Switzerland Sleep Aids Market Report: Trends, Growth and Forecast (2026-2032)

By Product (Single Ingredient (Doxylamine Succinate, Diphenhydramine, Melatonin), Combination Ingredient (Diphenhydramine + Acetaminophen, Other Antihistamine-Based Combinations), Herbal & Traditional Sleep Aids (Valerian root, Passionflower, Chamomile, Kava, Multi-Herbal Sleep Blends)), By Sleep Disorder (Insomnia, Sleep Apnea, Restless Legs Syndrome, Narcolepsy, Sleep Walking, Others), By Age Group (Young to Mid Adults (25-44 Years), Middle-Aged Adults (45-64 Years), Geriatric Population (65+ Years)), By Sales Channel (Retail Online, Retail Offline), By End User (Homecare/Individual Consumers, Hospitals, Sleep Centers & Clinics), By Formulation (Tablets, Gummies, Capsules, Liquid, Sublingual) ... Read more

|

Major Players

|

Switzerland Sleep Aids Market Statistics and Insights, 2026

- Market Size Statistics

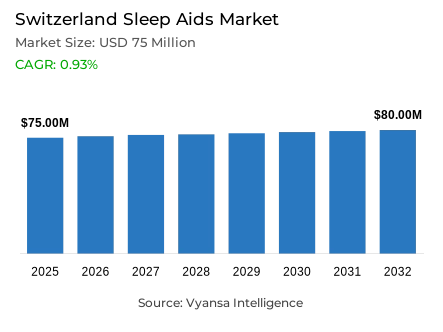

- Sleep aids market size in Switzerland was estimated at USD 75 million in 2025.

- The market size is expected to grow to USD 80 million by 2032.

- Market to register a CAGR of around 0.93% during 2026-32.

- Product Shares

- Melatonin grabbed market share of 40%.

- Competition

- More than 10 companies are actively engaged in producing sleep aids in Switzerland.

- Top 5 companies acquired around 50% of the market share.

- Weleda AG, A Vogel AG, PharmaSGP GmbH, Sidroga AG, Bayer (Schweiz) AG etc., are few of the top companies.

- Sales channel

- Retail offline grabbed 65% of the market.

Switzerland Sleep Aids Market Outlook

The Switzerland sleep aids market was valued at USD 75 million in 2025 and is projected to grow from USD 77.81 million in 2026 to USD 80 million by 2032, registering a CAGR of 0.93% over the forecast period. This measured growth is primarily sustained by a rising prevalence of insomnia, which affects over 30% of adults due to urbanisation, chronic stress, and pervasive digital device usage. As Swiss consumers grow increasingly aware of the direct link between restful sleep and overall health, demand for credible and professional sleep solutions remains steady.

The market is currently shaped by a strong and deepening preference for herbal and traditional remedies, widely perceived as safer and more wholesome than synthetic options. Melatonin has established a 40% product share as consumers seek effective ways to regulate their internal clocks, while trusted local brands such as Valverde Schlaf and Zeller Schlaf continue to lead the category. Many residents actively prefer these established names over lesser-known alternatives to avoid concerns around potential side effects or long-term dependency.

Retail offline channels dominate the distribution landscape with 65% of the market, with pharmacies serving as the primary touchpoint for expert guidance and product reassurance. Drugstores are gaining incremental traction through private label offerings and their proximity to rural consumers, yet the professional consultation provided by pharmacists remains a decisive factor, particularly for those managing complex or persistent sleep symptoms requiring careful product selection.

Looking toward 2032, the market is expected to navigate high levels of saturation alongside growing competition from holistic health practices including meditation, yoga, and digital wellness tools. While these alternatives may temper long-term volume expansion, the continuous introduction of new product formats and premium natural formulations will sustain value sales. Manufacturers will consequently focus on evolving their portfolios to ensure modern sleep aids meet the sophisticated and health-conscious expectations of the Swiss consumer population.

Switzerland Sleep Aids Market Growth DriverStress, Device Use, and Low Activity Sustain Sleep Support Demand

Sleep disturbance remains an endemic and common problem across Switzerland, with urbanization, stress, anxiety, heavy use of nighttime devices, and lack of physical exercise continuing to interfere with natural sleep cycles. Physical pain caused by pains, breathing problems, and underlying health problems also contribute to sleep problems, especially when risk factors like old age and overweight are involved in the constant deterioration of the quality of rest.

