Southeast Asia Clinical Laboratory Services Market Report: Trends, Growth and Forecast (2026-2032)

By Test Type (Clinical Chemistry (Routine Chemistry Testing, Therapeutic Drug Monitoring Testing, Endocrinology Chemistry Testing, Specialized Chemistry Testing, Other Clinical Chemistry Testing), Hematology Testing, Medical Microbiology (Infectious Disease Testing, Transplant Diagnostic Testing, Other Microbiology Testing), Immunology & Serology Testing, Molecular Diagnostics, Genetic Testing, Pathology (Cytopathology, Histopathology), Blood Banking & Transfusion Services, Toxicology & Drug Abuse Testing, Other Specialty/Esoteric Tests), By Service Provider (Hospital-based Laboratories, Independent/Standalone Clinical Laboratories, Clinic/Physician Office Laboratories, Public Health Laboratories, Specialty Laboratories), By Application (Routine Diagnostic Testing, Chronic Disease Testing, Infectious Disease Testing, Oncology Testing, Preventive/Screening Testing, Specialized/Genetic Testing), By Country (Indonesia, Thailand, Vietnam, Malaysia, Philippines, Singapore) ... Read more

|

Major Players

|

Southeast Asia Clinical Laboratory Services Market Statistics and Insights, 2026

- Market Size Statistics

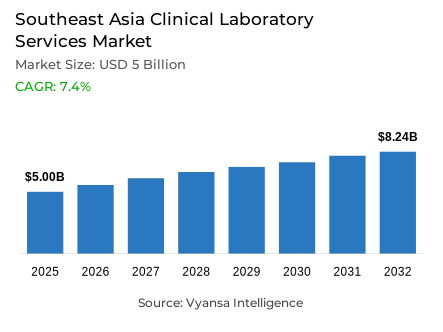

- Clinical laboratory services market size in Southeast Asia was valued at USD 5 billion in 2025 and is estimated at USD 5.37 billion in 2026.

- The market size is expected to grow to USD 8.24 billion by 2032.

- Market to register a CAGR of around 7.4% during 2026-32.

- Test Type Shares

- Clinical chemistry grabbed market share of 25%.

- Competition

- More than 10 companies are actively engaged in producing clinical laboratory services in Southeast Asia.

- Top 5 companies acquired around 10% of the market share.

- Raffles Diagnostica Laboratory, Parkway Laboratory Services, IHH Laboratories, Pathology Asia, Innoquest Diagnostics etc., are few of the top companies.

- Service Provider

- Hospital-based Laboratories grabbed 40% of the market.

- Country

- Indonesia leads with a 30% share of the Southeast Asia market.

Southeast Asia Clinical Laboratory Services Market Outlook

The Southeast Asia clinical laboratory services market was valued at USD 5 billion in 2025, establishing a commercially active and institutionally well-supported foundation within one of the world's most rapidly evolving regional healthcare diagnostics ecosystems. Projected to advance from USD 5.37 billion in 2026 to USD 8.24 billion by 2032, the sector registers a CAGR of 7.4% across the forecast horizon. This steady and structurally supported expansion trajectory reflects the sustained and intensifying clinical demand for diagnostic testing support across a region confronting a dual burden of noncommunicable and infectious disease, expanding hospital care networks, and progressive national commitments to universal health coverage whose combined institutional force sustains consistent laboratory service procurement investment across diverse healthcare system contexts throughout Southeast Asia.

The test type architecture defining this market's commercial structure is anchored in clinical chemistry testing. Clinical Chemistry commands approximately 25% of total test type market share, reflecting the consistent and broad clinical preference for routine diagnostic testing categories whose high-volume applicability, repeat evaluation frequency, and broad clinical relevance across patient assessment, chronic disease monitoring, and hospital-based care workflows make clinical chemistry the reference test category across the region's most commercially significant laboratory service environments. This test type concentration confirms that Southeast Asian laboratory service buyers and clinical users consistently prioritize well-established, high-throughput diagnostic testing categories whose operational integration and clinical workflow compatibility create natural and durable demand advantages over more specialized or lower-volume test alternatives.

