Portugal Room Air Conditioners Market Report: Trends, Growth and Forecast (2026-2032)

By Product Type (Split Air Conditioners (Up to 9,000 BTU/h, 9,001-12,000 BTU/h, 12,001-18,000 BTU/h, 18,001-24,000 BTU/h, Above 24,000 BTU/h), Window Air Conditioners (Up to 9,000 BTU/h, 9,001-12,000 BTU/h, 12,001-18,000 BTU/h, 18,001-24,000 BTU/h, Above 24,000 BTU/h), Others), By Technology (Inverter, Non-Inverter), By Price (Up to USD 300, USD 301 to USD 600, USD 601 to USD 1,000, Above USD 1,000), By End User (Residential (Individual Households, Apartments/Condominiums, Vacation/Secondary Homes), Commercial (Offices, Retail Stores/Showrooms, Hospitality, Healthcare Facilities, Educational Institutions, Small Commercial Establishments, Others)), By Sales Channel (Retail Online (Brand-Owned Websites/D2C, E-Commerce Marketplaces), Retail Offline (Exclusive Brand Stores, Multi-Brand Electronics & Appliance Stores, Specialty Stores, Hypermarkets/Supermarkets, Home Improvement Stores, Dealer/Distributor Network, Direct Sales/Institutional Sales, Local Independent Retailers)), By Refrigerant Type (R-32, R-410A, R-290, R-454B, Others), By Connectivity (Smart/Connected, Conventional/Non-Smart), By Energy Efficiency (1 Star, 2 Star, 3 Star, 4 Star, 5 Star) ... Read more

|

Major Players

|

Portugal Room Air Conditioners Market Statistics and Insights, 2026

- Market Size Statistics

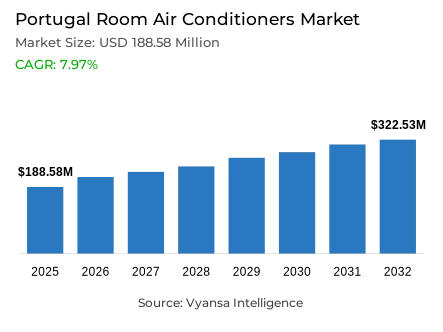

- Room air conditioners market size in Portugal was valued at USD 188.58 million in 2025 and is estimated at USD 214.89 million in 2026.

- The market size is expected to grow to USD 322.53 million by 2032.

- Market to register a CAGR of around 7.97% during 2026-32.

- Product Type Shares

- Split air conditioners grabbed market share of 85%.

- Competition

- More than 10 companies are actively engaged in producing room air conditioners in Portugal.

- Top 5 companies acquired around 50% of the market share.

- Haier Group, Gree Electric Appliances Inc of Zhuhai, Panasonic Corp, Daikin Industries Ltd, Mitsubishi Electric Corp etc., are few of the top companies.

- End User

- Residential grabbed 75% of the market.

Portugal Room Air Conditioners Market Outlook

The Portugal room air conditioners market was valued at USD 188.58 million in 2025, and projected to advance from USD 214.89 million in 2026 to USD 322.53 million by 2032, the sector registers a CAGR of approximately 7.97% over the forecast horizon a growth velocity that substantially outpaces Western European cooling market averages and reflects the structural convergence of climatic intensification, household electrification transition momentum, and residential renovation activity that is simultaneously expanding the addressable market and activating latent first-installation demand across Portugal's diverse housing geography.

The product architecture defining this market's commercial structure is characterized by pronounced format concentration within the split system category. Split air conditioners command approximately 85% of total product share a near-dominant position reflecting sustained consumer and installer preference for fixed, room-level cooling systems whose performance reliability, installation practicality, and long-term operational economics align more naturally with Portuguese household cooling requirements than portable or window-unit alternatives. This format concentration creates a focused competitive environment where brand differentiation is constructed on energy efficiency credentials, ecodesign compliance certification, and after-sales service reliability.

The end-user architecture reinforces the primacy of residential demand as the category's primary commercial engine. Residential buyers account for approximately 75% of total market share confirming that home-based cooling demand defines the category's volume base and replacement cycle dynamics. The European Commission's documentation of more than 85,000 residential energy renovations already completed in Portugal validates the structural expansion of the modernized residential installation base generating consistent upgrade-driven and first-installation cooling demand across the country's progressively improving housing stock.

The forward outlook through 2032 is defined by four structural market forces climatic intensification documented by IPMA elevating household cooling urgency, residential renovation and electrification funding programs administered through Portugal's Fundo Ambiental converting unequipped dwellings into active acquisition candidates, household electricity price pressures documented by Eurostat reshaping product selection toward energy-efficient models, and the deep structural inefficiency of over 75% of Portuguese residential buildings carrying an energy rating of C or lower collectively defining a commercial environment that rewards suppliers with compliant, efficient product portfolios and robust residential distribution networks through 2032.

