South Africa Digestive Remedies Market Report: Trends, Growth and Forecast (2026-2032)

By Product Type (Paediatric Digestive Remedies (Paediatric Diarrhoeal Remedies, Paediatric Indigestion & Heartburn Remedies, Paediatric Laxatives, Paediatric Motion Sickness Remedies), Diarrhoeal Remedies, IBS Treatments, Indigestion & Heartburn Remedies (Antacids, Antiflatulents, Digestive Enzymes, H2 Blockers, Proton Pump Inhibitors), Laxatives, Motion Sickness Remedies), By Age Group (Children & Adolescents (01-17 years), Adults (18-65 years), Geriatric (65+ years)), By Sales Channel (Retail Online, Retail Offline (Hospitals, Clinics, Pharmacies)), By Region (Gauteng, Western Cape, Eastern Cape, North West, Others) ... Read more

|

Major Players

|

South Africa Digestive Remedies Market Statistics and Insights, 2026

- Market Size Statistics

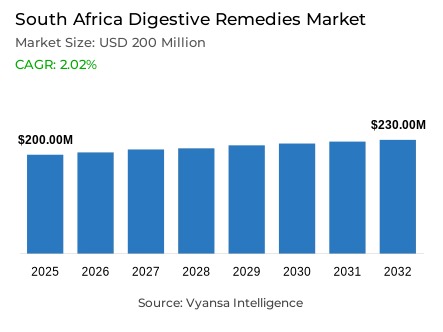

- Digestive remedies market size in South Africa was valued at USD 200 million in 2025 and is estimated at USD 205 Million in 2026.

- The market size is expected to grow to USD 230 million by 2032.

- Market to register a CAGR of around 2.02% during 2026-32.

- Product Type Shares

- Indigestion & heartburn remedies grabbed market share of 65%.

- Competition

- More than 10 companies are actively engaged in producing digestive remedies in South Africa.

- Top 5 companies acquired around 45% of the market share.

- Bayer (Pty) Ltd, Aspen Pharmacare (Pty) Ltd, Johnson & Johnson (Pty) Ltd, Adcock Ingram Holdings Ltd, GSK Consumer Healthcare etc., are few of the top companies.

- Sales Channel

- Retail offline grabbed 70% of the market.

South Africa Digestive Remedies Market Outlook

South Africa digestive remedies market size was valued at USD 200 million in 2025 and is projected to grow from USD 205 million in 2026 to USD 230 million by 2032, exhibiting a CAGR of 2.02% during the forecast period. The steady growth reflects consistent demand driven by everyday digestive health needs, even as broader economic conditions remain challenging.

Ongoing mealtime disruption and greater dependence on convenient food continue to support demand for digestive remedies. Loadshedding, busy work routines, and increased takeaway consumption contribute to irregular eating habits, which commonly lead to indigestion, heartburn, and related discomfort. As a result, consumers continue to rely on quick-relief digestive remedies for everyday symptom management, especially those that are easy to access and use without medical consultation.

At the same time, rising price sensitivity remains a key factor shaping purchasing behavior. High unemployment and increasing food costs push many consumers to trade down to more affordable options, including generics and private label products. Despite this, demand for digestive remedies remains stable, supported by their essential role in managing common health concerns. Indigestion and heartburn remedies dominate the category with a 65% share, reflecting strong preference for fast-acting solutions aligned with self-medication habits.

A growing shift toward natural, probiotic, and easy-to-consume formats is also influencing product development and consumer choice. Increased digital access supports awareness of gut health and alternative solutions, while herbal and complementary options gain attention as gentler alternatives. In addition, retail offline channels account for 70% of sales, as consumers continue to prefer pharmacies and physical stores for immediate purchase and trusted advice when buying digestive remedies.

South Africa Digestive Remedies Market Growth DriverMeal Disruptions and Convenience Eating Support Daily Symptom Relief

The constant interference during mealtime and increased reliance on ready-made food remain to sustain the demand of digestive remedies in South Africa. Load shedding, busy work habits, and increased use of takeaways drive consumers to fast food and unbalanced eating habits. These are habits that usually cause indigestion, heartburn, constipation, and other stomach-related issues that make quick-relief digestive products pertinent in daily life.

Official household data supports this demand. Stats SA’s General Household Survey shows that 21.0% of households experience load shedding every day during the seven days before the survey. Although there are periods of power supply enhancement, this degree of inconvenience continues to impact food preparation and food storage in most households, leading to more dependence on ready-to-eat foods that worsen digestive issues.

