Saudi Arabia Diagnostic Labs Market Report: Trends, Growth and Forecast (2026-2032)

By Lab Type (Single/Independent Laboratories, Hospital-based Laboratories, Physician Office Laboratories, Others), By Testing Services (Physiological Function Testing, General & Clinical Testing, Esoteric Testing, Specialized Testing, Non-invasive Prenatal Testing, COVID-19 Testing, Others), By Disease (Cardiology, Oncology, Neurology, Orthopedics, Gastroenterology, Gynecology, Odontology, Others), By Revenue Source (Healthcare Plan, Out-of-Pocket, Public System), By Test Type (Pathology, Radiology), By End User (Referrals, Walk-ins, Corporate Clients), By Region (East, West, South, Central) ... Read more

|

Major Players

|

Saudi Arabia Diagnostic Labs Market Statistics and Insights, 2026

- Market Size Statistics

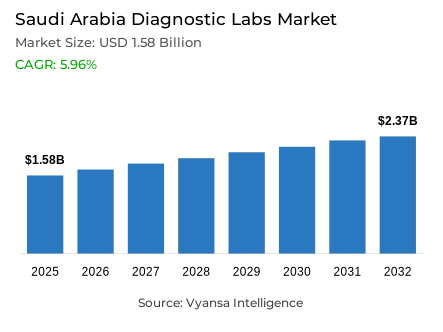

- Diagnostic labs market size in Saudi Arabia was estimated at USD 1.58 billion in 2025.

- The market size is expected to grow to USD 2.37 billion by 2032.

- Market to register a CAGR of around 5.96% during 2026-32.

- Lab Type Shares

- Hospital-based laboratories grabbed market share of 55%.

- Competition

- More than 10 companies are actively engaged in producing diagnostic labs in Saudi Arabia.

- Top 5 companies acquired around 70% of the market share.

- Roya Specialized Medical Laboratories, Tibyana Medical Laboratories, Al Hyatt Medical Laboratory Company, Al Borg Diagnostics, Delta Medical Laboratories etc., are few of the top companies.

- Testing Services

- General & clinical testing grabbed 45% of the market.

Saudi Arabia Diagnostic Labs Market Outlook

The diagnostic labs market in Saudi Arabia estimated at $1.58 billion in 2025 and is expected to reach $2.37 billion by 2032, growing at a CAGR of around 5.96% during 2026-32. Hospital-based laboratories dominate the landscape with a 55% market share, driven by their integration within hospitals where round-the-clock testing supports emergency care, inpatient monitoring, and intensive care cases. General and Clinical Testing leads testing services with a 45% share, serving as the first line for most patient journeys through routine blood counts, biochemistry panels, and infection screening that clinicians order regularly.

Testing demand continues to rise sharply across the public system, with the Ministry of Health reporting 237 million laboratory investigations in 2024 compared to 188 million in 2022. These volumes push labs to adopt high-throughput workflows, maintain analyzer calibration, and improve sample logistics for faster turnaround times. This sustained workload keeps purchasing cycles active for reagents, quality controls, collection tubes, and automation consumables while strengthening pre-analytical processes through barcode tracking and standardized procedures.

The advent of a fast-growing virtual care environment is reshaping the way laboratories operate in the digital era. The Seha Virtual Hospital currently has 44 medical specialties and is connected to about 232 hospitals, compared to the Wasfaty platform that has already processed over 200 million e-prescriptions to over 17 million beneficiaries. Laboratories now must be able to facilitate electronic test ordering, real-time status monitoring, and timely delivery of electronic results, thus increasing the use of integrated LIS platforms and standardized test codes across interconnected hubs.

The industry is supported by strong governmental support, as the FY2026 budget of Saudi Arabia has allocated SAR 259 billion to health and social development. This financial obligation enables the mass acquisition of analyzers, automation systems, and IT infrastructure, as well as renewal of supply contracts. The compulsory CBAHI accreditation of all laboratories is a guarantee of continuous investment in quality systems, employee training, and compliance with regulations, and the network of 843 accredited bodies and 529 assessors of the Saudi Accreditation Center ensures strict control that maintains investment in diagnostic infrastructure.

