UAE Facial Cleanser Market Report: Trends, Growth and Forecast (2026-2032)

By Product Type (Gel Cleanser, Foam Cleanser, Cream Cleanser, Liquid Cleanser, Oil Cleanser, Balm Cleanser, Micellar Cleanser, Powder/Bar Cleanser), By Skin Type (Oily & Acne-Prone Skin, Dry Skin, Sensitive Skin, Combination Skin, Normal Skin), By Ingredient (Conventional, Natural/Organic, Sulfate-Free, Fragrance-Free, Medicated/Active-Based), By Consumer Group (Women, Men, Unisex, Teen), By Distribution Channel (Retail Offline (Supermarkets/Hypermarkets, Pharmacies/Drug Stores, Specialty Beauty Stores, Department Stores), Retail Online (E-commerce Platforms, Brand-Owned Websites (D2C), Online Beauty Retailers)), By Price Point (Mass, Premium, Luxury), By Regions (Dubai, Abu Dhabi, Sharjah, Northern Emirates) ... Read more

|

Major Players

|

UAE Facial Cleanser Market Statistics and Insights, 2026

- Market Size Statistics

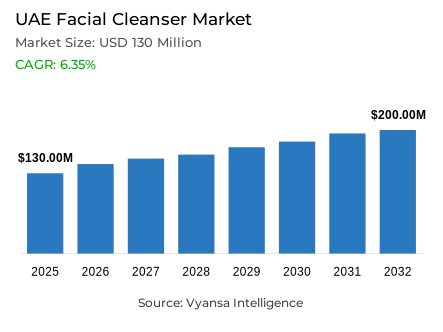

- Facial cleanser market size in UAE was valued at USD 130 million in 2025 and is estimated at USD 140 million in 2026.

- The market size is expected to grow to USD 200 million by 2032.

- Market to register a CAGR of around 6.35% during 2026-32.

- Product Type Shares

- Gel cleanser grabbed market share of 20%.

- Competition

- More than 10 companies are actively engaged in producing facial cleanser in UAE.

- Top 5 companies acquired around 60% of the market share.

- Procter & Gamble, NAOS, The Estee Lauder Companies, Beiersdorf AG, Unilever PLC etc., are few of the top companies.

- Skin Type

- Oily & acne-prone skin grabbed 30% of the market.

UAE Facial Cleanser Market Outlook

The UAE facial cleanser market size was valued at USD 130 million in 2025 and is projected to grow from USD 140 million in 2026 to USD 200 million by 2032, exhibiting a CAGR of 6.35% during the forecast period. According to data published by the National Center of Meteorology, Dubai records maximum temperatures of 43° Celsius and humidity levels reaching 90% in July 2025, while Abu Dhabi experiences even higher temperatures at 46° Celsius with 70% humidity during the same period. These extreme climatic conditions accelerate sebum production and moisture loss in consumers, making frequent facial cleansing essential for maintaining skin health rather than optional. Sweat and oil accumulate rapidly on skin surfaces throughout daily routines, driving repeated cleanser usage and supporting consistent product demand across all demographic segments within the region.

Population concentration in urban centers establishes strong structural foundations for the face wash market category. According to statistics released by the World Bank, the UAE population reached 10,986,400 in 2024 with 86% residing in urban areas. High-density consumer clustering in major cities generates concentrated retail foot traffic, supports robust e-commerce penetration, and enables efficient supply chain distribution that benefits established brands. This urban concentration creates market conditions where facial cleanser products achieve higher purchase frequency and faster inventory turnover compared to less densely populated regions, allowing manufacturers to optimize production schedules and distributors to minimize holding periods.

