Thailand Diagnostic Labs Market Report: Trends, Growth and Forecast (2026-2032)

By Lab Type (Single/Independent Laboratories, Hospital-based Laboratories, Physician Office Laboratories, Others), By Testing Services (Physiological Function Testing, General & Clinical Testing, Esoteric Testing, Specialized Testing, Non-invasive Prenatal Testing, COVID-19 Testing, Others), By Disease (Cardiology, Oncology, Neurology, Orthopedics, Gastroenterology, Gynecology, Odontology, Others), By Revenue Source (Healthcare Plan, Out-of-Pocket, Public System), By Test Type (Pathology, Radiology), By End User (Referrals, Walk-ins, Corporate Clients) ... Read more

|

Major Players

|

Thailand Diagnostic Labs Market Statistics and Insights, 2026

- Market Size Statistics

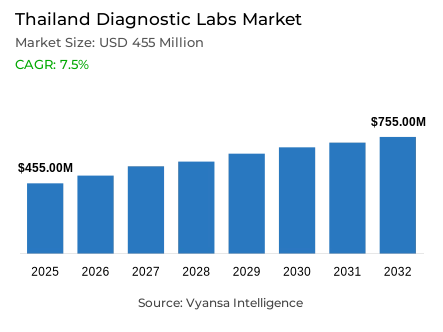

- Diagnostic labs market size in Thailand was estimated at USD 455 million in 2025.

- The market size is expected to grow to USD 755 million by 2032.

- Market to register a CAGR of around 7.5% during 2026-32.

- Lab Type Shares

- Hospital-based laboratories grabbed market share of 50%.

- Competition

- More than 10 companies are actively engaged in producing diagnostic labs in Thailand.

- Top 5 companies acquired around 55% of the market share.

- Bangkok R.I.A. Group (BRIA LAB), Central Laboratory (Thailand) Co. Ltd., Thonburi Lab Center, Bumrungrad Laboratory, Bangkok Medical Lab etc., are few of the top companies.

- Testing Services

- General & clinical testing grabbed 45% of the market.

Thailand Diagnostic Labs Market Outlook

Thailand diagnostic labs market is positioned for steady expansion, estimated at $455 million in 2025 and projected to reach $755 million by 2032, registering a CAGR of approximately 7.5% during the 2026-32 period. This growth is fundamentally driven by Thailand's transition into an ageing society, with 14.03 million people aged 60 and above representing 20% of the total population. As chronic conditions including diabetes, cardiovascular diseases, and renal disorders become more prevalent, this demographic cohort routinely requires repeat laboratory tests such as blood glucose monitoring, lipid panels, and kidney function assessments, sustaining steady sample volumes across testing facilities.

Under the Lab Type segmentation, hospital-based laboratories dominate the market with a 50% share, operating within hospital facilities to handle routine and urgent testing requirements linked to outpatient consultations, emergency care, and inpatient monitoring. Their physical proximity to ordering physicians significantly reduces sample transport time and supports rapid clinical decision-making. Independent stand-alone and reference laboratories comprise the remaining market share, competing on convenience factors, competitive pricing, and extensive collection networks, particularly for walk-in testing panels and corporate health screening programs.

The Testing Services segment is dominated by General and Clinical Testing with a market share of forty five percent which includes high frequency diagnostic tests like complete blood counts, glucose, lipid profiles and liver and kidney functional panels. The tests are ordered in almost all care environments such as preventive check-ups, chronic disease follow-ups, and post-treatment follow-ups, thus guaranteeing high testing volumes at all times. Higher levels of testing, including molecular diagnostics and immunology, are typically growing based on specialist referrals and complicated clinical needs.

Thailand is also advancing in terms of healthcare digitalization, which benefits the market since 10,435 health facilities are currently connected to shared electronic health databases, which allow faster electronic referrals and better access to previous test results. In addition, high inbound travel 17.5 million foreign visitors in the first half of 2024 generates high demand of rapid diagnostic services that are specific to international patients, which is advantageous to providers with fast turnaround times and internationally accepted reporting formats.

Thailand Diagnostic Labs Market Growth Driver

Demographic Shift Driving Sustained Testing Volumes

Thailand is moving towards an ageing population, thus essentially increasing the minimum level of demand of laboratory monitoring services. In April-June 2024, the Survey of the Older Persons in Thailand, a survey of 86,880 sampled households in the country, conducted by the National Statistical Office, reported 14.03 million persons aged 60 and above, or 20.0% of the total population. The survey also reported old-age dependency ratio of 31.1 implying that every 100 working-age people have to take care of about 31 elderly people.

