Switzerland Contact Lenses and Solutions Market Report: Trends, Growth and Forecast (2026-2032)

By Product Type (Contact Lenses (Standard Vision Correction Lenses, Myopia Control Lenses), Contact Lens Solutions), By Usage (Contact Lenses (Daily Disposable, Bi-Weekly, Monthly, Quarterly/Annual), Contact Lens Solutions (Daily-Use Care Solutions, Weekly/Periodic Deep-Clean Systems, Travel/Mini Packs)), By Material Type (Contact Lenses (Silicone Hydrogel, Hydrogel (Soft), Rigid Gas Permeable (RGP), Hybrid/Scleral/Specialty), Contact Lens Solutions (Multi-Purpose Solutions, Hydrogen Peroxide Systems, Saline Solutions, Enzymatic & Specialty Cleaners)), By Application (Contact Lenses (Spherical (Myopia/Hyperopia), Toric (Astigmatism), Multifocal (Presbyopia), Myopia Control, Cosmetic/Colored, Therapeutic/Medical), Contact Lens Solutions (Soft Lens Care, RGP Lens Care, Sensitive Eye/Preservative-Free Care)), By Sales Channel (Retail Offline (Optical Stores, Hospitals & Clinics, Others (Pharmacies, Beauty Centres, etc.)), Retail Online (Company-owned Portals, E-commerce Platforms)), By Pack Size (Contact Lenses (Trial Packs, Standard Packs, Bulk/Value Packs), Contact Lens Solutions (Up to 120 mL, 121–360 mL, Above 360 mL, Combo/Twin Packs)) ... Read more

|

Major Players

|

Switzerland Contact Lenses and Solutions Market Statistics and Insights, 2026

- Market Size Statistics

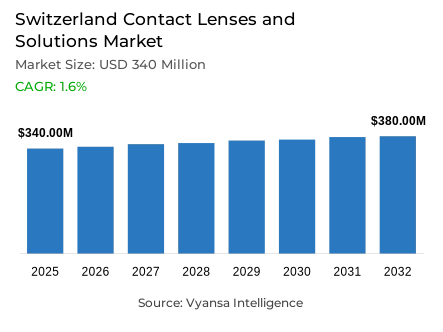

- Contact lenses and solutions market size in Switzerland was estimated at USD 340 million in 2025.

- The market size is expected to grow to USD 380 million by 2032.

- Market to register a CAGR of around 1.6% during 2026-32.

- Product Type Shares

- Contact lenses grabbed market share of 80%.

- Competition

- More than 5 companies are actively engaged in producing contact lenses and solutions in Switzerland.

- Top 5 companies acquired around 75% of the market share.

- Prolens AG, Swisslens SA, Wöhlk Contactlinsen GmbH, Johnson & Johnson AG, Alcon Switzerland AG etc., are few of the top companies.

- Sales Channel

- Retail offline grabbed 70% of the market.

Switzerland Contact Lenses and Solutions Market Outlook

The Switzerland contact‑lens and solution market was valued at USD 340 million in 2025 and is projected to expand to USD 380 million by 2032, registering a CAGR of approximately 1.6% during 2026-2032. The increasing prevalence of myopia supports growth. The World Health Organization (2025) states that the prevalence of myopia in the world is on the rise, especially in children and adolescents because of the long-term exposure to screens. In Switzerland, 27.5 % of young Swiss adults aged 18‑25 are estimated to be affected by myopia, sustaining long‑term demand for corrective vision products.

Myopia-control lenses and orthokeratology lenses have been included in the MiGeL reimbursement catalogue of Switzerland since July 2024, with a maximum reimbursement of CHF 850 (USD 1100.75) per year (Federal Office of Public Health, 2024). This policy enhances organized clinical adoption and enhances accessibility. Contact lenses and solutions benefit from this reimbursement framework, especially among younger demographics receiving professional prescriptions.