Portugal Room Air Conditioners Market Growth DriverClimatic Intensification Elevates Cooling from Comfort Preference to Residential Necessity

The measurable and accelerating intensification of summer climate conditions across mainland Portugal represents the primary structural driver of room air conditioner demand functioning as a persistent environmental motivator that is systematically elevating household cooling investment priority among a consumer base confronting heat severity at a frequency and intensity that structurally alters the perceived necessity of cooling appliance ownership. This climatic driver reflects a durable behavioral shift in which repeated exposure to extreme temperature events progressively converts cooling from a discretionary comfort enhancement into a broadly expected residential infrastructure investment.

The quantitative evidence validating this dynamic is documented with precision by IPMA and Eurostat. Mainland Portugal records an average air temperature of 16.49°C in 2024, alongside 8 confirmed heat waves, 64 new maximum temperature extremes, and persistent drought across multiple months conditions generating powerful first-purchase and upgrade motivation across the residential base. Eurostat's documentation of cooling degree days at least doubling in 78% of EU regions between 1993 and 2023 further confirms that Portugal's cooling demand growth trajectory is a structurally durable directional shift sustaining market expansion through 2032.

Portugal Room Air Conditioners Market ChallengeElevated Electricity Costs and Housing Inefficiency Constrain Adoption Velocity

Portugal's structurally elevated and rapidly rising household electricity price environment, compounded by the deep energy inefficiency of the existing residential building stock, constitutes the most consequential demand-side challenge confronting the market creating persistent total ownership cost sensitivity that moderates purchase decision velocity, constrains multi-room installation ambitions, and shapes product selection toward energy-efficient models whose operating economics justify premium upfront investment through long-term electricity expenditure reduction.

The structural depth of this challenge is quantified by Eurostat, which documents household electricity prices in Portugal surging by 14.2% in the second half of 2024. This price acceleration operates within a housing base where the European Commission documents over 75% of residential buildings carrying an energy rating of C or lower meaning cooling system operating costs are amplified by poor building envelope performance. For market participants, this creates a strategic imperative to lead product communication with efficiency economics and total cost-of-ownership modeling as primary purchase justification tools through 2032.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Portugal Room Air Conditioners Market TrendResidential Electrification and Renovation Funding Accelerates Cooling System Adoption

The convergence of Portugal's domestic residential electrification support programs and European-framework renovation funding architecture represents a defining structural trend reshaping the demand activation environment for room air conditioners fundamentally expanding the cohort of households whose cooling system acquisition is financially enabled and behaviorally motivated by the simultaneous availability of public subsidy mechanisms, building envelope improvement activity, and electrification transition incentives across the national residential geography.

The programmatic scale of this trend is documented by Portugal's Fundo Ambiental. The E-LAR programme launched on 5 August 2025 with EUR 30 million targeting replacement of gas equipment with efficient electric solutions across mainland Portugal directly channels household electrification investment toward split system cooling products. Simultaneously, the Bairros + Sustentáveis programme's EUR 60 million allocation targeting 3,500 residential unit renovations by June 2026 in Lisbon and Porto creates a concentrated, high-conversion first-installation demand cohort within Portugal's most underserved residential cooling market segments through 2032.

Portugal Room Air Conditioners Market OpportunityDeep Residential Building Inefficiency Creates a Large Upgrade Demand Base

The profound structural energy inefficiency of Portugal's existing residential building stock combined with the accelerating pace of renovation funding deployment and rising household cooling motivation driven by climatic intensification represents the market's most significant and commercially durable opportunity, providing a large and progressively upgrade-motivated demand base whose conversion into active room air conditioner purchasing is being systematically enabled by the convergence of public funding programs and building envelope improvement activity.

The quantitative scale of this opportunity is established by the European Commission and Portugal's Fundo Ambiental. With over 75% of Portuguese residential buildings carrying an energy rating of C or lower and approximately 17.5% of the population still experiencing difficulty heating their homes, the structural scale of the residential comfort infrastructure deficit is substantial and geographically pervasive. The more than 85,000 residential energy renovations already completed nationally confirm the operational momentum of the conversion pipeline positioning suppliers with competitive pricing, efficiency credibility, and accessible installation networks to capture disproportionate value through 2032.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Portugal Room Air Conditioners Market Segmentation Analysis

