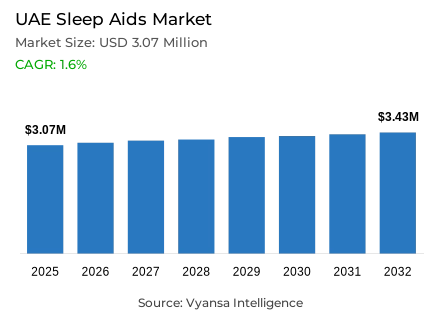

- Sleep aids market size in UAE was estimated at USD 3.07 million in 2025

- The market size is expected to grow to USD 3.43 million by 2032.

- Market to register a CAGR of around 1.6% during 2026-32.

- Product Shares

- Melatonin grabbed market share of 45%.

- Competition

- More than 5 companies are actively engaged in producing sleep aids in UAE.

- Top 5 companies acquired around 50% of the market share.

- Natrol LLC, Ginsana Products Lugano SA, Sensilab SA, GSK Consumer Healthcare, Julphar Gulf Pharmaceuticals etc., are few of the top companies.

- Sales channel

- Retail offline grabbed 85% of the market.

UAE Sleep Aids Market Outlook

The UAE Sleep Aids Market size is estimated to be USD 3.07 million in 2025 and is expected to increase to USD 3.43 million in 2032 with a CAGR of 1.63% over the forecast period. This gradual increase is backed by the growing population and the growing sleep problems among younger groups of people who experience academic and career stress. As the growth persists, the rate has slowed down with more residents embracing holistic wellness practices, including mindfulness and better sleep hygiene, to minimize long-term reliance on medicinal remedies.

The market is moving towards natural and herbal products, but melatonin is still a giant with a market share of 45%. The most popular brands like Panadol Night have a dynamic presence as they provide dual-purpose formula that treats pain and restlessness. With the increasing global awareness of the side effects of synthetic ingredients, end user are increasingly turning to botanical sleep aids that include chamomile or valerian root, which are seen as softer, more environmentally friendly options.

Distribution is very much concentrated in the physical locations and the retail offline channels are currently controlling 85% of the market. This area is dominated by pharmacies due to a local culture that places importance on face-to-face consultation with pharmacists to seek health advice and product recommendations. Although digital platforms continue to grow, the knowledge base of a brick-and-mortar pharmacy is still the main entry point to individuals who buy sleep aids first or require individual advice.

In the future, the digital technology and wellness trends will be integrated, which will provide the industry with new opportunities. Sleep-tracking applications and wearables promote an active attitude towards health, which tends to prescribe certain supplements to maximise sleep patterns. With the emphasis on stress relief and the connection between sleep and appearance, the manufacturers will be able to sell their sleep aids to the beauty-conscious population that pays attention to the overall health and longevity.

UAE Sleep Aids Market Growth Driver

Population Growth Keeps the Category Broad-Based

The growing resident population supports a consistent and growing need of sleep aids, with more end user struggling with hectic schedules, disrupted daily routines, and chronic daily stress, all of which negatively affect sleep quality and consistency. This population increase keeps expanding the base of first-time buyers and maintaining repeat purchases, especially of those products that are sold as easy-to-use support systems and not as heavy or addictive drugs.

The UAE has a total population of 11.4 million people in 2025, according to the United Nations Population Fund (UNFPA), which significantly increases the number of end user to whom the retail sleep solutions are sold across the vast network of pharmacies and supermarkets in the country. This continued population growth ensures that the category has a wide and diversifying consumer base that supports long-term volume growth up to 2032.

UAE Sleep Aids Market Challenge

Lifestyle-Led Sleep Management Reduces Product Reliance

The structural moderating force of category growth is that more end user are actively trying to enhance sleep by adopting sustainable behavioural patterns, including better sleep hygiene, mindfulness, less screen time, and more routine daily routines, before they turn to over-the-counter sleep aids. The increasing awareness of the issue of long-term dependency also makes a part of the shoppers more selective and more intermittent in their product consumption habits.