However, cost sensitivity is still a structural issue; the Swiss Federal Statistical Office (2025) indicates that healthcare spending per capita is one of the highest in Europe, which strengthens the prudent end-user spending on recurring health products.

By segmentation, contact lenses constitute 80 % of the product share, reflecting strong demand for convenience and active‑lifestyle compatibility; offline retail dominates with a 70 % share, as professional eye examinations and reimbursement procedures necessitate optician‑led purchasing pathways.

Switzerland Contact Lenses and Solutions Market Growth DriverRising Myopia Prevalence Supporting Corrective Eye Care Demand

Switzerland has a high and increasing prevalence of myopia, which is the direct basis of long-term demand of corrective eyewear. The World Health Organization (WHO, 2025) reports that the prevalence of myopia is on the increase worldwide, especially in children and adolescents because of the long-term exposure to screens and lifestyle. In Switzerland, 27.5 % of young Swiss adults aged 18‑25 are estimated to be affected by myopia, reflecting a strong underlying need for long‑term vision correction solutions.

Moreover, myopia-control lenses and orthokeratology lenses have been included in the MiGeL reimbursement catalogue of Switzerland since July 2024, and are covered by CHF 850 (USD 1100.75) per year when prescribed to persons aged 21 and below (Federal Office of Public Health - FOPH). This reimbursement policy enhances accessibility and facilitates uptake via medical channels, reinforcing organized eye-care adoption among younger populations.

Switzerland Contact Lenses and Solutions Market ChallengeHigher Cost Compared to Spectacles Limiting Broader Adoption

Cost sensitivity is a structural constraint despite the continued demand. The Swiss Federal Statistical Office (FSO, 2025) notes that the healthcare spending per capita in Switzerland is one of the highest in Europe, which supports the end-user discretionary spending in health-related matters. Compared to spectacles, contact lenses tend to be more costly in the long run, particularly in daily disposable models, which restricts their usage to active or lifestyle users.

In addition, the increased price sensitivity forces end users to move to private-label substitutes and subscriptions. Although Switzerland has a high purchasing power, value-sensitive behaviour still exists. The cost difference between spectacles and contact lenses still affects the end-user choice, which poses as a structural impediment to quicker penetration in all age groups.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Switzerland Contact Lenses and Solutions Market TrendInsurance-Backed Myopia Management Gaining Traction

There is a significant change in the systematic use of myopia management. Since the addition of myopia-control products to the MiGeL aid list (Federal Office of Public Health) in Switzerland, both orthokeratology and myopia-control lenses receive annual reimbursement of up to CHF 850 (USD 1100.75) to eligible youth. This policy enhances vision correction clinical pathways.

Early ocular-care interventions are further supported by the growing screen exposure of children and adolescents, as well as by the growing parental awareness. Optician and ophthalmologist professional endorsements are also used to encourage a shift in reactive correction to proactive management of myopia, which is a wider healthcare-based trend in corrective vision practice.

Switzerland Contact Lenses and Solutions Market OpportunityTechnological Advancements in Diagnostic and Lens Materials

The healthcare system in Switzerland is still adopting digital innovation. The Federal Office of Public Health (2025) states that digital health technologies and AI-assisted diagnostics are growing in clinical environments. Retinal screening tools that are AI-based enhance the early detection of glaucoma and retinal disorders, which indirectly facilitates more accurate prescription pathways.

At the same time, silicone-hydrogel materials are improving oxygen permeability and comfort, and consumers are becoming more focused on UV protection and breathable formulations. These innovation-based enhancements reinforce the long-term product relevance and are in line with the Swiss standards of high quality of healthcare and adoption of medical technologies.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Switzerland Contact Lenses and Solutions Market Segmentation Analysis

By Product Type

- Contact Lenses

- Contact Lens Solutions

The segment that has the highest share under the product type is contact lenses, which holds 80% market share. Contact lenses dominate due to their convenience, flexibility during sports such as skiing, and compatibility with hybrid work and active lifestyles. Swiss end users increasingly favour daily disposable and silicone hydrogel lenses for hygiene and enhanced oxygen permeability.

