Latin America Soil Treatment Market Report: Trends, Growth and Forecast (2026-2032)

By Type (Organic Amendments (Animal Manure, Crop Residue, Compost, Sewage Sludge and Biosolids), pH Adjusters and Soil Conditioners (Aglime, Gypsum, Others), Soil Protection Products (Herbicides, Insecticides, Fungicides, Nematicides)), By Technology (Physicochemical Treatment, Biological Treatment, Thermal Treatment), By Application (Soil Fertility Improvement, Soil Remediation, pH Correction, Weed Management, Pest Management, Soil Structure Improvement), By Crop Type (Grains and Cereals, Fruits and Vegetables, Pulses and Oilseeds, Commercial Crops, Turf and Ornamentals), By Country (Brazil, Mexico, Argentina, Chile, Colombia, Peru, Rest of Latin America) ... Read more

|

Major Players

|

Latin America Soil Treatment Market Statistics and Insights, 2026

- Market Size Statistics

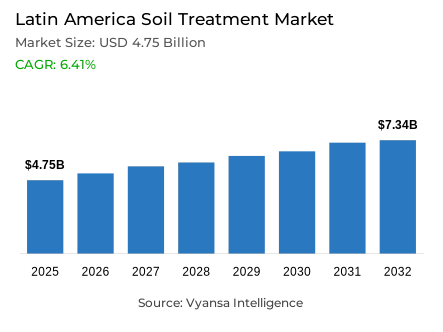

- Soil treatment market size in Latin America was valued at USD 4.75 billion in 2025 and is estimated at USD 5.1 billion in 2026.

- The market size is expected to grow to USD 7.34 billion by 2032.

- Market to register a CAGR of around 6.41% during 2026-32.

- Type Shares

- Soil protection products grabbed market share of 45%.

- Competition

- Soil treatment in Latin America is currently being catered to by more than 10 companies.

- Top 5 companies acquired around 40% of the market share.

- SUMITOMO CHEMICAL BRASIL INDÚSTRIA QUÍMICA SA, FMC Química do Brasil Ltda., Adama Brasil S/A, SYNGENTA PROTEÇÃO DE CULTIVOS LTDA. (Seedcare), Bayer S.A. etc., are few of the top companies.

- Technology

- Physicochemical Treatment grabbed 55% of the market.

- Country

- Brazil leads with a 40% share of the Latin America market.

Latin America Soil Treatment Market Outlook

Latin America soil treatment market is valued at USD 4.75 billion in 2025 and USD 5.10 billion in 2026, and is projected to reach USD 7.34 billion by 2032, growing at a CAGR of 6.41% from 2026 to 2032. It covers soil protection products, amendments, conditioners, biofertilizers, remediation solutions, and physicochemical treatment systems used by crop producers, plantations, remediation contractors, and agronomic service providers across commercial agriculture and land recovery programs regionwide today.

Soil degradation, climate variability, and nutrient stress are intensifying demand for soil fertility restoration across the region. According to FAO, 75% of soils in Latin America and the Caribbean face degradation issues, with estimated annual losses reaching USD 60 billion, which strengthens procurement of soil conservation inputs, soil amendments, and biological soil treatment across the Latin America soil treatment market. These pressures shift buyer priorities from seasonal correction toward continuous soil health management.

Agricultural output protection gives the Latin America soil treatment industry a strategic role in farm productivity, food security, and input efficiency. The Latin America soil treatment market supports crop yield improvement by restoring soil structure, improving pH balance, improving microbial activity, and reducing erosion-linked productivity losses, especially across soybean, maize, sugarcane, coffee, horticulture, and plantation systems where soil quality directly shapes yield stability and input productivity. It also improves supplier visibility in advisory-led procurement channels.

The 2026 trajectory is shaped by regulatory support for bioinputs, wider use of soil analytics, and Brazil’s strong agricultural scale. The Latin America soil treatment industry is moving toward integrated soil health management, where suppliers combine soil conditioners, biofertilizers, microbial inoculants, pH correction, and monitoring tools to improve adoption, strengthen compliance readiness, and expand operational uptake across large farms, degraded land recovery projects, and climate-smart agriculture programs. This positions treatment portfolios as productivity infrastructure rather than discretionary farm inputs.