South Africa Digestive Remedies Market ChallengeConsumer Downtrading Puts Pressure on Premium OTC Brands

One of the threats facing the digestive remedies in South Africa is the increasing consumer price sensitivity. Numerous families are financially stressed and are moving down to less expensive generics or own-label items. This complicates the ability of premium and international digestive remedy brands to sustain pricing power even in cases where digestive complaints are widespread and category demand is sustained. This pressure is confirmed by recent official data.

Stats SA reports that South Africa’s official unemployment rate is 31.4% in Q4 2025, while food and non‑alcoholic beverages inflation reaches 4.5% in September 2025. In the case of high unemployment and food prices are still increasing, consumers tend to spend less on discretionary healthcare and switch to less expensive digestive remedies rather than branded ones.

Unlock Market Intelligence

Explore the market potential with our data-driven report

South Africa Digestive Remedies Market TrendDigital Health Content Lifts Demand for Natural and Convenient Formats

Another trend that is being observed in South Africa is the increasing consumer preference towards natural, probiotic, and more convenient to drink digestive products. Tik Tok and Instagram are social media platforms that can be used to inform consumers about gut health, probiotics, and herbal or traditional remedies. Meanwhile, lifestyle-friendly products like gummies and portable packs are gaining popularity due to their ease of transportation and consumption.

The levels of digital access in South Africa support this change. Stats SA’s General Household Survey shows that 75.6% of households access the internet through mobile devices, while 17.4% have fixed internet at home. The same report notes that internet access through a cell phone rises to 82.1% in 2024. This wide digital presence assists health influencers and wellness content to influence consumer preferences to natural and alternative digestive care formats.

South Africa Digestive Remedies Market OpportunityHerbal and Complementary Portfolios Create White-Space for Expansion

One of the opportunities in South Africa is the growth of herbal, traditional, and complementary digestive remedies portfolios. A large number of consumers are increasingly considering these products as being milder and more natural compared to regular OTC products. This leaves space to category players to expand their digestive health product range with herbal or complementary products that are more aligned with the current consumer trends in gut health and holistic wellness.

This direction is supported by the regulatory and policy environment. According to South African Health Products Regulatory Authority (SAHPRA), the complementary medicines in South Africa are recognised in six major disciplines, one of which is Western Herbal Medicine. Moreover, WHO notes that South Africa celebrates the African Traditional Medicine Day on 29 August and reiterates its intention to incorporate traditional medicine into the national health system, with 51 practitioners and community health workers recently trained with the assistance of WHO. This provides a better platform on which to develop herbal digestive products.

Unlock Market Intelligence

Explore the market potential with our data-driven report

South Africa Digestive Remedies Market Segmentation Analysis

By Product Type

- Paediatric Digestive Remedies

- Paediatric Diarrhoeal Remedies

- Paediatric Indigestion & Heartburn Remedies

- Paediatric Laxatives

- Paediatric Motion Sickness Remedies

- Diarrhoeal Remedies

- IBS Treatments

- Indigestion & Heartburn Remedies

- Antacids

- Antiflatulents

- Digestive Enzymes

- H2 Blockers

- Proton Pump Inhibitors

- Laxatives

- Motion Sickness Remedies

The segment has the highest share within the product type of indigestion and heartburn remedies, with a 65% market share. This segment is the leader since it deals with the most immediate and the most common digestive complaints in South Africa. Unpredictable eating schedules, reliance on takeaways, consumption of fast foods, and hectic day-to-day schedules usually lead to acidity, indigestion, and associated stomach pains, and thus the quick-relief products are the most viable option to consumers.

This high stance is also an indication of purchasing behaviour in the category. Consumers tend to seek fast acting, easy to administer, and do not need to visit a doctor to find a solution to common digestive discomfort. Consequently, remedies of indigestion and heartburn remain ahead of other product categories, which are backed by their applicability in daily digestive problems and their high compatibility with self-medication behavior.

By Sales Channel

- Retail Online

- Retail Offline

- Hospitals

- Clinics

- Pharmacies

The segment has the highest share within the sales channel of retail offline, with a 70% market share. This channel is the leader since digestive remedies are frequently purchased to be used immediately, and a significant number of South Africans continue to use pharmacies and physical stores when they experience such symptoms as indigestion, constipation, or heartburn. The in-store shopping also provides the consumer with an opportunity to compare products within a short time and consult during the purchase.