While solutions remain essential for lens maintenance, the primary value contribution lies within lens products themselves. Ongoing improvements in material technology and UV protection features reinforce the strong positioning of contact lenses within the overall product structure.

By Sales Channel

- Retail Offline

- Retail Online

The segment that has the highest share under the sales channel is retail offline, which holds 70% market share. Optical goods stores remain the primary purchasing channel due to professional eye examinations, prescription validation, and fitting requirements.

Swiss end users demonstrate high trust in opticians for personalised recommendations, especially for multifocal and myopia control lenses. Although online subscription models are expanding, physical retail continues to dominate due to clinical reliability and structured healthcare reimbursement processes linked to professional consultation.

List of Companies Covered in Switzerland Contact Lenses and Solutions Market

The companies listed below are highly influential in the Switzerland contact lenses and solutions market, with a significant market share and a strong impact on industry developments.

- Prolens AG

- Swisslens SA

- Wöhlk Contactlinsen GmbH

- Johnson & Johnson AG

- Alcon Switzerland AG

- Bausch & Lomb Swiss AG

- Visilab SA

- CooperVision GmbH

Competitive Landscape

The competitive landscape in Switzerland remains concentrated, with Johnson & Johnson AG leading at 30% share in 2025, supported by its strong Acuvue portfolio, including Moist, Oasys, and Vita. The brand maintains high recognition among consumers and opticians, driven by comfort-focused innovation and broad prescription coverage across astigmatism and presbyopia segments. Alcon Switzerland AG follows with an 18.4% share, leveraging its Dailies and Total lines, particularly in silicone hydrogel and oxygen-permeable lenses. Competition is intensifying as private label ranges expand through major optical retailers, offering comparable quality at more competitive price points. Innovation remains centred on multifocal design, moisture retention, and myopia control solutions, while insurance reimbursement under the MiGeL list reshapes purchasing pathways toward medical channels. Overall, strong brand equity, optician partnerships, and incremental product innovation continue to define competitive positioning in 2025.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Switzerland Contact Lenses and Solution Market Policies, Regulations, and Standards

- Switzerland Contact Lenses and Solution Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Switzerland Contact Lenses and Solution Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold in Thousand Units

- Market Segmentation & Growth Outlook

- By Product Type

- Contact Lenses- Market Insights and Forecast 2022-2032, USD Million

- Standard Vision Correction Lenses- Market Insights and Forecast 2022-2032, USD Million

- Myopia Control Lenses- Market Insights and Forecast 2022-2032, USD Million

- Contact Lens Solutions- Market Insights and Forecast 2022-2032, USD Million

- Contact Lenses- Market Insights and Forecast 2022-2032, USD Million

- By Usage

- Contact Lenses- Market Insights and Forecast 2022-2032, USD Million

- Daily Disposable- Market Insights and Forecast 2022-2032, USD Million

- Bi-Weekly- Market Insights and Forecast 2022-2032, USD Million

- Monthly- Market Insights and Forecast 2022-2032, USD Million

- Quarterly/Annual- Market Insights and Forecast 2022-2032, USD Million

- Contact Lens Solutions- Market Insights and Forecast 2022-2032, USD Million

- Daily-Use Care Solutions- Market Insights and Forecast 2022-2032, USD Million

- Weekly/Periodic Deep-Clean Systems- Market Insights and Forecast 2022-2032, USD Million