In accordance with the OECD Health at a Glance 2025 country note, 22% of Swiss adults fail to achieve adequate physical activity levels, thereby reinforcing one of the principal lifestyle determinants directly associated with ongoing sleep difficulties. This combination of behavioural and physical factors maintains a wide and long-term need of easily available sleep support solutions throughout the Swiss market until 2032.

Switzerland Sleep Aids Market ChallengeSaturated Pharmacy Shelves and Efficacy Scepticism Tighten Competition

Competition in Switzerland is already very dense, and both local and global brands are providing low-side-effect formulations and milder natural substitutes. As a result, meaningful breakthrough differentiation is becoming more of a burden, especially since a portion of consumers are now actively doubting product efficacy or are seeking non-product solutions like meditation, yoga, dietary changes, and less screen time.

PharmaSuisse Facts and Figures 2025 states that there are about 20 pharmacies per 100,000 people in Switzerland, which concentrates the competition in a highly professional retail setting where trust in pharmacists and in-store advice have a powerful impact on the ultimate purchase decision. This concentration increases the barrier to entry of brands that want to differentiate themselves and strengthens the leading position of well-established brands that already have pharmacist acceptance and brand recognition.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Switzerland Sleep Aids Market TrendHerbal-First Preference Expands Complementary Product Pipeline

Natural, herbal and traditional sleep aids are increasingly becoming popular among the consumers in Switzerland due to the perception of being more wholesome, more tolerable and less likely to cause side effects than the synthetic counterparts. Tea formats are supporting this change by making sleep support a recognizable and helpful hot drink instead of traditional medication, which helps to promote local brands that are based on established tablet and tea habits.

Swissmedic reports that eleven new complementary and herbal medicinal products were approved in 2025, five of which had a specific indication, which confirms that the pipeline remains active in the herbal field. This regulatory trend is an indication that the herbal-first preference is not just influencing consumer behaviour, but is also actively driving product development and portfolio expansion in the Swiss sleep aid category up to 2032.

Switzerland Sleep Aids Market OpportunityPremium, Comorbidity-Safe Positioning Builds Value in Mature Market

There is a strong potential to have trusted brands capture incremental value by focusing on reassurance, more explicit usage instructions, and formulations that are framed as milder and appropriate to consumers with multiple health concerns at once. With the ongoing worries about dependency and side effects, products that convey safety, tolerability, and compatibility with more general health conditions have a unique and increasing popularity.

In line with the OECD Health at a Glance 2025 country note, self‑reported obesity prevalence in Switzerland stands at 12%, underscoring the relevance of sleep solutions that address disruption alongside broader health factors. This provides a plausible and commercially viable route to value growth through premiumisation as opposed to volume disruption, allowing brands to build differentiated portfolios that appeal to the health-conscious and discerning consumer market in Switzerland up to 2032.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Switzerland Sleep Aids Market Segmentation Analysis

By Product

- Single Ingredient

- Combination Ingredient

- Herbal & Traditional Sleep Aids

The product type with the highest market share is melatonin, accounting for approximately 40% of the total market. This leadership is indicative of a market in which consumers are more comfortable with familiar and low-friction solutions and tend to begin with solutions that are seen as milder and more tolerable before considering more powerful synthetic alternatives. The broad consumer awareness and the long-standing safety record of Melatonin keep it as the mainstream sleep aid of choice.

Such dominance also provides a significant level of product development flexibility, with melatonin being able to be offered in a variety of formats and combined with calming or herbal-adjacent positioning without changing the active ingredient. Dosing clarity, format convenience, and trust-based communication are effective ways of differentiation that brands can adopt to meet the strong preference of the Swiss market to well-known names and tolerability-based benefit messages until 2032.

By Sales Channel

- Retail Online

- Retail Offline

The sales channel with the greatest market share is retail offline, accounting for approximately 65% of the total market. This is indicative of the sensitivity of the usage of sleep aids where shoppers highly regard professional advice on the anticipated effects, proper usage instructions, and possible interactions of ingredients-needs that the in-store pharmacy setting is uniquely placed to provide with consistency and credibility.

The offline strength is also supported by the increasing role of drugstores in less populated and rural regions where physical proximity strengthens access and convenience in purchasing. The development of own label in drugstores is also expanding the scope of low-cost alternatives offered via offline channels, and pharmacies are still keeping the consumer trust and maintaining the professional consultation experience that will be at the center of sleep aid purchasing decisions in Switzerland until 2032.

List of Companies Covered in Switzerland Sleep Aids Market

The companies listed below are highly influential in the Switzerland sleep aids market, with a significant market share and a strong impact on industry developments.

