Thailand Paediatric Consumer Health Market Report: Trends, Growth and Forecast (2026-2032)

By Product Type (Paediatric Analgesics (Paediatric Acetaminophen, Paediatric Aspirin, Paediatric Combination Products Analgesics, Paediatric Dipyrone, Paediatric Ibuprofen, Paediatric Naproxen), Paediatric Cough, Cold and Allergy Remedies (Paediatric Allergy Remedies, Paediatric Cough/Cold Remedies), Paediatric Digestive Remedies (Paediatric Diarrhoeal Remedies, Paediatric Indigestion and Heartburn Remedies, Paediatric Laxatives, Paediatric Motion Sickness Remedies), Paediatric Dermatologicals, Nappy (Diaper) Rash Treatments, Paediatric Vitamins and Dietary Supplements), By Dosage Form (Liquid Syrups, Chewable Tablets, Drops, Powders/Sachets, Gummies, Topical Creams & Ointments), By Age Group (Infants & Toddlers (0-3 Years), Children (4-12 Years), Adolescents (13-18 Years)), By Treatment Type (Acute Treatment, Chronic Condition Management, Genetic & Rare Disease Management), By Sales Channel (Retail Online (Online Pharmacies, E-commerce Platforms, Brand Websites), Retail Offline (Hospital Pharmacies, Retail Pharmacies / Drugstores, Supermarkets & Hypermarkets, Specialty Baby Stores)) ... Read more

|

Major Players

|

Thailand Paediatric Consumer Health Market Statistics and Insights, 2026

- Market Size Statistics

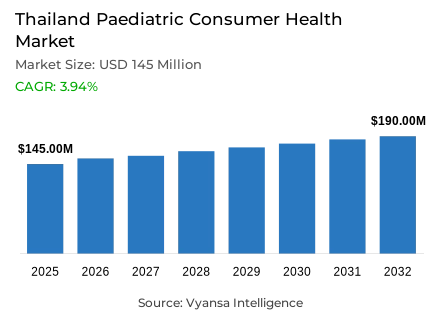

- Paediatric consumer health market size in Thailand was valued at USD 145 million in 2025 and is estimated at USD 157.13 Million in 2026.

- The market size is expected to grow to USD 190 million by 2032.

- Market to register a CAGR of around 3.94% during 2026-32.

- Product Type Shares

- Paediatric vitamins and dietary supplements grabbed market share of 55%.

- Competition

- More than 20 companies are actively engaged in producing paediatric consumer health in Thailand.

- Top 5 companies acquired around 50% of the market share.

- Johnson & Johnson (Thailand) Ltd, Mega Lifesciences Pty Ltd, British Dispensary (LP) Co Ltd, GSK Consumer Healthcare, Seven Seas Health Care Ltd etc., are few of the top companies.

- Sales Channel

- Retail offline grabbed 75% of the market.

Thailand Paediatric Consumer Health Market Outlook

The Thailand paediatric consumer Health market size was valued at USD 145 million in 2025 and is projected to grow from USD 157.13 Million in 2026 to USD 190 million by 2032, exhibiting a CAGR of 3.94% during the forecast period. This upward momentum is driven by a shift toward preventative care as children return to normal social activities and school environments. While a falling birth rate presents a demographic challenge, it is being offset by more informed parents who are willing to invest heavily in premium health solutions for their fewer offspring.

Preventative wellness is a core priority for modern Thai families, particularly as paediatric vitamins and dietary supplements grabbed market share of 55%. Parents are increasingly seeking specialized ingredients like elderberry, probiotics, and DHA to support immunity and brain development. This strong interest in paediatric consumer Health has encouraged brands to innovate with appetising formats such as jelly sticks and oral sprays, making it easier for caregivers to maintain their children's daily health routines.

Despite the rapid rise of digital platforms, physical pharmacies remain the primary choice for many, as retail offline grabbed 75% of the market. Trusted experts and immediate availability keep these stores at the center of the paediatric consumer Health landscape. However, social media and e-commerce are gaining ground by providing detailed product reviews and a wider variety of imported goods, helping parents research specific claims such as sleep aids or eye health supplements before making a purchase.