According to the Dubai Media Office, the Dubai Fitness Challenge 2025 has seen more than 3 million people participate, which is a strong and strengthening wellness culture that actively supports non-product strategies like organized exercise and community wellness programs. These lifestyle options can be successfully used to replace sleep aids in mild and moderate situations, thus moderating overall volume growth despite the fact that the underlying consumer base of the category is growing.

Unlock Market Intelligence

Explore the market potential with our data-driven report

UAE Sleep Aids Market Trend

Pharmacies Stay Central While Digital Buying Becomes Routine

Pharmacies are the main channel of sale of sleep aids because end user still appreciate pharmacist advice, easy-to-understand dosage, and brand loyalty, especially when trying a product first. At the same time, pharmacy-related e-commerce platforms and super-app ordering are under steady growth as end user are moving towards online comparison and reordering with more convenience, solidifying an omnichannel buying channel throughout the UAE market.

According to the Emirates News Agency, 67% of UAE end user used their phones during their latest retail purchase as of July 2025, highlighting the growing importance of mobile-led shopping in facilitating online discovery and repeat purchases across health categories, including sleep aids. This mobile-first buying behaviour is expected to intensify further as the digital retail infrastructure keeps evolving until 2032.

UAE Sleep Aids Market Opportunity

Digital Sleep Tracking Creates a New Conversion Funnel

Sleep trackers and wellness apps encourage a more active attitude towards sleep health by transforming the quality of sleep into quantifiable and continuously trackable personal information. end user who recognize poor sleep metrics using these tools are significantly more likely to initially explore lifestyle changes and then think about sleep-support supplements as a component of a more deliberate, comprehensive nighttime wellness habit.

The International Telecommunication Union estimates that 6 billion individuals are using the internet in 2025 and 5G subscriptions have reached about 3 billion with coverage reaching 55% of the global population. This powerful connectivity foundation reinforces app-based product suggestions and wearable-based wellness behaviours, thus establishing an expanding and highly focused digital conversion funnel of sleep aid brands aiming to tap health-conscious and data-conscious UAE end user through 2032.

Unlock Market Intelligence

Explore the market potential with our data-driven report

UAE Sleep Aids Market Segmentation Analysis

By Product

- Single Ingredient

- Doxylamine Succinate

- Diphenhydramine

- Melatonin

- Combination Ingredient

- Diphenhydramine + Acetaminophen

- Other Antihistamine-Based Combinations

- Herbal & Traditional Sleep Aids

- Valerian root

- Passionflower

- Chamomile

- Kava

- Multi-Herbal Sleep Blends

The largest market share in the ingredient-based product mix is melatonin, which has approximately 45% of the total market. This leadership indicates that melatonin has a high and well-established correlation with sleep-cycle regulation and that it is a natural fit with end user who are looking to find a familiar and easy-to-use solution that is significantly lighter and less addictive than prescription sedative options that are offered through clinical channels.

The 45% market share of Melatonin maintains competitive attention on branding quality, dosage clarity, and dual positioning around sleep and stress relief instead of ingredient novelty or reformulation. This market share also facilitates commercially viable line-extension opportunities, where brands launching gentler botanical substitutes aim to deliver similar consumer advantages but expand category reach and maintain melatonin-led shelf leadership through 2032.

By Sales Channel

- Retail Online

- Retail Offline

The Retail Offline segment has the largest market share in the sales channel, which is about 85% of the total market. The pharmacies prevail in this environment since first-time buyers always need to be reassured and professionally guided, and sleep health is a valuable well-being issue where expert in-store advice is a decisive factor in establishing initial purchase confidence and brand loyalty.

This offline leadership supports the strategic imperative of high shelf presence, aggressive pharmacist prescribing, and effective in-store promotional activity as a critical strategic requirement of brands competing in the UAE sleep aids market. Although online purchasing is increasing via pharmacy-linked platforms and supermarket applications, offline retail will be the main conversion point of the first trial and the basis of long-term trust-building with the consumer base until 2032.

List of Companies Covered in UAE Sleep Aids Market

The companies listed below are highly influential in the UAE sleep aids market, with a significant market share and a strong impact on industry developments.