Since chronic illnesses like diabetes, cardiovascular disease and renal disorders are age-related, this age group of the population regularly needs repeat laboratory tests, such as blood glucose monitoring, lipid profiles, kidney and liver function tests, and complete blood counts to diagnose, monitor medications and complications. The population also contributes to the need to have convenient collection methods like the use of local draw centres and home visits, and effective turnaround time to facilitate follow-up appointments. Since these are periodic and protocol-based tests, the growing 60+ base maintains constant sample volumes in both hospital-based and independent laboratories, even when elective procedures are changing.

Thailand Diagnostic Labs Market Challenge

Import Reliance Creates Cost and Availability Vulnerabilities

The diagnostic laboratory industry in Thailand is highly exposed to imported kits and reagents, which makes the costs and availability of the industry highly sensitive to the global supply conditions and logistical disruptions. According to World Bank WITS data, which is based on UN Comtrade, imports of Thailand of the category of goods of the HS 382200, which is Medical Test kits, amounted to US 489 757.07 000 in 2023, including 7,562,200 kg of imported goods. The biggest suppliers are the United States, which contributes US$175,025.48k, and Germany, which contributes US 79,886.14k.

Importing vital consumables means that laboratories have to deal with longer lead times, cold-chain logistics needs, and price fluctuations associated with freight expenses and currency variations. This is especially a problem in smaller stand-alone laboratories that have less purchasing power and less safety-stock capacity. The resulting pressures influence test pricing and service consistency, with laboratories potentially rationing some assays, increasing turnaround times, or replacing testing methods in cases of supply shortages, directly influencing end-user experience and satisfaction.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Thailand Diagnostic Labs Market Trend

Digital Integration Enhancing Healthcare Connectivity

The healthcare infrastructure in Thailand is evolving to a more closely digitalized system of patient data, which has significantly enhanced the flow of laboratory results across care environments and the clinical decision-making process. In a February 2025 update on the health data linkage project of the Ministry of Public Health-Prince of Songkla University, the Faculty of Medicine stated that 10435 health facilities in the country are linked to the shared electronic health database. The update also featured 1648375 Mor Prom app users in Regional Health 12 who are able to access personal health data on mobile platforms.

In the case of diagnostic laboratories, this digital transformation enables quicker electronic referrals, better access to previous test outcomes, and a smooth hand-off between ordering clinicians and testing locations. Improved interoperability minimizes redundant testing due to missing patient history and allows clinicians to understand longitudinal changes in indicators like renal function panels or HbA1c measurements. Also, faster delivery of results to the end users enhances satisfaction and adherence to treatment, making turnaround time and quality of reporting a key competitive differentiator as laboratories compete to gain market share.

Thailand Diagnostic Labs Market Opportunity

Medical Tourism Supporting Premium Diagnostic Services

The inbound travel is high and supports the private healthcare ecosystem in Thailand and creates high demand of quick and reliable diagnostic services to meet international end users. According to the Government Public Relations Department, which cited the Ministry of Tourism and Sports, Thailand received 17,501,283 foreign visitors in the first six months of 2024, or between January 1 and June 30. Although not every visit is medical, the large number of visitors increases the demand of traveler-facing healthcare services such as urgent care visits, pre-procedure screening, and infection diagnosis.

In the case of diagnostic laboratories, this environment favours providers with the ability to provide fast turnaround times, internationally accepted test reporting formats, and strong quality assurance procedures to assist hospitals and clinics in Bangkok and other key tourist provinces. It also establishes joint ventures with travel insurance companies and medical centres that need standardised test panels like complete blood counts, electrolyte tests and basic infection screening services on expedited schedules. The competitive advantages of serving this mobile end-user base are to laboratories that invest in longer operating hours and advanced specimen logistics.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Thailand Diagnostic Labs Market Segmentation Analysis

By Lab Type

- Single/Independent Laboratories

- Hospital-based Laboratories

- Physician Office Laboratories

- Others

Under the Lab Type segmentation, hospital-based laboratories represent the dominant segment, commanding a 50% market share. These laboratories operate within hospital facilities, positioning them to handle the majority of routine and urgent testing requirements linked to outpatient consultations, emergency care presentations, and inpatient monitoring protocols. Their physical proximity to ordering physicians significantly reduces sample transport time and supports rapid clinical decision-making for surgery clearance, infection diagnosis, and critical care management.

