North America Modular Data Centers Market Report: Trends, Growth and Forecast (2026-2032)

By Component (Solutions (All-in-One Modular Data Centers, Prefabricated Module Solutions), Services (Consulting & Design Services, Deployment, Integration & Maintenance Services)), By Form Factor (ISO Container-based Modular Data Centers, Enclosure-based Modular Data Centers, Skid-mounted Modular Data Centers), By Build Type (Semi-Prefabricated Modular Data Centers, Fully Prefabricated Modular Data Centers), By Deployment Type (Indoor Modular Data Centers, Outdoor Modular Data Centers), By Organization Size (Large Enterprises, Small & Medium Enterprises), By End User (Cloud Service Providers, Telecom Service Providers, BFSI, Government & Defense, Healthcare, Retail & E-commerce, Manufacturing, Energy & Utilities, Others), By Capacity (Small Capacity Modular Data Centers, Medium Capacity Modular Data Centers, Large Capacity Modular Data Centers), By Country (US, Canada, Mexico, Rest of North America) ... Read more

|

Major Players

|

North America Modular Data Centers Market Statistics and Insights, 2026

- Market Size Statistics

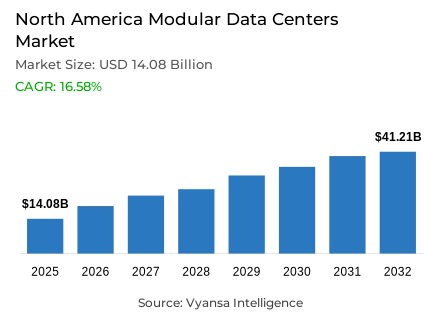

- Modular data centers market size in North America was valued at USD 14.08 billion in 2025 and is estimated at USD 16.41 billion in 2026.

- The market size is expected to grow to USD 41.21 billion by 2032.

- Market to register a CAGR of around 16.58% during 2026-32.

- Component Shares

- Solutions grabbed market share of 80%.

- Competition

- More than 10 companies are actively engaged in producing modular data centers in North America.

- Top 5 companies acquired around 40% of the market share.

- IE Corp, Rittal, Hewlett Packard Enterprise (HPE), Schneider Electric, Dell Technologies etc., are few of the top companies.

- End User

- Cloud Service Providers grabbed 35% of the market.

- Country

- US leads with a 85% share of the North America market.

North America Modular Data Centers Market Outlook

The North America Modular Data Centers Market was valued at USD 14.08 billion in 2025, establishing a commercially powerful and structurally well-anchored foundation within the world's most advanced and most actively expanding digital infrastructure ecosystem. Projected to advance from USD 16.41 billion in 2026 to USD 41.21 billion by 2032, the sector registers a compound annual growth rate of 16.58% across the forecast horizon. This near-tripling of market value reflects a fundamental and durable shift in how North American operators approach infrastructure capacity planning one where deployment speed, phased scalability, and operational predictability are systematically displacing long-cycle conventional construction approaches across hyperscale, enterprise, and edge computing facility development contexts. Growth is sustained by genuine infrastructure necessity rather than technology cycle enthusiasm, giving this market a degree of commercial resilience that few digital infrastructure categories maintain across a comparable forecast window.

The component architecture defining this market's commercial structure is anchored in integrated deployment offerings. Solutions command approximately 80% of total component market share a dominant position reflecting the consistent and deepening preference among North American operators for pre-engineered, standardized infrastructure packages that compress installation timelines, reduce deployment risk, and deliver reliable operational outcomes across diverse facility environments. This concentration signals a market whose buyers have moved decisively beyond component-level procurement toward outcome-oriented solution investment a behavioral maturation that sustains higher average contract values, stronger provider-operator relationships, and more durable competitive advantages for solution providers with proven large-scale deployment track records.

The end-user architecture reinforces the structural centrality of cloud infrastructure operators as the market's dominant demand source. Cloud Service Providers command approximately 35% of total end-user market share a leading position reflecting the natural alignment between modular deployment characteristics and the specific infrastructure requirements of cloud operators managing variable, rapidly evolving workload profiles across geographically distributed service networks. Commercial computing already accounts for an estimated 8% of US commercial sector electricity consumption in 2024, as documented by the Department of Energy a utilization intensity that confirms the scale of compute infrastructure driving consistent cloud capacity expansion pressure and making modular deployment formats operationally indispensable to providers seeking agile, cost-controlled growth pathways.

