Philippines Diagnostic Labs Market Report: Trends, Growth and Forecast (2026-2032)

By Lab Type (Single/Independent Laboratories, Hospital-based Laboratories, Physician Office Laboratories, Others), By Testing Services (Physiological Function Testing, General & Clinical Testing, Esoteric Testing, Specialized Testing, Non-invasive Prenatal Testing, COVID-19 Testing, Others), By Disease (Cardiology, Oncology, Neurology, Orthopedics, Gastroenterology, Gynecology, Odontology, Others), By Revenue Source (Healthcare Plan, Out-of-Pocket, Public System), By Test Type (Pathology, Radiology), By End User (Referrals, Walk-ins, Corporate Clients) ... Read more

|

Major Players

|

Philippines Diagnostic Labs Market Statistics and Insights, 2026

- Market Size Statistics

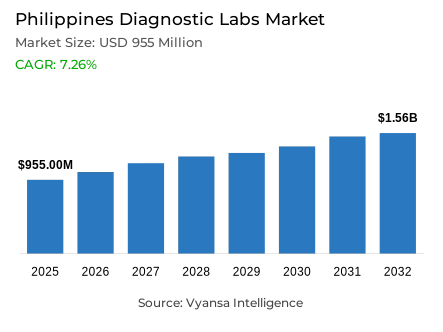

- Diagnostic labs market size in Philippines was estimated at USD 955 million in 2025.

- The market size is expected to grow to USD 1.56 billion by 2032.

- Market to register a CAGR of around 7.26% during 2026-32.

- Lab Type Shares

- Hospital-based laboratories grabbed market share of 50%.

- Competition

- Diagnostic labs in Philippines is currently being catered to by more than 10 companies.

- Top 5 companies acquired around 50% of the market share.

- iScan Diagnostic Center, Singapore Diagnostics, Accuteqs Diagnostics Laboratory, Hi Precision Diagnostics, LCM Diagnostics etc., are few of the top companies.

- Testing Services

- General & clinical testing grabbed 45% of the market.

Philippines Diagnostic Labs Market Outlook

The Philippines diagnostic labs market is positioned for steady expansion, valued at $955 million in 2025 and projected to reach $1.56 billion by 2032, growing at a CAGR of approximately 7.26% during 2026-32. This growth trajectory reflects increasing healthcare awareness and the government's push toward structured primary care delivery through initiatives like the PhilHealth Konsulta program. However, market expansion faces a significant constraint as out-of-pocket payments account for 44.4% of total health expenditure in 2023, creating affordability barriers that cause patients to postpone confirmatory tests or reduce preventive screening, directly impacting laboratory revenues and test volumes.

Hospital-based laboratories dominate the market with a 50% share, benefiting from their strategic position within hospital care pathways where they serve emergency departments, inpatient wards, and specialist clinics requiring rapid turnaround times for clinical decisions. Meanwhile, General & Clinical Testing commands 45% of testing services, driven by high-frequency, repeat-driven demand for routine diagnostics including diabetes monitoring, infection screening, kidney function tests, and lipid panels that form the foundation of preventive and chronic disease management.

Accreditation frameworks are reshaping competitive dynamics, with PhilHealth's payer-linked standards determining where test volumes concentrate. As of January 2026, 96 accredited COVID-19 testing labs (59 government, 37 private) demonstrate that market access increasingly depends on maintaining compliance readiness, quality system discipline, and audit preparedness. The PhilHealth Konsulta program's standardized basket of 25 targeted diagnostics—covering routine tests like HbA1c, serum creatinine, and CBC, plus imaging services—creates consistent demand patterns that favor laboratories capable of aligning workflows with covered screening requirements.

Strategic opportunities emerge as primary care transitions toward networked delivery models, with physicians coordinating up to 20,000 beneficiaries each. Laboratories positioned as network partners rather than standalone vendors are best placed to capture recurring screening volumes through outsourced contracts, integrated reporting systems, and standardized collection logistics throughout the forecast period.

Philippines Diagnostic Labs Market Growth Driver

Insurance Integration Reshaping Primary Care Testing Pathways

The Circular No. 2024-0022 of PhilHealth implements the guidelines of the PhilHealth Konsulta programme that is combined with the selected SDG-related benefit packages, thus making this initiative a stepping stone towards a more comprehensive outpatient benefit called Konsulta+. With the organisation of screening and follow-up procedures in the form of structured provider networks, diagnostic laboratories will become an inseparable part of the routine care delivery in the Philippines in the 2026-2032 period. Annex A2 of this circular standardises the demand of testing by defining 25 targeted diagnostics, based on the life stage and health assessment needs, including routine diagnostics (HbA1c, serum creatinine, lipid profile, and CBC) and imaging services (ultrasound and mammography).