Latin America Soil Treatment Market Growth Driver

Soil Degradation Pressures are Reshaping Input Priorities

Farmland degradation and productivity risk are increasing demand for preventive soil health management. The Latin America soil treatment market benefits as producers adopt soil conditioners, biofertilizers, microbial inoculants, and pH correction products to reduce nutrient depletion, improve water retention, and protect crop yield potential. This demand is strongest in high-intensity farming systems where erosion, acidity, compaction, and organic matter depletion affect input efficiency and long-term production planning across climate-exposed crop belts, supporting annual input budgeting and agronomic risk mitigation priorities.

Regional water stress is reinforcing the soil-water management link. FAO states that Latin America and the Caribbean hold 34% of the world’s freshwater and receive average precipitation of 1,600 mm per year, yet uneven distribution, seasonality, and climate impacts expose farmers to localized water stress. That operating environment supports the Latin America soil treatment industry by increasing demand for soil structure improvement, moisture retention, and conservation-oriented soil treatment solutions.

Latin America Soil Treatment Market Challenge

Diagnostic Gaps Continue to Slow Precision Adoption

Fragmented soil data and uneven testing capacity continue to limit precision treatment planning. The Latin America soil treatment market requires reliable soil diagnostics to match soil amendments, microbial inputs, liming materials, and remediation methods with local soil chemistry. Where sampling, laboratory quality, or advisory coverage remains inconsistent, suppliers face slower adoption cycles, weaker farmer confidence, less efficient product targeting, and higher risk of underperforming field recommendations during expansion into heterogeneous soil zones regionally today.

FAO’s 2026 SISLAC update shows the scale of the data-quality challenge. The improved regional soil database expanded to 66,746 profiles after cleaning and integration, while 15% of original profiles were excluded for inaccurate diagnostic horizon descriptions and 32% of total profiles analyzed had erroneous descriptions or spatial duplication. This improves transparency for the Latin America soil treatment industry, but also shows why technical validation remains critical for procurement, advisory services, and field-level treatment decisions properly.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Latin America Soil Treatment Market Trend

Bio-Based Inputs Are Moving Into Mainstream Agronomy

Bio-based soil inputs are moving from niche adoption toward mainstream agronomic programs. The Latin America soil treatment market is increasingly shaped by biological soil treatment, microbial inoculants, biofertilizers, and plant-growth solutions that support soil fertility restoration while reducing dependence on conventional synthetic inputs. This trend is strongest where producers need yield resilience, soil microbiome recovery, and compliance alignment with sustainable agriculture frameworks, particularly in export-oriented crop systems, where traceability and residue-management expectations influence input choices.

Brazil’s regulatory pipeline is accelerating biological product availability. The Ministry of Agriculture and Livestock reported that Brazil granted 912 registrations in 2025, including 162 products classified as bioinputs, the highest annual quantity recorded, covering biological, microbiological, biochemical, plant-extract, growth-regulator, and semiochemical products. This strengthens the Latin America soil treatment industry by expanding product choice, improving supplier participation, and supporting commercial scale-up for biological soil treatment across regulated agricultural channels and distributor-led technical programs regionwide now.

Latin America Soil Treatment Market Opportunity

Advisory-Led Soil Programs Can Expand Field Uptake

Technical advisory expansion creates a strong opportunity for soil testing, training, and treatment-service providers. The Latin America soil treatment market can capture higher adoption where agronomists, cooperatives, input distributors, and public programs connect soil diagnostics with practical recommendations for degraded soil treatment, soil pH correction, microbial inoculation, and organic amendment use. Extension-led models improve trust, reduce misuse, and expand demand among small and medium producers seeking practical, field-specific guidance and affordable rural diagnostics.

Mexico’s Soil Doctors initiative shows how structured training can convert awareness into field uptake. IICA reports that the program expanded to 320 certified Soil Doctor trainers, trained 820 certified farmers, involved approximately 4,100 farmers, and managed at least 160 hectares with improved soil practices. This strengthens the Latin America soil treatment industry by creating scalable channels for advisory-backed procurement, localized soil restoration services, and recurring demand for technically validated inputs across priority farming clusters regionwide steadily.