The forward outlook through 2032 is defined by four structural forces operating in sustained and mutually reinforcing convergence. The US Department of Energy's identification of data center expansion and AI applications as the primary drivers of rising national electricity demand establishes the infrastructure investment imperative whose execution velocity requirements favor modular deployment formats above all alternatives. The DOE's portfolio of over 30 programs supporting grid-scale clean energy deployment, grid infrastructure enhancement, and energy efficiency creates a policy support architecture that sustains large-scale facility development momentum across diverse geographic and operator contexts. The White House's July 2025 framework qualifying data center projects requiring more than 100 megawatts of new load for expedited permitting under FAST-41 accelerates development timelines and compresses the interval between investment commitment and active deployment contract generation. The US market's 85% share of total North America demand confirms that the region's commercial center of gravity is firmly and durably established making the United States the organizing geography around which all competitive strategy, product localization investment, and supply chain development priorities are structured through 2032.

North America Modular Data Centers Market Growth Driver

Surging Compute and AI Infrastructure Demand Accelerates Modular Deployment Adoption

The rapid and institutionally documented escalation of electricity consumption and compute infrastructure investment across North America represents the primary structural driver of modular data center demand functioning as a persistent capacity pressure mechanism that continuously accelerates infrastructure addition requirements across cloud operators, enterprise IT organizations, and AI-linked facility developers whose workload growth trajectories demand deployment solutions capable of delivering new capacity faster than conventional construction timelines allow. As AI applications deepen their penetration across commercial, industrial, and government computing environments, the scale and urgency of infrastructure capacity requirements are compounding at a pace that makes modular deployment formats with their pre-engineered design, rapid commissioning characteristics, and phased scalability structurally indispensable to operators competing on infrastructure readiness speed.

The quantitative momentum of this compute-driven demand dynamic is documented with precision by the Department of Energy and the Energy Information Administration. Commercial computing accounts for an estimated 8% of US commercial sector electricity consumption in 2024 a utilization intensity that confirms the infrastructure scale driving consistent capacity expansion pressure across the region's data center ecosystem. The DOE explicitly identifies rising electricity demand as being mainly driven by data center expansion and the rise of artificial intelligence applications establishing an institutional validation of the demand trajectory that is sustaining consistent modular deployment investment across North America's most commercially active digital infrastructure geographies. These demand dynamics are expected to sustain structural modular data center market growth at an accelerating pace.

North America Modular Data Centers Market Challenge

Specialized Technical Workforce Constraints Limit Deployment Execution Velocity

The specialized and multi-disciplinary workforce requirements of modular data center installation, commissioning, and lifecycle management represent the most consequential structural challenge confronting solution providers seeking to scale delivery capability in line with accelerating facility development demand across North America. Unlike commodity construction projects, modular data center deployment demands simultaneous technical competency across electrical power systems, advanced thermal and cooling infrastructure, and digital network integration a combination of specialist skills whose labor market scarcity, wage premium requirements, and continuous training obligations create persistent workforce supply constraints that moderate deployment execution velocity and elevate cost structures across the industry's most technically demanding project categories.

The structural depth and wage-level specificity of this workforce challenge are quantified with precision by the US Bureau of Labor Statistics. Heating, air conditioning, and refrigeration mechanics and installers hold approximately 425,200 jobs nationally at a median annual wage of USD 59,810 confirming the significant labor investment that thermal and cooling infrastructure deployment capability requires at scale. Computer network support specialists record a median annual wage of USD 73,340 as of May 2024, reflecting the additional cost tier associated with digital infrastructure integration competency across complex modular facility environments. The multi-skill premium created by the intersection of these specialist labor categories means that comprehensive modular deployment workforce development demands sustained investment in recruitment, retention, and continuous technical training obligations that create meaningful execution pressure and scalability constraints for solution providers competing on deployment speed and lifecycle management quality.

Unlock Market Intelligence

Explore the market potential with our data-driven report

North America Modular Data Centers Market Trend

High-Density Cooling Evolution Reshapes Modular Design and Deployment Requirements

The progressive transition of North American data center cooling infrastructure from conventional air-based systems toward higher-efficiency and liquid-cooled configurations represents the defining structural trend reshaping modular data center design priorities, engineering investment, and competitive differentiation across the market. This cooling evolution is being driven by the escalating rack power densities associated with AI and high-performance compute workloads whose thermal output intensity exceeds the practical management capacity of traditional air cooling approaches and demands purpose-built liquid cooling infrastructure whose engineering requirements are fundamentally reshaping modular facility design standards and deployment solution specifications across the region's most advanced facility development programs.

