Poland Sleep Aids Market Report: Trends, Growth and Forecast (2026-2032)

By Product (Single Ingredient (Doxylamine Succinate, Diphenhydramine, Melatonin), Combination Ingredient (Diphenhydramine + Acetaminophen, Other Antihistamine-Based Combinations), Herbal & Traditional Sleep Aids (Valerian root, Passionflower, Chamomile, Kava, Multi-Herbal Sleep Blends)), By Sleep Disorder (Insomnia, Sleep Apnea, Restless Legs Syndrome, Narcolepsy, Sleep Walking, Others), By Age Group (Young to Mid Adults (25-44 Years), Middle-Aged Adults (45-64 Years), Geriatric Population (65+ Years)), By Sales Channel (Retail Online, Retail Offline), By End User (Homecare/Individual Consumers, Hospitals, Sleep Centers & Clinics), By Formulation (Tablets, Gummies, Capsules, Liquid, Sublingual) ... Read more

|

Major Players

|

Poland Sleep Aids Market Statistics and Insights, 2026

- Market Size Statistics

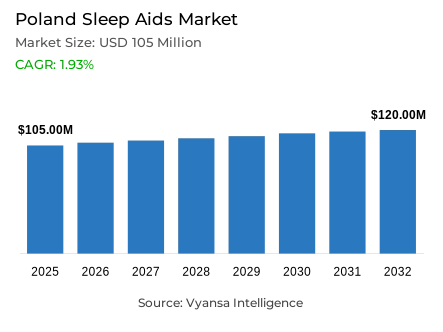

- Sleep aids market size in Poland was estimated at USD 105 million in 2025.

- The market size is expected to grow to USD 120 million by 2032.

- Market to register a CAGR of around 1.93% during 2026-32.

- Product Shares

- Single ingredient grabbed market share of 45%.

- Competition

- More than 10 companies are actively engaged in producing sleep aids in Poland.

- Top 5 companies acquired around 60% of the market share.

- Herbapol Lublin SA, Nepentes Pharma Sp zoo, PPF Hasco-Lek SA, GSK Consumer Healthcare, Axellus Sp zoo etc., are few of the top companies.

- Sales channel

- Retail offline grabbed 70% of the market.

Poland Sleep Aids Market Outlook

The Poland sleep aids market continues to register steady value growth, supported by persistent lifestyle-related stress and rising awareness of insomnia management. The market is valued at USD 105 million in 2025 and is projected to reach USD 120 million by 2032, reflecting a CAGR of 1.93%. While overall volume growth remains moderate, value expansion is driven by sustained consumer reliance on over-the-counter solutions to manage anxiety-related sleep disruption and improve daily functioning.

Consumer preference is increasingly oriented toward natural and herbal formulations, which account for a significant portion of value sales. Vitamin B complexes and botanical blends are perceived as safer long-term options. At the same time, synthetic substances such as doxylamine maintain demand among users seeking rapid symptom relief for acute insomnia, creating a dual-structured market split between gentle, routine support and short-term efficacy-driven solutions.

Product innovation plays a critical competitive role. Polish consumers are receptive to alternative delivery formats including mouth sprays, chewable tablets, and gummies that emphasize faster absorption and convenience. Interest in cannabidiol-based solutions is rising among younger demographics, although broader uptake remains moderated by dependency concerns.

sales channel remains heavily concentrated in Retail Offline channels, particularly pharmacies, which provide professional reassurance and guidance. However, digital platforms and sleep-tracking technologies are gradually influencing purchasing behavior, integrating sleep aids into a broader, technology-enabled wellness framework expected to evolve further by 2032.

Poland Sleep Aids Market Growth DriverElevated Stress Levels Sustain Consistent Demand for Nighttime Sleep Relief

Elevated stress and anxiety levels continue to sustain demand for short-term sleep support solutions in Poland. Insomnia linked to work pressure and adjustment disorders reinforces the relevance of easily accessible, pharmacy-available products that do not require formal medical appointments. End users display dual preferences milder herbal formulations for routine stress management and faster-acting synthetic preparations when sleep disruption becomes acute.

Data from the Polish Social Insurance Institution (ZUS) confirm the structural nature of stress-related burden. In 2024, reactions to severe stress and adjustment disorders accounted for 35.3% of all medical certificates issued for mental and behavioural disorders. The number of such certificates increased by 18.6%, while associated sick-leave days rose by 21.6% compared to 2023. These figures substantiate the scale of work-related psychological strain, providing a clear foundation for continued demand for convenient nighttime relief solutions.

