Norway Paediatric Consumer Health Market Report: Trends, Growth and Forecast (2026-2032)

By Product Type (Paediatric Analgesics (Paediatric Acetaminophen, Paediatric Aspirin, Paediatric Combination Products Analgesics, Paediatric Dipyrone, Paediatric Ibuprofen, Paediatric Naproxen), Paediatric Cough, Cold and Allergy Remedies (Paediatric Allergy Remedies, Paediatric Cough/Cold Remedies), Paediatric Digestive Remedies (Paediatric Diarrhoeal Remedies, Paediatric Indigestion and Heartburn Remedies, Paediatric Laxatives, Paediatric Motion Sickness Remedies), Paediatric Dermatologicals, Nappy (Diaper) Rash Treatments, Paediatric Vitamins and Dietary Supplements), By Dosage Form (Liquid Syrups, Chewable Tablets, Drops, Powders/Sachets, Gummies, Topical Creams & Ointments), By Age Group (Infants & Toddlers (0-3 Years), Children (4-12 Years), Adolescents (13-18 Years)), By Treatment Type (Acute Treatment, Chronic Condition Management, Genetic & Rare Disease Management), By Sales Channel (Retail Online (Online Pharmacies, E-commerce Platforms, Brand Websites), Retail Offline (Hospital Pharmacies, Retail Pharmacies / Drugstores, Supermarkets & Hypermarkets, Specialty Baby Stores)) ... Read more

|

Major Players

|

Norway Paediatric Consumer Health Market Statistics and Insights, 2026

- Market Size Statistics

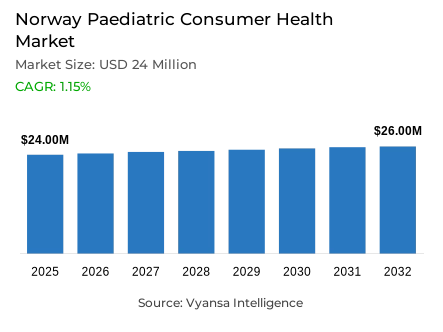

- Paediatric consumer health market size in Norway was valued at USD 24 million in 2025 and is estimated at USD 25.2 Million in 2026.

- The market size is expected to grow to USD 26 million by 2032.

- Market to register a CAGR of around 1.15% during 2026-32.

- Product Type Shares

- Paediatric vitamins and dietary supplements grabbed market share of 40%.

- Competition

- More than 20 companies are actively engaged in producing paediatric consumer health in Norway.

- Top 5 companies acquired around 75% of the market share.

- Lifeline Pharma AS, Evolan Pharma AB, Bonaventura Sales AS, Orkla Health AS, Haleon Norway AS etc., are few of the top companies.

- Sales Channel

- Retail offline grabbed 75% of the market.

Norway Paediatric Consumer Health Market Outlook

The Norway paediatric consumer health market was valued at USD 24 million in 2025 and is projected to expand from USD 25.2 million in 2026 to USD 26 million by 2032, reflecting a compound annual growth rate of 1.15% over the forecast period. This gradual yet consistent growth pattern is indicative of the nature of the Norwegian developed healthcare culture, in which a conservative and thoughtful attitude towards the use of medication creates a structural limit to the total volumes of category sales. Although the low birth rates and the nature of the dosage needed to consume paediatric products limit growth, the market is supported by a robust and entrenched focus on preventive care and an uncompromising focus on high-quality product standards throughout the end-user base.

A significant portion of overall market value is generated by the nutritional support segment, with paediatric vitamins and dietary supplements accounting for 40% of total market share. Vitamin-D drops in infants and multivitamin gummy formulations are products that have a high level of end-user acceptance in Norwegian households. Parents demonstrate a consistent and pronounced preference for premium paediatric consumer health offerings carrying clean‑label credentials, including vegan certification, sugar‑free formulation, and preservative‑free composition, reflecting a clear willingness among end users to invest in products perceived as delivering meaningful long‑term health benefits for their children.

