South Korea Diagnostic Labs Market Report: Trends, Growth and Forecast (2026-2032)

By Lab Type (Single/Independent Laboratories, Hospital-based Laboratories, Physician Office Laboratories, Others), By Testing Services (Physiological Function Testing, General & Clinical Testing, Esoteric Testing, Specialized Testing, Non-invasive Prenatal Testing, COVID-19 Testing, Others), By Disease (Cardiology, Oncology, Neurology, Orthopedics, Gastroenterology, Gynecology, Odontology, Others), By Revenue Source (Healthcare Plan, Out-of-Pocket, Public System), By Test Type (Pathology, Radiology), By End User (Referrals, Walk-ins, Corporate Clients) ... Read more

|

Major Players

|

South Korea Diagnostic Labs Market Statistics and Insights, 2026

- Market Size Statistics

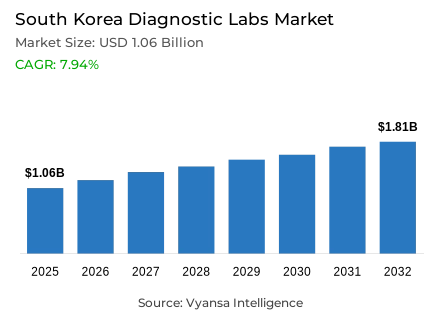

- Diagnostic labs market size in South Korea was estimated at USD 1.06 billion in 2025.

- The market size is expected to grow to USD 1.81 billion by 2032.

- Market to register a CAGR of around 7.94% during 2026-32.

- Lab Type Shares

- Hospital-based laboratories grabbed market share of 50%.

- Competition

- Diagnostic labs in South Korea is currently being catered to by more than 10 companies.

- Top 5 companies acquired around 60% of the market share.

- Geneone Life Science Inc., Humanpass Inc., Ellead, Seegene medical foundation, Green Cross Laboratories etc., are few of the top companies.

- Testing Services

- General & clinical testing grabbed 45% of the market.

South Korea Diagnostic Labs Market Outlook

The South Korea diagnostic laboratories market is set to grow steadily, with a growth of 1.06 billion in 2025 to 1.81 billion 2032, with a CAGR of about 7.94% in the 2026-32 period. This trend is underpinned by a steady high attendance at government-sponsored preventive health programmes, with the overall health check-up rates remaining at 75.7% in 2024 and cancer screening attendance at 60.2%. These strong screening practices produce predictable, high volume sample flows that produce repeatable revenue streams to laboratories across the country.

The market is currently dominated by hospital-based laboratories with a 50% share, which have the advantage of being strategically integrated into healthcare systems and have direct access to ordering clinicians. The largest segment is general and clinical testing services with 45% due to routine haematology and biochemistry panels requested to check-up and monitor chronic diseases. Inbound medical tourism also contributes to the strength of the market, as it increased to 1,170,467 foreign patients in 2024 compared to 605,768 in 2023, generating incremental demand of rapid, internationally standardised testing services with premium pricing potential.

Nevertheless, laboratories are increasingly challenged by the growing cybersecurity threats, and the number of hacking cases is growing, reaching 151 cases in 2023 and 171 cases in 2024. The introduction of the Digital Medical Products Act in Korea in January 2025, as well as the increase in the number of medical device cybersecurity requirements (15 to 35 criteria), is pushing laboratories to spend a lot of money on improved IT infrastructure, compliance measures, and security solutions.

In the future, the key to success will be the capacity of laboratories to strike a balance between automation investments, quality assurance, and responsiveness to the changing regulatory frameworks and the ability to capitalise on both domestic screening programmes and the increasing number of international patients that will sustain the market growth through 2032.

South Korea Diagnostic Labs Market Growth Driver

Sustained Participation in National Screening Programs Drives Steady Test Volumes

The South Korea diagnostic laboratories market enjoys a high rate of participation in the preventive health programs backed by the government. According to data provided by the National Health Insurance Service (NHIS), general health check-ups are still well-participated (75.9% in 2023 and 75.7% in 2024), with the comprehensive six-cancer screening programme being 59.8% in 2023 and 60.2% in 2024. These consistent levels of participation guarantee predictable high volume sample flows to laboratories throughout the country.

Such a regular screening habit is especially useful to laboratories as it produces predictable revenue streams and uniform testing processes. Routine diagnostic profiles including blood counts, glucose, lipid profiles, and liver and kidney markers generate significant daily workload, and abnormal results naturally lead to subsequent investigative efforts that do not necessitate any extra patient acquisition. Laboratories operating screening contracts are focused on automation infrastructure, robust reagent supply chains and strict quality-control measures to sustain competitive turnaround times and provide reporting accuracy to meet clinical standards.

