Kenya Paediatric Consumer Health Market Report: Trends, Growth and Forecast (2026-2032)

By Product Type (Paediatric Analgesics (Paediatric Acetaminophen, Paediatric Aspirin, Paediatric Combination Products Analgesics, Paediatric Dipyrone, Paediatric Ibuprofen, Paediatric Naproxen), Paediatric Cough, Cold and Allergy Remedies (Paediatric Allergy Remedies, Paediatric Cough/Cold Remedies), Paediatric Digestive Remedies (Paediatric Diarrhoeal Remedies, Paediatric Indigestion and Heartburn Remedies, Paediatric Laxatives, Paediatric Motion Sickness Remedies), Paediatric Dermatologicals, Nappy (Diaper) Rash Treatments, Paediatric Vitamins and Dietary Supplements), By Dosage Form (Liquid Syrups, Chewable Tablets, Drops, Powders/Sachets, Gummies, Topical Creams & Ointments), By Age Group (Infants & Toddlers (0-3 Years), Children (4-12 Years), Adolescents (13-18 Years)), By Treatment Type (Acute Treatment, Chronic Condition Management, Genetic & Rare Disease Management), By Sales Channel (Retail Online (Online Pharmacies, E-commerce Platforms, Brand Websites), Retail Offline (Hospital Pharmacies, Retail Pharmacies / Drugstores, Supermarkets & Hypermarkets, Specialty Baby Stores)) ... Read more

|

Major Players

|

Kenya Paediatric Consumer Health Market Statistics and Insights, 2026

- Market Size Statistics

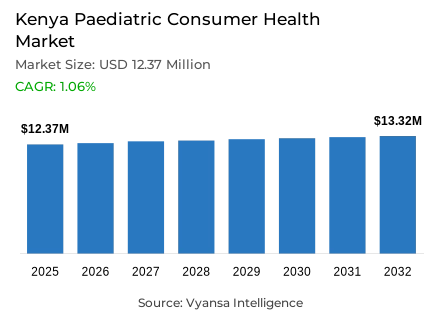

- Paediatric consumer health market size in Kenya was valued at USD 12.37 million in 2025 and is estimated at USD 12.99 Million in 2026.

- The market size is expected to grow to USD 13.32 million by 2032.

- Market to register a CAGR of around 1.06% during 2026-32.

- Product Type Shares

- Paediatric vitamins and dietary supplements grabbed market share of 50%.

- Competition

- More than 10 companies are actively engaged in producing paediatric consumer health in Kenya.

- Top 5 companies acquired around 20% of the market share.

- Reckitt, Kenvue, Bayer, Lab & Allied, Haleon etc., are few of the top companies.

- Sales Channel

- Retail offline grabbed 95% of the market.

Kenya Paediatric Consumer Health Market Outlook

The Kenyan paediatric consumer health market was estimated to be USD 12.37 million. It is forecast to rise from USD 12.99 million in 2026 to USD 13.32 million by 2032, implying a compound annual growth rate of 1.06%. This measured trajectory indicates a modest but resilient category, where everyday child-health needs continue to sustain demand. The market’s stability reflects parents’ willingness to protect essential paediatric spending even as budgets remain constrained.

Affordability is now a central force shaping category mechanics and brand selection. The rising cost of living is driving parents to shift towards domestic and generic paediatric consumer health products that deliver practical relief for fever, pain, colds, and flu. This shift supports steady market movement because families are trading down rather than withdrawing from child-health purchases altogether. As a result, value-oriented brands are gaining stronger relevance within everyday household treatment routines.

Preventive care and wellness-led purchasing are also becoming more influential across the category. Paediatric vitamins and dietary supplements comprise 50% of market revenue, reflecting robust parental interest in immunity, nutrition, and daily wellbeing support. This indicates that end-user demand is no longer driven only by illness response but also on routine health maintenance. The category therefore benefits from a wider role in household care decisions.

Retail offline accounts for 95% of sales, affirming pharmacies and chemists as the predominant access points. At the same time, online connectivity is increasing the convenience of search, payment, and repeat-purchase among busy families. With 60.2 million data subscriptions, 85.2% smartphone penetration, and 48.6 million mobile-money subscriptions as of September 2025, the market is becoming increasingly connected. This combination of offline trust and digital convenience should keep category demand stable yet selective over the forecast period.

Kenya Paediatric Consumer Health Market Growth DriverAffordability Anchors Household Purchases

Affordability remains the primary growth lever in Kenya’s paediatric consumer health market. Parents are increasingly choosing domestic and generic products that offer credible relief at lower price points. This behaviour is sustaining category demand because families continue addressing fever, pain, and minor illnesses even under tighter budgets. The result is a value-based market where accessible pricing supports purchasing continuity and protects volume from sharper erosion.