Trusted brand equity and professional healthcare recommendations remain foundational determinants of end‑user purchasing behaviour within this market, a dynamic reinforced by retail offline accounting for 75% of total market share. Physical pharmacies are the main channel of distribution, which enjoys high institutional trust and serves as the main source of professional product advice. In such settings, the presence of well-established adult healthcare brands that have been extended into paediatric formulations, such as Paracet and Otrivin, hold dominant positions in the paediatric consumer health market, with Norwegian parents showing a high propensity to stick to familiar brand names with well-established safety and efficacy profiles.

In the future, the digital distribution environment is set to grow increasingly dynamic as online retail stores continue to gain momentum among time-starved families that are interested in having more convenient purchasing options and increased access to products. Online pharmacy platforms are increasing their product lines to include niche and premium products that do not always secure physical shelf space in brick-and-mortar settings. With the current demographic downturn in the younger demographic posing a structural growth limitation that is unlikely to be overcome soon, future market growth will rely to a growing extent on continued product innovation, the implementation of sustainable packaging credentials, and the ability of established brands to sustain and intensify end-user loyalty in an increasingly competitive and innovation-driven category environment.

Norway Paediatric Consumer Health Market Growth DriverPreventive Supplement Use Sustains Consistent Category Demand

The most clearly defined and stable source of demand in the Norwegian paediatric consumer health market is paediatric vitamins and dietary supplements, which is indicative of the prevention-focused and conservative nature of the Norwegian attitude towards child health management. Although the Norwegian parents tend to have a tendency of restricting the unnecessary use of over-the-counter products, they are always open and eager to use products that are seen to have a purpose, easy to administer, and directly related to the daily wellbeing of children. This orientation solidly places child-specific vitamin drops, gummy formulations, and chewable formats as regular support products that are bought on a regular basis as opposed to occasional or reactive basis.

This demand dynamic is also supported by official nutritional advice on the intake of vitamin-D by infants. According to the infant nutrition guidelines of the Norwegian Directorate of Health, 700 millilitres of infant formula contains 10 micrograms of vitamin-D, which is the recommended daily intake, and infants who consume between 100 and 300 millilitres of infant formula daily should take five drops of vitamin-D, and those who consume between 400 and 600 millilitres should take three drops. This degree of prescriptive official advice entrenches particular supplementation products into prescribed infant-care practices, which offers a long-term and institutionally anchored base of category demand among families with young children.

Norway Paediatric Consumer Health Market ChallengeA Contracting Child Population Constrains Addressable Volume Growth

The major structural challange of the Norwegian paediatric consumer health market is the slow shrinkage of the natural end-user base of child-oriented products. The category already exists in a mature market environment with conservative buying behaviour, and a falling child population is increasingly making it more challenging to achieve any meaningful volume growth. This limitation is especially applicable to early-childhood product lines and formats that rely on high-frequency household replenishment as opposed to low-frequency or low-dose purchasing events.

This pressure is well depicted by official demographic statistics of the country provided by Statistics Norway. The number of children between 00 and 17 years of age decreased by 4,788 in 2024 to 4,851 in 2025. In this group, the number of children between 0 and 5 years of age also decreased by 331,478 to 330,451 during the same time. This demographic shift directly reduces the number of addressable end-users of child-oriented end user-health products and places a structural limit on the extent to which volume-based growth can be attained without simultaneous increases in per-household expenditure, product premiumisation, or category penetration among the current end-user households.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Norway Paediatric Consumer Health Market TrendRetail Online Channels Gain Increasing Relevance Within the Paediatric Purchasing Journey

The most significant and enduring trends in the Norwegian paediatric consumer health market is the increasing commercial importance of retail online distribution and the structural dominance of physical pharmacy distribution. Physical pharmacies maintain their leadership role as the main point of purchase, since parents trust them to provide professional advice on products, reassurance on child-appropriate formulations, and access to both medicinal and supplementation products immediately. At the same time, online retailing is increasingly appealing to time-starved families in need of convenience in making purchases, increased product range, more effective price comparison, and access to high-quality or specialist paediatric products that might not be given adequate physical shelf space in retail settings.

This structural change is captured in official retail commerce statistics. Statistics Norway reports that retail online turnover increased from NOK 8,120 million in the fifth period of 2024 to NOK 8,625 million in the fifth period of 2025, representing growth of 6.2% over the comparable period. This upward trend justifies the increasing importance of digital channels in the paediatric consumer health buying process, especially among knowledgeable and research-intensive parents who consider product credentials, ingredient profiles, and end-user reviews before making a purchase decision.