Latin America Soil Treatment Market Country Analysis

By Country

- Brazil

- Mexico

- Argentina

- Chile

- Colombia

- Peru

- Rest of Latin America

Brazil holds 40% share under By Country, supported by large-scale soybean, corn, sugarcane, coffee, citrus, and horticulture systems that require continuous soil fertility restoration and soil health management. The Latin America soil treatment market gains scale from Brazil’s intensive crop acreage, strong cooperative network, bioinput regulation, and established use of liming, gypsum, microbial inoculants, soil conditioners, and remediation practices across commercial agriculture and export-oriented farm supply chains that depend on reliable soil productivity and input efficiency.

Conab’s May 2026 grain outlook estimates Brazil’s 2025/26 grain production at 358 million tons, confirming the country’s operational scale and reinforcing demand for soil treatment across high-volume crop systems. Brazil’s crop base strengthens the Latin America soil treatment industry by creating recurring procurement for soil amendments, biofertilizers, soil pH correction products, and field advisory services linked to productivity, sustainability, and compliance goals, while improving supplier scale, distributor coverage, and advisory penetration across producing states.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Latin America Soil Treatment Market Segmentation Analysis

By Type

- Organic Amendments

- Animal Manure

- Crop Residue

- Compost

- Sewage Sludge and Biosolids

- pH Adjusters and Soil Conditioners

- Aglime

- Gypsum

- Others

- Soil Protection Products

- Herbicides

- Insecticides

- Fungicides

- Nematicides

Soil Protection Products hold 45% share under Type, supported by their direct role in erosion control, soil conservation, fertility protection, and degraded land recovery. The Latin America soil treatment market relies on these products where producers need to protect organic matter, stabilize soil structure, improve nutrient retention, and reduce yield volatility across high-value and broad-acre crops. Their leadership reflects demand for preventive rather than purely corrective soil management across climate-vulnerable production zones and erosion-prone agricultural frontiers with fragile topsoil.

Soil protection is also tied to climate and carbon priorities. FAO data indicates that soils in Latin America and the Caribbean have the world’s greatest carbon sequestration potential and could mitigate 12% to 48% of the region’s net total greenhouse gases. This strengthens procurement of soil amendments, conditioners, cover-support products, and conservation inputs because soil protection improves productivity, resilience, and environmental compliance positioning for growers and input suppliers seeking sustainability outcomes.

By Technology

- Physicochemical Treatment

- Biological Treatment

- Thermal Treatment

Physicochemical Treatment holds 55% share under Technology, driven by the need to correct acidity, improve nutrient availability, reduce aluminum toxicity, and stabilize soil structure in intensive agricultural zones. The Latin America soil treatment market depends on liming, gypsum use, pH correction, and soil chemical adjustment where tropical and subtropical soils limit nutrient uptake and root development. Its dominance reflects measurable field performance, established advisory workflows, and compatibility with large-scale mechanized farming systems, especially in acidic soils and newly converted land.

A 2024 Embrapa-linked study on Cerrado soybean areas reported that 10 t ha−1 of lime increased grain yield by 18% and 12% across two crop years, while lime and gypsum improved soil chemical conditions and reduced acidity components. This reinforces physicochemical treatment adoption by linking soil correction to yield protection, fertility restoration, input efficiency, faster land conversion, and agronomic risk reduction for producers converting or intensifying farmland under pressure.

Various Market Players in Latin America Soil Treatment Market

The companies mentioned below are highly active in the Latin America soil treatment market, occupying a considerable portion of the market and shaping industry progress.

- SUMITOMO CHEMICAL BRASIL INDÚSTRIA QUÍMICA SA

- FMC Química do Brasil Ltda.

- Adama Brasil S/A

- SYNGENTA PROTEÇÃO DE CULTIVOS LTDA. (Seedcare)

- Bayer S.A.

- BASF S.A.

- Corteva Agriscience do Brasil Ltda.

- UPL do Brasil – Indústria e Comércio de Insumos Agropecuários S.A.

- AMVAC do Brasil 3P Ltda.