Looking ahead, the market will likely see a blurring of lines between nutrition and medicine as parents adopt a holistic approach through fortified foods and organic remedies. Innovations in child-specific herbal treatments and "clean label" products will continue to attract those cautious about chemical-based options. By focusing on niche health concerns and high-quality formulations, the paediatric consumer Health sector is well-positioned to maintain steady value growth as urbanization and hectic lifestyles drive the demand for convenient, effective wellness products.

Thailand Paediatric Consumer Health Market Growth DriverEveryday Illness Exposure and Environmental Health Pressures Sustain Consistent Home Care Demand

The resumption of structured childhood routines emerges as the key and long-term driver of paediatric consumer Health demand within the Thai market. As the proportion of time that children spend within the school environment, the outdoors, and structured group activities increases, parents are more vigilant with regards to coughs, colds, fever, injuries, and allergy-based discomforts. This drives the trend towards an increasingly large proportion of households keeping child-based health products as part of the routine inventory within the home setting, which can be used at the earliest onset of symptoms as the means of addressing the full range of manageable illnesses.

Environmental air quality conditions provide the second key driver of the end user health demand trend within the Thai market setting. As indicated by UNICEF Thailand, there are approximately 13.6 million children within the country setting that are highly exposed to fine particulate matter at PM2.5 concentration levels, which significantly increases the level of health risks faced by young children within the country setting. As such, within the context of the environmental setting, parents are highly vigilant with regards to products that provide the means of addressing symptoms, reinforcing the immune system, and addressing the full range of child wellness considerations in a consistent manner.

Thailand Paediatric Consumer Health Market ChallengeA Contracting Child Population Imposes Structural Constraints on Volume-Led Growth

A declining birth rate signifies the most clearly defined structural challenge facing Thailand's paediatric consumer Health market. While the category benefits from heightened health awareness and willingness to spend on health by parents, the category continues to experience a progressively declining target end user base. This serves as a constraint to broader category growth and increasingly pressures brand operators to drive category growth through rising per child expenditure as opposed to rising numbers of end users.

Thailand's National Statistical Office indicates that the population of children aged 00 to 14 years has been declining to 15.2% of the total population as of 2024, as opposed to 15.6% as of 2023. The crude birth rate per 1,000 population in Thailand has been declining to 6.7 as of 2024, from 7.2 as of 2023. The total fertility rate per woman in Thailand as of 2024 stood at 1.0. These figures clearly indicate that the declining birth rate presents a constraint to the growth of the pediatric end user health category, and such a constraint will need to be addressed by strategic players in the market over the long term.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Thailand Paediatric Consumer Health Market TrendDigital Discovery Channels Are Actively Reshaping End User Purchasing Behaviour

A notable and increasingly pronounced feature of the Thai paediatric consumer Health marketplace has been the rising importance of retail online and social media as influencers of end user purchasing behaviour. This reflects the increasingly favourable receptiveness of parents to education of end users by brands, marketplace operators, and fellow end users via such media of brands and the rising importance of such media as influencers of end user purchasing behaviour. This makes retail online environments increasingly important as conduits of end user purchasing behaviour, as well as conduits of brand awareness development.

According to Thailand's National Statistical Office, in the year 2024, 89.7% of the population of the country above the age of six had access to the internet. In addition to this, Thailand's National Statistical Office indicates that in the year 2024, 91.5% of households had access to the internet. This makes Thailand a country with a strong digital infrastructure, thus providing a strong foundation for the rising importance of retail online as a conduit of end user purchasing behaviour, despite the dominance of physical distribution channels in terms of sales volume.

Thailand Paediatric Consumer Health Market OpportunityTargeted Functional Health Claims Create a Well-Defined Premium Product Opportunity

A commercially viable and clearly defined opportunity exists in the development of premium pediatric health products with clearly defined and functionally specific health benefits. The end user orientation is clearly moving away from generic concepts of providing broad-scope immunity benefits to products with clearly defined benefits in the areas of brain development, appetite control, digestive health benefits, sleep quality, and vision health benefits. This clearly evolving end user orientation presents a significant commercial opportunity to brands that are able to clearly articulate benefits of child-specific health formulations with more convenient delivery systems and a stronger perception of quality and scientific credibility to warrant a premium price point in the health and wellness category.