Norway Paediatric Consumer Health Market OpportunityClean Label Premiumisation Creates Meaningful Value Expansion Opportunity

There is a clear business opportunity in the high-end, clean-label segment of the Norwegian paediatric supplements market, which is motivated by the proven readiness of Norwegian parents to pay a price premium to products that are viewed as safer, easier to compose, and more child-friendly. The product features, including vegan certification, sugar-free formulation, and the lack of artificial preservatives, have a significant purchase power in this end-user group. This dynamic provides significant headroom to brands in a mature market where volume growth is structurally limited, and where incremental value is created through formulation quality, ingredient transparency, and the creation of child-friendly delivery formats, as opposed to depending on increased frequency of use as a growth engine.

This strategic direction is further supported by the broader regulatory environment. The Ministry of Health and Care Services in Norway has confirmed that the laws against the marketing of unhealthy food and beverages to children came into effect on 25 October 2025, and has also added that one out of five children in Norway is now overweight or obese. This regulatory and societal environment of health-first enhances the commercial attractiveness of better-positioned paediatric wellness products and offers an enabling environment of premium innovation based on cleaner and more transparently formulated products.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Norway Paediatric Consumer Health Market Segmentation Analysis

By Product Type

- Paediatric Analgesics

- Paediatric Acetaminophen

- Paediatric Aspirin

- Paediatric Combination Products Analgesics

- Paediatric Dipyrone

- Paediatric Ibuprofen

- Paediatric Naproxen

- Paediatric Cough, Cold and Allergy Remedies

- Paediatric Allergy Remedies

- Paediatric Cough/Cold Remedies

- Paediatric Digestive Remedies

- Paediatric Diarrhoeal Remedies

- Paediatric Indigestion and Heartburn Remedies

- Paediatric Laxatives

- Paediatric Motion Sickness Remedies

- Paediatric Dermatologicals

- Nappy (Diaper) Rash Treatments

- Paediatric Vitamins and Dietary Supplements

Within the product‑type segmentation, Paediatric Vitamins and Dietary Supplements represent the leading segment, accounting for 40% of total market share. This leadership role indicates the core and long-established role of preventive care in the Norwegian paediatric health environment. Recipes that incorporate chewable supplements, gummy products, and vitamin drops are well-suited to the parental preferences of easy, low-effort daily routines that promote the health and development of children without fostering a culture of pharmaceutical intervention.

This segment also enjoys high and sustained end-user acceptance of child-friendly product formats that are trusted. Although Norwegian parents are quite selective in their buying choices, they are also willing to spend on products that can be proven to be of good quality, easy to administer, and with clean ingredient positioning. High-quality product features such as vegan certification, sugar-free formulation, and preservative-free composition can be used to meaningfully enhance end-user attraction and support repeat purchasing behaviour. All these factors contribute to the fact that paediatric vitamins and dietary supplements remain the most popular type of product in the market.

By Sales Channel

- Retail Online

- Online Pharmacies

- E-commerce Platforms

- Brand Websites

- Retail Offline

- Hospital Pharmacies

- Retail Pharmacies / Drugstores

- Supermarkets & Hypermarkets

- Specialty Baby Stores

Within the sales‑channel segmentation, Retail Offline accounts for 75% of total market share, retaining its position as the dominant distribution channel for paediatric consumer health products in Norway. The main point of purchase in this category is still physical pharmacies, where parents can get reliable professional guidance, product-specific assurance, and direct access to both medicinal and supplementation products. These attributes carry particular weight in a category characterised by cautious and selective purchasing behaviour, where end users are generally reluctant to experiment with unfamiliar products or sellers.

The offline distribution of retail also has the advantage of the small commercial presence of other channels in the daily paediatric buying. Grocery retail outlets predominantly carry basic analgesic products and established children’s vitamin ranges, while specialist health stores serve a comparatively small segment of ingredient‑conscious end users. Despite the fact that retail online channels are still registering significant growth, retail offline still enjoys its status of unquestioned leadership considering that pharmacist-led consultation, instant product access, and established purchasing behavior are still the key factors that define purchase decisions in the Norwegian paediatric consumer health market.

