Mexico Diagnostic Labs Market Report: Trends, Growth and Forecast (2026-2032)

By Lab Type (Single/Independent Laboratories, Hospital-based Laboratories, Physician Office Laboratories, Others), By Testing Services (Physiological Function Testing, General & Clinical Testing, Esoteric Testing, Specialized Testing, Non-invasive Prenatal Testing, COVID-19 Testing, Others), By Disease (Cardiology, Oncology, Neurology, Orthopedics, Gastroenterology, Gynecology, Odontology, Others), By Revenue Source (Healthcare Plan, Out-of-Pocket, Public System), By Test Type (Pathology, Radiology), By End User (Referrals, Walk-ins, Corporate Clients) ... Read more

|

Major Players

|

Mexico Diagnostic Labs Market Statistics and Insights, 2026

- Market Size Statistics

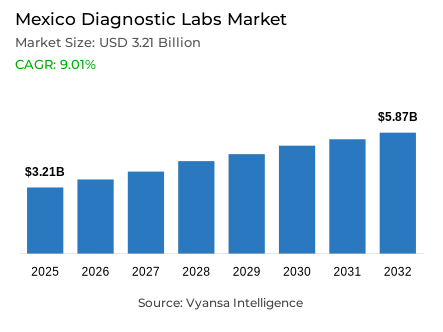

- Diagnostic labs market size in Mexico was estimated at USD 3.21 billion in 2025.

- The market size is expected to grow to USD 5.87 billion by 2032.

- Market to register a CAGR of around 9.01% during 2026-32.

- Lab Type Shares

- Hospital-based laboratories grabbed market share of 50%.

- Competition

- Diagnostic labs in Mexico is currently being catered to by more than 5 companies.

- Top 5 companies acquired around 70% of the market share.

- Estudios Clinicos Dr. T.J. Oriard S.A. de C.V., Laboratorio Médico del Chopo, Salud Digna etc., are few of the top companies.

- Testing Services

- General & clinical testing grabbed 45% of the market.

Mexico Diagnostic Labs Market Outlook

Mexico diagnostic labs market is positioned for strong expansion over the forecast period, with the market size estimated at USD 3.21 billion in 2025 and projected to grow to USD 5.87 billion by 2032, registering a robust CAGR of around 9.01% during 2026-32. This growth trajectory reflects the rising healthcare demands driven by the country's increasing burden of chronic diseases, particularly hypertension and diabetes, which have become leading health concerns. As more patients require regular monitoring and screening for these conditions, diagnostic laboratories are experiencing sustained increases in test volumes across both public and private healthcare facilities.

The diagnostic labs expansion is further supported by Mexico's ongoing efforts to achieve universal health coverage, with approximately 87% of the population already covered by public or social insurance programs as of 2025. As coverage extends to the remaining population in informal employment sectors and rural areas, millions of additional individuals will gain access to diagnostic services. Government initiatives, including the IMSS-Bienestar program, are establishing new clinics and mobile units in underserved regions, which will drive demand for on-site laboratory testing and preventive screening services.

Within the market structure, hospital-based laboratories dominate the landscape, commanding approximately 50% market share among laboratory facility types. These hospital-integrated facilities handle the majority of diagnostic procedures, serving both inpatient and outpatient populations across major healthcare centers. Meanwhile, independent diagnostic facilities and outpatient laboratory centers collectively account for the remaining 50% of the market, catering to walk-in patients and routine screening needs.

From a service perspective, General and Clinical Testing holds the leading position with approximately 45% market share, encompassing routine blood chemistry, hematology, and standard pathology examinations that physicians order daily. Specialized services, including advanced imaging, genetic testing, and sophisticated pathology, comprise the remaining 55% of the market, though routine general testing continues to generate the highest utilization volumes across Mexican healthcare facilities.