Independent stand-alone laboratories and reference laboratories comprise the remaining market share and typically compete on convenience factors, competitive pricing structures, and extensive collection networks. These facilities are frequently utilized for walk-in testing panels, corporate health screening programs, and specialized send-out tests that smaller hospitals may not offer in-house. As hospital systems increasingly focus on core clinical pathways, outsourcing arrangements and referral flows sustain the relevance of non-hospital laboratories, particularly those offering home collection services, digital result reporting, and recognized quality certifications.

By Testing Services

- Physiological Function Testing

- General & Clinical Testing

- Esoteric Testing

- Specialized Testing

- Non-invasive Prenatal Testing

- COVID-19 Testing

- Others

Under the Testing Services segmentation, General & Clinical Testing emerges as the leading segment, accounting for 45% of the total market share. This category encompasses high-frequency diagnostic tests including complete blood counts, glucose measurements, lipid profiles, liver and kidney function panels, and basic urinalysis. These tests are ordered across virtually every care setting—preventive health checkups, chronic disease follow-ups, pre-admission workups, and post-treatment monitoring—ensuring consistently high testing volumes.

Other testing service categories such as advanced immunology, molecular diagnostics, microbiology cultures, and histopathology typically experience growth driven by specialist referrals and complex clinical requirements. These services often necessitate sophisticated instrumentation, stringent sample handling protocols, and specialized technical expertise, concentrating capacity within larger hospital laboratories and dedicated reference facilities. Consequently, general and clinical testing remains the fundamental service line anchoring day-to-day laboratory operations, while specialized testing categories contribute value through clinical complexity and higher diagnostic specificity.

List of Companies Covered in Thailand Diagnostic Labs Market

The companies listed below are highly influential in the Thailand diagnostic labs market, with a significant market share and a strong impact on industry developments.

- Bangkok R.I.A. Group (BRIA LAB)

- Central Laboratory (Thailand) Co. Ltd.

- Thonburi Lab Center

- Bumrungrad Laboratory

- Bangkok Medical Lab

- Medical Innovation Center (MIC Lab)

- Hi-Tech Laboratories

- Bio Molecular Laboratory (BML)

- Innotech Lab Services

- Pathlab (Thailand) Ltd.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. Thailand Diagnostic Labs Market Policies, Regulations, and Standards

4. Thailand Diagnostic Labs Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. Thailand Diagnostic Labs Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in USD Million

5.2. Market Segmentation & Growth Outlook

5.2.1.By Lab Type

5.2.1.1. Single/Independent Laboratories- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Hospital-based Laboratories- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3. Physician Office Laboratories- Market Insights and Forecast 2022-2032, USD Million

5.2.1.4. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Testing Services

5.2.2.1. Physiological Function Testing- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. General & Clinical Testing- Market Insights and Forecast 2022-2032, USD Million

5.2.2.3. Esoteric Testing- Market Insights and Forecast 2022-2032, USD Million

5.2.2.4. Specialized Testing- Market Insights and Forecast 2022-2032, USD Million

5.2.2.5. Non-invasive Prenatal Testing- Market Insights and Forecast 2022-2032, USD Million

5.2.2.6. COVID-19 Testing- Market Insights and Forecast 2022-2032, USD Million

5.2.2.7. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Disease

5.2.3.1. Cardiology- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Oncology- Market Insights and Forecast 2022-2032, USD Million

5.2.3.3. Neurology- Market Insights and Forecast 2022-2032, USD Million

5.2.3.4. Orthopedics- Market Insights and Forecast 2022-2032, USD Million

5.2.3.5. Gastroenterology- Market Insights and Forecast 2022-2032, USD Million

5.2.3.6. Gynecology- Market Insights and Forecast 2022-2032, USD Million

5.2.3.7. Odontology- Market Insights and Forecast 2022-2032, USD Million

5.2.3.8. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Revenue Source

5.2.4.1. Healthcare Plan- Market Insights and Forecast 2022-2032, USD Million

5.2.4.2. Out-of-Pocket- Market Insights and Forecast 2022-2032, USD Million

5.2.4.3. Public System- Market Insights and Forecast 2022-2032, USD Million

5.2.5.By Test Type

5.2.5.1. Pathology- Market Insights and Forecast 2022-2032, USD Million

5.2.5.2. Radiology- Market Insights and Forecast 2022-2032, USD Million

5.2.6.By End User

5.2.6.1. Referrals- Market Insights and Forecast 2022-2032, USD Million

5.2.6.2. Walk-ins- Market Insights and Forecast 2022-2032, USD Million

5.2.6.3. Corporate Clients- Market Insights and Forecast 2022-2032, USD Million

5.2.7.By Competitors

5.2.7.1. Competition Characteristics

5.2.7.2. Market Share & Analysis

6. Thailand Single/Independent Laboratories Market Statistics, 2022-2032

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in USD Million

6.2. Market Segmentation & Growth Outlook

6.2.1.By Testing Services- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Disease- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By Revenue Source- Market Insights and Forecast 2022-2032, USD Million