The technical specificity and current deployment scale of this cooling transition trend are documented with authority by the Department of Energy. The DOE's updated 2024 best-practices guidance now explicitly spans cooling and electrical systems across facilities ranging from traditional air-cooled sites to cutting-edge data centers utilizing liquid cooling at the chip level confirming that advanced thermal management has moved from emerging practice into mainstream engineering expectation across North America's most active deployment markets. DOE Better Buildings materials from 2025 further confirm that air cooling still dominates approximately 90% of existing non-AI hyperscale and colocation facilities even as higher-density compute increasingly demands liquid cooling establishing a transitional mixed-cooling environment whose simultaneous support requirements are expanding the engineering scope and technical differentiation potential of modular deployment solution providers. Competitors that build demonstrated liquid cooling integration capability alongside established air system expertise will capture the full spectrum of this evolving deployment opportunity.

North America Modular Data Centers Market Opportunity

Federal Policy Framework Creates Durable Large-Scale Deployment Contract Pipeline

The comprehensive federal policy and program support framework being deployed to enable large-scale data center infrastructure development across the United States creates a structurally significant and commercially durable opportunity for modular data center solution providers delivering a policy-amplified demand expansion dynamic whose investment scale, project timeline acceleration, and expedited permitting pathways generate modular deployment contract opportunities of exceptional commercial value and execution urgency. This policy opportunity is distinguished by its operational specificity: support frameworks targeting facilities with new power loads exceeding 100 megawatts directly identify the project scale at which pre-engineered, rapidly deployable modular solutions deliver their most compelling competitive advantages creating a natural and commercially powerful alignment between federal infrastructure investment incentives and the deployment characteristics that modular formats uniquely provide.

The quantitative scale and programmatic breadth of this policy opportunity are documented with authority by the Department of Energy and the White House. The DOE maintains over 30 programs available to support data center energy needs covering grid-scale clean energy deployment, grid infrastructure enhancement, energy efficiency optimization, demand flexibility, and technical assistance creating a multi-pathway policy support architecture that sustains facility investment momentum across diverse operator types and geographic markets. The White House's July 2025 framework defines qualifying projects to include data center developments requiring more than 100 megawatts of new electrical load granting access to expedited permitting under FAST-41 alongside loans, grants, and tax incentives that accelerate development timelines and compress the interval between investment commitment and active modular deployment contract generation. Solution providers that align their deployment capability, engineering portfolio, and operational infrastructure with this policy-supported facility expansion pipeline will capture disproportionate value from North America's most structurally guaranteed digital infrastructure growth opportunity

North America Modular Data Centers Market Country Analysis

By Country

- US

- Canada

- Mexico

- Rest of North America

The segment with highest market share under the Country is the United States, accounting for approximately 85% of the total North America market. This dominant position reflects the convergence of the world's largest and most active digital infrastructure investment base, the highest concentration of hyperscaler operational capacity, the most sophisticated enterprise IT procurement environment, and a policy and regulatory framework whose recent evolution is actively accelerating large-scale data center development timelines across the country's most commercially significant deployment geographies. With nearly nine-tenths of total regional market value concentrated within a single national market, the United States defines the commercial scale, competitive intensity, and technology adoption trajectory parameters of the North America modular data centers market making it the organizing geography around which all regional competitive strategy, product development investment, and supply chain infrastructure decisions are structured.

The structural dominance of the United States is sustained by demand characteristics operating across multiple commercial dimensions simultaneously active large-format hyperscale capacity additions among established cloud operators, rapid AI-linked infrastructure development creating new deployment pipeline activity, enterprise digital modernization programs generating consistent distributed facility demand, and a federal policy framework whose energy support programs and expedited permitting pathways are collectively accelerating the development timelines that favor modular deployment formats. The DOE's identification of data center expansion and AI applications as primary drivers of rising national electricity demand combined with the White House's July 2025 framework supporting qualifying projects requiring more than 100 megawatts of new load confirms that both market forces and policy architecture are aligned in favor of sustained large-scale modular deployment activity. The United States' structural position as the regional market's dominant commercial engine is expected to deepen through 2032.

