Singapore Room Air Conditioners Market Report: Trends, Growth and Forecast (2026-2032)

By Product Type (Split Air Conditioners (Up to 9,000 BTU/h, 9,001-12,000 BTU/h, 12,001-18,000 BTU/h, 18,001-24,000 BTU/h, Above 24,000 BTU/h), Window Air Conditioners (Up to 9,000 BTU/h, 9,001-12,000 BTU/h, 12,001-18,000 BTU/h, 18,001-24,000 BTU/h, Above 24,000 BTU/h), Others), By Technology (Inverter, Non-Inverter), By Price (Up to USD 300, USD 301 to USD 600, USD 601 to USD 1,000, Above USD 1,000), By End User (Residential (Individual Households, Apartments/Condominiums, Vacation/Secondary Homes), Commercial (Offices, Retail Stores/Showrooms, Hospitality, Healthcare Facilities, Educational Institutions, Small Commercial Establishments, Others)), By Sales Channel (Retail Online (Brand-Owned Websites/D2C, E-Commerce Marketplaces), Retail Offline (Exclusive Brand Stores, Multi-Brand Electronics & Appliance Stores, Specialty Stores, Hypermarkets/Supermarkets, Home Improvement Stores, Dealer/Distributor Network, Direct Sales/Institutional Sales, Local Independent Retailers)), By Refrigerant Type (R-32, R-410A, R-290, R-454B, Others), By Connectivity (Smart/Connected, Conventional/Non-Smart), By Energy Efficiency (1 Star, 2 Star, 3 Star, 4 Star, 5 Star) ... Read more

|

Major Players

|

Singapore Room Air Conditioners Market Statistics and Insights, 2026

- Market Size Statistics

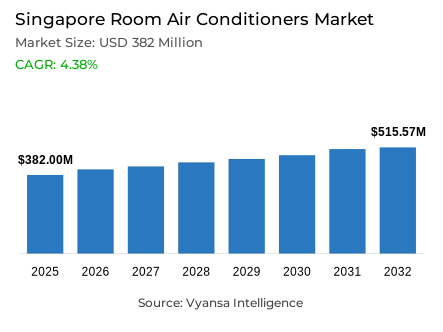

- Room air conditioners market size in Singapore was valued at USD 382 million in 2025 and is estimated at USD 406.98 million in 2026.

- The market size is expected to grow to USD 515.57 million by 2032.

- Market to register a CAGR of around 4.38% during 2026-32.

- Product Type Shares

- Split air conditioners grabbed market share of 85%.

- Competition

- More than 5 companies are actively engaged in producing room air conditioners in Singapore.

- Top 5 companies acquired around 80% of the market share.

- Panasonic Corp, LG Corp, Haier Group, Daikin Industries Ltd, Mitsubishi Electric Corp etc., are few of the top companies.

- End User

- Residential grabbed 55% of the market.

Singapore Room Air Conditioners Market Outlook

Singapore room air conditioners market was valued at USD 382 million in 2025, projected to reach USD 406.98 million in 2026 and USD 515.57 million by 2032 at a CAGR of 4.38%. That pace is measured, not exceptional but it points to a market running on embedded, recurring demand rather than first-time adoption or speculative uptake. Steady compounding of this kind, in a mature urban economy like Singapore, tends to hold up better over time than faster growth in less established markets.

At approximately 85% of the total market, split air conditioners do not just lead the category they functionally define it. Pricing norms, product development priorities, how brands compete for shelf space and installer relationships all of it plays out within this one segment. The concentration maps directly onto Singapore's housing stock, where high-rise apartments and standardized layouts leave limited room for alternative formats to gain any real foothold.

Residential end users account for around 55% of total demand. That makes household behavior the single most important variable in how this market moves replacement timing, sensitivity to running costs, unit sizing all feed into purchase decisions at the household level. Electricity bills are visible, living space is constrained, and buyers in this environment tend to weigh upgrade economics carefully before committing. Impulse purchases do not move the needle here.

Split systems anchor supply, residential buyers anchor demand, and the consumption environment is mature enough that growth comes primarily from replacement cycles and efficiency-driven upgrades rather than net new installations. For brands planning product pipelines and distribution investments over the forecast period, that predictability carries real commercial value.

