Philippines Paediatric Consumer Health Market Report: Trends, Growth and Forecast (2026-2032)

By Product Type (Paediatric Analgesics (Paediatric Acetaminophen, Paediatric Aspirin, Paediatric Combination Products Analgesics, Paediatric Dipyrone, Paediatric Ibuprofen, Paediatric Naproxen), Paediatric Cough, Cold and Allergy Remedies (Paediatric Allergy Remedies, Paediatric Cough/Cold Remedies), Paediatric Digestive Remedies (Paediatric Diarrhoeal Remedies, Paediatric Indigestion and Heartburn Remedies, Paediatric Laxatives, Paediatric Motion Sickness Remedies), Paediatric Dermatologicals, Nappy (Diaper) Rash Treatments, Paediatric Vitamins and Dietary Supplements), By Dosage Form (Liquid Syrups, Chewable Tablets, Drops, Powders/Sachets, Gummies, Topical Creams & Ointments), By Age Group (Infants & Toddlers (0-3 Years), Children (4-12 Years), Adolescents (13-18 Years)), By Treatment Type (Acute Treatment, Chronic Condition Management, Genetic & Rare Disease Management), By Sales Channel (Retail Online (Online Pharmacies, E-commerce Platforms, Brand Websites), Retail Offline (Hospital Pharmacies, Retail Pharmacies / Drugstores, Supermarkets & Hypermarkets, Specialty Baby Stores)) ... Read more

|

Major Players

|

Philippines Paediatric Consumer Health Market Statistics and Insights, 2026

- Market Size Statistics

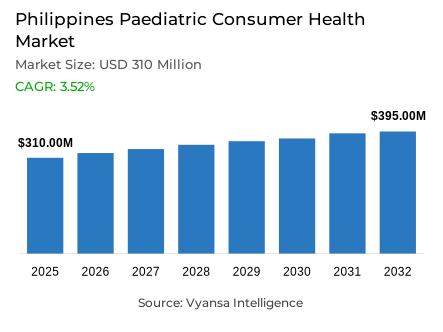

- Paediatric consumer health market size in Philippines was valued at USD 310 million in 2025 and is estimated at USD 329.81 Million in 2026.

- The market size is expected to grow to USD 395 million by 2032.

- Market to register a CAGR of around 3.52% during 2026-32.

- Product Type Shares

- Paediatric vitamins and dietary supplements grabbed market share of 60%.

- Competition

- More than 10 companies are actively engaged in producing paediatric consumer health in Philippines.

- Top 5 companies acquired around 75% of the market share.

- UHS Essential Health Philippines Inc, Amway Philippines LLC, Foundation Consumer Healthcare LLC, United Laboratories Inc, Taisho Pharmaceutical (Philippines) Inc etc., are few of the top companies.

- Sales Channel

- Retail offline grabbed 90% of the market.

Philippines Paediatric Consumer Health Market Outlook

The Philippines paediatric consumer health market was valued at USD 310 million in 2025 and is projected to grow from USD 329.81 million in 2026 to USD 395 million by 2032, reflecting a compound annual growth rate of 3.52% over the forecast period. Growth remains well-supported by the country's relatively high birth rate and the strong and consistent tendency of Filipino families to prioritise spending on children's health and physical wellbeing above most other household discretionary categories.

A significant portion of this expansion is driven by paediatric vitamins and dietary supplements, which hold 60% of the total market. Parents remain highly focused on maintaining their children's physical health, sustaining strong demand for immunity-supporting supplements and products linked to general wellness and growth. Interest in height-related supplement brands also remains commercially visible, reinforced by school-based activities and brand-led community engagement efforts that keep these products front of mind among caregiving households.

Purchasing behaviour across the category is evolving in meaningful ways. Loyalty and membership programmes are becoming more influential in driving repeat purchases, particularly among mothers who actively seek cost-saving opportunities. Brands are integrating paediatric consumer health products into retail online strategies through targeted incentives, while pharmacy networks and digital payment platforms are helping to strengthen end user engagement and encourage consistent repurchase behaviour.

Retail Offline accounts for 90% of total market sales, confirming that physical channels continue to dominate the category. At the same time, paediatric consumer health is seeing growing momentum from probiotics, child-friendly product formats, and increasing parental attention to children's eye care as screen-based activity becomes more embedded in both education and recreation across the country.

Philippines Paediatric Consumer Health Market Growth DriverA Large and Renewing Child Population Keeps Preventive Health Demand Active

The child population in the Philippines has one of the most stable bases for commercial foundation as it relates to paediatric consumer health. Parents are consistently directing their total expenditures on vitamins, supplements and everyday wellness products for their children to preventative solutions that are associated with immunity, physical growth and overall development, and that therefore sustain activity in that category and investment in those brands regardless of the economic environment as a whole.

Registered births in the Philippines reached 1,345,087 from January to December 2024, as reported by the Philippine Statistics Authority as of 30 July 2025. Total population stood at 112,729,484 as of 1 July 2024. This large and continuously renewing end user base provides a stable, long-term foundation for child-focused health products particularly those positioned around immunity support, healthy growth, and sustained physical wellbeing throughout childhood.