The service provider architecture reinforces the structural centrality of hospital-based laboratories as the category's dominant service delivery platform. Hospital-Based Laboratories command approximately 40% of total service provider market share, reflecting the foundational role of institutional care settings in coordinating diagnostic workflows, physician-laboratory integration, and timely testing access across the region's most clinically active patient management environments. WHO South-East Asia's documentation that noncommunicable diseases account for 55% of all deaths in the region and 9.5 million deaths annually confirms the chronic disease burden that sustains consistent hospital-based diagnostic testing volume across the inpatient, outpatient, and emergency care settings where integrated laboratory service delivery generates its highest utilization rates.

The future outlook is defined by four converging structural forces whose combined commercial impact creates a clinical laboratory services market of sustained and well-grounded expansion momentum. WHO South-East Asia's documentation that the region accounts for approximately 34% of global incident tuberculosis, with a TB incidence rate of 201 per 100,000 population in 2024, confirms the infectious disease burden that sustains consistent clinical laboratory testing demand alongside the region's growing chronic disease diagnostic requirements. The consultative meeting on establishing an ASEAN Laboratory Network, held in Jakarta in September 2025, confirms the regional institutional momentum toward coordinated laboratory capability development that will progressively strengthen the technical and infrastructure foundation of Southeast Asia's clinical laboratory ecosystem. The AIIB-backed USD 4 billion Indonesia health system modernization initiative, encompassing enhancements across approximately 10,000 community health centers and laboratory infrastructure spanning Tiers 2 through 5, creates the most commercially significant country-level expansion opportunity in the regional market. Indonesia's 30% regional market share leadership establishes the national commercial center around which regional competitive strategy and service capacity investment are organized over the forecast period.

Southeast Asia Clinical Laboratory Services Market Growth Driver

Dual Disease Burden Sustains Consistent Clinical Laboratory Testing Demand

The sustained and institutionally documented dual burden of noncommunicable and infectious disease across Southeast Asia represents the primary structural driver of clinical laboratory services demand, functioning as a persistent diagnostic testing imperative that sustains consistent service utilization across patient diagnosis, disease monitoring, treatment response assessment, and population health surveillance programs throughout the region's diverse national healthcare systems. This disease burden-driven demand dynamic transcends healthcare investment cycle fluctuations, reflecting a genuine clinical necessity whose testing volume generation is structurally anchored in the irreducible requirement for accurate and timely diagnostic support across the patient populations confronting the region's most prevalent and most consequential health conditions.

The quantitative evidence validating this disease burden-driven demand dynamic is documented with precision by WHO South-East Asia. Noncommunicable diseases account for 55% of all deaths in the region and 9.5 million deaths annually, confirming the chronic disease management burden that sustains consistent high-volume clinical chemistry, hematology, and biomarker testing demand across hospital-based and ambulatory care laboratory environments throughout Southeast Asia. The region accounts for approximately 34% of global incident tuberculosis, with a TB incidence rate of 201 per 100,000 population in 2024, confirming the infectious disease testing demand that sustains consistent microbiological, molecular, and immunological diagnostic service utilization across the region's public health and clinical laboratory networks. These disease burden metrics validate a clinical testing demand base of sufficient scale and chronicity to sustain structural laboratory services market growth over the forecast period.

Southeast Asia Clinical Laboratory Services Market Challenge

Healthcare Financing Gaps and Uneven Access Constrain Market Development Velocity

The persistent structural gap between healthcare financing needs and available resources across Southeast Asia's most populous national healthcare systems represents the most consequential challenge confronting clinical laboratory services market development, creating systematic access, utilization, and service expansion constraints that moderate adoption velocity and maintain uneven laboratory service penetration across national markets despite the region's consistent underlying diagnostic testing demand. In a healthcare service environment where out-of-pocket expenditure remains the primary financing mechanism for laboratory testing access across significant portions of the regional patient population, the financial barrier to diagnostic service utilization directly constrains the translation of clinical need into active laboratory service procurement, limiting market development velocity in the geographies where disease burden-driven testing demand is most acute.