Saudi Arabia Diagnostic Labs Market Growth Driver

High-Volume Testing Demand and Infrastructure Requirements Drive Market Expansion

The public healthcare system has high demand of testing, making laboratory capacity a key element of care delivery. The Statistical Yearbook 2024 of the Ministry of Health shows that 237,082,756 laboratory investigations were carried out in MoH facilities in 2024, compared to 188,021,504 in 2022. This increase over a short period reflects the sustained and substantial nature of routine diagnostic workloads, and active buying cycles of reagents, quality controls, collection tubes, and automation consumables are maintained.

Such volumes require that laboratories run high-throughput workflows, have calibrated and accessible analyzers, and handle sample logistics effectively, all while responding to increased demands of rapid turnaround, thus allowing clinicians to triage emergencies and modify chronic-disease treatment in a timely manner. This compels providers to standardize SOPs and strengthen pre-analytical operations with barcode tracking and centrifugation to reduce errors and repeat testing, creating a sustained demand in diagnostic infrastructure and operational technologies.

Saudi Arabia Diagnostic Labs Market Challenge

Stringent Accreditation Standards and Compliance Requirements Hindering Market Growth

Diagnostic laboratories are subject to a high and compulsory quality control, which significantly increases the compliance load. The CBAHI provides that all public and private medical laboratories, hospitals, polyclinics, and blood banks in Saudi Arabia are obliged to be accredited; in this regard, laboratories should always have policies, documentation, and audit preparedness to meet the expectations of the regulations.

The national accreditation ecosystem is large and dynamic, as the Saudi Accreditation Center has identified 843 accredited organisations, has 529 assessors and experts, and has implemented 149 training programmes that have served 3,567 participants. To the operators, compliance with these standards requires constant investment in quality systems, employee training, validation, and traceability, and may extend timelines when adding instruments or introducing new test menus, especially in smaller laboratories with lean compliance teams.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Saudi Arabia Diagnostic Labs Market Trend

Digital Healthcare Integration and Virtual-First Service Models Transform Laboratory Operations

The healthcare system of Saudi Arabia is going digital and virtual, and the laboratories are adjusting to virtual-first referrals as care pathways become more digital and networked. The Ministry of Finance states in the FY2026 Budget Statement that the Seha Virtual Hospital will increase its range to 44 core medical specialties and 71 subspecialties, connecting the system to approximately 232 hospitals across the country, and Wasfaty will reach over 200 million e-prescriptions and over 17 million beneficiaries.

With the growth of virtual consultations, e-referrals, and e-prescriptions, laboratories need to support electronic test ordering, real-time status reporting, and fast digital dissemination of results to clinicians and end users. This necessitates laboratories to improve LIS connectivity, align test codes across hubs, and standardise pre-analytical processes, such as collection, labelling, and transportation, to allow samples in remote locations to reach central analysers without quality loss, thus driving adoption of integrated digital platforms.

Saudi Arabia Diagnostic Labs Market Opportunity

Government Healthcare Investment Creates Significant Growth Potential for Laboratory Modernization

The government spending remains focused on healthcare, thus, opening the possibilities of laboratory renovations and service development across the Kingdom. The FY2026 Budget Statement of Saudi Arabia allocates SAR 259 billion to the sector of Health and Social Development, including healthcare delivery, emergency services, and research activities, which facilitates the continuous procurement and modernisation of the entire public health system.

In the case of diagnostic laboratories, this public-budget model provides the possibility of large-volume purchasing cycles of analyzers, automation lines, and IT connectivity, and of recurring supply contracts of reagents and quality controls. It also facilitates collaborations that improve access outside of metropolitan regions with centralised hub-and-spoke testing, supplemented by dependable specimen transportation and electronic reporting, thus being especially relevant to routine screening and chronic-disease surveillance within the scope of the sector, which expressly includes system-wide service delivery.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Saudi Arabia Diagnostic Labs Market Segmentation Analysis

By Lab Type

- Single/Independent Laboratories

- Hospital-based Laboratories

- Physician Office Laboratories

- Others

The segment with the highest share around lab type is Hospital-based laboratories with market share of around 55%. Their lead comes from being embedded in hospitals where testing is needed nonstop for emergency cases, inpatient monitoring, pre-surgery screening, and intensive care follow-ups, all of which require quick turnaround and close clinician coordination for optimal patient outcomes.