Unlock Market Intelligence

Explore the market potential with our data-driven report

North America Modular Data Centers Market Segmentation Analysis

By Component

- Solutions

- All-in-One Modular Data Centers

- Prefabricated Module Solutions

- Services

- Consulting & Design Services

- Deployment, Integration & Maintenance Services

The segment with highest market share under the Component is Solutions, accounting for approximately 80% of the total market. This commanding position reflects the deep and structurally embedded preference among North American data center operators for integrated deployment packages that combine power, cooling, compute, and connectivity infrastructure within a standardized, pre-engineered format that simplifies procurement decisions, accelerates commissioning timelines, and delivers consistent performance outcomes across both large-format hyperscale and distributed edge facility environments. With four-fifths of total market value concentrated within a single component category, Solutions define the commercial priorities, product development investments, and competitive differentiation frameworks of the North America modular data centers market setting the deployment efficiency benchmarks and operational consistency standards that all market participants must credibly deliver to compete for high-value infrastructure contracts.

The structural leadership of Solutions is being actively reinforced by the operational imperatives driving North America's data center expansion wave. As AI-linked hyperscale buildouts, cloud capacity additions, and enterprise digital modernization programs all converge on shared requirements for faster, more predictable deployment outcomes, the commercial case for integrated solutions over fragmented component procurement strengthens in direct proportion to project scale and timeline pressure. The White House's July 2025 expedited permitting framework for qualifying projects requiring more than 100 megawatts of new load is compressing development approval timelines simultaneously accelerating the transition from planning to active deployment and elevating the premium placed on solution providers capable of delivering pre-validated, rapidly installable infrastructure packages. The segment's structural dominance as the market's primary revenue contributor and competitive innovation focal point is expected to deepen through 2032.

By End User

- Cloud Service Providers

- Telecom Service Providers

- BFSI

- Government & Defense

- Healthcare

- Retail & E-commerce

- Manufacturing

- Energy & Utilities

- Others

The segment with highest market share under the End User is Cloud Service Providers, accounting for approximately 35% of the total market. This leading position reflects the structural alignment between cloud operators' infrastructure requirements characterized by rapid workload growth, phase-based capacity expansion needs, and the imperative for consistent deployment outcomes across geographically distributed service environments and the specific operational advantages that modular data center formats deliver across all three dimensions simultaneously. With more than one-third of total market value anchored in cloud service provider demand, this end-user segment defines the deployment specification priorities, scalability performance requirements, and speed-of-commissioning expectations that shape product development and commercial strategy across the North America modular data centers market.

The structural leadership of Cloud Service Providers is being actively intensified by the sustained escalation of compute and storage demand across North America's digital economy. Commercial computing's documented 8% share of US commercial sector electricity consumption in 2024 confirms the infrastructure utilization scale that sustains consistent cloud capacity expansion pressure creating a demand trajectory whose pace and predictability make modular formats the structurally preferred buildout approach for operators managing the region's most demanding digital service growth environments. As cloud operators continue to prioritize flexible expansion across multiple locations while maintaining deployment speed and operational consistency, the modular format's ability to deliver rapid commissioning, phased capacity scaling, and cost-controlled deployment economics reinforces this segment's commercial leadership position. Cloud Service Providers' structural authority as the market's primary demand anchor is expected to strengthen through 2032.

Various Market Players in North America Modular Data Centers Market

The companies mentioned below are highly active in the North America modular data centers market, occupying a considerable portion of the market and shaping industry progress.

- IE Corp

- Rittal

- Hewlett Packard Enterprise (HPE)

- Schneider Electric

- Dell Technologies

- Vertiv

- Hubbell

- Eaton

- IBM

- WESCO International

- Delta Electronics

- TAS Energy

Market News & Updates

- Schneider Electric, 2026:

Schneider Electric announced in San Jose that, with NVIDIA and AVEVA, it had developed new validated blueprints for gigawatt-scale AI factories, including a Vera Rubin reference design that validates power and cooling for the latest NVIDIA rack-scale systems and introduces higher-voltage distribution and new thermal parameters for dense AI clusters. For North America’s modular data centers market, this matters because standardized, pre-validated power-and-cooling reference architectures lower design risk, shorten deployment cycles, and make it easier for developers and operators to industrialize modular, high-density AI capacity rather than engineer each project from scratch.