By Product Type

- Split Air Conditioners

- Up to 9,000 BTU/h

- 9,001-12,000 BTU/h

- 12,001-18,000 BTU/h

- 18,001-24,000 BTU/h

- Above 24,000 BTU/h

- Window Air Conditioners

- Up to 9,000 BTU/h

- 9,001-12,000 BTU/h

- 12,001-18,000 BTU/h

- 18,001-24,000 BTU/h

- Above 24,000 BTU/h

- Others

The segment commanding the highest market share within the product type dimension is Split Air Conditioners, accounting for approximately 85% of total Portugal room air conditioners market value. This near-dominant position reflects the deep structural alignment between split system technology and the specific installation and comfort management requirements of Portuguese residential housing typologies where compact, wall-mounted configurations requiring no whole-building infrastructure modification make split systems the unambiguous product of choice across urban apartments, family homes, and retrofit installation environments. With four-fifths of total market value concentrated within a single format, split air conditioners define the entire competitive, commercial, and regulatory agenda of the Portugal room air conditioners market.

The structural leadership of split air conditioners is actively reinforced by the European Commission's ecodesign requirements establishing mandatory minimum energy performance standards, maximum sound level thresholds, and comprehensive product information obligations for air conditioners with rated cooling capacity of 12 kW or below, a specification range encompassing the vast majority of Portugal's residential split system market. These regulatory requirements create a compliance differentiation axis that progressively disadvantages lower-efficiency legacy portfolios while generating sustainable competitive advantage for brands with certified, high-efficiency split system offerings. The segment's commanding position as the primary revenue contributor and competitive focal point is expected to remain structurally intact through 2032.

By End User

- Residential

- Individual Households

- Apartments/Condominiums

- Vacation/Secondary Homes

- Commercial

- Offices

- Retail Stores/Showrooms

- Hospitality

- Healthcare Facilities

- Educational Institutions

- Small Commercial Establishments

- Others

The segment commanding the highest market share within the end user dimension is Residential, accounting for approximately 75% of total Portugal room air conditioners market value. This dominant position confirms household-based cooling demand as the category's primary commercial engine where purchase decisions are motivated by recurring summer heat discomfort, indoor thermal management necessity across extended high-temperature seasons, and the progressive normalization of room-level cooling as a standard residential comfort infrastructure expectation. With three-quarters of total market revenue anchored in residential consumption, the category's commercial trajectory is structurally inseparable from the behavioral and climatic dynamics shaping Portuguese household cooling adoption.

The structural centrality of residential demand is validated by the European Commission's documentation of over 75% of Portuguese residential buildings carrying an energy rating of C or lower alongside Portugal's Fundo Ambiental's Bairros and Sustentáveis programme carrying EUR 60 million and targeting renovation of 3,500 residential units by June 2026 in energy-poverty areas of Lisbon and Porto. These converging renovation and upgrade dynamics create a high-conversion first-installation demand cohort among households simultaneously improving building envelopes and comfort infrastructure. The residential segment's structural dominance as the market's primary demand anchor is expected to deepen progressively through 2032.

List of Companies Covered in Portugal Room Air Conditioners Market

The companies listed below are highly influential in the Portugal room air conditioners market, with a significant market share and a strong impact on industry developments.

- Haier Group

- Gree Electric Appliances Inc of Zhuhai

- Panasonic Corp

- Daikin Industries Ltd

- Mitsubishi Electric Corp

- Midea Group Co Ltd

- LG Corp

- Samsung Corp

- Fujitsu Ltd

- Whirlpool Corp

Market News & Updates

- Daikin Industries Ltd, 2026:

Daikin Portugal entered 2026 by being named the No. 1 air-conditioning brand in “Escolha do Consumidor 2026” for the second consecutive year, with Daikin stating that the award drew on more than 260,000 evaluations from 12,592 Portuguese consumers and that it stood out on price/quality, innovation and trust. For Portugal’s room-AC market, that is a meaningful competitive development because it strengthens installer and channel confidence around Daikin’s residential split offering, supports premium positioning in a market that values efficiency and reliability, and raises the hurdle for challengers trying to win share without matching Daikin on both product perception and brand reassurance at the point of sale.

- LG Corp, 2025:

LG’s Portuguese site is actively rolling out the new DUALCOOL AI/Premium residential split range, with official model pages highlighting AI Air with presence sensing, Soft Air, Dual Vane, proactive energy control, All Cleaning and ThinQ app integration, while also presenting the lineup as a newly arrived air-conditioner family for Portugal. The significance for the Portuguese market is that LG is reinforcing the shift toward connected inverter room AC that cools, heats and manages indoor comfort more intelligently, which should accelerate premiumization in residential demand by making app control, airflow personalization and energy optimization more central to purchase decisions rather than secondary add-ons

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Portugal Room Air Conditioners Market Policies, Regulations, and Standards

- Portugal Room Air Conditioners Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Portugal Room Air Conditioners Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold in Thousand Units

