Spain Contact Lenses and Solutions Market Report: Trends, Growth and Forecast (2026-2032)

By Product Type (Contact Lenses (Standard Vision Correction Lenses, Myopia Control Lenses), Contact Lens Solutions), By Usage (Contact Lenses (Daily Disposable, Bi-Weekly, Monthly, Quarterly/Annual), Contact Lens Solutions (Daily-Use Care Solutions, Weekly/Periodic Deep-Clean Systems, Travel/Mini Packs)), By Material Type (Contact Lenses (Silicone Hydrogel, Hydrogel (Soft), Rigid Gas Permeable (RGP), Hybrid/Scleral/Specialty), Contact Lens Solutions (Multi-Purpose Solutions, Hydrogen Peroxide Systems, Saline Solutions, Enzymatic & Specialty Cleaners)), By Application (Contact Lenses (Spherical (Myopia/Hyperopia), Toric (Astigmatism), Multifocal (Presbyopia), Myopia Control, Cosmetic/Colored, Therapeutic/Medical), Contact Lens Solutions (Soft Lens Care, RGP Lens Care, Sensitive Eye/Preservative-Free Care)), By Sales Channel (Retail Offline (Optical Stores, Hospitals & Clinics, Others (Pharmacies, Beauty Centres, etc.)), Retail Online (Company-owned Portals, E-commerce Platforms)), By Pack Size (Contact Lenses (Trial Packs, Standard Packs, Bulk/Value Packs), Contact Lens Solutions (Up to 120 mL, 121–360 mL, Above 360 mL, Combo/Twin Packs)) ... Read more

|

Major Players

|

Spain Contact Lenses and Solutions Market Statistics and Insights, 2026

- Market Size Statistics

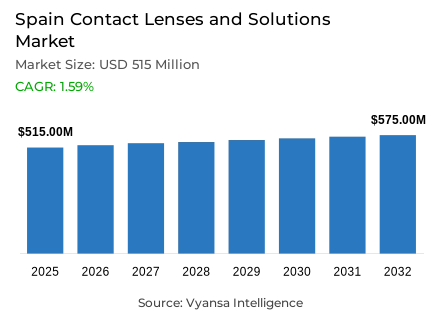

- Contact lenses and solutions market size in Spain was estimated at USD 515 million in 2025.

- The market size is expected to grow to USD 575 million by 2032.

- Market to register a CAGR of around 1.59% during 2026-32.

- Product Type Shares

- Contact lenses grabbed market share of 90%.

- Competition

- More than 5 companies are actively engaged in producing contact lenses and solutions in Spain.

- Top 5 companies acquired around 60% of the market share.

- Bausch & Lomb Espana SA, Alcon Healthcare SA, Conoptica SL, CooperVision Iberia SL, Johnson & Johnson SA etc., are few of the top companies.

- Sales Channel

- Retail offline grabbed 80% of the market.

Spain Contact Lenses and Solutions Market Outlook

Spain contact lenses and solutions market is valued at USD 515 million in 2025 and is projected to reach USD 575 million by 2032, registering a CAGR of around 1.59% during 2026-32. Growth remains moderate and is primarily supported by rising myopia among teenagers. According to Journal of Clinical Medicine (MDPI) , approximately 19% of younger children aged 5-7 years suffer from myopia, sustaining demand for corrective eyewear.

Contact lenses and solutions remain important for long-term vision management among young consumers. However, adoption remains structurally limited, as FEDAO (2025) reports that while over 80% of the population requires vision correction, only 5% use contact lenses. Public health support strengthens accessibility.

In 2025, the Spanish Ministry of Health allocated EUR 43 million to support the financing of eye care products for lower-income families, making it easier to overcome affordability issues. At the same time, increased awareness about myopia control systems is also triggering a shift in consumer preferences toward preventive eye management solutions.

By product type, contact lenses currently command 90% market share, driven by consumer preference for convenience and compatibility with spectacles. By sales channel, retail offline currently contributes 80% to overall distribution, driven by professional eye care and optometrist recommendations.

Spain Contact Lenses and Solutions Market Growth DriverRising Myopia Prevalence Among Teenagers

Spain is experiencing a rising number of vision impairments among the younger generations, directly contributing to the demand for vision correction. As reported by the Journal of Clinical Medicine (MDPI), 19% of younger children aged 5-7 years suffer from myopia. This is a direct result of the rising screen usage and digital lifestyles, making the demand for vision correction even more imperative.

The rising awareness among parents about the importance of eye health management in children continues to drive the demand for myopia control. Since children and teenagers need vision correction for an extended period, contact lenses continue to benefit from this trend. The rising number of vision impairments among the Spanish population creates a consistent base demand, especially for daily disposable lenses and myopia control lenses.