Mexico Diagnostic Labs Market Growth Driver

Rising Prevalence of Chronic Diseases

Mexico is experiencing a significant rise in chronic diseases, which is the primary cause of the demand of laboratory testing services in the healthcare system. According to government health data, the prevalence of hypertension in adults has increased dramatically, with the percentage of the population with hypertension growing by 34.1 to 47.8% over the years 2018 to 2022, and the prevalence of diabetes has also risen by 14.4 to 18.3%. Such alarming disease rates have made heart disease and diabetes the top causes of death in the country in 2024, with a combined death toll of more than 300,000. This burden of chronic diseases in clinical practice is translated into increased dependence on blood tests and diagnostic procedures to screen and monitor patients.

The growing chronic disease burden is driving the continued increase in the demand of laboratory services across Mexican hospitals and clinics. With more and more end users demanding continuous monitoring of their conditions, including diabetes and hypertension, laboratories are experiencing an increase in the number of tests being ordered to monitor their blood chemistry, glucose monitoring, and other diagnostic tests. To control these non-communicable diseases, healthcare facilities should conduct regular complete blood counts, cholesterol profiles, kidney functional tests, and extensive screening batteries. The high and increasing prevalence of chronic conditions in Mexico is thus generating strong and sustained demand of diagnostic laboratory services in both the public and the private health care facilities.

Mexico Diagnostic Labs Market Challenge

Limited Healthcare Resources and Infrastructure

One of the key issues facing the diagnostic laboratory industry in Mexico is the highly limited healthcare infrastructure and resource distribution in the national healthcare system. The total health expenditure is just about 6% of GDP, of which the government expenditure is about 3% of that amount, which is significantly lower than the averages of OECD member countries. This long-term underinvestment has led to the lack of adequate numbers of healthcare professionals and facilities to work and serve diagnostic laboratories. Mexico has approximately 2.7 physicians and 3.0 nurses per 1000 population compared to OECD averages of 3.9 and 9.2 respectively and hospital bed capacity is only 1 per 1000 people as opposed to OECD average of about 4.2.

Such shortages of resources cause major bottlenecks in operations, which are reflected in overcrowded hospitals and long queues in seeking diagnostic services across the healthcare system. Most of the public clinics and rural health centres still do not have the necessary laboratory equipment, which significantly limits the capacity of testing in underserved areas. This access gap is well demonstrated by low screening utilisation rates, with approximately 20% of Mexican women aged 40–69 years reporting recent mammogram screening, which is lower than half the OECD average. The small number of workers and poor infrastructure also lead to the slow processing of samples and reporting of results, especially in non-major urban centres, which poses a severe capacity constraint that impedes access to laboratory-based diagnostic care in a timely manner across the nation.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Mexico Diagnostic Labs Market Trend

Technological Advancement and Digital Integration

The Mexican diagnostic services are experiencing a major technological change, and there is a consistent uptake of sophisticated imaging devices and digital connectivity solutions in healthcare institutions. The federal health ministry is in the process of building a new High-Specialty Diagnostic Centre in Mexico City, which will have five MRI units and three PET-CT scanners with a capacity of about 190 imaging studies per day. This state-of-the-art facility will be used to serve the National Institutes of Health network with high-level imaging services and also act as a central tele-radiology centre where X-ray and MRI images can be electronically sent to clinics around the country to the specialist radiologists at the centre. The centre will also be a professional training centre to the radiologists, which will assist in meeting the urgent workforce development requirements.

These advances represent a wider sectoral trend of digitally-enabled, specialised diagnostic infrastructure across the healthcare system in Mexico. To improve operational efficiency and expand specialist knowledge, laboratories are adopting telemedicine platforms and digital workflow management systems, such as electronic transfer of scan images and laboratory data. The use of artificial intelligence applications and full electronic health record systems is gaining momentum in line with the global trends in healthcare technology. In practice, rural clinics will gradually forward biological samples and diagnostic images to centralised labs to be analysed by specialised methods, and urban medical centres will install high-throughput automated testing devices. The diagnostic industry is shifting to a networked, technology-based model of operation that concentrates the complex testing in specialised centres and links routine labs via integrated digital networks.