The structural depth and human impact scale of this healthcare financing challenge are documented with precision by WHO South-East Asia. Over 65 million people in the region are pushed into poverty because of health expenditure, confirming the financial burden severity that constrains diagnostic service access across the region's most economically vulnerable patient populations. The 2025 regional UHC update, tracking all 10 Southeast Asian member states, confirms that critical gaps in universal health coverage still require accelerated action to achieve the 2030 coverage targets that would systematically reduce out-of-pocket laboratory service access barriers across the region. For laboratory service providers, navigating this financing challenge demands strategic service pricing, public-private partnership engagement, and geographic deployment models that extend laboratory access across previously underserved populations while maintaining commercial viability over the forecast period.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Southeast Asia Clinical Laboratory Services Market Trend

Regional Laboratory Network Development Strengthens Diagnostic Infrastructure Connectivity

The progressive institutional momentum toward coordinated regional laboratory network development and advanced diagnostic capability integration across Southeast Asia represents the defining structural trend reshaping the competitive landscape, technical capability requirements, and cross-border collaboration frameworks of the regional clinical laboratory services market. This regional connectivity trend is moving the development conversation in Southeast Asia's laboratory services ecosystem beyond individual national system improvement into the domain of coordinated surveillance capability, shared quality standards, interoperable laboratory information infrastructure, and collective public health emergency preparedness, dimensions that are progressively redefining the technical and institutional standards against which regional laboratory service providers must demonstrate credibility.

The institutional specificity and technical advancement trajectory of this regional connectivity trend are documented with authority across official government and health organization sources. The consultative meeting on establishing an ASEAN Laboratory Network, held in Jakarta from 15 to 17 September 2025, confirms that regional stakeholders representing Southeast Asia's most influential health system authorities are actively working toward structured laboratory capability coordination and diagnostic preparedness integration across national laboratory networks. Indonesia's three national polio laboratories joining a whole genome sequencing workshop from 2 to 11 July 2025 confirms that advanced molecular diagnostic and genomic sequencing capability is being actively integrated into national public health laboratory infrastructure, raising the technical benchmark for regional laboratory capability development. As this regional connectivity momentum translates into shared quality standards and coordinated capability investment, the technical requirements for competitive participation in the region's most significant laboratory service markets will advance progressively over the forecast period.

Southeast Asia Clinical Laboratory Services Market Opportunity

Indonesia's Health System Modernization Creates the Region's Largest Expansion Opening

The AIIB-backed USD 4 billion Indonesia health system modernization initiative represents the Southeast Asia clinical laboratory services market's most commercially significant and institutionally certain growth opportunity, delivering a government-guaranteed infrastructure investment program whose geographic breadth, multi-tier laboratory enhancement scope, and long-horizon implementation commitment create laboratory service capacity expansion demand of a scale and durability that substantially exceeds the organic market growth opportunities available across any other national market in the regional landscape. This Indonesia-centered opportunity is distinguished from conventional private sector healthcare investment demand by its institutional investment certainty, its systematic geographic reach across previously underserved rural and provincial healthcare settings, and the structural demand expansion it creates across every tier of Indonesia's national laboratory service ecosystem.

The quantitative scale and implementation specificity of this Indonesia modernization opportunity are documented with precision by the Asian Infrastructure Investment Bank. The health system modernization initiative is a USD 4 billion effort specifically designed to ensure sustainable delivery of essential health and laboratory services while reducing geographic disparities in care quality and outcomes across Indonesia's diverse national healthcare delivery system. The initiative's scope encompasses Indonesia's three-tier system of approximately 10,000 community health centers and over 3,000 hospitals, with dedicated enhancements to public health laboratories spanning Tiers 2 through 5, confirming the breadth of laboratory infrastructure investment whose implementation will progressively expand laboratory service access, testing capacity, and diagnostic capability across regions that currently remain underserved relative to Indonesia's national healthcare delivery potential. Laboratory service providers that invest in capability alignment, geographic deployment readiness, and partnership frameworks suited to Indonesia's public health system expansion priorities will capture disproportionate value from this structurally significant and policy-guaranteed market development opportunity over the forecast period.