Digital connectivity has reshaped product discovery and purchasing behavior in ways that fundamentally restructure market dynamics. Validated reports indicate that 100% of the UAE population utilizes internet services, creating comprehensive digital exposure to product information and consumer reviews across social media platforms and online retailers. Safety-conscious buying behavior has intensified through official verification infrastructure that enables consumers to authenticate product credentials before purchase. According to data from Dubai Municipality, the Muntaji system now registers over 500,000 beauty products and allows consumers to verify product specifications, origin, and health safety compliance in real time. This transparency mechanism shifts purchasing decisions from brand heritage alone toward verifiable safety credentials and ingredient clarity, rewarding manufacturers capable of demonstrating regulatory compliance and clinical substantiation.

Market segmentation patterns reveal strong consumer preference for targeted formulations addressing specific skin concerns rather than generic solutions. Gel-based cleansers establish category leadership at 20% share due to their alignment with regional climate demands and consumer preferences for lightweight, fast-absorbing textures that feel fresh in hot, humid environments. Meanwhile, products formulated for anti-acne facial cleanser solutions account for 30% of demand, indicating that consumers increasingly select solutions addressing visible skin concerns. These segmentation trends signal market maturation toward performance-driven purchasing where efficacy claims and dermatological positioning drive differentiation. Manufacturers must align formulation strategies, marketing messaging, and distribution focus with these demonstrated preferences to capture emerging market opportunities and strengthen competitive positioning throughout the forecast period.

UAE Facial Cleanser Market Growth Driver

Climate Exposure Keeps Daily Use Strong

Extreme environmental conditions establish physiological drivers that maintain consistent cleanser demand independent of economic cycles. The National Center of Meteorology documents that Dubai and Abu Dhabi experience sustained temperatures exceeding 43° Celsius combined with humidity levels reaching 90%, conditions that trigger accelerated skin oil secretion and faster accumulation of sweat and surface impurities on facial skin. Consumers across the UAE must cleanse faces more frequently than populations in temperate climates to maintain skin health and prevent pore congestion. These environmental imperatives create structural market demand that persists throughout economic downturns and seasonal variations, establishing facial cleansers as essential rather than discretionary products within consumer budgets.

Population density amplifies the scale of cleanser consumption across urban markets. The World Bank reports that the UAE population reached 10.99 million residents in 2024 with 86% concentrated in urban centers where retail density remains exceptionally high and consumer product accessibility is maximized. This concentrated population base supports stronger routine product turnover, enables manufacturers to achieve economies of scale through high-volume production runs, and allows distributors to service retail networks efficiently. Urban concentration also facilitates direct-to-consumer digital commerce through e-commerce facial cleanser channels, permitting brands to reach customers through online platforms that bypass traditional retail gatekeepers and create opportunities for smaller manufacturers to establish market presence through social media engagement and influencer partnerships.

UAE Facial Cleanser Market Challenge

Compliance Pressure Keeps Entry Tight

Facial cleanser brands must navigate complex regulatory systems before scaling operations throughout the UAE market. According to Dubai Municipality data, approximately 560,000 imported products are processed annually through Dubai's ports, while over 500,000 beauty products remain registered in the Muntaji system for consumer verification. Beauty products imported into the UAE are tested using advanced techniques aligned with ISO/IEC 17025 international standards, creating substantial compliance workloads around ingredient documentation, safety testing, and batch consistency verification. Product registration delays and testing cycles impose capital requirements that disadvantage smaller manufacturers lacking dedicated regulatory affairs resources. Companies must invest in laboratory testing, clinical substantiation documentation, and regulatory consultancy services to secure market access, raising barriers to entry for emerging brands and concentrating market share among larger, better-resourced competitors.

Market saturation within regulatory registration systems creates competitive pressure and timing challenges for product launches. Dubai Municipality reports that nearly 40,000 shipments containing over 560,000 imported products are processed annually, while approximately 10,000 institutions trade consumer products throughout Dubai alone. This registration volume indicates highly crowded market conditions where new entrants face extended approval timelines and must differentiate offerings more effectively than in less regulated environments. Product launches experience timing uncertainty as regulatory bodies conduct safety testing and documentation verification, forcing manufacturers to maintain larger inventory buffers and accept extended time-to-market windows. Competitive pressure intensifies as established brands leverage regulatory infrastructure familiarity and approved ingredient portfolios to respond rapidly to emerging consumer trends while new entrants struggle with approval processes and market access delays.