Spain Contact Lenses and Solutions Market ChallengeLow Penetration of Contact Lens Usage

Although there is a massive demand for vision correction, the penetration rate remains low. According to FEDAO (Spanish Federation of Optical Sector Associations, 2025), “More than 80% of the Spanish population needs vision correction, but only 5% wear contact lenses.”

Consumer sentiment regarding discomfort, dry eye, and unwillingness to touch the eyes will continue to act as a deterrent for new users. Moreover, economic prudence also impacts spending, as people tend to favor spectacles over contact lenses. Such behavioral and perception-driven factors act as a deterrent to wider penetration, making it a challenge to accelerate the category.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Spain Contact Lenses and Solutions Market TrendGrowing Adoption of Myopia Control Solutions

Myopia control systems are also gaining popularity as awareness among families increases. Consejo General de Colegios de Opticos-Optometristas (CGCOO) also verifies that the prevalence of myopia among teenagers is high, triggering interest in preventive and corrective measures beyond spectacles. Optical stores are also promoting myopia management products as part of eye care programs.

This shift reflects a broader trend toward proactive eye health management. Myopia control lenses are progressively replacing older orthokeratology approaches in many optical stores due to easier handling and lower complexity. The evolution of these solutions indicates a gradual transformation in corrective eyewear preferences across younger age groups.

Spain Contact Lenses and Solutions Market OpportunityGovernment Support for Eye Care Accessibility

Public health initiatives create potential support for category expansion. In 2025, the Spanish Ministry of Health allocated EUR 43 million to finance eye care products, aiming to improve access for lower-income households.

Such measures enhance affordability and may reduce financial barriers to vision correction. Increased institutional backing for eye health strengthens awareness and accessibility, particularly among underserved populations. This policy-level support provides an opportunity to broaden usage of corrective solutions within Spain’s evolving healthcare framework.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Spain Contact Lenses and Solutions Market Segmentation Analysis

By Product Type

- Contact Lenses

- Contact Lens Solutions

The segment that has the highest share under the product type is contact lenses, which holds 90% market share. Contact lenses dominate due to their convenience and compatibility with dual usage alongside spectacles. Many end users prefer daily disposable formats for occasional wear, especially when combining lenses with glasses.

While solutions remain essential for maintenance, the primary value contribution lies within lens products. The strong presence of daily disposable and myopia control lenses reinforces the leading position of contact lenses in the overall product structure.

By Sales Channel

- Retail Offline

- Retail Online

The segment that has the highest share under the sales channel is retail offline, which holds 80% market share. Optical goods stores remain the dominant channel due to professional eye examinations and prescription validation requirements.

End users in Spain continue to rely heavily on optometrists for product recommendations and fitting services. Although price comparison via e-commerce is increasing, physical retail maintains leadership due to clinical trust and personalised consultation in vision care purchasing decisions.

List of Companies Covered in Spain Contact Lenses and Solutions Market

The companies listed below are highly influential in the Spain contact lenses and solutions market, with a significant market share and a strong impact on industry developments.

- Bausch & Lomb Espana SA

- Alcon Healthcare SA

- Conoptica SL

- CooperVision Iberia SL

- Johnson & Johnson SA

- Menicon Iberia SL

Competitive Landscape

The competitive landscape in Spain’s contact lenses and solutions category remains concentrated, with CooperVision Iberia SL and Johnson & Johnson SA jointly leading at 17.3% value share each. In 2024, CooperVision Iberia overtook Johnson & Johnson to become the leading player, supported by strong performances from brands such as MiSight 1 Day, Biofinity, and Proclear. MiSight 1 Day remains particularly strong within the fast-growing myopia control segment, reinforcing CooperVision’s positioning in specialised vision care. Despite the strength of multinational brands, private label holds a larger share than any individual company, benefiting from Spain’s price-sensitive environment. Opticians increasingly recommend competitively priced private label options to retain customers and limit migration to e-commerce. Additionally, retailers and online specialists such as Farmaoptics and E-lentillas are expanding their own branded ranges, further intensifying competition and strengthening private label influence within the category.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Spain Contact Lenses and Solution Market Policies, Regulations, and Standards

- Spain Contact Lenses and Solution Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Spain Contact Lenses and Solution Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold in Thousand Units

- Market Segmentation & Growth Outlook

- By Product Type

- Contact Lenses- Market Insights and Forecast 2022-2032, USD Million

- Standard Vision Correction Lenses- Market Insights and Forecast 2022-2032, USD Million