The economic backdrop validates why this shift remains so powerful across household decisions. Annual inflation reached 4.3% in February 2026, while food and non-alcoholic beverage inflation stood at 7.3%. Transport inflation was 4.0%, and housing, water, electricity, gas, and other fuels rose 1.8%. Such pressures increase price sensitivity and reinforce the appeal of affordable local syrups and pain relievers, keeping practical paediatric healthcare purchases active up to 2032.

Kenya Paediatric Consumer Health Market ChallengeCompliance Pressure Raises the Bar

Regulatory compliance remains the principal challenge shaping competition in Kenya’s paediatric consumer health market. Products are widely available through pharmacies and chemists, but the operating environment is becoming more controlled. To be commercially credible, companies are required to maintain strict registration, certification, and supply-chain discipline, This raises the execution burden, particularly when smaller or less-prepared players are trying to enter a trust-sensitive paediatric category.

Government action confirms that compliance has become a more demanding commercial threshold. In November 2025, the Ministry of Health instructed the Pharmacy and Poisons Board to intensify surveillance and remove substandard, falsified, counterfeit, and unregistered medicines in the market. The Ministry also indicated that the Social Health Authority would not reimburse medicines that were not certified by PPB. These steps increase regulatory pressure and elevate the cost of market participation up to 2032.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Kenya Paediatric Consumer Health Market TrendHerbal Remedies Move Into the Mainstream

A notable trend in Kenya is the mainstreaming of herbal and natural paediatric remedies. Parents are increasingly choosing products that are viewed as softer, wellness-focused, and more aligned with the traditional care practices. This change is important as products that were initially viewed as informal substitutes are now being packaged in more professional forms and more robust retail forms. That evolution improves credibility and expands their commercial appeal beyond niche wellness purchasers.

Digital infrastructure is helping this trend scale more effectively across the market. By September 2025, Kenya had recorded 60.2 million data subscriptions, with 78.3% on mobile broadband, while smartphone penetration reached 85.2%. These conditions improve product visibility, discovery, and brand communication of officially promoted herbal remedies. As a result, natural paediatric products are moving from peripheral options toward broader retail relevance and end-user acceptance by 2032.

Kenya Paediatric Consumer Health Market OpportunityConvenience Creates OTC Headroom

Affordable OTC paediatric products tailored to busy family routines present the strongest opportunity in Kenya. Parents increasingly need quick-access solutions to fever, colds, and influenza that are work-friendly, transport-friendly, and pressure-friendly in the daily household. Brands that combine affordability, familiarity, and reliable symptom relief are in a good position to tap into this demand. The prospect is especially attractive in the case when neighbourhood pharmacies and chemists are still readily available.

Digital reach is strengthening this commercial opening, which increases the convenience of purchases and repeat interaction. By September 2025, mobile-money subscriptions reached 48.6 million, mobile SIM subscriptions rose to 78.3 million, and smartphone penetration stood at 85.2%. These conditions support online search, digital payment, and smoother replenishment behaviour despite the pharmacy-led fulfilment. This creates stronger headroom for affordable OTC brands to widen access and capture routine demand by 2032.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Kenya Paediatric Consumer Health Market Segmentation Analysis

By Product Type

- Paediatric Analgesics

- Paediatric Acetaminophen

- Paediatric Aspirin

- Paediatric Combination Products Analgesics

- Paediatric Dipyrone

- Paediatric Ibuprofen

- Paediatric Naproxen

- Paediatric Cough, Cold and Allergy Remedies

- Paediatric Allergy Remedies

- Paediatric Cough/Cold Remedies

- Paediatric Digestive Remedies

- Paediatric Diarrhoeal Remedies

- Paediatric Indigestion and Heartburn Remedies

- Paediatric Laxatives

- Paediatric Motion Sickness Remedies

- Paediatric Dermatologicals

- Nappy (Diaper) Rash Treatments

- Paediatric Vitamins and Dietary Supplements

The segment commanding the highest market share within the Product Type category is Paediatric Vitamins and Dietary Supplements, accounting for approximately 50% of total market volume. Its leadership indicates the close correlation of the category with nutrition, prevention, and daily child wellness. Parents are paying more attention to the health of children by providing regular support products instead of only using treatments when the illness has already developed. This gives the segment greater household applicability and maintains more consistent buying than categories that are only associated with episodic symptoms.

Its leadership is also a reflection of the increasing popularity of value-based and wellness-focused healthcare options. The intersection of affordability, preventive care, and perceived long-term benefit is filled by vitamins and supplements, which further support their position in everyday family expenditure. With the growing visibility of herbal and natural positioning, this segment will be even more commercially viable as parents will be looking to find a practical everyday support up to 2032.