Unlock Market Intelligence

Explore the market potential with our data-driven report

UAE Facial Cleanser Market Trend

Transparency-Led Buying Gains Ground

Consumer purchasing behavior increasingly reflects safety consciousness enabled by digital verification tools that authenticate product credentials. Individuals using the Internet account for 100% of the UAE population in 2024, according to World Bank data, creating universal exposure to digital product discovery platforms and online safety verification systems. The Muntaji application provides consumers with real-time access to registered product information, health safety specifications, testing compliance details, and origin documentation, fundamentally reshaping purchase decision mechanisms away from brand recognition alone and toward verifiable product credentials. Consumers now compare skin cleansing products by examining official safety certifications and ingredient transparency rather than relying solely on advertising messages or retail recommendations. This shift toward verification-led buying behavior favors brands that can demonstrate transparent ingredient sourcing, clinical testing substantiation, and regulatory compliance through easily accessible digital channels.

Digital transparency mechanisms are pushing the facial cleanser category toward safer formulations and more honest product positioning. According to Dubai Municipality, beauty products are tested in line with ISO/IEC 17025 standards while over 500,000 products are registered and verifiable through the Muntaji system. This formal verification infrastructure eliminates information asymmetries that previously allowed brands to make unsubstantiated claims, instead requiring manufacturers to align marketing messages with actual tested product performance and certified specifications. Younger demographics and digitally native consumers increasingly demand transparent ingredient lists, clinical testing evidence, and third-party certifications before committing to purchases. This transparency trend creates competitive advantages for brands willing to invest in clinical research, independent testing, and detailed product documentation while disadvantaging companies relying on traditional marketing approaches or ingredient formulations that cannot withstand scientific scrutiny.

UAE Facial Cleanser Market Opportunity

Premium and Regional Scale-Up Create the Strongest White Space

Strong opportunities are emerging for premium vs mass market facial cleanser brands to expand from the UAE into neighboring GCC markets where demand for higher-value skincare products continues to accelerate. According to World Integrated Trade Solution (WITS) data, Saudi Arabia imported USD 133.37 million of skin cleansing products from the UAE in 2024, establishing the strongest demand corridor in the region. Oman imported USD 48.94 million, Kuwait purchased USD 24.76 million, and Qatar acquired USD 11.68 million of UAE skincare exports during the same period. These cross-border trade flows demonstrate that UAE based brands have already established viable routes to place cleansing product lines across regional markets. Manufacturers operating in the UAE can leverage supply chain infrastructure, regulatory compliance expertise, and market knowledge developed domestically to penetrate larger neighboring markets without requiring extensive recapitalization or market development investments.

Domestic purchasing power and demographic composition support expansion of premium personal care cleansing product lines addressing specific skin concerns. The World Bank reports that UAE GDP per capita reached USD 50,273.50 in 2024, establishing the region as one of the highest income markets in the Middle East with pronounced consumer willingness to purchase premium skincare solutions. The domestic population base of 10.99 million residents combined with high purchasing power creates room for facial cleanser brands to develop acne care lines, sensitive skin formulations, and ingredient-led product ranges serving both local demand and cross-border expansion. Premium positioning strategies addressing dermatological concerns generate higher profit margins than mass market offerings, enabling manufacturers to invest in clinical research, product innovation, and sophisticated digital marketing campaigns. These favorable domestic conditions permit UAE brands to incubate premium product portfolios and validate marketing strategies before scaling into regional markets where similar consumer demographics and purchasing power prevail.