Because these labs sit inside the care pathway, they typically run around the clock and keep a broader test menu under one roof, from routine panels to specialized confirmations routed through hospital departments. They also support infection control teams with rapid microbiology and serology results that guide isolation and treatment decisions, making this operational fit position hospital-based labs as the default choice for high-acuity testing while independent labs mainly capture scheduled outpatient and walk-in volumes.

By Testing Services

- Physiological Function Testing

- General & Clinical Testing

- Esoteric Testing

- Specialized Testing

- Non-invasive Prenatal Testing

- COVID-19 Testing

- Others

The segment with the highest share around testing services is General & Clinical testing with market share of around 45%. It leads because these tests are the first line for most patient journeys, covering complete blood counts, basic biochemistry, liver and kidney panels, lipid profiles, and common infectious screening that clinicians order repeatedly for diagnosis and follow-up while also supporting routine checkups and pre-procedure workups.

This service block benefits from standardization as hospitals and independent labs can run large batches with automated analyzers, making it faster to deliver results at scale and anchor daily lab throughput. As a result, general and clinical testing forms the operational backbone of laboratory services, while specialized services including advanced molecular panels, genetics, or pathology sub-specialties remain more case-specific and referral-driven across the market.

List of Companies Covered in Saudi Arabia Diagnostic Labs Market

The companies listed below are highly influential in the Saudi Arabia diagnostic labs market, with a significant market share and a strong impact on industry developments.

- Roya Specialized Medical Laboratories

- Tibyana Medical Laboratories

- Al Hyatt Medical Laboratory Company

- Al Borg Diagnostics

- Delta Medical Laboratories

- Alfa Medical Laboratories

- Saudi Diagnostic Limited

- Al Farabi Medical Laboratories

- Al Arab Medical Laboratories

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. Saudi Arabia Diagnostic Labs Market Policies, Regulations, and Standards

4. Saudi Arabia Diagnostic Labs Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. Saudi Arabia Diagnostic Labs Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in USD Million

5.2. Market Segmentation & Growth Outlook

5.2.1.By Lab Type

5.2.1.1. Single/Independent Laboratories- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Hospital-based Laboratories- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3. Physician Office Laboratories- Market Insights and Forecast 2022-2032, USD Million

5.2.1.4. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Testing Services

5.2.2.1. Physiological Function Testing- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. General & Clinical Testing- Market Insights and Forecast 2022-2032, USD Million

5.2.2.3. Esoteric Testing- Market Insights and Forecast 2022-2032, USD Million

5.2.2.4. Specialized Testing- Market Insights and Forecast 2022-2032, USD Million

5.2.2.5. Non-invasive Prenatal Testing- Market Insights and Forecast 2022-2032, USD Million

5.2.2.6. COVID-19 Testing- Market Insights and Forecast 2022-2032, USD Million

5.2.2.7. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Disease

5.2.3.1. Cardiology- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Oncology- Market Insights and Forecast 2022-2032, USD Million

5.2.3.3. Neurology- Market Insights and Forecast 2022-2032, USD Million

5.2.3.4. Orthopedics- Market Insights and Forecast 2022-2032, USD Million

5.2.3.5. Gastroenterology- Market Insights and Forecast 2022-2032, USD Million

5.2.3.6. Gynecology- Market Insights and Forecast 2022-2032, USD Million

5.2.3.7. Odontology- Market Insights and Forecast 2022-2032, USD Million

5.2.3.8. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Revenue Source

5.2.4.1. Healthcare Plan- Market Insights and Forecast 2022-2032, USD Million

5.2.4.2. Out-of-Pocket- Market Insights and Forecast 2022-2032, USD Million

5.2.4.3. Public System- Market Insights and Forecast 2022-2032, USD Million

5.2.5.By Test Type

5.2.5.1. Pathology- Market Insights and Forecast 2022-2032, USD Million

5.2.5.2. Radiology- Market Insights and Forecast 2022-2032, USD Million

5.2.6.By End User

5.2.6.1. Referrals- Market Insights and Forecast 2022-2032, USD Million

5.2.6.2. Walk-ins- Market Insights and Forecast 2022-2032, USD Million

5.2.6.3. Corporate Clients- Market Insights and Forecast 2022-2032, USD Million

5.2.7.By Region

5.2.7.1. East

5.2.7.2. West

5.2.7.3. South

5.2.7.4. Central

5.2.8.By Competitors

5.2.8.1. Competition Characteristics

5.2.8.2. Market Share & Analysis

6. Saudi Arabia Single/Independent Laboratories Market Statistics, 2022-2032

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in USD Million

6.2. Market Segmentation & Growth Outlook

6.2.1.By Testing Services- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Disease- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By Revenue Source- Market Insights and Forecast 2022-2032, USD Million