By Sales Channel

- Retail Online

- Online Pharmacies

- E-commerce Platforms

- Brand Websites

- Retail Offline

- Hospital Pharmacies

- Retail Pharmacies / Drugstores

- Supermarkets & Hypermarkets

- Specialty Baby Stores

The segment claiming the highest market share within the Sales Channel category is Retail Offline, accounting for approximately 95% of total market activity. This leadership highlights the long-term significance of neighbourhood pharmacies, chemists, and store-based purchasing in the paediatric consumer health market in Kenya. Physical retail is the most practical path because parents need to have access to products to treat fever, colds, and influenza as soon as possible. Channel performance is thus still focused on immediate availability and product familiarity.

The high price-sensitive purchasing behaviour in the market also supports offline leadership. Shopping in-store gives parents the opportunity to directly compare low-cost brands and choose local or generic options on the shelf. Online discovery and convenience in digital payments are enhanced, but final purchases are strongly biased towards familiar physical stores. This keeps Retail Offline as the dominant sales channel till 2032.

List of Companies Covered in Kenya Paediatric Consumer Health Market

The companies listed below are highly influential in the Kenya paediatric consumer health market, with a significant market share and a strong impact on industry developments.

- Reckitt

- Kenvue

- Bayer

- Lab & Allied

- Haleon

- Glenmark Pharmaceuticals

- Medley Pharmaceuticals

- Pharmaton

- Abbott

- Sanofi

Market News & Updates

- Reckitt, 2025:

Reckitt introduced Mucinex Children’s Mighty Chews Cold & Flu in August 2025, offering daytime and nighttime chewable formats for children aged six and older. This is relevant to Kenya’s paediatric consumer health market because Reckitt is one of the listed players there and the launch strengthens the paediatric cough/cold remedies category with an easier-to-administer format for families.

- Bayer, 2025:

Bayer launched One A Day Kids Multi with Iron in July 2025 as one of three products in its new kids’ supplement line, aimed at helping children fill common nutrient gaps. This is important for Kenya’s paediatric consumer health market because Bayer is a listed player in the country and the launch supports the paediatric vitamins and dietary supplements segment with a child-focused gummy format.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Kenya Paediatric Consumer Health Market Policies, Regulations, and Standards

- Kenya Paediatric Consumer Health Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Kenya Paediatric Consumer Health Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product Type

- Paediatric Analgesics- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Acetaminophen- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Aspirin- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Combination Products Analgesics- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Dipyrone- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Ibuprofen- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Naproxen- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Cough, Cold and Allergy Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Allergy Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Cough/Cold Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Digestive Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Diarrhoeal Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Indigestion and Heartburn Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Laxatives- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Motion Sickness Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Dermatologicals- Market Insights and Forecast 2022-2032, USD Million

- Nappy (Diaper) Rash Treatments- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Vitamins and Dietary Supplements- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Analgesics- Market Insights and Forecast 2022-2032, USD Million

- By Dosage Form

- Liquid Syrups- Market Insights and Forecast 2022-2032, USD Million

- Chewable Tablets- Market Insights and Forecast 2022-2032, USD Million

- Drops- Market Insights and Forecast 2022-2032, USD Million

- Powders/Sachets- Market Insights and Forecast 2022-2032, USD Million

- Gummies- Market Insights and Forecast 2022-2032, USD Million

- Topical Creams & Ointments- Market Insights and Forecast 2022-2032, USD Million

- By Age Group

- Infants & Toddlers (0-3 Years)- Market Insights and Forecast 2022-2032, USD Million

- Children (4-12 Years)- Market Insights and Forecast 2022-2032, USD Million

- Adolescents (13-18 Years)- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type

- Acute Treatment- Market Insights and Forecast 2022-2032, USD Million

- Chronic Condition Management- Market Insights and Forecast 2022-2032, USD Million

- Genetic & Rare Disease Management- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- Online Pharmacies- Market Insights and Forecast 2022-2032, USD Million

- E-commerce Platforms- Market Insights and Forecast 2022-2032, USD Million

- Brand Websites- Market Insights and Forecast 2022-2032, USD Million

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- Hospital Pharmacies- Market Insights and Forecast 2022-2032, USD Million

- Retail Pharmacies / Drugstores- Market Insights and Forecast 2022-2032, USD Million

- Supermarkets & Hypermarkets- Market Insights and Forecast 2022-2032, USD Million

- Specialty Baby Stores

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Product Type

- Market Size & Growth Outlook

- Kenya Paediatric Analgesics Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Dosage Form- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Kenya Paediatric Cough, Cold and Allergy Remedies Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Dosage Form- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Kenya Paediatric Digestive Remedies Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Dosage Form- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Kenya Paediatric Dermatologicals Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Dosage Form- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Kenya Nappy (Diaper) Rash Treatments Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Dosage Form- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Kenya Paediatric Vitamins and Dietary Supplements Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Dosage Form- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Lab & Allied

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Haleon

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Glenmark Pharmaceuticals

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Medley Pharmaceuticals

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Pharmaton

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Reckitt

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Kenvue

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Bayer

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Abbott

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Sanofi

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Lab & Allied

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Dosage Form |

|

| By Age Group |

|

| By Treatment Type |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.