This fixed, payer-based testing basket establishes predictable volumes of high-frequency panels and motivates laboratories to align their service menus and operational processes with covered screening needs, integrating diagnostic testing directly into the primary-care pathway as an non-optional element of routine health management.

Philippines Diagnostic Labs Market Challenge

Direct Payment Burden Constraining Testing Utilization Rates

One of the major market limitations is the large share of healthcare spending that the end users have to directly shoulder in case of test re-tests, additional diagnostics, or access restricted cases. This dynamic sustains very price-sensitive demand patterns in the diagnostic laboratory industry, with end users often delaying confirmatory testing services, narrowing the scope of preventive panels, or avoiding chronic condition monitoring cycles, which directly affect laboratory footfall and test mix composition in the Philippines in 2026-2032. The Philippine National Health Accounts analyzed by the government indicate that out-of-pocket payment is the most significant healthcare financing scheme in 2023, with 44.4% of the current health expenditure.

As almost half of all health expenditure is directly funded by household budgets, laboratories face a long-standing affordability challenge that specifically impacts repeat diagnostics and add-on tests of higher value that end users may deprioritize when constrained by budgets, limiting market growth opportunities despite increasing healthcare awareness.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Philippines Diagnostic Labs Market Trend

Accreditation Standards Driving Capacity Concentration Patterns

A strong market trend shows that payer-based accreditation models are becoming more and more influential in defining the location of diagnostic test volumes within the Philippines laboratory ecosystem. PhilHealth constantly revises accredited facility categories based on benefit package type, thus strengthening compliance requirements, documentation discipline and operational standards as the viable channel of accessing reimbursable diagnostic demand directly or through hospital and provider network arrangements. This trend is especially apparent in specialised testing segments, with the Status of Accreditation table of PhilHealth as of 31 January 2026 listing 96 accredited SARS-CoV-2 testing laboratories, including 59 governmental and 37 non-governmental operations.

This publicly monitored accredited laboratory base shows that recognised diagnostic capacity is still essentially linked to eligibility checks and continuous monitoring procedures, and keeps accreditation preparedness, such as renewals, audits, and quality system maintenance, as a key component of the strategic and operational playbook of laboratory operators during the forecast period.

Philippines Diagnostic Labs Market Opportunity

Network-Scale Primary Care Creating Partnership Infrastructure Opportunities

The emergence of significant market opportunities is seen as primary care delivery models shift to wider, networked operational frameworks throughout the Philippines healthcare environment. Within the Konsulta with SDG-related package design framework, healthcare services are provided by a primary provider in collaboration with related facilities, which provides a significant space to the diagnostic laboratories to win outsourced processing contracts, sample referral processes, and network-wide standardisation efforts including collection logistics, turnaround time discipline, and integration of reporting systems.

A maximum absorptive capacity of 20,000 beneficiaries per physician to serve Konsulta with SDG participants, as mentioned in Annex B of PhilHealth Circular No. 2024-0022, is inherently biased towards those laboratories that can handle high-throughput routine testing and smoothly incorporate the results into network information systems. Laboratories that are strategically located as network partners and not as independent service providers are best placed to win recurring screening and monitoring volumes in 2026-2032, as they are embedded in coordinated care delivery models.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Philippines Diagnostic Labs Market Segmentation Analysis

By Lab Type

- Single/Independent Laboratories

- Hospital-based Laboratories

- Physician Office Laboratories

- Others

Hospital-based Laboratories command 50% market share within the Lab Type segmentation, representing the highest share category due to hospitals functioning as central hubs within end user healthcare journeys encompassing emergency care, inpatient monitoring, surgical workups, and specialist outpatient department follow-ups. Since attending physicians and hospital wards require rapid turnaround times for clinical decision-making processes, in-house hospital laboratories naturally receive steady flows of both routine and urgent sample volumes.

In comparison, freestanding and independent laboratories compete primarily on convenience factors including walk-in access, extended operating hours, and home collection services, potentially attracting preventive healthcare end users. However, hospital-based laboratories continue deriving structural advantages from being embedded within hospital care pathways and institutional procurement processes, sustaining their dominant market position throughout the forecast period.