Mexico Diagnostic Labs Market Opportunity

Preventive Care Expansion and Universal Coverage

The low screening rates among the Mexican population are a huge growth potential of diagnostic laboratory services due to the increased preventive healthcare programs. Numerous standard diagnostic tests are still significantly underutilized compared to clinical guidelines, which means that the systematic growth of preventive care programmes would lead to a significant rise in the demand of laboratory tests. This opportunity is reflected in current mammography screening rates, where only about one out of every five eligible women undergoes recommended screening procedures. Mexico is also on the path to full universal health coverage, and as of 2025, about 87% of the population is already covered by a public or social insurance programme.

With the ongoing expansion of healthcare coverage to cover the rest of the population, which is mostly in informal jobs and rural areas, millions of other people will have access to medical care and diagnostic tests. Operationally, this expansion of coverage will translate to higher patient volumes in healthcare centers that need blood tests, preventive screenings, and regular health check-ups. Government healthcare programmes, such as IMSS-Bienestar that serve rural areas, are actively building new clinics and sending mobile medical units, which creates more demand on on-site laboratory services. The combination of continuous health sector reforms with the increased focus on preventive care is expected to bring many more people under the formal healthcare delivery system, which will provide a large potential to the diagnostic laboratories to gain previously unutilized testing volumes and contribute to the important goals of early disease detection.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Mexico Diagnostic Labs Market Segmentation Analysis

By Lab Type

- Single/Independent Laboratories

- Hospital-based Laboratories

- Physician Office Laboratories

- Others

Hospital-based diagnostic laboratories command the dominant position within Mexico's diagnostic testing infrastructure, holding approximately 50% market share among laboratory facility types. Roughly half of all diagnostic testing procedures performed across Mexico occur within hospital laboratory settings, encompassing both public sector and private hospital facilities throughout the country. These hospital-integrated laboratories serve extensive patient populations including both admitted inpatients and outpatient visitors seeking diagnostic services at major healthcare centers, providing them with exceptionally broad market reach. Their market dominance reflects the structural characteristics of Mexico's healthcare delivery system, where major diagnostic procedures including comprehensive blood testing panels and medical imaging studies are predominantly conducted within hospital settings rather than standalone clinical facilities.

Independent diagnostic facilities and outpatient laboratory centers collectively comprise the remaining market share within Mexico's diagnostic laboratory sector. Private clinical laboratories and smaller specialized diagnostic centers together account for the remaining 50% of testing services, serving walk-in patients and routine health screening requirements. However, no alternative laboratory format approaches the operational scale and market penetration of hospital-based facilities. The fact that hospital-based diagnostic laboratories control approximately 50% market share underscores their central importance to Mexico's diagnostic infrastructure, as these facilities process the majority of diagnostic testing volume even while other laboratory provider categories continue experiencing growth across both urban and expanding rural healthcare markets.

By Testing Services

- Physiological Function Testing

- General & Clinical Testing

- Esoteric Testing

- Specialized Testing

- Non-invasive Prenatal Testing

- COVID-19 Testing

- Others

General and Clinical Testing services represent the clear market leader within diagnostic service categories, commanding approximately 45% market share of laboratory testing volumes. This dominant segment encompasses routine diagnostic assays including blood chemistry panels, hematology testing, and standard pathology examinations that form the foundation of clinical diagnostics. These common laboratory tests are ordered daily by physicians across all medical specialties and collectively account for nearly half of all laboratory services performed throughout Mexico's healthcare system. The substantial market share held by general clinical testing demonstrates that everyday diagnostic procedures, such as complete blood counts, comprehensive metabolic panels, and basic health screening batteries, remain the fundamental backbone supporting Mexico's diagnostic laboratory market.

Specialized diagnostic services, including advanced medical imaging, genetic testing, and sophisticated pathology examinations, collectively comprise the remaining 55% of the diagnostic services market. While these specialized services often involve higher technological complexity or serve lower-volume niche applications, the majority of testing volume continues originating from general laboratory procedures. Mexico's diagnostic laboratory sector remains predominantly driven by broad-based clinical testing services that serve widespread medical requirements. As advanced diagnostic technologies progressively diffuse throughout the healthcare system over time, specialized services may capture increasing market share, but currently routine general testing continues dominating the service mix and generating the highest utilization volumes across Mexican healthcare facilities.