- Myopia Control Lenses- Market Insights and Forecast 2022-2032, USD Million

- Contact Lens Solutions- Market Insights and Forecast 2022-2032, USD Million

- Contact Lenses- Market Insights and Forecast 2022-2032, USD Million

- By Usage

- Contact Lenses- Market Insights and Forecast 2022-2032, USD Million

- Daily Disposable- Market Insights and Forecast 2022-2032, USD Million

- Bi-Weekly- Market Insights and Forecast 2022-2032, USD Million

- Monthly- Market Insights and Forecast 2022-2032, USD Million

- Quarterly/Annual- Market Insights and Forecast 2022-2032, USD Million

- Contact Lens Solutions- Market Insights and Forecast 2022-2032, USD Million

- Daily-Use Care Solutions- Market Insights and Forecast 2022-2032, USD Million

- Weekly/Periodic Deep-Clean Systems- Market Insights and Forecast 2022-2032, USD Million

- Travel/Mini Packs- Market Insights and Forecast 2022-2032, USD Million

- Contact Lenses- Market Insights and Forecast 2022-2032, USD Million

- By Material Type

- Contact Lenses- Market Insights and Forecast 2022-2032, USD Million

- Silicone Hydrogel- Market Insights and Forecast 2022-2032, USD Million

- Hydrogel (Soft)- Market Insights and Forecast 2022-2032, USD Million

- Rigid Gas Permeable (RGP)- Market Insights and Forecast 2022-2032, USD Million

- Hybrid/Scleral/Specialty- Market Insights and Forecast 2022-2032, USD Million

- Contact Lens Solutions- Market Insights and Forecast 2022-2032, USD Million

- Multi-Purpose Solutions- Market Insights and Forecast 2022-2032, USD Million

- Hydrogen Peroxide Systems- Market Insights and Forecast 2022-2032, USD Million

- Saline Solutions- Market Insights and Forecast 2022-2032, USD Million

- Enzymatic & Specialty Cleaners- Market Insights and Forecast 2022-2032, USD Million

- Contact Lenses- Market Insights and Forecast 2022-2032, USD Million

- By Application

- Contact Lenses- Market Insights and Forecast 2022-2032, USD Million

- Spherical (Myopia/Hyperopia)- Market Insights and Forecast 2022-2032, USD Million

- Toric (Astigmatism)- Market Insights and Forecast 2022-2032, USD Million

- Multifocal (Presbyopia)- Market Insights and Forecast 2022-2032, USD Million

- Myopia Control- Market Insights and Forecast 2022-2032, USD Million

- Cosmetic/Colored- Market Insights and Forecast 2022-2032, USD Million

- Therapeutic/Medical- Market Insights and Forecast 2022-2032, USD Million

- Contact Lens Solutions- Market Insights and Forecast 2022-2032, USD Million

- Soft Lens Care- Market Insights and Forecast 2022-2032, USD Million

- RGP Lens Care- Market Insights and Forecast 2022-2032, USD Million

- Sensitive Eye/Preservative-Free Care- Market Insights and Forecast 2022-2032, USD Million

- Contact Lenses- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- Optical Stores- Market Insights and Forecast 2022-2032, USD Million

- Hospitals & Clinics- Market Insights and Forecast 2022-2032, USD Million

- Others (Pharmacies, Beauty Centres, etc.)- Market Insights and Forecast 2022-2032, USD Million

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- Company-owned Portals- Market Insights and Forecast 2022-2032, USD Million

- E-commerce Platforms- Market Insights and Forecast 2022-2032, USD Million

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- By Pack Size

- Contact Lenses- Market Insights and Forecast 2022-2032, USD Million

- Trial Packs- Market Insights and Forecast 2022-2032, USD Million

- Standard Packs- Market Insights and Forecast 2022-2032, USD Million

- Bulk/Value Packs- Market Insights and Forecast 2022-2032, USD Million

- Contact Lens Solutions- Market Insights and Forecast 2022-2032, USD Million

- Up to 120 mL- Market Insights and Forecast 2022-2032, USD Million

- 121–360 mL- Market Insights and Forecast 2022-2032, USD Million

- Above 360 mL- Market Insights and Forecast 2022-2032, USD Million

- Combo/Twin Packs- Market Insights and Forecast 2022-2032, USD Million

- Contact Lenses- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Product Type

- Market Size & Growth Outlook

- Spain Contact Lenses Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold in Thousand Units

- Market Segmentation & Growth Outlook

- By Usage- Market Insights and Forecast 2022-2032, USD Million

- By Material Type- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Pack Size- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Spain Contact Lens Solutions Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold in Thousand Units

- Market Segmentation & Growth Outlook

- By Usage- Market Insights and Forecast 2022-2032, USD Million

- By Material Type- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Pack Size- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- CooperVision Iberia SL

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Johnson & Johnson SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Bausch & Lomb España SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Alcon Healthcare SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Conóptica SL

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Menicon Iberia SL

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Alcon Cusí SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- CooperVision Iberia SL

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Usage |

|

| By Material Type |

|

| By Application |

|

| By Sales Channel |

|

| By Pack Size |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.