Singapore Room Air Conditioners Market Growth DriverPersistent Heat Conditions Reinforcing Continuous Residential Cooling Demand

Singapore's annual average temperature hit 28.4°C in 2024, matching record highs from 2019 and 2016. Each month throughout the year consistently met or exceeded long-term averages, effectively eliminating any typical seasonal decline in cooling demand. Air conditioners stay in active use year-round, replacement cycles compress, and point-of-sale activity stays relatively even rather than clustering around particular months for brands and retailers, that kind of consistency is commercially useful.

The decade from 2015 to 2024 was the warmest Singapore has on record, averaging 28.11°C across the full ten-year span. At that intensity and persistence, heat no longer acts as a temporary weather factor but becomes a constant environmental condition. Households are increasingly shifting from viewing cooling systems as optional purchases to recognizing them as essential infrastructure. This transition reduces the typical price sensitivity seen in discretionary categories and helps maintain a relatively stable baseline demand through 2032..

Singapore Room Air Conditioners Market ChallengeElevated Electricity Tariffs Constraining Cost-Sensitive Purchase Decisions

Residential electricity tariffs stood at 26.71 cents per kWh, or 29.11 cents per kWh, for the January to March 2026 quarter. At those rates, running an air conditioner is a tangible, recurring line item not something households absorb passively. Energy consumption becomes a practical filter at the point of sale, often sitting alongside upfront price when end user compare models.

Total electricity consumption grew 4.0% to 58 TWh in 2024, with households accounting for 14.6% of that total, or roughly 8 TWh. That is a meaningful share, and it keeps financial pressure on residential buyers persistent and visible. Low-efficiency models face real resistance, upgrade decisions get benchmarked against long-term running costs, and brands that cannot demonstrate clear efficiency gains are at a disadvantage competing for replacement demand. Nothing in the outlook suggests that dynamic eases over the forcast period.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Singapore Room Air Conditioners Market TrendRegulatory Efficiency Standards Accelerating Transition Toward High-Performance Systems

All regulated household air conditioners sold in Singapore are required to display the mandatory Energy Label and meet the prescribed Minimum Energy Performance Standards. At the point of sale, that shifts the comparison basis cooling capacity and price still matter, but efficiency ratings on a standardized tick scale become a built-in part of how buyers evaluate options. Once that framework is embedded in how products are displayed and discussed, it is difficult for end user or brands to work around it.

The technical thresholds are not cosmetic. A 5-tick single-split inverter unit must achieve a weighted COP of at least 5.50 with standby power capped at 4 watts, a 4-tick model requires a COP of at least 4.86 and standby power at or below 18 watts. Those gaps translate into real differences in lifetime running costs and buyers attuned to electricity bills notice them.Market preference has been moving toward higher-rated models, and brands with credible top-tier efficiency performance are better placed to capture upgrade demand through 2032.

Singapore Room Air Conditioners Market OpportunityGovernment Voucher Schemes Unlocking Premium Replacement Demand

Government-backed Climate Voucher programmes create a strong opportunity for accelerating replacement demand. From 15 April 2025 through 31 December 2027, eligible households in Singapore can claim up to SGD 400 in Climate Vouchers for energy- and water-efficient appliances. Direct subsidies at that level reduce effective purchase cost in ways that tend to bring upgrade decisions forward particularly relevant here, where replacement timing already tracks closely against running cost sensitivity and household budgets.

Eligibility is not open-ended. Air conditioners must carry a 5-tick energy label to qualify, which directs the subsidy squarely at premium, high-efficiency models. For brands with credible 5-tick offerings, government support and consumer upgrade intent are pointing in the same direction within the same purchase window. That alignment builds a demand pathway for premiumization in a market otherwise growing at a measured pace and it holds through the end of the programme in 2027 and into the broader forecast period.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Singapore Room Air Conditioners Market Segmentation Analysis