Southeast Asia Clinical Laboratory Services Market Country Analysis

By Country

- Indonesia

- Thailand

- Vietnam

- Malaysia

- Philippines

- Singapore

The segment with highest market share under the Country is Indonesia, accounting for approximately 30% of the total market. This leading national market position reflects the structural convergence of Southeast Asia's largest population base, the region's most ambitious healthcare infrastructure modernization investment program, the deepest concentration of hospital and community health center service delivery points, and a national health system development trajectory whose scale and institutional commitment make Indonesia the organizing commercial geography around which regional laboratory service competitive strategy, capacity investment, and market entry prioritization decisions are structured. With nearly one-third of total regional market value concentrated within a single national market, Indonesia defines the commercial scale and growth trajectory parameters of the Southeast Asia clinical laboratory services market.

The structural dominance of Indonesia is being actively reinforced by the AIIB-backed USD 4 billion health system modernization initiative that is systematically expanding and upgrading the country's laboratory service infrastructure across its three-tier healthcare delivery system. The initiative's scope encompassing approximately 10,000 community health centers and over 3,000 hospitals, combined with dedicated enhancements to public health laboratories from Tiers 2 through 5, confirms the institutional investment breadth that is progressively expanding laboratory service capacity, geographic reach, and technical capability across previously underserved regions of the country. As this infrastructure investment translates into expanded laboratory service access and rising diagnostic testing utilization across Indonesia's diverse geographic and demographic contexts, the country's structural market share leadership will deepen and its commercial importance as the primary regional growth driver will strengthen over the forecast period.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Southeast Asia Clinical Laboratory Services Market Segmentation Analysis

By Test Type

- Clinical Chemistry

- Routine Chemistry Testing

- Therapeutic Drug Monitoring Testing

- Endocrinology Chemistry Testing

- Specialized Chemistry Testing

- Other Clinical Chemistry Testing

- Hematology Testing

- Medical Microbiology

- Infectious Disease Testing

- Transplant Diagnostic Testing

- Other Microbiology Testing

- Immunology & Serology Testing

- Molecular Diagnostics

- Genetic Testing

- Pathology

- Cytopathology

- Histopathology

- Blood Banking & Transfusion Services

- Toxicology & Drug Abuse Testing

- Other Specialty/Esoteric Tests

The segment with highest market share under the Test Type is Clinical Chemistry, accounting for approximately 25% of the total market. This leading position reflects the deep structural alignment between clinical chemistry testing capabilities and the specific diagnostic workflow requirements of Southeast Asia's most institutionally significant laboratory service environments, where the high-volume applicability, repeat testing frequency, and broad clinical relevance of biochemical analysis across metabolic assessment, organ function monitoring, chronic disease management, and routine health screening make clinical chemistry the reference test category across hospital-based, independent, and public health laboratory settings throughout the region. With one-quarter of total market value concentrated within a single test type category, Clinical Chemistry defines the equipment investment priorities, reagent procurement frameworks, and operational capacity planning benchmarks of the Southeast Asia clinical laboratory services market.

The structural leadership of Clinical Chemistry is being actively sustained by the dual disease burden of chronic noncommunicable disease and persistent infectious disease that characterizes Southeast Asia's regional health profile, both of which generate consistent and high-frequency biochemical testing requirements across patient monitoring, treatment response assessment, and population screening programs. WHO South-East Asia's documentation of 9.5 million annual noncommunicable disease deaths confirms the chronic disease management demand that sustains consistent clinical chemistry testing volume across diabetes monitoring, cardiovascular risk assessment, kidney function evaluation, and liver health screening workflows. As universal health coverage programs expand laboratory service access across previously underserved populations, the high-volume and cost-accessible characteristics of clinical chemistry testing position it favorably for adoption acceleration across the region's most rapidly developing healthcare system contexts. The segment's structural commercial leadership is expected to consolidate over the forecast period.