South Korea Diagnostic Labs Market Challenge

Rising Cybersecurity Threats Create Operational and Compliance Pressures

The issue of data security is becoming a more important limitation to diagnostic laboratories as the healthcare digitalization accelerates. In 2024, the Personal Information Protection Commission (PIPC) and the Korea Internet & Security Agency (KISA) registered 307 notifications of personal data breaches, with 56% (171 cases) of these incidents being hacking, 30% (91 cases) work-related errors, and 7% (23 cases) system failures. Notably, the count of hacking cases increased to 171 in 2024 compared to 151 in 2023, which highlights the growing threat environment.

Diagnostic labs deal with very sensitive personal and clinical information, which makes them a very attractive target and a subject of increased compliance scrutiny. The identified patterns of breaches require the deployment of more stringent access controls, round-the-clock surveillance mechanisms, and secure data-sharing policies with hospitals and digital health platforms; all of which raise IT spending and can slow down integration initiatives. In addition to financial consequences, cybersecurity events introduce the risk of operational downtime and possible reputational damage that can undermine end-user trust, making a well-developed security infrastructure a necessity and not a luxury to the labs that seek to grow their services.

Unlock Market Intelligence

Explore the market potential with our data-driven report

South Korea Diagnostic Labs Market Trend

Regulatory Framework for Digital Diagnostics Establishes Clearer Pathways and Higher Standards

The regulatory framework of digital and AI-enabled diagnostic technologies is experiencing a major structural transformation. The Digital Medical Products Act of Korea, which comes into effect on January 24, 2025, provides a detailed framework specifically targeting digital medical devices and related health products, backed by 32 supporting guidance documents. Also, medical device cybersecurity guidance was significantly revised in November 2024, with 15 criteria being increased to 35 to meet international standards and respond to new digital threats.

To diagnostic laboratories, this regulatory modernization provides a clearer route to implementing software-based innovations such as AI-assisted result interpretation, interconnected analyzer systems, and remote updates, and also increases the level of validation and cybersecurity compliance expectations. Laboratories and their device vendors are now required to adopt more stringent documentation procedures, lifecycle risk management procedures, and disciplined change-control procedures to make sure that digital diagnostic tools are compliant throughout their operational lifecycle. This regulatory tightening is a visible trend that is gradually shaping procurement decision-making, vendor selection criteria, and long-term technology investment strategies throughout the laboratory industry.

South Korea Diagnostic Labs Market Opportunity

Medical Tourism Expansion Creates Incremental Testing Demand with Premium Characteristics

The rise of inbound medical travel is expanding the market of diagnostic testing services that can be addressed to beyond domestic end users. The portal of Medical Korea (KHIDI) in Korea lists 1,170,467 foreign patients in 2024 across 202 countries, which is a significant rise compared to 605,768 patients in 2023. The fact that the one-million patient mark is reached indicates a significant increase in the number of care episodes that usually begin with baseline diagnostic tests and extensive pre-procedure screening procedures.

This influx of international patients presents unique opportunities to laboratories that can provide fast, internationally standardized results such as English-language reports, globally accepted reference ranges, and secure digital delivery systems specific to hospitals and clinics that serve overseas end users. Infection screening panels, routine pre-operative tests, and post-treatment monitoring services are especially demanded by the medical tourism segment in high-traffic medical destinations. Labs that proactively invest in multilingual support systems, internationally accepted quality standards, and simplified reporting systems are best placed to tap this incremental, largely cash-based testing market that frequently fetches a premium price over and above the normal domestic reimbursement rates.

Unlock Market Intelligence

Explore the market potential with our data-driven report

South Korea Diagnostic Labs Market Segmentation Analysis

By Lab Type

- Single/Independent Laboratories

- Hospital-based Laboratories

- Physician Office Laboratories

- Others

In the segmentation analysis under Lab Type, hospital-based laboratories command the highest market share at 50%, reflecting their strategic integration within tertiary and general hospital systems. These facilities manage diverse testing portfolios encompassing inpatient consultations, outpatient services, emergency department requirements, and pre-surgical clearance protocols. Alternative laboratory configurations including independent reference laboratories and stand-alone diagnostic centers fulfill complementary roles, typically concentrating on outsourced testing volumes or specialized assay capabilities that hospitals choose not to maintain in-house.