According to Thailand's National Statistical Office, the country had an urban population of 34.3% as of 2024. Thailand's National Statistical Office also indicates that as of the same year, 91.5% of households had access to the internet. This urbanized and increasingly connected end user orientation significantly reduces the commercial viability of premium brands to educate end users about the benefits of differentiated health products and sustain long-term demand for premium pediatric health solutions to address clearly defined health benefits for children.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Thailand Paediatric Consumer Health Market Segmentation Analysis

By Product Type

- Paediatric Analgesics

- Paediatric Acetaminophen

- Paediatric Aspirin

- Paediatric Combination Products Analgesics

- Paediatric Dipyrone

- Paediatric Ibuprofen

- Paediatric Naproxen

- Paediatric Cough, Cold and Allergy Remedies

- Paediatric Allergy Remedies

- Paediatric Cough/Cold Remedies

- Paediatric Digestive Remedies

- Paediatric Diarrhoeal Remedies

- Paediatric Indigestion and Heartburn Remedies

- Paediatric Laxatives

- Paediatric Motion Sickness Remedies

- Paediatric Dermatologicals

- Nappy (Diaper) Rash Treatments

- Paediatric Vitamins and Dietary Supplements

The segment with highest market share under product type is paediatric vitamins and bietary supplements represent the leading segment, accounting for approximately 55% of total market share. This position of clear leadership reflects the strong and deeply embedded parental preference for preventive care solutions, particularly products associated with immunity reinforcement, digestive health support, brain development, and general childhood wellness management as components of an established daily health routine. The segment's dominance confirms that end user demand within this category is driven primarily by proactive health maintenance intent rather than reactive illness treatment, giving these products a structurally advantaged and recurring role within household purchasing behaviour.

The segment additionally benefits from a broad and continuously expanding range of child-appropriate delivery formats that meaningfully improve both end user product acceptance and parental purchasing frequency. Formats including jelly sticks, oral sprays, and stick pouches make these products more accessible for children to consume and more appealing for parents to incorporate into regular daily wellness routines, sustaining the segment's leading structural position within the overall Thai paediatric consumer Health product mix.

By Sales Channel

- Retail Online

- Online Pharmacies

- E-commerce Platforms

- Brand Websites

- Retail Offline

- Hospital Pharmacies

- Retail Pharmacies / Drugstores

- Supermarkets & Hypermarkets

- Specialty Baby Stores

The segment with highest market share under sales channel is retail offline accounts for approximately 75% of total market share, confirming physical retail as the overwhelmingly dominant purchase channel within Thailand's paediatric consumer Health market. End users continue to demonstrate a clear and consistent preference for store-based purchasing environments, which provide immediate product availability, a higher degree of perceived trust, and a more familiar and reassuring context for making health product selections on behalf of children, particularly in circumstances where prompt access to remedies is required.

Physical pharmacy and store-based outlets enable end users to compare products directly and arrive at confident purchase decisions with greater efficiency, an attribute of particular value when responding to immediate childhood health needs across cough, cold, fever, and wellness categories. While retail online channels continue to attract growing end user interest and incremental commercial volume, retail offline retains its foundational dominance by virtue of its proximity, reliability, and well-established role within the everyday paediatric health purchasing journey across Thailand.

List of Companies Covered in Thailand Paediatric Consumer Health Market

The companies listed below are highly influential in the Thailand paediatric consumer health market, with a significant market share and a strong impact on industry developments.

