Spain Digestive Remedies Market Report: Trends, Growth and Forecast (2026-2032)

By Product Type (Paediatric Digestive Remedies (Paediatric Diarrhoeal Remedies, Paediatric Indigestion & Heartburn Remedies, Paediatric Laxatives, Paediatric Motion Sickness Remedies), Diarrhoeal Remedies, IBS Treatments, Indigestion & Heartburn Remedies (Antacids, Antiflatulents, Digestive Enzymes, H2 Blockers, Proton Pump Inhibitors), Laxatives, Motion Sickness Remedies), By Age Group (Children & Adolescents (01-17 years), Adults (18-65 years), Geriatric (65+ years)), By Sales Channel (Retail Online, Retail Offline (Hospitals, Clinics, Pharmacies)) ... Read more

|

Major Players

|

Spain Digestive Remedies Market Statistics and Insights, 2026

- Market Size Statistics

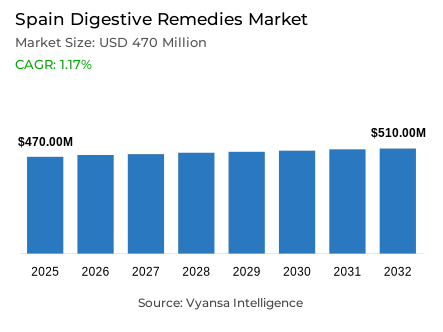

- Digestive remedies market size in Spain was valued at USD 470 million in 2025 and is estimated at USD 487 Million in 2026.

- The market size is expected to grow to USD 510 million by 2032.

- Market to register a CAGR of around 1.17% during 2026-32.

- Product Type Shares

- Laxatives grabbed market share of 52%.

- Competition

- More than 10 companies are actively engaged in producing digestive remedies in Spain.

- Top 5 companies acquired around 40% of the market share.

- Haleon Spain SA, Bayer Hispania SL, Reckitt Benckiser Espana SL, Almirall SA, Johnson & Johnson SA etc., are few of the top companies.

- Sales Channel

- Retail offline grabbed 80% of the market.

Spain Digestive Remedies Market Outlook

Spain digestive remedies market size was valued at USD 470 million in 2025 and is projected to grow from USD 487 million in 2026 to USD 510 million by 2032, exhibiting a CAGR of 1.17% during the forecast period. Growth remains supported by stronger consumer focus on self-care, preventive health, and daily wellbeing, while sales in 2025 already show slight improvement over 2023 as awareness around digestive health continues to rise.

Consumer education around gut health, immunity, mood, and overall comfort continues to shape buying habits. Social media discussions on microbiota, intestinal balance, and preventive care keep these topics visible, while many people increasingly look for products that help manage constipation, reflux, indigestion, and mild digestive discomfort. This keeps digestive remedies relevant as part of routine health management rather than only occasional symptom relief.

Category development is also influenced by changing product preferences. Probiotics, prebiotics, and herbal options are attracting more attention, especially among consumers seeking natural and preventive solutions for bloating, constipation, and mild digestive imbalance. At the same time, digestive remedies continue to hold an important place in household purchases, with Laxatives accounting for 52% of the market, supported by frequent constipation concerns and growing interest in regular digestive support.

Travel and pharmacy-led shopping further support category stability. High tourist movement and domestic trips increase purchase occasions for products used for diarrhoea, indigestion, constipation, and reflux during travel. Retail structure also remains highly important, with Retail Offline holding 80% of the market, as consumers still prefer pharmacies and physical stores for quick access, pharmacist advice, and trusted purchase decisions around digestive remedies.

Spain Digestive Remedies Market Growth DriverGut-Health Awareness Strengthens Everyday Self-Care

People in Spain are continuously learning about their own digestion and the products that are used to support it, which is positively influencing the sale of digestive remedies in this country. Consumers in Spain increasingly link gut health with other aspects of wellbeing, such as immunity, mood, and day-to-day comfort, and this continued education has resulted in the continual relevance of stomach-related products such as those that help with constipation, reflux, indigestion, and mild digestive discomfort. The trend, especially as self-care becomes a bigger reason to make purchases, is towards increased awareness of gut health; through discussions on social media regarding microbiota, intestinal balance and preventative measures, gut health is being given more exposure and consideration amongst consumers when making routine wellness decisions.