6.2.4.By Test Type- Market Insights and Forecast 2022-2032, USD Million

6.2.5.By End User- Market Insights and Forecast 2022-2032, USD Million

7. Thailand Hospital-based Laboratories Market Statistics, 2022-2032

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in USD Million

7.2. Market Segmentation & Growth Outlook

7.2.1.By Testing Services- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Disease- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By Revenue Source- Market Insights and Forecast 2022-2032, USD Million

7.2.4.By Test Type- Market Insights and Forecast 2022-2032, USD Million

7.2.5.By End User- Market Insights and Forecast 2022-2032, USD Million

8. Thailand Physician Office Laboratories Market Statistics, 2022-2032

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in USD Million

8.2. Market Segmentation & Growth Outlook

8.2.1.By Testing Services- Market Insights and Forecast 2022-2032, USD Million

8.2.2.By Disease- Market Insights and Forecast 2022-2032, USD Million

8.2.3.By Revenue Source- Market Insights and Forecast 2022-2032, USD Million

8.2.4.By Test Type- Market Insights and Forecast 2022-2032, USD Million

8.2.5.By End User- Market Insights and Forecast 2022-2032, USD Million

9. Competitive Outlook

9.1. Company Profiles

9.1.1.Bumrungrad Laboratory

9.1.1.1. Business Description

9.1.1.2. Service Portfolio

9.1.1.3. Collaborations & Alliances

9.1.1.4. Recent Developments

9.1.1.5. Financial Details

9.1.1.6. Others

9.1.2.Bangkok Medical Lab

9.1.2.1. Business Description

9.1.2.2. Service Portfolio

9.1.2.3. Collaborations & Alliances

9.1.2.4. Recent Developments

9.1.2.5. Financial Details

9.1.2.6. Others

9.1.3.Medical Innovation Center (MIC Lab)

9.1.3.1. Business Description

9.1.3.2. Service Portfolio

9.1.3.3. Collaborations & Alliances

9.1.3.4. Recent Developments

9.1.3.5. Financial Details

9.1.3.6. Others

9.1.4.Hi-Tech Laboratories

9.1.4.1. Business Description

9.1.4.2. Service Portfolio

9.1.4.3. Collaborations & Alliances

9.1.4.4. Recent Developments

9.1.4.5. Financial Details

9.1.4.6. Others

9.1.5.Bio Molecular Laboratory (BML)

9.1.5.1. Business Description

9.1.5.2. Service Portfolio

9.1.5.3. Collaborations & Alliances

9.1.5.4. Recent Developments

9.1.5.5. Financial Details

9.1.5.6. Others

9.1.6.Bangkok R.I.A. Group (BRIA LAB)

9.1.6.1. Business Description

9.1.6.2. Service Portfolio

9.1.6.3. Collaborations & Alliances

9.1.6.4. Recent Developments

9.1.6.5. Financial Details

9.1.6.6. Others

9.1.7.Central Laboratory (Thailand) Co. Ltd.

9.1.7.1. Business Description

9.1.7.2. Service Portfolio

9.1.7.3. Collaborations & Alliances

9.1.7.4. Recent Developments

9.1.7.5. Financial Details

9.1.7.6. Others

9.1.8.Thonburi Lab Center

9.1.8.1. Business Description

9.1.8.2. Service Portfolio

9.1.8.3. Collaborations & Alliances

9.1.8.4. Recent Developments

9.1.8.5. Financial Details

9.1.8.6. Others

9.1.9.Innotech Lab Services

9.1.9.1. Business Description

9.1.9.2. Service Portfolio

9.1.9.3. Collaborations & Alliances

9.1.9.4. Recent Developments

9.1.9.5. Financial Details

9.1.9.6. Others

9.1.10. Pathlab (Thailand) Ltd.

9.1.10.1. Business Description

9.1.10.2. Service Portfolio

9.1.10.3. Collaborations & Alliances

9.1.10.4. Recent Developments

9.1.10.5. Financial Details

9.1.10.6. Others

10. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Lab Type |

|

| By Testing Services |

|

| By Disease |

|

| By Revenue Source |

|

| By Test Type |

|

| By End User |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.