The significance of pharmacy-led access is supported by official data. According to the General Household Survey 2024 by Stats SA, approximately 212,000 households use a pharmacy/chemist as their usual place of consultation. Simultaneously, the South African Pharmacy Council reports that pharmacists in 2024 increased the primary care in community pharmacy. This reinforces the position of the offline pharmacies as the primary and most reliable channel of purchase of digestive remedies.

List of Companies Covered in South Africa Digestive Remedies Market

The companies listed below are highly influential in the South Africa digestive remedies market, with a significant market share and a strong impact on industry developments.

- Bayer (Pty) Ltd

- Aspen Pharmacare (Pty) Ltd

- Johnson & Johnson (Pty) Ltd

- Adcock Ingram Holdings Ltd

- GSK Consumer Healthcare

- Reckitt Benckiser South Africa (Pty) Ltd

- Ingelheim Pharmaceuticals (Pty) Ltd

- Norgine Pty Ltd

- Takeda (Pty) Ltd

- Abbott Laboratories SA Pty Ltd

Competitive Landscape

The competitive landscape of digestive remedies in South Africa remains fairly fragmented, despite the presence of several leading players. Adcock Ingram Holdings Ltd, GSK Consumer Healthcare, and Reckitt Benckiser South Africa (Pty) Ltd hold notable double-digit value shares through key brands such as Citro-Soda, Eno, and Gaviscon. However, the largest combined share is still held by smaller players grouped under “others”, highlighting the absence of a dominant market leader. Price sensitivity among consumers is intensifying competition, encouraging a shift towards private label and more affordable alternatives. Pharmacists play a critical role in influencing purchasing decisions, often recommending both branded and generic options, which fosters brand loyalty over time. Additionally, competition is increasing from herbal and traditional remedies, as consumers increasingly favour natural, gentler solutions, prompting companies to expand their portfolios to include such offerings.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- South Africa Digestive Remedies Market Policies, Regulations, and Standards

- South Africa Digestive Remedies Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- South Africa Digestive Remedies Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product Type

- Paediatric Digestive Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Diarrhoeal Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Indigestion & Heartburn Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Laxatives- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Motion Sickness Remedies- Market Insights and Forecast 2022-2032, USD Million

- Diarrhoeal Remedies- Market Insights and Forecast 2022-2032, USD Million

- IBS Treatments- Market Insights and Forecast 2022-2032, USD Million

- Indigestion & Heartburn Remedies- Market Insights and Forecast 2022-2032, USD Million

- Antacids- Market Insights and Forecast 2022-2032, USD Million

- Antiflatulents- Market Insights and Forecast 2022-2032, USD Million

- Digestive Enzymes- Market Insights and Forecast 2022-2032, USD Million

- H2 Blockers- Market Insights and Forecast 2022-2032, USD Million

- Proton Pump Inhibitors- Market Insights and Forecast 2022-2032, USD Million

- Laxatives- Market Insights and Forecast 2022-2032, USD Million

- Motion Sickness Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Digestive Remedies- Market Insights and Forecast 2022-2032, USD Million

- By Age Group

- Children & Adolescents (01-17 years)- Market Insights and Forecast 2022-2032, USD Million

- Adults (18-65 years)- Market Insights and Forecast 2022-2032, USD Million

- Geriatric (65+ years)- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- Hospitals- Market Insights and Forecast 2022-2032, USD Million

- Clinics- Market Insights and Forecast 2022-2032, USD Million

- Pharmacies- Market Insights and Forecast 2022-2032, USD Million

- By Region

- Gauteng

- Western Cape

- Eastern Cape

- North West

- Others

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Product Type

- Market Size & Growth Outlook

- South Africa Paediatric Digestive Remedies Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- South Africa Diarrhoeal Remedies Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- South Africa IBS Treatments Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- South Africa Indigestion & Heartburn Remedies Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- South Africa Laxatives Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- South Africa Motion Sickness Remedies Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Adcock Ingram Holdings Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- GSK Consumer Healthcare

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Reckitt Benckiser South Africa (Pty) Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Ingelheim Pharmaceuticals (Pty) Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Norgine Pty Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Bayer (Pty) Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Aspen Pharmacare (Pty) Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Johnson & Johnson (Pty) Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Takeda (Pty) Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Abbott Laboratories SA Pty Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Adcock Ingram Holdings Ltd

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Age Group |

|

| By Sales Channel |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.