Unlock Market Intelligence

Explore the market potential with our data-driven report

UAE Facial Cleanser Market Segmentation Analysis

By Product Type

- Gel Cleanser

- Foam Cleanser

- Cream Cleanser

- Liquid Cleanser

- Oil Cleanser

- Balm Cleanser

- Micellar Cleanser

- Powder/Bar Cleanser

Gel based facial cleansers command market leadership at 20% share, establishing clear product type dominance across the UAE facial cleanser landscape. This segment maintains its position as the leading product category due to strong fit with regional climatic requirements and demonstrated consumer preferences for lightweight, fast absorbing formulations that provide fresh sensations in hot, humid environments. Gel cleansers deliver superior rinse profiles compared to cream or lotion formats, requiring minimal water volume and leaving no residual film on skin surfaces, attributes that resonate strongly with time pressed professionals navigating high temperature conditions throughout daily routines. Consumer preference for gel formats reflects both functional alignment and sensory perception, as these formulations feel cool and refreshing immediately after application, creating positive user experiences that support repeat purchases and strong brand loyalty.

This leadership position reflects consumer selection of product types that integrate easily into simplified skincare routines without requiring special application techniques or extended rinse procedures. Gel cleanser formats support repeated daily application, suiting the elevated cleansing frequency that extreme UAE climates necessitate, while remaining lightweight enough to avoid irritating already stressed facial skin. The 20% market share indicates that this segment continues shaping category assortments, retail shelf presence, and inventory forecasting decisions among retailers and distributors throughout the region. As the category expands into secondary markets and consumer demographics shift toward younger, digitally native populations prioritizing efficiency and simplicity, gel format leadership is expected to intensify. Manufacturers focused on gel technology platforms are positioned advantageously to capture growth in this expanding category through product line extensions and distribution network expansion.

By Skin Type

- Oily & Acne-Prone Skin

- Dry Skin

- Sensitive Skin

- Combination Skin

- Normal Skin

The oily and acne-prone skin segment demonstrates commanding market position at 30% share, establishing clear categorical leadership within the facial cleanser market's skin type segmentation framework. This dominance reflects demographic composition patterns where younger populations predominate within UAE urban centers and this age cohort experiences heightened sebaceous gland activity, accelerated acne susceptibility, and increased demand for targeted cleansing solutions addressing visible skin concerns. Consumers in this demographic segment actively seek anti-acne facial cleanser formulations specifically designed to manage excess sebum production, maintain pore clarity, and support ongoing skin health through daily cleansing routines. Evidence from market analysis indicates that consumers selecting products addressing oily and acne-prone conditions exhibit higher engagement levels, greater willingness to try new brands, and increased brand loyalty when products deliver visible results relative to generic cleanser consumers.

Product development is being reshaped by performance-driven requirements as manufacturers introduce ingredient sophistication to substantiate efficacy claims and support differentiation within increasingly crowded retail environments. Brands formulating for this skin type segment are incorporating specialized actives such as salicylic acid derivatives, kaolin clay minerals, and enzymatic exfoliants designed to address sebum management and pore blockage through targeted chemical and physical mechanisms. The 30% market share indicates that this segment continues influencing formulation focus, competitive positioning, and purchasing priorities throughout the facial cleanser category. As direct-to-consumer brands and skincare specialists establish market presence through digital channels and e-commerce platforms, consumers seeking clinical substantiation and transparent ingredient disclosures will find increasing product choices tailored to their specific skin needs. Manufacturers competing within this segment must balance efficacy positioning with safety compliance while maintaining regulatory documentation standards required for sustained market access and consumer trust.

List of Companies Covered in UAE Facial Cleanser Market

The companies listed below are highly influential in the UAE facial cleanser market, with a significant market share and a strong impact on industry developments.

- Procter & Gamble

- NAOS

- The Estee Lauder Companies

- Beiersdorf AG

- Unilever PLC

- L’Oreal S.A.

- Galderma

- Kenvue

- Pierre Fabre

- Shiseido Company Limited

Market News & Updates

- Galderma, 2025:

In August 2025, Galderma launched Cetaphil Nourishing Oil to Foam Cleanser. The company presented it as a first-of-its-kind formula. It targets normal-to-dry sensitive skin globally. The cleanser transforms from oil to foam on contact. Galderma says it removes makeup, oil, and dirt effectively. It also supports hydration and the skin moisture barrier. The formula includes PENTAVITIN, flaxseed oil, niacinamide, and panthenol. The launch matters for the global facial cleanser market. It strengthens demand for hydrating, barrier-supporting, dermatologist-led cleansing products. It also supports premiumization within sensitive-skin facial care worldwide.