List of Companies Covered in Norway Paediatric Consumer Health Market

The companies listed below are highly influential in the Norway paediatric consumer health market, with a significant market share and a strong impact on industry developments.

- Lifeline Pharma AS

- Evolan Pharma AB

- Bonaventura Sales AS

- Orkla Health AS

- Haleon Norway AS

- Karo Pharma AS

- Orifarm Healthcare AS

- Perrigo Norge AS

- JNTL Consumer Health Norway AS

- Orkla Care AS

Competitive Landscape

Norway paediatric consumer health market in 2025 reflects a competitive landscape dominated by trusted domestic healthcare brands and well-established OTC extensions for children. Orkla Health AS retains the leading position, supported by a strong portfolio including Collett Vitaminbjørner, Sana‑Sol, and Möller’s, all widely recognised among Norwegian families. In vitamins and dietary supplements, Orifarm Group competes strongly through its Nycoplus range, particularly vitamin D drops for infants. Premium-oriented brands such as VitaYummy are also gaining traction, driven by demand for vegan, sugar-free and clean-label formulations. Overall competition remains centred on highly trusted brands with strong pharmacy distribution and child-friendly supplement formats.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Norway Paediatric Consumer Health Market Policies, Regulations, and Standards

- Norway Paediatric Consumer Health Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Norway Paediatric Consumer Health Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product Type

- Paediatric Analgesics- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Acetaminophen- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Aspirin- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Combination Products Analgesics- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Dipyrone- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Ibuprofen- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Naproxen- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Cough, Cold and Allergy Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Allergy Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Cough/Cold Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Digestive Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Diarrhoeal Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Indigestion and Heartburn Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Laxatives- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Motion Sickness Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Dermatologicals- Market Insights and Forecast 2022-2032, USD Million

- Nappy (Diaper) Rash Treatments- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Vitamins and Dietary Supplements- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Analgesics- Market Insights and Forecast 2022-2032, USD Million

- By Dosage Form

- Liquid Syrups- Market Insights and Forecast 2022-2032, USD Million

- Chewable Tablets- Market Insights and Forecast 2022-2032, USD Million

- Drops- Market Insights and Forecast 2022-2032, USD Million

- Powders/Sachets- Market Insights and Forecast 2022-2032, USD Million

- Gummies- Market Insights and Forecast 2022-2032, USD Million

- Topical Creams & Ointments- Market Insights and Forecast 2022-2032, USD Million

- By Age Group

- Infants & Toddlers (0-3 Years)- Market Insights and Forecast 2022-2032, USD Million

- Children (4-12 Years)- Market Insights and Forecast 2022-2032, USD Million

- Adolescents (13-18 Years)- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type

- Acute Treatment- Market Insights and Forecast 2022-2032, USD Million

- Chronic Condition Management- Market Insights and Forecast 2022-2032, USD Million

- Genetic & Rare Disease Management- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- Online Pharmacies- Market Insights and Forecast 2022-2032, USD Million

- E-commerce Platforms- Market Insights and Forecast 2022-2032, USD Million

- Brand Websites- Market Insights and Forecast 2022-2032, USD Million

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- Hospital Pharmacies- Market Insights and Forecast 2022-2032, USD Million

- Retail Pharmacies / Drugstores- Market Insights and Forecast 2022-2032, USD Million

- Supermarkets & Hypermarkets- Market Insights and Forecast 2022-2032, USD Million

- Specialty Baby Stores

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Product Type

- Market Size & Growth Outlook

- Norway Paediatric Analgesics Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Dosage Form- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Norway Paediatric Cough, Cold and Allergy Remedies Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Dosage Form- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Norway Paediatric Digestive Remedies Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Dosage Form- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Norway Paediatric Dermatologicals Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Dosage Form- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Norway Nappy (Diaper) Rash Treatments Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Dosage Form- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Norway Paediatric Vitamins and Dietary Supplements Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Dosage Form- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Orkla Health AS

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Haleon Norway AS

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Karo Pharma AS

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Orifarm Healthcare AS

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Perrigo Norge AS

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Lifeline Pharma AS

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Evolan Pharma AB

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Bonaventura Sales AS

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- JNTL Consumer Health Norway AS

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Orkla Care AS

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Orkla Health AS

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Dosage Form |

|

| By Age Group |

|

| By Treatment Type |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.