By Service Provider

- Hospital-based Laboratories

- Independent/Standalone Clinical Laboratories

- Clinic/Physician Office Laboratories

- Public Health Laboratories

- Specialty Laboratories

The segment with highest market share under the Service Provider is Hospital-Based Laboratories, accounting for approximately 40% of the total market. This dominant position reflects the foundational operational reality of Southeast Asian clinical diagnostics, where the integration of laboratory testing within hospital care workflows, the physician-directed testing referral patterns of institutional care settings, and the round-the-clock diagnostic access requirements of inpatient and emergency care environments collectively generate the highest concentration and most clinically urgent laboratory service demand across the regional market. With two-fifths of total market value anchored in hospital-based laboratory service delivery, this provider segment defines the testing volume benchmarks, quality standard expectations, and equipment investment priorities of the Southeast Asia clinical laboratory services market.

The structural leadership of Hospital-Based Laboratories is being actively sustained by the progressive expansion of hospital care infrastructure across Southeast Asia's most rapidly urbanizing national healthcare systems, where government and private sector hospital capacity investment is generating consistent expansion in the institutional care settings whose laboratory service requirements create the most commercially significant diagnostic testing demand concentrations in the regional market. Indonesia's AIIB-backed health system modernization initiative, which encompasses over 3,000 hospitals alongside enhancements to public health laboratories across multiple tiers, directly validates the hospital infrastructure investment trajectory that sustains hospital-based laboratory service demand expansion. As healthcare system formalization advances and hospital utilization rates increase across the region's high-growth national markets, the hospital-based laboratory provider segment's structural commercial dominance is expected to deepen over the forecast period.

Various Market Players in Southeast Asia Clinical Laboratory Services Market

The companies mentioned below are highly active in the Southeast Asia clinical laboratory services market, occupying a considerable portion of the market and shaping industry progress.

- Raffles Diagnostica Laboratory

- Parkway Laboratory Services

- IHH Laboratories

- Pathology Asia

- Innoquest Diagnostics

- Innoquest Pathology

- Prodia

- Diagnos Laboratorium

- Bumrungrad Laboratory

- Bangkok Dusit Medical Services (BDMS)

- Hi-Precision Diagnostics

- The Medical City

Market News & Updates

- Prodia, 2025:

Prodia inaugurated the Prodia Clinical Multiomics Centre (PCMC), describing it as a next-generation laboratory built around mass spectrometry technology and capable of supporting more than 140 biomarkers with higher analytical precision. For the Southeast Asia clinical laboratory services market, this is one of the strongest innovation-led updates because it pushes the region’s private lab sector toward more advanced specialty testing and multi-omics capability rather than routine diagnostics alone.

- Raffles Medical Group / Raffles Diagnostica Laboratory, 2026:

Raffles Medical Group announced that its Raffles Healthy Longevity Centre would open in Q1 2026 as a physician-led, multidisciplinary service built around advanced diagnostics and evidence-based preventive care. For the Southeast Asia clinical laboratory services market, this is a meaningful service launch because it ties diagnostics more directly to preventive and longevity-oriented care pathways, expanding the role of laboratory services in early risk identification and personalized health management.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Southeast Asia Clinical Laboratory Services Market Policies, Regulations, and Standards

- Southeast Asia Clinical Laboratory Services Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Southeast Asia Clinical Laboratory Services Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Test Type

- Clinical Chemistry- Market Insights and Forecast 2022-2032, USD Million

- Routine Chemistry Testing- Market Insights and Forecast 2022-2032, USD Million

- Therapeutic Drug Monitoring Testing- Market Insights and Forecast 2022-2032, USD Million