Poland Sleep Aids Market ChallengeDietary Supplement Growth Exerts Competitive Pressure on Conventional Sleep Aid Formats

The rapid normalization of dietary supplement consumption is redirecting part of demand away from conventional sleep medicines. A growing segment of end users prefers vitamin-based and multi-ingredient supplement formulations over traditional pharmacological sleep aids, perceiving them as gentler and safer for regular use. This substitution dynamic places competitive pressure on established OTC sleep formats.

A nationally representative survey published in Frontiers in Nutrition in December 2025, covering 5,006 Polish adults, found that 39.1% reported regular supplement use in the previous three months and 31.5% reported occasional use. The combined prevalence illustrates how supplements have become embedded in daily health routines, increasing competitive displacement risk for traditional sleep aid products that lack strong natural positioning or differentiated value propositions.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Poland Sleep Aids Market TrendFast-Acting Antihistamine Formulations Gain Market Visibility

Doxylamine-based sleep aids are increasingly visible in the Polish pharmacy landscape, reflecting demand for rapid-onset, short-term solutions. These products address occasional insomnia episodes linked to stress and anxiety while maintaining a defined and limited usage window, which aligns with consumer preference for controlled self-medication.

Product registration data illustrate this positioning. Dorminox is approved in Poland with 12.5 mg of doxylamine hydrogenosuccinate per tablet, with a recommended starting dose of 12.5 mg and a maximum daily dose of 25 mg. Usage is generally limited to up to seven days without medical consultation. This clearly defined dosing framework reinforces trust and supports short-duration use, sustaining relevance within a diversified competitive environment.

Poland Sleep Aids Market OpportunityCannabidiol-Based Sleep Formulations Create a New Space for Product Differentiation

Cannabidiol-based sleep products present a notable differentiation opportunity, particularly among younger adults seeking alternatives perceived as more natural than conventional hypnotics. Properly formulated CBD solutions emphasizing transparent dosing, non-habit-forming positioning, and pharmacy guidance can attract experimentation without triggering concerns associated with stronger pharmaceutical interventions.

However, trust barriers remain material. A national survey conducted in July 2025 among 1,113 Polish adults found that 32.4% expressed concern that legalization of medical cannabis could encourage recreational use. This sensitivity underscores the importance of responsible communication, pharmacist education, and compliance-driven branding. Companies that proactively address safety perceptions and dosing clarity are positioned to convert curiosity into sustained repeat purchasing and long-term category engagement.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Poland Sleep Aids Market Segmentation Analysis

By Product

- Single Ingredient

- Combination Ingredient

- Herbal & Traditional Sleep Aids

The segment with highest market share under Product is Single-Ingredient products, accounting for approximately 45% of total market share. The prominence of mono-substances such as melatonin and doxylamine underpins this leadership, as consumers associate them with predictable and targeted efficacy. Simplicity of formulation and transparent labeling enhance user confidence, particularly among individuals cautious of complex multi-ingredient blends.

Although herbal and multivitamin supplements are gaining visibility, single-ingredient products remain preferred for addressing specific sleep latency challenges. Established safety profiles and strong brand recognition reinforce this segment’s anchor position within the Polish market. Ongoing innovation in delivery forms, including sprays and gummies, is expected to further sustain regular usage of single-ingredient solutions through 2032.

By Sales Channel

- Retail Online

- Retail Offline

Retail Offline holds approximately 70% of total market share, maintaining its leadership position in sales channel. Physical pharmacies form the backbone of this channel, as Polish consumers value pharmacist consultation when evaluating product safety, dosage, and short-term use considerations. This reassurance is particularly important given persistent sensitivity around dependency risks and transitions from prescription to OTC options.

Despite growing use of retai online for research and price comparison, final purchases predominantly occur in physical stores. Immediate access during acute sleep disruption episodes strengthens offline relevance. Supported by trust, professional advisory services, and convenient availability, Retail Offline is expected to remain the dominant sales channel in Poland through 2032.

List of Companies Covered in Poland Sleep Aids Market

The companies listed below are highly influential in the Poland sleep aids market, with a significant market share and a strong impact on industry developments.