- Johnson & Johnson (Thailand) Ltd

- Mega Lifesciences Pty Ltd

- British Dispensary (LP) Co Ltd

- GSK Consumer Healthcare

- Seven Seas Health Care Ltd

- Thai Nakorn Patana Co Ltd

- Boehringer Ingelheim (Thai) Ltd

- Bristol-Myers Squibb (Thailand) Ltd

- SSL International Plc

- Ouayun Dispensary Co Ltd

Competitive Landscape

Thailand paediatric consumer health market reflects a competitive landscape driven by local herbal brands, emerging supplement innovators, and diversified product formats tailored for children. Mr Herb is gaining traction in cough and cold remedies through natural formulations aligned with parental preference for herbal solutions, while Master Rabbit is expanding its presence with products such as Master Rabbit P Lysine and immune-support sprays. Meanwhile, brands like Zogumi and Vita Plus are differentiating through child-friendly formats such as jelly sticks and sprays, enhancing product appeal. Increasing competition is also visible in probiotic-focused offerings from Lamoon Baby. Overall, the market is becoming highly dynamic, with brands competing through natural positioning, innovative formats, and targeted functional benefits for children.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Thailand Paediatric Consumer Health Market Policies, Regulations, and Standards

- Thailand Paediatric Consumer Health Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Thailand Paediatric Consumer Health Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product Type

- Paediatric Analgesics- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Acetaminophen- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Aspirin- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Combination Products Analgesics- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Dipyrone- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Ibuprofen- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Naproxen- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Cough, Cold and Allergy Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Allergy Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Cough/Cold Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Digestive Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Diarrhoeal Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Indigestion and Heartburn Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Laxatives- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Motion Sickness Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Dermatologicals- Market Insights and Forecast 2022-2032, USD Million

- Nappy (Diaper) Rash Treatments- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Vitamins and Dietary Supplements- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Analgesics- Market Insights and Forecast 2022-2032, USD Million

- By Dosage Form

- Liquid Syrups- Market Insights and Forecast 2022-2032, USD Million

- Chewable Tablets- Market Insights and Forecast 2022-2032, USD Million

- Drops- Market Insights and Forecast 2022-2032, USD Million

- Powders/Sachets- Market Insights and Forecast 2022-2032, USD Million

- Gummies- Market Insights and Forecast 2022-2032, USD Million

- Topical Creams & Ointments- Market Insights and Forecast 2022-2032, USD Million

- By Age Group

- Infants & Toddlers (0-3 Years)- Market Insights and Forecast 2022-2032, USD Million

- Children (4-12 Years)- Market Insights and Forecast 2022-2032, USD Million

- Adolescents (13-18 Years)- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type

- Acute Treatment- Market Insights and Forecast 2022-2032, USD Million

- Chronic Condition Management- Market Insights and Forecast 2022-2032, USD Million

- Genetic & Rare Disease Management- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- Online Pharmacies- Market Insights and Forecast 2022-2032, USD Million

- E-commerce Platforms- Market Insights and Forecast 2022-2032, USD Million

- Brand Websites- Market Insights and Forecast 2022-2032, USD Million

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- Hospital Pharmacies- Market Insights and Forecast 2022-2032, USD Million

- Retail Pharmacies / Drugstores- Market Insights and Forecast 2022-2032, USD Million

- Supermarkets & Hypermarkets- Market Insights and Forecast 2022-2032, USD Million

- Specialty Baby Stores

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Product Type

- Market Size & Growth Outlook

- Thailand Paediatric Analgesics Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Dosage Form- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Thailand Paediatric Cough, Cold and Allergy Remedies Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Dosage Form- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Thailand Paediatric Digestive Remedies Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Dosage Form- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Thailand Paediatric Dermatologicals Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Dosage Form- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Thailand Nappy (Diaper) Rash Treatments Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Dosage Form- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Thailand Paediatric Vitamins and Dietary Supplements Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Dosage Form- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- GSK Consumer Healthcare

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Seven Seas Health Care Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Thai Nakorn Patana Co Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Boehringer Ingelheim (Thai) Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Bristol-Myers Squibb (Thailand) Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Johnson & Johnson (Thailand) Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Mega Lifesciences Pty Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- British Dispensary (LP) Co Ltd The

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- SSL International Plc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Ouayun Dispensary Co Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- GSK Consumer Healthcare

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Dosage Form |

|

| By Age Group |

|

| By Treatment Type |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.