Philippines Paediatric Consumer Health Market ChallengeGrowing Category Saturation Is Slowing Supplement Momentum

Paediatric vitamins and dietary supplements remain the category's most commercially significant segment. Saturation, however, is making it progressively harder for standard product offerings to generate the level of end user interest they once produced. Parents across the Philippines accept vitamins as routine but the category has become crowded, and evolving expectations around format, taste, and functional specificity are raising the bar for what constitutes a compelling product.

Real pressure now falls on brands to move beyond broad immunity-support positioning. Format matters. Gummies, powders, syrups, and dropper presentations are becoming baseline expectations rather than differentiators. Without sustained product innovation, paediatric vitamin brands face a more difficult path to purchase conversion in a category where a growing share of households are experienced supplement users. These households are becoming considerably more selective, and a familiar product in a standard format generates less response than it once did.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Philippines Paediatric Consumer Health Market TrendDigital Loyalty Ecosystems Are Reshaping the Paediatric Purchase Journey

Loyalty programmes and digitally enabled purchasing pathways are reshaping how end users discover, evaluate, and repeatedly buy child health products in the Philippines. Mothers, in particular, respond strongly to cost-saving offers, reward points, and pharmacy-linked purchase incentives. As digital payment infrastructure and household internet access continue to expand, this behaviour is becoming both more powerful and more commercially scalable.

In 2024, digital payments accounted for 57.4% of total monthly retail payment volume, according to the Bangko Sentral ng Pilipinas. Household internet access reached 48.8% in the same period, while 67.3% of individuals aged 10 years and above used the internet during 2024, as reported by the Philippine Statistics Authority. Together, these conditions are strengthening digitally assisted purchasing behaviour across paediatric health categories. Loyalty-led retail online channels are an increasingly important route for repeat purchases of child-focused vitamins, supplements, and general health products.

Philippines Paediatric Consumer Health Market OpportunityRising Screen Exposure Is Opening a New Commercial Space in Paediatric Eye Care

A well-defined commercial opening is emerging within paediatric eye care. Digital media has become deeply embedded in daily childhood routines across the Philippines, and parents are becoming more attentive to visual strain and screen-related eye discomfort as devices are used for longer durations in both educational and recreational contexts. This awareness is generating demand for eye care products designed specifically for children and positioned around preventive visual health support.

Among individuals aged 10 years and above, 67.3% used the internet in 2024, with average daily time spent online reaching 4.6 hours, according to the Philippine Statistics Authority. Screen exposure is now a routine feature of childhood across Filipino households. Paediatric eye care holds a credible and growing commercial position as parents actively seek practical solutions to protect their children's visual health before screen-related concerns develop into more serious conditions.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Philippines Paediatric Consumer Health Market Segmentation Analysis

By Product Type

- Paediatric Analgesics

- Paediatric Acetaminophen

- Paediatric Aspirin

- Paediatric Combination Products Analgesics

- Paediatric Dipyrone

- Paediatric Ibuprofen

- Paediatric Naproxen

- Paediatric Cough, Cold and Allergy Remedies

- Paediatric Allergy Remedies

- Paediatric Cough/Cold Remedies

- Paediatric Digestive Remedies

- Paediatric Diarrhoeal Remedies

- Paediatric Indigestion and Heartburn Remedies

- Paediatric Laxatives

- Paediatric Motion Sickness Remedies

- Paediatric Dermatologicals

- Nappy (Diaper) Rash Treatments

- Paediatric Vitamins and Dietary Supplements

The segment with highest market share under Product Type is Paediatric Vitamins and Dietary Supplements,accounting for 60% of the total market. This leadership position reflects the central role of preventive care in Filipino parenting culture. Parents regard supplements as a practical and accessible mechanism for supporting children's immunity, physical growth, and daily nutritional intake. These products integrate naturally into established family health routines and address nutritional gaps in a way parents view as straightforward and dependable.

Broad applicability across diverse child health concerns strengthens the segment's commercial position further. Height development, immunity strengthening, and daily nutritional support are all purchase drivers within the same category. Child-friendly delivery formats and active brand engagement initiatives reinforce consistent product use. Compared with more occasional remedy categories, paediatric vitamins and dietary supplements benefit from wider and more frequent usage occasions a structural advantage that keeps them commercially dominant within the overall product mix.

By Sales Channel

- Retail Online

- Online Pharmacies

- E-commerce Platforms

- Brand Websites

- Retail Offline

- Hospital Pharmacies

- Retail Pharmacies / Drugstores

- Supermarkets & Hypermarkets

- Specialty Baby Stores

The segment with highest market share under Sales Channel is Retail Offline, accounting for 90% of the total market. Physical channels remain the primary and most trusted purchasing destination for paediatric consumer health products across the Philippines. Pharmacies and established offline retail outlets serve as the default point of purchase for parents buying children's health products. Immediate product availability, brand familiarity, and direct access to pharmacy staff each contribute meaningfully to the purchase decision.