- Herbapol Lublin SA

- Nepentes Pharma Sp zoo

- PPF Hasco-Lek SA

- GSK Consumer Healthcare

- Axellus Sp zoo

- Zakłady Farmaceutyczne Polpharma SA

- Aflofarm Farmacja Polska Sp zoo

- Innowacyjno-Wdrożeniowe Laboratorium Farmaceutyczne Labofarm Mgr Farm Tadeusz Pawelek

- Farmak Sp zoo

- Procter & Gamble Operations Polska Sp zoo

Competitive Landscape

Poland sleep aids market is features a fragmented but competitive landscape, with Dorminox leading the doxylamine-based segment, leveraging its positioning as a fast-acting and effective solution for insomnia and anxiety. Herbal/traditional products account for a larger share of value sales, reflecting consumer preference for perceived safer, plant-based remedies over synthetic or prescription options. However, OTC sleep aids face intensifying indirect competition from vitamins and dietary supplements, particularly vitamin B combinations positioned as gentler sleep-support solutions. Emerging CBD-based offerings are gaining traction among consumers under 34, though concerns about dependency remain a barrier. Key differentiation opportunities lie in novel delivery formats such as chewables and sprays, flavour innovation, and clear communication around safety, non-addictive properties, and stress-related sleep support.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Poland Sleep Aids Market Policies, Regulations, and Standards

- Poland Sleep Aids Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Poland Sleep Aids Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product

- Single Ingredient- Market Insights and Forecast 2022-2032, USD Million

- Doxylamine Succinate- Market Insights and Forecast 2022-2032, USD Million

- Diphenhydramine- Market Insights and Forecast 2022-2032, USD Million

- Melatonin- Market Insights and Forecast 2022-2032, USD Million

- Combination Ingredient- Market Insights and Forecast 2022-2032, USD Million

- Diphenhydramine + Acetaminophen- Market Insights and Forecast 2022-2032, USD Million

- Other Antihistamine-Based Combinations- Market Insights and Forecast 2022-2032, USD Million

- Herbal & Traditional Sleep Aids- Market Insights and Forecast 2022-2032, USD Million

- Valerian root- Market Insights and Forecast 2022-2032, USD Million

- Passionflower- Market Insights and Forecast 2022-2032, USD Million

- Chamomile- Market Insights and Forecast 2022-2032, USD Million

- Kava- Market Insights and Forecast 2022-2032, USD Million

- Multi-Herbal Sleep Blends- Market Insights and Forecast 2022-2032, USD Million

- Single Ingredient- Market Insights and Forecast 2022-2032, USD Million

- By Sleep Disorder

- Insomnia- Market Insights and Forecast 2022-2032, USD Million

- Sleep Apnea- Market Insights and Forecast 2022-2032, USD Million

- Restless Legs Syndrome- Market Insights and Forecast 2022-2032, USD Million

- Narcolepsy- Market Insights and Forecast 2022-2032, USD Million

- Sleep Walking- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Age Group

- Young to Mid Adults (25-44 Years)- Market Insights and Forecast 2022-2032, USD Million

- Middle-Aged Adults (45-64 Years)- Market Insights and Forecast 2022-2032, USD Million

- Geriatric Population (65+ Years)- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- By End User

- Homecare/Individual Consumers- Market Insights and Forecast 2022-2032, USD Million

- Hospitals- Market Insights and Forecast 2022-2032, USD Million

- Sleep Centers & Clinics- Market Insights and Forecast 2022-2032, USD Million

- By Formulation

- Tablets- Market Insights and Forecast 2022-2032, USD Million

- Gummies- Market Insights and Forecast 2022-2032, USD Million

- Capsules- Market Insights and Forecast 2022-2032, USD Million

- Liquid- Market Insights and Forecast 2022-2032, USD Million

- Sublingual- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Product

- Market Size & Growth Outlook

- Poland Single Ingredient Sleep Aids Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Sleep Disorder- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Formulation- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Poland Combination Ingredient Sleep Aids Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Sleep Disorder- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Formulation- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Poland Herbal & Traditional Sleep Aids Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Sleep Disorder- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Formulation- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- GSK Consumer Healthcare

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Axellus Sp zoo

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Zaklady Farmaceutyczne Polpharma SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Aflofarm Farmacja Polska Sp zoo

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Innowacyjno-Wdrozeniowe Laboratorium Farmaceutyczne Labofarm Mgr Farm Tadeusz Pawelek

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Herbapol Lublin SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Nepentes Pharma Sp zoo

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- PPF Hasco-Lek SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Farmak Sp zoo

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Procter & Gamble Operations Polska Sp zoo

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- GSK Consumer Healthcare

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product |

|

| By Sleep Disorder |

|

| By Age Group |

|

| By Sales Channel |

|

| By End User |

|

| By Formulation |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.