With national screening participation maintaining stability at 75.7% for general health check-ups in 2024, hospital laboratories continue experiencing concentrated daily sample influxes that necessitate immediate results for clinical decision-making. This structural advantage enables hospital-based facilities to justify investments in advanced automation platforms and maintain direct connectivity with ordering clinicians, while independent laboratories compete through comprehensive specimen pickup networks, efficient batch processing systems, and differentiated niche testing capabilities. The persistent dominance of hospital laboratories reflects both their convenience advantages and their ability to support the full continuum of care within integrated healthcare delivery systems.

By Testing Services

- Physiological Function Testing

- General & Clinical Testing

- Esoteric Testing

- Specialized Testing

- Non-invasive Prenatal Testing

- COVID-19 Testing

- Others

In the segmentation analysis by testing services, general & clinical testing holds the largest market share at 45%, encompassing routine hematology and biochemistry panels that physicians order for preventive check-ups, chronic disease monitoring, and pre-procedure medical clearance. Specialty services including molecular diagnostics, genetic testing, and advanced pathology represent smaller volume segments but fulfill critical functions for complex case management and precision medicine applications that require sophisticated analytical capabilities.

The dominance of routine testing services directly aligns with Korea's well-established preventive health behaviors, as evidenced by the 75.7% participation rate in general health check-ups recorded by NHIS in 2024, which generates sustained demand for standardized laboratory panels. For service providers, this market composition drives strategic priorities toward high-throughput analyzer platforms, reagent cost optimization, and accelerated reporting systems that support efficient processing of large sample volumes. Simultaneously, laboratories pursue differentiation strategies by incorporating specialty testing capabilities as a complementary service layer, which becomes particularly valuable when routine screening results identify abnormalities requiring advanced diagnostic investigation to guide clinical management decisions.

List of Companies Covered in South Korea Diagnostic Labs Market

The companies listed below are highly influential in the South Korea diagnostic labs market, with a significant market share and a strong impact on industry developments.

- Geneone Life Science Inc.

- Humanpass Inc.

- Ellead

- Seegene medical foundation

- Green Cross Laboratories

- Bio Focus Co. Ltd.

- Infinitt Healthcare Co.Ltd.

- Medipost Co.Ltd.

- Eone Diagnomics Genome Center

Market News & Updates

- Seegene Medical Foundation, 2025:

The Seegene Medical Foundation, a major Korean reference laboratory affiliated with Seegene, participated in the 2025 Korean Society for Laboratory Medicine International Conference (LMCE 2025) to showcase its advanced diagnostic infrastructure including automated PCR systems, next-gen LIS platforms and NIPT solutions, highlighting its leadership and technology outreach in clinical diagnostics innovation.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. South Korea Diagnostic Labs Market Policies, Regulations, and Standards

4. South Korea Diagnostic Labs Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. South Korea Diagnostic Labs Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in USD Million

5.2. Market Segmentation & Growth Outlook

5.2.1.By Lab Type

5.2.1.1. Single/Independent Laboratories- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Hospital-based Laboratories- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3. Physician Office Laboratories- Market Insights and Forecast 2022-2032, USD Million

5.2.1.4. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Testing Services

5.2.2.1. Physiological Function Testing- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. General & Clinical Testing- Market Insights and Forecast 2022-2032, USD Million

5.2.2.3. Esoteric Testing- Market Insights and Forecast 2022-2032, USD Million

5.2.2.4. Specialized Testing- Market Insights and Forecast 2022-2032, USD Million

5.2.2.5. Non-invasive Prenatal Testing- Market Insights and Forecast 2022-2032, USD Million

5.2.2.6. COVID-19 Testing- Market Insights and Forecast 2022-2032, USD Million

5.2.2.7. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Disease

5.2.3.1. Cardiology- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Oncology- Market Insights and Forecast 2022-2032, USD Million