- Market Segmentation & Growth Outlook

- By Product Type

- Split Air Conditioners- Market Insights and Forecast 2022-2032, USD Million

- Up to 9,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- 9,001-12,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- 12,001-18,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- 18,001-24,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- Above 24,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- Window Air Conditioners- Market Insights and Forecast 2022-2032, USD Million

- Up to 9,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- 9,001-12,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- 12,001-18,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- 18,001-24,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- Above 24,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Split Air Conditioners- Market Insights and Forecast 2022-2032, USD Million

- By Technology

- Inverter- Market Insights and Forecast 2022-2032, USD Million

- Non-Inverter- Market Insights and Forecast 2022-2032, USD Million

- By Price

- Up to USD 300- Market Insights and Forecast 2022-2032, USD Million

- USD 301 to USD 600- Market Insights and Forecast 2022-2032, USD Million

- USD 601 to USD 1,000- Market Insights and Forecast 2022-2032, USD Million

- Above USD 1,000- Market Insights and Forecast 2022-2032, USD Million

- By End User

- Residential- Market Insights and Forecast 2022-2032, USD Million

- Individual Households- Market Insights and Forecast 2022-2032, USD Million

- Apartments/Condominiums- Market Insights and Forecast 2022-2032, USD Million

- Vacation/Secondary Homes- Market Insights and Forecast 2022-2032, USD Million

- Commercial- Market Insights and Forecast 2022-2032, USD Million

- Offices- Market Insights and Forecast 2022-2032, USD Million

- Retail Stores/Showrooms- Market Insights and Forecast 2022-2032, USD Million

- Hospitality- Market Insights and Forecast 2022-2032, USD Million

- Healthcare Facilities- Market Insights and Forecast 2022-2032, USD Million

- Educational Institutions- Market Insights and Forecast 2022-2032, USD Million

- Small Commercial Establishments- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Residential- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- Brand-Owned Websites/D2C- Market Insights and Forecast 2022-2032, USD Million

- E-Commerce Marketplaces- Market Insights and Forecast 2022-2032, USD Million

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- Exclusive Brand Stores- Market Insights and Forecast 2022-2032, USD Million

- Multi-Brand Electronics & Appliance Stores- Market Insights and Forecast 2022-2032, USD Million

- Specialty Stores- Market Insights and Forecast 2022-2032, USD Million

- Hypermarkets/Supermarkets- Market Insights and Forecast 2022-2032, USD Million

- Home Improvement Stores- Market Insights and Forecast 2022-2032, USD Million

- Dealer/Distributor Network- Market Insights and Forecast 2022-2032, USD Million

- Direct Sales/Institutional Sales- Market Insights and Forecast 2022-2032, USD Million

- Local Independent Retailers- Market Insights and Forecast 2022-2032, USD Million

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- By Refrigerant Type

- R-32- Market Insights and Forecast 2022-2032, USD Million

- R-410A- Market Insights and Forecast 2022-2032, USD Million

- R-290- Market Insights and Forecast 2022-2032, USD Million

- R-454B- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Connectivity

- Smart/Connected- Market Insights and Forecast 2022-2032, USD Million

- Conventional/Non-Smart- Market Insights and Forecast 2022-2032, USD Million

- By Energy Efficiency

- 1 Star- Market Insights and Forecast 2022-2032, USD Million

- 2 Star- Market Insights and Forecast 2022-2032, USD Million

- 3 Star- Market Insights and Forecast 2022-2032, USD Million

- 4 Star- Market Insights and Forecast 2022-2032, USD Million

- 5 Star- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Product Type

- Market Size & Growth Outlook

- Portugal Split Air Conditioners Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold in Thousand Units

- Market Segmentation & Growth Outlook

- By Technology- Market Insights and Forecast 2022-2032, USD Million

- By Price- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Refrigerant Type- Market Insights and Forecast 2022-2032, USD Million

- By Connectivity- Market Insights and Forecast 2022-2032, USD Million

- By Energy Efficiency- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Portugal Window Air Conditioners Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold in Thousand Units

- Market Segmentation & Growth Outlook

- By Technology- Market Insights and Forecast 2022-2032, USD Million

- By Price- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Refrigerant Type- Market Insights and Forecast 2022-2032, USD Million

- By Connectivity- Market Insights and Forecast 2022-2032, USD Million

- By Energy Efficiency- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Daikin Industries Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Mitsubishi Electric Corp

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Midea Group Co Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- LG Corp

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Samsung Corp

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Haier Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Gree Electric Appliances Inc of Zhuhai

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Panasonic Corp

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Fujitsu Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Whirlpool Corp

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Daikin Industries Ltd

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Technology |

|

| By Price |

|

| By End User |

|

| By Sales Channel |

|

| By Refrigerant Type |

|

| By Connectivity |

|

| By Energy Efficiency |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.