- Bioceres Crop Solutions Corp. (Rizobacter)

- Koppert Biological Systems

- Albaugh LLC

Market News & Updates

- Syngenta Proteção de Cultivos Ltda., 2025:

Syngenta introduced VICTRATO in Brazil for the 2025/2026 crop season, positioning it for seed treatment against nematodes, initial foliar diseases, and soil-borne pathogens. The product uses TYMIRIUM technology and targets early crop establishment risks in soybeans and other crops. The update strengthens biological and chemical seed-treatment options within Latin America’s soil protection demand base.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Latin America Soil Treatment Market Policies, Regulations, and Standards

- Latin America Soil Treatment Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Latin America Soil Treatment Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Type

- Organic Amendments- Market Insights and Forecast 2022-2032, USD Million

- Animal Manure- Market Insights and Forecast 2022-2032, USD Million

- Crop Residue- Market Insights and Forecast 2022-2032, USD Million

- Compost- Market Insights and Forecast 2022-2032, USD Million

- Sewage Sludge and Biosolids- Market Insights and Forecast 2022-2032, USD Million

- pH Adjusters and Soil Conditioners- Market Insights and Forecast 2022-2032, USD Million

- Aglime- Market Insights and Forecast 2022-2032, USD Million

- Gypsum- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Soil Protection Products- Market Insights and Forecast 2022-2032, USD Million

- Herbicides- Market Insights and Forecast 2022-2032, USD Million

- Insecticides- Market Insights and Forecast 2022-2032, USD Million

- Fungicides- Market Insights and Forecast 2022-2032, USD Million

- Nematicides- Market Insights and Forecast 2022-2032, USD Million

- Organic Amendments- Market Insights and Forecast 2022-2032, USD Million

- By Technology

- Physicochemical Treatment- Market Insights and Forecast 2022-2032, USD Million

- Biological Treatment- Market Insights and Forecast 2022-2032, USD Million

- Thermal Treatment- Market Insights and Forecast 2022-2032, USD Million

- By Application

- Soil Fertility Improvement- Market Insights and Forecast 2022-2032, USD Million

- Soil Remediation- Market Insights and Forecast 2022-2032, USD Million

- pH Correction- Market Insights and Forecast 2022-2032, USD Million

- Weed Management- Market Insights and Forecast 2022-2032, USD Million

- Pest Management- Market Insights and Forecast 2022-2032, USD Million

- Soil Structure Improvement- Market Insights and Forecast 2022-2032, USD Million

- By Crop Type

- Grains and Cereals- Market Insights and Forecast 2022-2032, USD Million

- Fruits and Vegetables- Market Insights and Forecast 2022-2032, USD Million

- Pulses and Oilseeds- Market Insights and Forecast 2022-2032, USD Million

- Commercial Crops- Market Insights and Forecast 2022-2032, USD Million

- Turf and Ornamentals- Market Insights and Forecast 2022-2032, USD Million

- By Country

- Brazil

- Mexico

- Argentina

- Chile

- Colombia

- Peru

- Rest of Latin America

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Type

- Market Size & Growth Outlook

- Brazil Soil Treatment Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Type- Market Insights and Forecast 2022-2032, USD Million

- By Technology- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Crop Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Mexico Soil Treatment Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Type- Market Insights and Forecast 2022-2032, USD Million

- By Technology- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Crop Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Argentina Soil Treatment Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Type- Market Insights and Forecast 2022-2032, USD Million

- By Technology- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Crop Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Chile Soil Treatment Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Type- Market Insights and Forecast 2022-2032, USD Million

- By Technology- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Crop Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Colombia Soil Treatment Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Type- Market Insights and Forecast 2022-2032, USD Million

- By Technology- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Crop Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Peru Soil Treatment Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Type- Market Insights and Forecast 2022-2032, USD Million

- By Technology- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Crop Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- SYNGENTA PROTEÇÃO DE CULTIVOS LTDA. (Seedcare)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Bayer S.A.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- BASF S.A.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Corteva Agriscience do Brasil Ltda.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- UPL do Brasil – Indústria e Comércio de Insumos Agropecuários S.A.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- SUMITOMO CHEMICAL BRASIL INDÚSTRIA QUÍMICA SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- FMC Química do Brasil Ltda.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Adama Brasil S/A

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- AMVAC do Brasil 3P Ltda.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Bioceres Crop Solutions Corp. (Rizobacter)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Koppert Biological Systems

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Albaugh LLC

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- SYNGENTA PROTEÇÃO DE CULTIVOS LTDA. (Seedcare)

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Type |

|

| By Technology |

|

| By Application |

|

| By Crop Type |

|

| By Country |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.