5.2.3.3. Neurology- Market Insights and Forecast 2022-2032, USD Million

5.2.3.4. Orthopedics- Market Insights and Forecast 2022-2032, USD Million

5.2.3.5. Gastroenterology- Market Insights and Forecast 2022-2032, USD Million

5.2.3.6. Gynecology- Market Insights and Forecast 2022-2032, USD Million

5.2.3.7. Odontology- Market Insights and Forecast 2022-2032, USD Million

5.2.3.8. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Revenue Source

5.2.4.1. Healthcare Plan- Market Insights and Forecast 2022-2032, USD Million

5.2.4.2. Out-of-Pocket- Market Insights and Forecast 2022-2032, USD Million

5.2.4.3. Public System- Market Insights and Forecast 2022-2032, USD Million

5.2.5.By Test Type

5.2.5.1. Pathology- Market Insights and Forecast 2022-2032, USD Million

5.2.5.2. Radiology- Market Insights and Forecast 2022-2032, USD Million

5.2.6.By End User

5.2.6.1. Referrals- Market Insights and Forecast 2022-2032, USD Million

5.2.6.2. Walk-ins- Market Insights and Forecast 2022-2032, USD Million

5.2.6.3. Corporate Clients- Market Insights and Forecast 2022-2032, USD Million

5.2.7.By Competitors

5.2.7.1. Competition Characteristics

5.2.7.2. Market Share & Analysis

6. South Korea Single/Independent Laboratories Market Statistics, 2022-2032

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in USD Million

6.2. Market Segmentation & Growth Outlook

6.2.1.By Testing Services- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Disease- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By Revenue Source- Market Insights and Forecast 2022-2032, USD Million

6.2.4.By Test Type- Market Insights and Forecast 2022-2032, USD Million

6.2.5.By End User- Market Insights and Forecast 2022-2032, USD Million

7. South Korea Hospital-based Laboratories Market Statistics, 2022-2032

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in USD Million

7.2. Market Segmentation & Growth Outlook

7.2.1.By Testing Services- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Disease- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By Revenue Source- Market Insights and Forecast 2022-2032, USD Million

7.2.4.By Test Type- Market Insights and Forecast 2022-2032, USD Million

7.2.5.By End User- Market Insights and Forecast 2022-2032, USD Million

8. South Korea Physician Office Laboratories Market Statistics, 2022-2032

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in USD Million

8.2. Market Segmentation & Growth Outlook

8.2.1.By Testing Services- Market Insights and Forecast 2022-2032, USD Million

8.2.2.By Disease- Market Insights and Forecast 2022-2032, USD Million

8.2.3.By Revenue Source- Market Insights and Forecast 2022-2032, USD Million

8.2.4.By Test Type- Market Insights and Forecast 2022-2032, USD Million

8.2.5.By End User- Market Insights and Forecast 2022-2032, USD Million

9. Competitive Outlook

9.1. Company Profiles

9.1.1.Seegene medical foundation

9.1.1.1. Business Description

9.1.1.2. Service Portfolio

9.1.1.3. Collaborations & Alliances

9.1.1.4. Recent Developments

9.1.1.5. Financial Details

9.1.1.6. Others

9.1.2.Green Cross Laboratories

9.1.2.1. Business Description

9.1.2.2. Service Portfolio

9.1.2.3. Collaborations & Alliances

9.1.2.4. Recent Developments

9.1.2.5. Financial Details

9.1.2.6. Others

9.1.3.Bio Focus Co. Ltd.

9.1.3.1. Business Description

9.1.3.2. Service Portfolio

9.1.3.3. Collaborations & Alliances

9.1.3.4. Recent Developments

9.1.3.5. Financial Details

9.1.3.6. Others

9.1.4.Infinitt Healthcare Co.Ltd.

9.1.4.1. Business Description

9.1.4.2. Service Portfolio

9.1.4.3. Collaborations & Alliances

9.1.4.4. Recent Developments

9.1.4.5. Financial Details

9.1.4.6. Others

9.1.5.Medipost Co.Ltd.

9.1.5.1. Business Description

9.1.5.2. Service Portfolio

9.1.5.3. Collaborations & Alliances

9.1.5.4. Recent Developments

9.1.5.5. Financial Details

9.1.5.6. Others

9.1.6.Geneone Life Science Inc.

9.1.6.1. Business Description

9.1.6.2. Service Portfolio

9.1.6.3. Collaborations & Alliances

9.1.6.4. Recent Developments

9.1.6.5. Financial Details

9.1.6.6. Others

9.1.7.Humanpass Inc.

9.1.7.1. Business Description

9.1.7.2. Service Portfolio

9.1.7.3. Collaborations & Alliances

9.1.7.4. Recent Developments

9.1.7.5. Financial Details

9.1.7.6. Others

9.1.8.Ellead

9.1.8.1. Business Description

9.1.8.2. Service Portfolio

9.1.8.3. Collaborations & Alliances

9.1.8.4. Recent Developments

9.1.8.5. Financial Details

9.1.8.6. Others

9.1.9.Eone Diagnomics Genome Center

9.1.9.1. Business Description

9.1.9.2. Service Portfolio

9.1.9.3. Collaborations & Alliances

9.1.9.4. Recent Developments

9.1.9.5. Financial Details

9.1.9.6. Others

10. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Lab Type |

|

| By Testing Services |

|

| By Disease |

|

| By Revenue Source |

|

| By Test Type |

|

| By End User |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.