6.2.4.By Test Type- Market Insights and Forecast 2022-2032, USD Million

6.2.5.By End User- Market Insights and Forecast 2022-2032, USD Million

6.2.6.By Region- Market Insights and Forecast 2022-2032, USD Million

7. Saudi Arabia Hospital-based Laboratories Market Statistics, 2022-2032

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in USD Million

7.2. Market Segmentation & Growth Outlook

7.2.1.By Testing Services- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Disease- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By Revenue Source- Market Insights and Forecast 2022-2032, USD Million

7.2.4.By Test Type- Market Insights and Forecast 2022-2032, USD Million

7.2.5.By End User- Market Insights and Forecast 2022-2032, USD Million

7.2.6.By Region- Market Insights and Forecast 2022-2032, USD Million

8. Saudi Arabia Physician Office Laboratories Market Statistics, 2022-2032

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in USD Million

8.2. Market Segmentation & Growth Outlook

8.2.1.By Testing Services- Market Insights and Forecast 2022-2032, USD Million

8.2.2.By Disease- Market Insights and Forecast 2022-2032, USD Million

8.2.3.By Revenue Source- Market Insights and Forecast 2022-2032, USD Million

8.2.4.By Test Type- Market Insights and Forecast 2022-2032, USD Million

8.2.5.By End User- Market Insights and Forecast 2022-2032, USD Million

8.2.6.By Region- Market Insights and Forecast 2022-2032, USD Million

9. Competitive Outlook

9.1. Company Profiles

9.1.1.Al Borg Diagnostics

9.1.1.1. Business Description

9.1.1.2. Service Portfolio

9.1.1.3. Collaborations & Alliances

9.1.1.4. Recent Developments

9.1.1.5. Financial Details

9.1.1.6. Others

9.1.2.Delta Medical Laboratories

9.1.2.1. Business Description

9.1.2.2. Service Portfolio

9.1.2.3. Collaborations & Alliances

9.1.2.4. Recent Developments

9.1.2.5. Financial Details

9.1.2.6. Others

9.1.3.Alfa Medical Laboratories

9.1.3.1. Business Description

9.1.3.2. Service Portfolio

9.1.3.3. Collaborations & Alliances

9.1.3.4. Recent Developments

9.1.3.5. Financial Details

9.1.3.6. Others

9.1.4.Saudi Diagnostic Limited

9.1.4.1. Business Description

9.1.4.2. Service Portfolio

9.1.4.3. Collaborations & Alliances

9.1.4.4. Recent Developments

9.1.4.5. Financial Details

9.1.4.6. Others

9.1.5.Al Farabi Medical Laboratories

9.1.5.1. Business Description

9.1.5.2. Service Portfolio

9.1.5.3. Collaborations & Alliances

9.1.5.4. Recent Developments

9.1.5.5. Financial Details

9.1.5.6. Others

9.1.6.Roya Specialized Medical Laboratories

9.1.6.1. Business Description

9.1.6.2. Service Portfolio

9.1.6.3. Collaborations & Alliances

9.1.6.4. Recent Developments

9.1.6.5. Financial Details

9.1.6.6. Others

9.1.7.Tibyana Medical Laboratories

9.1.7.1. Business Description

9.1.7.2. Service Portfolio

9.1.7.3. Collaborations & Alliances

9.1.7.4. Recent Developments

9.1.7.5. Financial Details

9.1.7.6. Others

9.1.8.Al Hyatt Medical Laboratory Company

9.1.8.1. Business Description

9.1.8.2. Service Portfolio

9.1.8.3. Collaborations & Alliances

9.1.8.4. Recent Developments

9.1.8.5. Financial Details

9.1.8.6. Others

9.1.9.Al Arab Medical Laboratories

9.1.9.1. Business Description

9.1.9.2. Service Portfolio

9.1.9.3. Collaborations & Alliances

9.1.9.4. Recent Developments

9.1.9.5. Financial Details

9.1.9.6. Others

10. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Lab Type |

|

| By Testing Services |

|

| By Disease |

|

| By Revenue Source |

|

| By Test Type |

|

| By End User |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.