By Product Type

- Split Air Conditioners

- Up to 9,000 BTU/h

- 9,001-12,000 BTU/h

- 12,001-18,000 BTU/h

- 18,001-24,000 BTU/h

- Above 24,000 BTU/h

- Window Air Conditioners

- Up to 9,000 BTU/h

- 9,001-12,000 BTU/h

- 12,001-18,000 BTU/h

- 18,001-24,000 BTU/h

- Above 24,000 BTU/h

- Others

The segment with highest market share under Product Type is Split air conditioners account for approximately 85% of Singapore's room air conditioner market. At that share, the segment does not just lead it sets the terms for pricing benchmarks, feature development, and how brands position themselves competitively. The underlying reasons are practical split systems fit Singapore's predominantly high-rise residential stock, offer installation flexibility across different room configurations, and deliver efficient cooling without the footprint or ducting demands of heavier alternatives. That preference has held across multiple product generations.

Competitive activity plays out almost entirely within this one segment, which means any meaningful shift in overall market performance whether from efficiency regulation, subsidy uptake, or replacement cycles running faster flows primarily through split systems. That is where the volume is, and that is where the commercial outcomes get decided. Through 2032, that concentration is not expected to shift.

By End User

- Residential

- Individual Households

- Apartments/Condominiums

- Vacation/Secondary Homes

- Commercial

- Offices

- Retail Stores/Showrooms

- Hospitality

- Healthcare Facilities

- Educational Institutions

- Small Commercial Establishments

- Others

The segment with highest market share under End user is residential account for approximately 55% of Singapore's room air conditioner market, making household demand the most reliable indicator of where the market is heading. Unlike some home appliance categories where purchases are heavily deferred, air conditioners here connect directly to daily comfort, sleep quality, and health in a climate that offers little natural relief. Demand pressure stays relatively steady even when broader consumer sentiment softens.

Purchase decisions at the household level are shaped by practical constraints electricity costs, unit sizing, installation requirements, efficiency ratings. These factors feed into buying behavior in ways specific to residential end user rather than commercial operators. When voucher schemes target eligible households and energy labels become a standard reference tool at retail, the residential segment responds to both signals directly. That sensitivity to cost pressures and policy incentives makes it the clearest lens for tracking where this market moves through 2032.

List of Companies Covered in Singapore Room Air Conditioners Market

The companies listed below are highly influential in the Singapore room air conditioners market, with a significant market share and a strong impact on industry developments.

- Panasonic Corp

- LG Corp

- Haier Group

- Daikin Industries Ltd

- Mitsubishi Electric Corp

- Midea Group Co Ltd

- Fujitsu Ltd

Market News & Updates

- LG Corp, 2025:

LG introduced its 2025 air care and residential cooling lineup in Singapore in May 2025, including the DUALCOOL™ AI Air alongside other connected air-care products. This is significant for the Singapore room air conditioners market because it reinforces the premium smart/connected split-AC segment, where app-based control, intelligent comfort adjustment, and indoor-air-quality integration are increasingly important in dense urban housing.

- Daikin Industries Ltd, 2025:

Daikin Singapore’s 2025 official consumer-site update highlighted its 5-ticks iSmileEco Series as an innovation-led residential air-conditioner line featuring energy-efficient cooling, PM2.5 dust filtration, and smart-home connectivity through the Reiri platform. While this is not a classic launch press release, it is one of the clearest 2025 official Singapore updates tied directly to a current RAC line, and it matters because it shows Daikin continuing to push efficiency and smart-home features in Singapore’s premium room-AC segment.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Singapore Room Air Conditioners Market Policies, Regulations, and Standards

- Singapore Room Air Conditioners Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Singapore Room Air Conditioners Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold in Thousand Units

- Market Segmentation & Growth Outlook

- By Product Type

- Split Air Conditioners- Market Insights and Forecast 2022-2032, USD Million

- Up to 9,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- 9,001-12,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- 12,001-18,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- 18,001-24,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- Above 24,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- Window Air Conditioners- Market Insights and Forecast 2022-2032, USD Million

- Up to 9,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- 9,001-12,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- 12,001-18,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- 18,001-24,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- Above 24,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Split Air Conditioners- Market Insights and Forecast 2022-2032, USD Million