- Weleda AG

- A Vogel AG

- PharmaSGP GmbH

- Sidroga AG

- Bayer (Schweiz) AG

- Medinova AG

- Haleon Schweiz AG

- Max Zeller Sohne AG

- Walther Schoenenberger Pflanzensaftwerk GmbH & Co KG

- Verfora AG

Competitive Landscape

Switzerland’s sleep aids market in 2025 is led by Sidroga AG with its Valverde Schlaf brand, which leverages strong herbal positioning and dual tablet and tea formats to capitalise on consumer preference for natural, low-side-effect solutions. Max Zeller Söhne AG follows with Zeller Schlaf, benefiting from local heritage and a segmented portfolio tailored to varying sleep needs. Pharmacies remain the dominant channel due to trust and professional advice, though drugstores are gaining share through proximity and private label expansion. The market is saturated, with limited room for disruptive entrants. Indirect competition from meditation, vitamins and dietary supplements, CBD, and lifestyle interventions is intensifying. Differentiation opportunities lie in premium herbal blends, trusted brand storytelling, and format innovation that reinforces safety and efficacy perceptions.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Switzerland Sleep Aids Market Policies, Regulations, and Standards

- Switzerland Sleep Aids Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Switzerland Sleep Aids Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product

- Single Ingredient- Market Insights and Forecast 2022-2032, USD Million

- Doxylamine Succinate- Market Insights and Forecast 2022-2032, USD Million

- Diphenhydramine- Market Insights and Forecast 2022-2032, USD Million

- Melatonin- Market Insights and Forecast 2022-2032, USD Million

- Combination Ingredient- Market Insights and Forecast 2022-2032, USD Million

- Diphenhydramine + Acetaminophen- Market Insights and Forecast 2022-2032, USD Million

- Other Antihistamine-Based Combinations- Market Insights and Forecast 2022-2032, USD Million

- Herbal & Traditional Sleep Aids- Market Insights and Forecast 2022-2032, USD Million

- Valerian root- Market Insights and Forecast 2022-2032, USD Million

- Passionflower- Market Insights and Forecast 2022-2032, USD Million

- Chamomile- Market Insights and Forecast 2022-2032, USD Million

- Kava- Market Insights and Forecast 2022-2032, USD Million

- Multi-Herbal Sleep Blends- Market Insights and Forecast 2022-2032, USD Million

- Single Ingredient- Market Insights and Forecast 2022-2032, USD Million

- By Sleep Disorder

- Insomnia- Market Insights and Forecast 2022-2032, USD Million

- Sleep Apnea- Market Insights and Forecast 2022-2032, USD Million

- Restless Legs Syndrome- Market Insights and Forecast 2022-2032, USD Million

- Narcolepsy- Market Insights and Forecast 2022-2032, USD Million

- Sleep Walking- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Age Group

- Young to Mid Adults (25-44 Years)- Market Insights and Forecast 2022-2032, USD Million

- Middle-Aged Adults (45-64 Years)- Market Insights and Forecast 2022-2032, USD Million

- Geriatric Population (65+ Years)- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- By End User

- Homecare/Individual Consumers- Market Insights and Forecast 2022-2032, USD Million

- Hospitals- Market Insights and Forecast 2022-2032, USD Million

- Sleep Centers & Clinics- Market Insights and Forecast 2022-2032, USD Million

- By Formulation

- Tablets- Market Insights and Forecast 2022-2032, USD Million

- Gummies- Market Insights and Forecast 2022-2032, USD Million

- Capsules- Market Insights and Forecast 2022-2032, USD Million

- Liquid- Market Insights and Forecast 2022-2032, USD Million

- Sublingual- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Product

- Market Size & Growth Outlook

- Switzerland Single Ingredient Sleep Aids Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Sleep Disorder- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Formulation- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Switzerland Combination Ingredient Sleep Aids Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Sleep Disorder- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Formulation- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Switzerland Herbal & Traditional Sleep Aids Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Sleep Disorder- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Formulation- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Sidroga AG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Bayer (Schweiz) AG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Medinova AG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Haleon Schweiz AG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Max Zeller Söhne AG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Weleda AG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- A Vogel AG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- PharmaSGP GmbH

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Walr Schoenenberger Pflanzensaftwerk GmbH & Co KG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Verfora AG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Sidroga AG

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product |

|

| By Sleep Disorder |

|

| By Age Group |

|

| By Sales Channel |

|

| By End User |

|

| By Formulation |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.