By Testing Services

- Physiological Function Testing

- General & Clinical Testing

- Esoteric Testing

- Specialized Testing

- Non-invasive Prenatal Testing

- COVID-19 Testing

- Others

General & Clinical Testing captures 45% market share within the Testing Services segmentation, representing the highest share category driven by repeat-driven, high-frequency testing patterns that support common clinical requirements including infection screening, diabetes tracking, kidney function assessments, lipid monitoring, and pre-employment or pre-procedure panels. For most end users, general testing represents the initial diagnostic step before any specialized referral consideration.

Specialized testing categories encompassing molecular diagnostics, genetic analysis, and advanced immunology retain importance but are utilized more selectively, often depending on specialist physician access and end user affordability considerations. Consequently, laboratories concentrate operational improvements on enhancing throughput capacity, quality consistency, and reporting speed for core clinical panel offerings that generate the majority of testing volumes and revenue streams.

List of Companies Covered in Philippines Diagnostic Labs Market

The companies listed below are highly influential in the Philippines diagnostic labs market, with a significant market share and a strong impact on industry developments.

- iScan Diagnostic Center

- Singapore Diagnostics

- Accuteqs Diagnostics Laboratory

- Hi Precision Diagnostics

- LCM Diagnostics

- Medi Linx Laboratory Inc.

- BioPATH Clinical Diagnostics Inc.

- PMP Diagnostic Center Inc.

- Biopath Clinical Diagnostics Inc.

- ASHREY Diagnostic Center

Market News & Updates

- Singapore Diagnostics, 2025:

Singapore Diagnostics was recognized at the Healthcare Asia Awards 2025 for digital innovation in laboratory workflow integration. This highlights continued investment in interoperable lab reporting systems and faster turnaround capabilities, strengthening its competitive positioning in the Philippines’ private diagnostics market.

- Hi-Precision Diagnostics, 2025:

Hi-Precision Diagnostics received the Platinum – Trusted Brand Award 2025, reinforcing its brand leadership in the Philippines’ outpatient diagnostic testing environment. In a cash-pay and HMO-driven market, brand recognition supports sustained walk-in volumes, repeat testing, and corporate tie-ups.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. Philippines Diagnostic Labs Market Policies, Regulations, and Standards

4. Philippines Diagnostic Labs Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. Philippines Diagnostic Labs Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in USD Million

5.2. Market Segmentation & Growth Outlook

5.2.1.By Lab Type

5.2.1.1. Single/Independent Laboratories- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Hospital-based Laboratories- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3. Physician Office Laboratories- Market Insights and Forecast 2022-2032, USD Million

5.2.1.4. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Testing Services

5.2.2.1. Physiological Function Testing- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. General & Clinical Testing- Market Insights and Forecast 2022-2032, USD Million

5.2.2.3. Esoteric Testing- Market Insights and Forecast 2022-2032, USD Million

5.2.2.4. Specialized Testing- Market Insights and Forecast 2022-2032, USD Million

5.2.2.5. Non-invasive Prenatal Testing- Market Insights and Forecast 2022-2032, USD Million

5.2.2.6. COVID-19 Testing- Market Insights and Forecast 2022-2032, USD Million

5.2.2.7. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Disease

5.2.3.1. Cardiology- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Oncology- Market Insights and Forecast 2022-2032, USD Million

5.2.3.3. Neurology- Market Insights and Forecast 2022-2032, USD Million

5.2.3.4. Orthopedics- Market Insights and Forecast 2022-2032, USD Million

5.2.3.5. Gastroenterology- Market Insights and Forecast 2022-2032, USD Million

5.2.3.6. Gynecology- Market Insights and Forecast 2022-2032, USD Million

5.2.3.7. Odontology- Market Insights and Forecast 2022-2032, USD Million

5.2.3.8. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Revenue Source

5.2.4.1. Healthcare Plan- Market Insights and Forecast 2022-2032, USD Million

5.2.4.2. Out-of-Pocket- Market Insights and Forecast 2022-2032, USD Million

5.2.4.3. Public System- Market Insights and Forecast 2022-2032, USD Million

5.2.5.By Test Type

5.2.5.1. Pathology- Market Insights and Forecast 2022-2032, USD Million

5.2.5.2. Radiology- Market Insights and Forecast 2022-2032, USD Million

5.2.6.By End User

5.2.6.1. Referrals- Market Insights and Forecast 2022-2032, USD Million

5.2.6.2. Walk-ins- Market Insights and Forecast 2022-2032, USD Million

5.2.6.3. Corporate Clients- Market Insights and Forecast 2022-2032, USD Million

5.2.7.By Competitors

5.2.7.1. Competition Characteristics

5.2.7.2. Market Share & Analysis

6. Philippines Single/Independent Laboratories Market Statistics, 2022-2032

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in USD Million

6.2. Market Segmentation & Growth Outlook

6.2.1.By Testing Services- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Disease- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By Revenue Source- Market Insights and Forecast 2022-2032, USD Million