- Endocrinology Chemistry Testing- Market Insights and Forecast 2022-2032, USD Million

- Specialized Chemistry Testing- Market Insights and Forecast 2022-2032, USD Million

- Other Clinical Chemistry Testing- Market Insights and Forecast 2022-2032, USD Million

- Hematology Testing- Market Insights and Forecast 2022-2032, USD Million

- Medical Microbiology- Market Insights and Forecast 2022-2032, USD Million

- Infectious Disease Testing- Market Insights and Forecast 2022-2032, USD Million

- Transplant Diagnostic Testing- Market Insights and Forecast 2022-2032, USD Million

- Other Microbiology Testing- Market Insights and Forecast 2022-2032, USD Million

- Immunology & Serology Testing- Market Insights and Forecast 2022-2032, USD Million

- Molecular Diagnostics- Market Insights and Forecast 2022-2032, USD Million

- Genetic Testing- Market Insights and Forecast 2022-2032, USD Million

- Pathology- Market Insights and Forecast 2022-2032, USD Million

- Cytopathology- Market Insights and Forecast 2022-2032, USD Million

- Histopathology- Market Insights and Forecast 2022-2032, USD Million

- Blood Banking & Transfusion Services- Market Insights and Forecast 2022-2032, USD Million

- Toxicology & Drug Abuse Testing- Market Insights and Forecast 2022-2032, USD Million

- Other Specialty/Esoteric Tests- Market Insights and Forecast 2022-2032, USD Million

- Clinical Chemistry- Market Insights and Forecast 2022-2032, USD Million

- By Service Provider

- Hospital-based Laboratories- Market Insights and Forecast 2022-2032, USD Million

- Independent/Standalone Clinical Laboratories- Market Insights and Forecast 2022-2032, USD Million

- Clinic/Physician Office Laboratories- Market Insights and Forecast 2022-2032, USD Million

- Public Health Laboratories- Market Insights and Forecast 2022-2032, USD Million

- Specialty Laboratories- Market Insights and Forecast 2022-2032, USD Million

- By Application

- Routine Diagnostic Testing- Market Insights and Forecast 2022-2032, USD Million

- Chronic Disease Testing- Market Insights and Forecast 2022-2032, USD Million

- Infectious Disease Testing- Market Insights and Forecast 2022-2032, USD Million

- Oncology Testing- Market Insights and Forecast 2022-2032, USD Million

- Preventive/Screening Testing- Market Insights and Forecast 2022-2032, USD Million

- Specialized/Genetic Testing- Market Insights and Forecast 2022-2032, USD Million

- By Country

- Indonesia

- Thailand

- Vietnam

- Malaysia

- Philippines

- Singapore

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Test Type

- Market Size & Growth Outlook

- Indonesia Clinical Laboratory Services Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Test Type- Market Insights and Forecast 2022-2032, USD Million

- By Service Provider- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Thailand Clinical Laboratory Services Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Test Type- Market Insights and Forecast 2022-2032, USD Million

- By Service Provider- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Vietnam Clinical Laboratory Services Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Test Type- Market Insights and Forecast 2022-2032, USD Million

- By Service Provider- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Malaysia Clinical Laboratory Services Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Test Type- Market Insights and Forecast 2022-2032, USD Million

- By Service Provider- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Philippines Clinical Laboratory Services Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Test Type- Market Insights and Forecast 2022-2032, USD Million

- By Service Provider- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Singapore Clinical Laboratory Services Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Test Type- Market Insights and Forecast 2022-2032, USD Million

- By Service Provider- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Pathology Asia

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Innoquest Diagnostics

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Innoquest Pathology

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Prodia

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Diagnos Laboratorium

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Raffles Diagnostica Laboratory

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Parkway Laboratory Services

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- IHH Laboratories

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Bumrungrad Laboratory

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Bangkok Dusit Medical Services (BDMS)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Hi-Precision Diagnostics

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- The Medical City

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Pathology Asia

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Test Type |

|

| By Service Provider |

|

| By Application |

|

| By Country |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.