- Unilever PLC, 2025:

In April 2025, Unilever launched Dove Regenerative, its first facial skincare range. The company described it as Dove’s entry into facial dermocosmetics. The range combines cosmetic appeal with advanced skincare science. Unilever said the line uses B3PRO technology across products. That combines niacinamide with Dove’s Pro-Retinol formula. The company positioned the range around simpler routines and stronger efficacy. This development matters for the global facial cleanser market. It shows major FMCG players are expanding into science-led facial care. It also raises competition in affordable dermocosmetic cleansing and skincare segments. The move should support wider consumer access to performance-focused facial cleansing solutions.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- UAE Facial Cleanser Market Policies, Regulations, and Standards

- UAE Facial Cleanser Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- UAE Facial Cleanser Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product Type

- Gel Cleanser- Market Insights and Forecast 2022-2032, USD Million

- Foam Cleanser- Market Insights and Forecast 2022-2032, USD Million

- Cream Cleanser- Market Insights and Forecast 2022-2032, USD Million

- Liquid Cleanser- Market Insights and Forecast 2022-2032, USD Million

- Oil Cleanser- Market Insights and Forecast 2022-2032, USD Million

- Balm Cleanser- Market Insights and Forecast 2022-2032, USD Million

- Micellar Cleanser- Market Insights and Forecast 2022-2032, USD Million

- Powder/Bar Cleanser- Market Insights and Forecast 2022-2032, USD Million

- By Skin Type

- Oily & Acne-Prone Skin- Market Insights and Forecast 2022-2032, USD Million

- Dry Skin- Market Insights and Forecast 2022-2032, USD Million

- Sensitive Skin- Market Insights and Forecast 2022-2032, USD Million

- Combination Skin- Market Insights and Forecast 2022-2032, USD Million

- Normal Skin- Market Insights and Forecast 2022-2032, USD Million

- By Ingredient

- Conventional- Market Insights and Forecast 2022-2032, USD Million

- Natural/Organic- Market Insights and Forecast 2022-2032, USD Million

- Sulfate-Free- Market Insights and Forecast 2022-2032, USD Million

- Fragrance-Free- Market Insights and Forecast 2022-2032, USD Million

- Medicated/Active-Based- Market Insights and Forecast 2022-2032, USD Million

- By Consumer Group

- Women- Market Insights and Forecast 2022-2032, USD Million

- Men- Market Insights and Forecast 2022-2032, USD Million

- Unisex- Market Insights and Forecast 2022-2032, USD Million

- Teen- Market Insights and Forecast 2022-2032, USD Million

- By Distribution Channel

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- Supermarkets/Hypermarkets- Market Insights and Forecast 2022-2032, USD Million

- Pharmacies/Drug Stores- Market Insights and Forecast 2022-2032, USD Million

- Specialty Beauty Stores- Market Insights and Forecast 2022-2032, USD Million

- Department Stores- Market Insights and Forecast 2022-2032, USD Million

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- E-commerce Platforms- Market Insights and Forecast 2022-2032, USD Million

- Brand-Owned Websites (D2C)- Market Insights and Forecast 2022-2032, USD Million

- Online Beauty Retailers- Market Insights and Forecast 2022-2032, USD Million

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- By Price Point

- Mass- Market Insights and Forecast 2022-2032, USD Million

- Premium- Market Insights and Forecast 2022-2032, USD Million

- Luxury- Market Insights and Forecast 2022-2032, USD Million

- By Regions

- Dubai- Market Insights and Forecast 2022-2032, USD Million

- Abu Dhabi- Market Insights and Forecast 2022-2032, USD Million

- Sharjah- Market Insights and Forecast 2022-2032, USD Million

- Northern Emirates- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Product Type