6.2.4.By Test Type- Market Insights and Forecast 2022-2032, USD Million

6.2.5.By End User- Market Insights and Forecast 2022-2032, USD Million

7. Philippines Hospital-based Laboratories Market Statistics, 2022-2032

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in USD Million

7.2. Market Segmentation & Growth Outlook

7.2.1.By Testing Services- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Disease- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By Revenue Source- Market Insights and Forecast 2022-2032, USD Million

7.2.4.By Test Type- Market Insights and Forecast 2022-2032, USD Million

7.2.5.By End User- Market Insights and Forecast 2022-2032, USD Million

8. Philippines Physician Office Laboratories Market Statistics, 2022-2032

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in USD Million

8.2. Market Segmentation & Growth Outlook

8.2.1.By Testing Services- Market Insights and Forecast 2022-2032, USD Million

8.2.2.By Disease- Market Insights and Forecast 2022-2032, USD Million

8.2.3.By Revenue Source- Market Insights and Forecast 2022-2032, USD Million

8.2.4.By Test Type- Market Insights and Forecast 2022-2032, USD Million

8.2.5.By End User- Market Insights and Forecast 2022-2032, USD Million

9. Competitive Outlook

9.1. Company Profiles

9.1.1.Hi Precision Diagnostics

9.1.1.1. Business Description

9.1.1.2. Service Portfolio

9.1.1.3. Collaborations & Alliances

9.1.1.4. Recent Developments

9.1.1.5. Financial Details

9.1.1.6. Others

9.1.2.LCM Diagnostics

9.1.2.1. Business Description

9.1.2.2. Service Portfolio

9.1.2.3. Collaborations & Alliances

9.1.2.4. Recent Developments

9.1.2.5. Financial Details

9.1.2.6. Others

9.1.3.Medi Linx Laboratory Inc.

9.1.3.1. Business Description

9.1.3.2. Service Portfolio

9.1.3.3. Collaborations & Alliances

9.1.3.4. Recent Developments

9.1.3.5. Financial Details

9.1.3.6. Others

9.1.4.BioPATH Clinical Diagnostics, Inc.

9.1.4.1. Business Description

9.1.4.2. Service Portfolio

9.1.4.3. Collaborations & Alliances

9.1.4.4. Recent Developments

9.1.4.5. Financial Details

9.1.4.6. Others

9.1.5.PMP Diagnostic Center Inc.

9.1.5.1. Business Description

9.1.5.2. Service Portfolio

9.1.5.3. Collaborations & Alliances

9.1.5.4. Recent Developments

9.1.5.5. Financial Details

9.1.5.6. Others

9.1.6.iScan Diagnostic Center

9.1.6.1. Business Description

9.1.6.2. Service Portfolio

9.1.6.3. Collaborations & Alliances

9.1.6.4. Recent Developments

9.1.6.5. Financial Details

9.1.6.6. Others

9.1.7.Singapore Diagnostics

9.1.7.1. Business Description

9.1.7.2. Service Portfolio

9.1.7.3. Collaborations & Alliances

9.1.7.4. Recent Developments

9.1.7.5. Financial Details

9.1.7.6. Others

9.1.8.Accuteqs Diagnostics Laboratory

9.1.8.1. Business Description

9.1.8.2. Service Portfolio

9.1.8.3. Collaborations & Alliances

9.1.8.4. Recent Developments

9.1.8.5. Financial Details

9.1.8.6. Others

9.1.9.Biopath Clinical Diagnostics Inc.

9.1.9.1. Business Description

9.1.9.2. Service Portfolio

9.1.9.3. Collaborations & Alliances

9.1.9.4. Recent Developments

9.1.9.5. Financial Details

9.1.9.6. Others

9.1.10. ASHREY Diagnostic Center

9.1.10.1. Business Description

9.1.10.2. Service Portfolio

9.1.10.3. Collaborations & Alliances

9.1.10.4. Recent Developments

9.1.10.5. Financial Details

9.1.10.6. Others

10. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Lab Type |

|

| By Testing Services |

|

| By Disease |

|

| By Revenue Source |

|

| By Test Type |

|

| By End User |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.