- Natrol LLC

- Ginsana Products Lugano SA

- Sensilab SA

- GSK Consumer Healthcare

- Julphar Gulf Pharmaceuticals

Competitive Landscape

UAE sleep aids market continues to record healthy retail value and volume growth in 2025, supported by population expansion and rising awareness of sleep health. However, growth is moderating as many consumers increasingly adopt holistic approaches such as mindfulness, improved sleep hygiene, reduced screen time and meditation instead of relying solely on sleep medications. Concerns regarding the long-term use of melatonin have also encouraged interest in gentler, natural alternatives. Within the competitive landscape, Panadol Night by GSK Consumer Healthcare remains the leading and most dynamic brand, followed by Adol PM from Julphar Gulf Pharmaceuticals and Natrol Melatonin by Natrol LLC, supported by strong pharmacy distribution and expanding e-commerce availability.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- UAE Sleep Aids Market Policies, Regulations, and Standards

- UAE Sleep Aids Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- UAE Sleep Aids Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product

- Single Ingredient- Market Insights and Forecast 2022-2032, USD Million

- Doxylamine Succinate- Market Insights and Forecast 2022-2032, USD Million

- Diphenhydramine- Market Insights and Forecast 2022-2032, USD Million

- Melatonin- Market Insights and Forecast 2022-2032, USD Million

- Combination Ingredient- Market Insights and Forecast 2022-2032, USD Million

- Diphenhydramine + Acetaminophen- Market Insights and Forecast 2022-2032, USD Million

- Other Antihistamine-Based Combinations- Market Insights and Forecast 2022-2032, USD Million

- Herbal & Traditional Sleep Aids- Market Insights and Forecast 2022-2032, USD Million

- Valerian root- Market Insights and Forecast 2022-2032, USD Million

- Passionflower- Market Insights and Forecast 2022-2032, USD Million

- Chamomile- Market Insights and Forecast 2022-2032, USD Million

- Kava- Market Insights and Forecast 2022-2032, USD Million

- Multi-Herbal Sleep Blends- Market Insights and Forecast 2022-2032, USD Million

- Single Ingredient- Market Insights and Forecast 2022-2032, USD Million

- By Sleep Disorder

- Insomnia- Market Insights and Forecast 2022-2032, USD Million

- Sleep Apnea- Market Insights and Forecast 2022-2032, USD Million

- Restless Legs Syndrome- Market Insights and Forecast 2022-2032, USD Million

- Narcolepsy- Market Insights and Forecast 2022-2032, USD Million

- Sleep Walking- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Age Group

- Young to Mid Adults (25-44 Years)- Market Insights and Forecast 2022-2032, USD Million

- Middle-Aged Adults (45-64 Years)- Market Insights and Forecast 2022-2032, USD Million

- Geriatric Population (65+ Years)- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- By End User

- Homecare/Individual Consumers- Market Insights and Forecast 2022-2032, USD Million

- Hospitals- Market Insights and Forecast 2022-2032, USD Million

- Sleep Centers & Clinics- Market Insights and Forecast 2022-2032, USD Million

- By Formulation

- Tablets- Market Insights and Forecast 2022-2032, USD Million

- Gummies- Market Insights and Forecast 2022-2032, USD Million

- Capsules- Market Insights and Forecast 2022-2032, USD Million

- Liquid- Market Insights and Forecast 2022-2032, USD Million

- Sublingual- Market Insights and Forecast 2022-2032, USD Million

- By Region

- Dubai

- Abu Dhabi

- Sharjah

- Northern Emirates

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Product

- Market Size & Growth Outlook

- UAE Single Ingredient Sleep Aids Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Sleep Disorder- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Formulation- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- UAE Combination Ingredient Sleep Aids Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Sleep Disorder- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Formulation- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- UAE Herbal & Traditional Sleep Aids Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Sleep Disorder- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Formulation- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- GSK Consumer Healthcare

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Julphar Gulf Pharmaceuticals

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Natrol LLC

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Ginsana Products Lugano SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Sensilab SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- GlaxoSmithKline Plc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Others

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- GSK Consumer Healthcare

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product |

|

| By Sleep Disorder |

|

| By Age Group |

|

| By Sales Channel |

|

| By End User |

|

| By Formulation |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.