List of Companies Covered in Mexico Diagnostic Labs Market

The companies listed below are highly influential in the Mexico diagnostic labs market, with a significant market share and a strong impact on industry developments.

- Estudios Clinicos Dr. T.J. Oriard S.A. de C.V.

- Laboratorio Médico del Chopo

- Salud Digna

- Lans Laboratorios de Referencia S.A. de C.V.

- OLAB Medical Diagnostics

- Diagno Laboratories Clínicos

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Mexico Diagnostic Labs Market Policies, Regulations, and Standards

- Mexico Diagnostic Labs Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Mexico Diagnostic Labs Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Lab Type

- Single/Independent Laboratories- Market Insights and Forecast 2022-2032, USD Million

- Hospital-based Laboratories- Market Insights and Forecast 2022-2032, USD Million

- Physician Office Laboratories- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Testing Services

- Physiological Function Testing- Market Insights and Forecast 2022-2032, USD Million

- General & Clinical Testing- Market Insights and Forecast 2022-2032, USD Million

- Esoteric Testing- Market Insights and Forecast 2022-2032, USD Million

- Specialized Testing- Market Insights and Forecast 2022-2032, USD Million

- Non-invasive Prenatal Testing- Market Insights and Forecast 2022-2032, USD Million

- COVID-19 Testing- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Disease

- Cardiology- Market Insights and Forecast 2022-2032, USD Million

- Oncology- Market Insights and Forecast 2022-2032, USD Million

- Neurology- Market Insights and Forecast 2022-2032, USD Million

- Orthopedics- Market Insights and Forecast 2022-2032, USD Million

- Gastroenterology- Market Insights and Forecast 2022-2032, USD Million

- Gynecology- Market Insights and Forecast 2022-2032, USD Million

- Odontology- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Revenue Source

- Healthcare Plan- Market Insights and Forecast 2022-2032, USD Million

- Out-of-Pocket- Market Insights and Forecast 2022-2032, USD Million

- Public System- Market Insights and Forecast 2022-2032, USD Million

- By Test Type

- Pathology- Market Insights and Forecast 2022-2032, USD Million

- Radiology- Market Insights and Forecast 2022-2032, USD Million

- By End User

- Referrals- Market Insights and Forecast 2022-2032, USD Million

- Walk-ins- Market Insights and Forecast 2022-2032, USD Million

- Corporate Clients- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Lab Type

- Market Size & Growth Outlook

- Mexico Single/Independent Laboratories Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Testing Services- Market Insights and Forecast 2022-2032, USD Million

- By Disease- Market Insights and Forecast 2022-2032, USD Million

- By Revenue Source- Market Insights and Forecast 2022-2032, USD Million

- By Test Type- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Mexico Hospital-based Laboratories Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Testing Services- Market Insights and Forecast 2022-2032, USD Million

- By Disease- Market Insights and Forecast 2022-2032, USD Million

- By Revenue Source- Market Insights and Forecast 2022-2032, USD Million

- By Test Type- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Mexico Physician Office Laboratories Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Testing Services- Market Insights and Forecast 2022-2032, USD Million

- By Disease- Market Insights and Forecast 2022-2032, USD Million

- By Revenue Source- Market Insights and Forecast 2022-2032, USD Million

- By Test Type- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Laboratorio Médico del Chopo

- Business Description

- Service Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Salud Digna

- Business Description

- Service Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Lans Laboratorios de Referencia S.A. de C.V.

- Business Description

- Service Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- OLAB Medical Diagnostics

- Business Description

- Service Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Diagno Laboratories Clínicos

- Business Description

- Service Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Estudios Clinicos Dr. T.J. Oriard S.A. de C.V.

- Business Description

- Service Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Laboratorio Médico del Chopo

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Lab Type |

|

| By Testing Services |

|

| By Disease |

|

| By Revenue Source |

|

| By Test Type |

|

| By End User |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.