- By Technology

- Inverter- Market Insights and Forecast 2022-2032, USD Million

- Non-Inverter- Market Insights and Forecast 2022-2032, USD Million

- By Price

- Up to USD 300- Market Insights and Forecast 2022-2032, USD Million

- USD 301 to USD 600- Market Insights and Forecast 2022-2032, USD Million

- USD 601 to USD 1,000- Market Insights and Forecast 2022-2032, USD Million

- Above USD 1,000- Market Insights and Forecast 2022-2032, USD Million

- By End User

- Residential- Market Insights and Forecast 2022-2032, USD Million

- Individual Households- Market Insights and Forecast 2022-2032, USD Million

- Apartments/Condominiums- Market Insights and Forecast 2022-2032, USD Million

- Vacation/Secondary Homes- Market Insights and Forecast 2022-2032, USD Million

- Commercial- Market Insights and Forecast 2022-2032, USD Million

- Offices- Market Insights and Forecast 2022-2032, USD Million

- Retail Stores/Showrooms- Market Insights and Forecast 2022-2032, USD Million

- Hospitality- Market Insights and Forecast 2022-2032, USD Million

- Healthcare Facilities- Market Insights and Forecast 2022-2032, USD Million

- Educational Institutions- Market Insights and Forecast 2022-2032, USD Million

- Small Commercial Establishments- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Residential- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- Brand-Owned Websites/D2C- Market Insights and Forecast 2022-2032, USD Million

- E-Commerce Marketplaces- Market Insights and Forecast 2022-2032, USD Million

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- Exclusive Brand Stores- Market Insights and Forecast 2022-2032, USD Million

- Multi-Brand Electronics & Appliance Stores- Market Insights and Forecast 2022-2032, USD Million

- Specialty Stores- Market Insights and Forecast 2022-2032, USD Million

- Hypermarkets/Supermarkets- Market Insights and Forecast 2022-2032, USD Million

- Home Improvement Stores- Market Insights and Forecast 2022-2032, USD Million

- Dealer/Distributor Network- Market Insights and Forecast 2022-2032, USD Million

- Direct Sales/Institutional Sales- Market Insights and Forecast 2022-2032, USD Million

- Local Independent Retailers- Market Insights and Forecast 2022-2032, USD Million

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- By Refrigerant Type

- R-32- Market Insights and Forecast 2022-2032, USD Million

- R-410A- Market Insights and Forecast 2022-2032, USD Million

- R-290- Market Insights and Forecast 2022-2032, USD Million

- R-454B- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Connectivity

- Smart/Connected- Market Insights and Forecast 2022-2032, USD Million

- Conventional/Non-Smart- Market Insights and Forecast 2022-2032, USD Million

- By Energy Efficiency

- 1 Star- Market Insights and Forecast 2022-2032, USD Million

- 2 Star- Market Insights and Forecast 2022-2032, USD Million

- 3 Star- Market Insights and Forecast 2022-2032, USD Million

- 4 Star- Market Insights and Forecast 2022-2032, USD Million

- 5 Star- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Product Type

- Market Size & Growth Outlook

- Singapore Split Air Conditioners Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold in Thousand Units

- Market Segmentation & Growth Outlook

- By Technology- Market Insights and Forecast 2022-2032, USD Million

- By Price- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Refrigerant Type- Market Insights and Forecast 2022-2032, USD Million

- By Connectivity- Market Insights and Forecast 2022-2032, USD Million

- By Energy Efficiency- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Singapore Window Air Conditioners Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold in Thousand Units

- Market Segmentation & Growth Outlook

- By Technology- Market Insights and Forecast 2022-2032, USD Million

- By Price- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Refrigerant Type- Market Insights and Forecast 2022-2032, USD Million

- By Connectivity- Market Insights and Forecast 2022-2032, USD Million

- By Energy Efficiency- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Daikin Industries Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Mitsubishi Electric Corp

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Panasonic Corp

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- LG Corp

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Midea Group Co Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Fujitsu Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Haier Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Others

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Daikin Industries Ltd

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Technology |

|

| By Price |

|

| By End User |

|

| By Sales Channel |

|

| By Refrigerant Type |

|

| By Connectivity |

|

| By Energy Efficiency |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.