- Market Size & Growth Outlook

- UAE Gel Cleanser Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Skin Type- Market Insights and Forecast 2022-2032, USD Million

- By Ingredient- Market Insights and Forecast 2022-2032, USD Million

- By Consumer Group- Market Insights and Forecast 2022-2032, USD Million

- By Distribution Channel- Market Insights and Forecast 2022-2032, USD Million

- By Price Point- Market Insights and Forecast 2022-2032, USD Million

- By Regions- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- UAE Foam Cleanser Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Skin Type- Market Insights and Forecast 2022-2032, USD Million

- By Ingredient- Market Insights and Forecast 2022-2032, USD Million

- By Consumer Group- Market Insights and Forecast 2022-2032, USD Million

- By Distribution Channel- Market Insights and Forecast 2022-2032, USD Million

- By Price Point- Market Insights and Forecast 2022-2032, USD Million

- By Regions- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- UAE Cream Cleanser Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Skin Type- Market Insights and Forecast 2022-2032, USD Million

- By Ingredient- Market Insights and Forecast 2022-2032, USD Million

- By Consumer Group- Market Insights and Forecast 2022-2032, USD Million

- By Distribution Channel- Market Insights and Forecast 2022-2032, USD Million

- By Price Point- Market Insights and Forecast 2022-2032, USD Million

- By Regions- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- UAE Liquid Cleanser Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Skin Type- Market Insights and Forecast 2022-2032, USD Million

- By Ingredient- Market Insights and Forecast 2022-2032, USD Million

- By Consumer Group- Market Insights and Forecast 2022-2032, USD Million

- By Distribution Channel- Market Insights and Forecast 2022-2032, USD Million

- By Price Point- Market Insights and Forecast 2022-2032, USD Million

- By Regions- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- UAE Oil Cleanser Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Skin Type- Market Insights and Forecast 2022-2032, USD Million

- By Ingredient- Market Insights and Forecast 2022-2032, USD Million

- By Consumer Group- Market Insights and Forecast 2022-2032, USD Million

- By Distribution Channel- Market Insights and Forecast 2022-2032, USD Million

- By Price Point- Market Insights and Forecast 2022-2032, USD Million

- By Regions- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- UAE Balm Cleanser Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Skin Type- Market Insights and Forecast 2022-2032, USD Million

- By Ingredient- Market Insights and Forecast 2022-2032, USD Million

- By Consumer Group- Market Insights and Forecast 2022-2032, USD Million

- By Distribution Channel- Market Insights and Forecast 2022-2032, USD Million

- By Price Point- Market Insights and Forecast 2022-2032, USD Million

- By Regions- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- UAE Micellar Cleanser Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Skin Type- Market Insights and Forecast 2022-2032, USD Million

- By Ingredient- Market Insights and Forecast 2022-2032, USD Million

- By Consumer Group- Market Insights and Forecast 2022-2032, USD Million

- By Distribution Channel- Market Insights and Forecast 2022-2032, USD Million

- By Price Point- Market Insights and Forecast 2022-2032, USD Million

- By Regions- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- UAE Powder/Bar Cleanser Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Skin Type- Market Insights and Forecast 2022-2032, USD Million

- By Ingredient- Market Insights and Forecast 2022-2032, USD Million

- By Consumer Group- Market Insights and Forecast 2022-2032, USD Million

- By Distribution Channel- Market Insights and Forecast 2022-2032, USD Million

- By Price Point- Market Insights and Forecast 2022-2032, USD Million

- By Regions- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Beiersdorf AG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Unilever PLC

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- L’Oreal S.A.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Galderma

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Kenvue

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Procter & Gamble

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- NAOS

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- The Estee Lauder Companies

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Pierre Fabre

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Shiseido Company Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Beiersdorf AG

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Skin Type |

|

| By Ingredient |

|

| By Consumer Group |

|

| By Distribution Channel |

|

| By Price Point |

|

| By Regions |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.