- Travel/Mini Packs- Market Insights and Forecast 2022-2032, USD Million

- Contact Lenses- Market Insights and Forecast 2022-2032, USD Million

- By Material Type

- Contact Lenses- Market Insights and Forecast 2022-2032, USD Million

- Silicone Hydrogel- Market Insights and Forecast 2022-2032, USD Million

- Hydrogel (Soft)- Market Insights and Forecast 2022-2032, USD Million

- Rigid Gas Permeable (RGP)- Market Insights and Forecast 2022-2032, USD Million

- Hybrid/Scleral/Specialty- Market Insights and Forecast 2022-2032, USD Million

- Contact Lens Solutions- Market Insights and Forecast 2022-2032, USD Million

- Multi-Purpose Solutions- Market Insights and Forecast 2022-2032, USD Million

- Hydrogen Peroxide Systems- Market Insights and Forecast 2022-2032, USD Million

- Saline Solutions- Market Insights and Forecast 2022-2032, USD Million

- Enzymatic & Specialty Cleaners- Market Insights and Forecast 2022-2032, USD Million

- Contact Lenses- Market Insights and Forecast 2022-2032, USD Million

- By Application

- Contact Lenses- Market Insights and Forecast 2022-2032, USD Million

- Spherical (Myopia/Hyperopia)- Market Insights and Forecast 2022-2032, USD Million

- Toric (Astigmatism)- Market Insights and Forecast 2022-2032, USD Million

- Multifocal (Presbyopia)- Market Insights and Forecast 2022-2032, USD Million

- Myopia Control- Market Insights and Forecast 2022-2032, USD Million

- Cosmetic/Colored- Market Insights and Forecast 2022-2032, USD Million

- Therapeutic/Medical- Market Insights and Forecast 2022-2032, USD Million

- Contact Lens Solutions- Market Insights and Forecast 2022-2032, USD Million

- Soft Lens Care- Market Insights and Forecast 2022-2032, USD Million

- RGP Lens Care- Market Insights and Forecast 2022-2032, USD Million

- Sensitive Eye/Preservative-Free Care- Market Insights and Forecast 2022-2032, USD Million

- Contact Lenses- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- Optical Stores- Market Insights and Forecast 2022-2032, USD Million

- Hospitals & Clinics- Market Insights and Forecast 2022-2032, USD Million

- Others (Pharmacies, Beauty Centres, etc.)- Market Insights and Forecast 2022-2032, USD Million

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- Company-owned Portals- Market Insights and Forecast 2022-2032, USD Million

- E-commerce Platforms- Market Insights and Forecast 2022-2032, USD Million

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- By Pack Size

- Contact Lenses- Market Insights and Forecast 2022-2032, USD Million

- Trial Packs- Market Insights and Forecast 2022-2032, USD Million

- Standard Packs- Market Insights and Forecast 2022-2032, USD Million

- Bulk/Value Packs- Market Insights and Forecast 2022-2032, USD Million

- Contact Lens Solutions- Market Insights and Forecast 2022-2032, USD Million

- Up to 120 mL- Market Insights and Forecast 2022-2032, USD Million

- 121–360 mL- Market Insights and Forecast 2022-2032, USD Million

- Above 360 mL- Market Insights and Forecast 2022-2032, USD Million

- Combo/Twin Packs- Market Insights and Forecast 2022-2032, USD Million

- Contact Lenses- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Product Type

- Market Size & Growth Outlook

- Switzerland Contact Lenses Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold in Thousand Units

- Market Segmentation & Growth Outlook

- By Usage- Market Insights and Forecast 2022-2032, USD Million

- By Material Type- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Pack Size- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Switzerland Contact Lens Solutions Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold in Thousand Units

- Market Segmentation & Growth Outlook

- By Usage- Market Insights and Forecast 2022-2032, USD Million

- By Material Type- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Pack Size- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Johnson & Johnson AG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Alcon Switzerland AG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Bausch & Lomb Swiss AG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Visilab SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- CooperVision GmbH

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Prolens AG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Swisslens SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Wöhlk Contactlinsen GmbH

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Mc Optik AG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Johnson & Johnson AG

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Usage |

|

| By Material Type |

|

| By Application |

|

| By Sales Channel |

|

| By Pack Size |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.