Routine purchasing behaviour reinforces offline dominance further. Many families incorporate paediatric health product purchases into regular pharmacy visits, allowing them to quickly compare available options and access familiar products at the point of need. Retail online channels and loyalty-linked digital purchasing are gaining influence within the category yet physical retail retains higher end user trust, greater purchase convenience, and the strength of long-established consumer habits. These factors keep it firmly positioned as the primary commercial channel for paediatric consumer health products across the Philippines.

List of Companies Covered in Philippines Paediatric Consumer Health Market

The companies listed below are highly influential in the Philippines paediatric consumer health market, with a significant market share and a strong impact on industry developments.

- UHS Essential Health Philippines Inc

- Amway Philippines LLC

- Foundation Consumer Healthcare LLC

- United Laboratories Inc

- Taisho Pharmaceutical (Philippines) Inc

- Haleon Philippines Inc

- Tynor Drug House Inc

- Sanofi-Aventis Philippines Inc

- Reckitt Benckiser (Philippines) Inc

- The Generics Pharmacy

Competitive Landscape

The competitive landscape of paediatric consumer health in the Philippines is shaped by strong demand, brand trust, and innovation, with paediatric vitamins and dietary supplements leading category performance. Major players such as Unilab and GSK strengthen their position through loyalty and membership programmes integrated with e-commerce, pharmacies like Mercury Drug, and digital wallets such as GCash, helping drive repeat purchases among value-conscious mothers. Competition is also influenced by medical credibility, as brands increasingly partner with paediatricians to create educational content and build consumer confidence. However, the vitamins segment is nearing saturation, pushing companies to innovate through gummies, syrups, powders, and droppers. Growth opportunities are rising in paediatric probiotics and children’s eye care, supported by digestive health awareness and increasing screen time among children.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Philippines Paediatric Consumer Health Market Policies, Regulations, and Standards

- Philippines Paediatric Consumer Health Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Philippines Paediatric Consumer Health Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product Type

- Paediatric Analgesics- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Acetaminophen- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Aspirin- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Combination Products Analgesics- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Dipyrone- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Ibuprofen- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Naproxen- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Cough, Cold and Allergy Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Allergy Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Cough/Cold Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Digestive Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Diarrhoeal Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Indigestion and Heartburn Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Laxatives- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Motion Sickness Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Dermatologicals- Market Insights and Forecast 2022-2032, USD Million

- Nappy (Diaper) Rash Treatments- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Vitamins and Dietary Supplements- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Analgesics- Market Insights and Forecast 2022-2032, USD Million

- By Dosage Form

- Liquid Syrups- Market Insights and Forecast 2022-2032, USD Million

- Chewable Tablets- Market Insights and Forecast 2022-2032, USD Million

- Drops- Market Insights and Forecast 2022-2032, USD Million

- Powders/Sachets- Market Insights and Forecast 2022-2032, USD Million

- Gummies- Market Insights and Forecast 2022-2032, USD Million

- Topical Creams & Ointments- Market Insights and Forecast 2022-2032, USD Million

- By Age Group

- Infants & Toddlers (0-3 Years)- Market Insights and Forecast 2022-2032, USD Million

- Children (4-12 Years)- Market Insights and Forecast 2022-2032, USD Million

- Adolescents (13-18 Years)- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type

- Acute Treatment- Market Insights and Forecast 2022-2032, USD Million

- Chronic Condition Management- Market Insights and Forecast 2022-2032, USD Million

- Genetic & Rare Disease Management- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- Online Pharmacies- Market Insights and Forecast 2022-2032, USD Million

- E-commerce Platforms- Market Insights and Forecast 2022-2032, USD Million

- Brand Websites- Market Insights and Forecast 2022-2032, USD Million

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- Hospital Pharmacies- Market Insights and Forecast 2022-2032, USD Million

- Retail Pharmacies / Drugstores- Market Insights and Forecast 2022-2032, USD Million

- Supermarkets & Hypermarkets- Market Insights and Forecast 2022-2032, USD Million

- Specialty Baby Stores

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Product Type

- Market Size & Growth Outlook

- Philippines Paediatric Analgesics Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Dosage Form- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Philippines Paediatric Cough, Cold and Allergy Remedies Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Dosage Form- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Philippines Paediatric Digestive Remedies Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Dosage Form- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Philippines Paediatric Dermatologicals Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Dosage Form- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Philippines Nappy (Diaper) Rash Treatments Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Dosage Form- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Philippines Paediatric Vitamins and Dietary Supplements Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Dosage Form- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- United Laboratories Inc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Taisho Pharmaceutical (Philippines) Inc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Haleon Philippines Inc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Tynor Drug House Inc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Sanofi-Aventis Philippines Inc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- UHS Essential Health Philippines Inc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Amway Philippines LLC

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Foundation Consumer Healthcare LLC

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Reckitt Benckiser (Philippines) Inc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- The Generics Pharmacy

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- United Laboratories Inc

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Dosage Form |

|

| By Age Group |

|

| By Treatment Type |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.