- Vertiv, 2026:

Vertiv introduced Vertiv MegaMod HDX for North America and EMEA, a new prefabricated modular liquid-cooling infrastructure solution designed for pod-style AI environments and advanced GPU clusters; Vertiv said the compact version supports up to 13 racks and 1.25 MW, while the combo configuration scales to 144 racks and 10 MW, with support for rack densities from 50 kW to more than 100 kW per rack. This is a major North American market development because it directly expands commercially available modular capacity for high-density AI workloads and strengthens the case for prefabricated pod deployments as operators face urgent timelines, higher cooling complexity, and growing power-density requirements.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- North America Modular Data Centers Market Policies, Regulations, and Standards

- North America Modular Data Centers Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- North America Modular Data Centers Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component

- Solutions- Market Insights and Forecast 2022-2032, USD Million

- All-in-One Modular Data Centers- Market Insights and Forecast 2022-2032, USD Million

- Prefabricated Module Solutions- Market Insights and Forecast 2022-2032, USD Million

- Services- Market Insights and Forecast 2022-2032, USD Million

- Consulting & Design Services- Market Insights and Forecast 2022-2032, USD Million

- Deployment, Integration & Maintenance Services- Market Insights and Forecast 2022-2032, USD Million

- Solutions- Market Insights and Forecast 2022-2032, USD Million

- By Form Factor

- ISO Container-based Modular Data Centers- Market Insights and Forecast 2022-2032, USD Million

- Enclosure-based Modular Data Centers- Market Insights and Forecast 2022-2032, USD Million

- Skid-mounted Modular Data Centers- Market Insights and Forecast 2022-2032, USD Million

- By Build Type

- Semi-Prefabricated Modular Data Centers- Market Insights and Forecast 2022-2032, USD Million

- Fully Prefabricated Modular Data Centers- Market Insights and Forecast 2022-2032, USD Million

- By Deployment Type

- Indoor Modular Data Centers- Market Insights and Forecast 2022-2032, USD Million

- Outdoor Modular Data Centers- Market Insights and Forecast 2022-2032, USD Million

- By Organization Size

- Large Enterprises- Market Insights and Forecast 2022-2032, USD Million

- Small & Medium Enterprises- Market Insights and Forecast 2022-2032, USD Million

- By End User

- Cloud Service Providers- Market Insights and Forecast 2022-2032, USD Million

- Telecom Service Providers- Market Insights and Forecast 2022-2032, USD Million

- BFSI- Market Insights and Forecast 2022-2032, USD Million

- Government & Defense- Market Insights and Forecast 2022-2032, USD Million

- Healthcare- Market Insights and Forecast 2022-2032, USD Million

- Retail & E-commerce- Market Insights and Forecast 2022-2032, USD Million

- Manufacturing- Market Insights and Forecast 2022-2032, USD Million

- Energy & Utilities- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Capacity

- Small Capacity Modular Data Centers- Market Insights and Forecast 2022-2032, USD Million

- Medium Capacity Modular Data Centers- Market Insights and Forecast 2022-2032, USD Million

- Large Capacity Modular Data Centers- Market Insights and Forecast 2022-2032, USD Million

- By Country

- US

- Canada

- Mexico

- Rest of North America

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Component

- Market Size & Growth Outlook

- US Modular Data Centers Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component- Market Insights and Forecast 2022-2032, USD Million

- By Form Factor- Market Insights and Forecast 2022-2032, USD Million

- By Build Type- Market Insights and Forecast 2022-2032, USD Million

- By Deployment Type- Market Insights and Forecast 2022-2032, USD Million

- By Organization Size- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Capacity- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Canada Modular Data Centers Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component- Market Insights and Forecast 2022-2032, USD Million

- By Form Factor- Market Insights and Forecast 2022-2032, USD Million

- By Build Type- Market Insights and Forecast 2022-2032, USD Million

- By Deployment Type- Market Insights and Forecast 2022-2032, USD Million

- By Organization Size- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Capacity- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Mexico Modular Data Centers Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component- Market Insights and Forecast 2022-2032, USD Million

- By Form Factor- Market Insights and Forecast 2022-2032, USD Million

- By Build Type- Market Insights and Forecast 2022-2032, USD Million

- By Deployment Type- Market Insights and Forecast 2022-2032, USD Million

- By Organization Size- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Capacity- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Schneider Electric

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Dell Technologies

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Vertiv

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Hubbell

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Eaton

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- IE Corp

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Rittal

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Hewlett Packard Enterprise (HPE)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- IBM

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- WESCO International

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Delta Electronics

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- TAS Energy

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Schneider Electric

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Component |

|

| By Form Factor |

|

| By Build Type |

|

| By Deployment Type |

|

| By Organization Size |

|

| By End User |

|

| By Capacity |

|

| By Country |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.