This focus on health is being reinforced by Spain’s overall engagement within the healthcare system. According to the Barómetro Sanitario, among those surveyed, 79.2% of people consulted with a public doctor in the past year and that 18.2% had to consult a healthcare provider because of a mental health issue. There is evidence to suggest that by being more involved in their own personal health, people will be more likely to place a greater level of focus on managing their gut health and implementing preventative measures for digestive care.

Spain Digestive Remedies Market ChallengeProbiotics and Alternatives Put Pressure on Traditional OTC Remedies

Increased demand of probiotics, prebiotics and herbal digestive products puts pressure on conventional digestive remedies in Spain. Consumers are increasingly demanding preventive and natural remedies to mild diarrhoea, constipation, bloating, and microbiota-related discomfort, as opposed to the traditional over-the-counter symptom management. This change undermines the impetus of traditional digestive remedies, particularly in situations where probiotics are viewed as milder and more consistent with long-term gut homeostasis.

Competitive pressure is strengthened by easy access. According to Spain’s 2025 ICT household survey, 59.6% of individuals aged sixteen to seventy‑four made an online purchase in the preceding three months, and 56.7% bought physical products online. At the same time, AESAN documents that food supplements are offered in capsules, tablets, pills, powder sachets, liquid ampoules, and similar dosage forms, which makes them convenient alternatives in the context of preventive digestive care.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Spain Digestive Remedies Market TrendPreventive and Natural Gut Care Gains Stronger Visibility

In Spain, there's an increasing number of people that are choosing preventive digestive therapies such as probiotics, prebiotics and herbal remedies as natural alternatives. Consumers are becoming more aware of their own microbiomes, SIBO phenomena, preventative measures against being constipated and how they may have a mild emotional imbalance due to their diet and digestive health. Therefore, consumers are also looking for products that fit into their existing daily routines of health & wellness; this includes the use of herbal remedies and phytotherapeutics as digestive aids, since consumers prefer these forms over traditional medicine which tends to just relieve symptoms.

The spread of this trend is boosted by digital reach. National Statistics Institute (INE) reports that in 2025, 96.3% of individuals aged sixteen to seventy‑four used the internet in the prior three months, 92.5% used it daily, and 66.5% possessed basic or advanced digital skills. This broad online coverage makes it easy to access digestive-health content, influencer advice, and wellness education, thus increasing the desire to use natural and preventive digestive products.

Spain Digestive Remedies Market OpportunityTourism-Linked Purchases Expand Consumption Occasions

Travel is an obvious opportunity to digestive remedies in Spain, with inbound tourists and domestic travelers often carrying or buying products to treat constipation, diarrhoea, indigestion and reflux during travel. The intensive tourist traffic in Spain, combined with the growing popularity of gastronomy and wine-related tourism, increases the risk of exposure to unhealthy eating habits, high-calorie food, and related digestive discomfort. These aspects expand the buying events beyond the daily domestic consumption and justify the stocking of digestive products in pharmacies and other retailers.

The scale of travel in Spain supports this opportunity. According to INE, Spain received more than 55.5 million foreign tourists during the first seven months of 2025, and Spanish residents made 46.4 million trips in the second quarter of 2025 alone. This traveller movement contributes to the constant demand of convenient digestive support products before, during, and after excursions.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Spain Digestive Remedies Market Segmentation Analysis

By Product Type

- Paediatric Digestive Remedies

- Paediatric Diarrhoeal Remedies

- Paediatric Indigestion & Heartburn Remedies

- Paediatric Laxatives

- Paediatric Motion Sickness Remedies

- Diarrhoeal Remedies

- IBS Treatments

- Indigestion & Heartburn Remedies

- Antacids

- Antiflatulents

- Digestive Enzymes

- H2 Blockers

- Proton Pump Inhibitors

- Laxatives

- Motion Sickness Remedies

Within the product type segment, laxatives command the largest share, representing 52% of the market. This leadership persists since constipation is one of the most frequent complaints of the digestive tract in Spain. The everyday eating habits, preventive purchasing behaviour and the growing consumer preference towards products that assist in keeping the bowel movements regular instead of treating them once the discomfort sets in, all reinforce the demand.

Laxatives also have the advantage of increased interest in digestive prevention in Spain. Consumers are also demanding more herbal and traditional products that can be used on a regular basis and in a natural manner, which fits well with the high standing of this segment. As a result, laxatives remain the most popular products, backed by the urgent need to relieve and the regular preventive gut-health practices.

By Sales Channel

- Retail Online

- Retail Offline

- Hospitals

- Clinics

- Pharmacies

In the sales channel segment, retail offline holds an 80% market share, representing the highest concentration. This dominance is maintained due to the fact that digestive remedies are often bought to provide immediate relief and Spanish consumers still prefer to use pharmacies and physical stores to get easy access, pharmacist guidance and reliable product choice. Repeat buying patterns in the digestive care category also fit offline purchases, with familiarity and convenience playing a major role in decision making.

The pharmacy access system in Spain supports the strength of this channel. In the 2024 Barómetro Sanitario, 56.9% of respondents report awareness that medicines can be collected at any pharmacy nationwide, and 60.0% indicate possession of an electronic certificate linked to that access framework. These results highlight the significance of pharmacy-based buying and support the importance of offline retail to the sales of digestive remedies.

List of Companies Covered in Spain Digestive Remedies Market

The companies listed below are highly influential in the Spain digestive remedies market, with a significant market share and a strong impact on industry developments.

- Haleon Spain SA

- Bayer Hispania SL

- Reckitt Benckiser Espana SL

- Almirall SA

- Johnson & Johnson SA

- Uriach-Aquilea OTC SL

- Sanofi-Aventis Espana SA

- Viatris Inc

- Faes Farma SA

- Laboratorios Estevi SL

Competitive Landscape

The competitive landscape of digestive remedies in Spain remains fragmented, with strong competition between traditional OTC products and rapidly growing probiotic and herbal alternatives. Almirall SA leads the category through its flagship brand Almax, which holds a clear advantage in indigestion and heartburn remedies due to its relatively affordable pricing compared to Gaviscon by Reckitt Benckiser España SL. However, competition is intensifying as players such as Prodeco Pharma expand their probiotic portfolios, while Faes Farma SA innovates with products like Arcid. Additionally, Schwabe Farma Ibérica is strengthening its position in herbal remedies with offerings such as Gastropan. Overall, competitive dynamics are shifting away from purely symptom-relief products toward preventive, natural, and microbiome-focused solutions.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Spain Digestive Remedies Market Policies, Regulations, and Standards

- Spain Digestive Remedies Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Spain Digestive Remedies Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product Type

- Paediatric Digestive Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Diarrhoeal Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Indigestion & Heartburn Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Laxatives- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Motion Sickness Remedies- Market Insights and Forecast 2022-2032, USD Million

- Diarrhoeal Remedies- Market Insights and Forecast 2022-2032, USD Million

- IBS Treatments- Market Insights and Forecast 2022-2032, USD Million

- Indigestion & Heartburn Remedies- Market Insights and Forecast 2022-2032, USD Million

- Antacids- Market Insights and Forecast 2022-2032, USD Million

- Antiflatulents- Market Insights and Forecast 2022-2032, USD Million

- Digestive Enzymes- Market Insights and Forecast 2022-2032, USD Million

- H2 Blockers- Market Insights and Forecast 2022-2032, USD Million

- Proton Pump Inhibitors- Market Insights and Forecast 2022-2032, USD Million

- Laxatives- Market Insights and Forecast 2022-2032, USD Million

- Motion Sickness Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Digestive Remedies- Market Insights and Forecast 2022-2032, USD Million

- By Age Group

- Children & Adolescents (01-17 years)- Market Insights and Forecast 2022-2032, USD Million

- Adults (18-65 years)- Market Insights and Forecast 2022-2032, USD Million

- Geriatric (65+ years)- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- Hospitals- Market Insights and Forecast 2022-2032, USD Million

- Clinics- Market Insights and Forecast 2022-2032, USD Million

- Pharmacies- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Product Type

- Market Size & Growth Outlook

- Spain Paediatric Digestive Remedies Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Spain Diarrhoeal Remedies Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Spain IBS Treatments Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Spain Indigestion & Heartburn Remedies Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Spain Laxatives Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Spain Motion Sickness Remedies Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Almirall SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Johnson & Johnson SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Uriach-Aquilea OTC SL

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Sanofi-Aventis Espana SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Viatris Inc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Haleon Spain SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Bayer Hispania SL

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Reckitt Benckiser Espana SL

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Faes Farma SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Laboratorios Estevi SL

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Almirall SA

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Age Group |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.