Kenya Digestive Remedies Market Report: Trends, Growth and Forecast (2026-2032)

By Product Type (Paediatric Digestive Remedies (Paediatric Diarrhoeal Remedies, Paediatric Indigestion & Heartburn Remedies, Paediatric Laxatives, Paediatric Motion Sickness Remedies), Diarrhoeal Remedies, IBS Treatments, Indigestion & Heartburn Remedies (Antacids, Antiflatulents, Digestive Enzymes, H2 Blockers, Proton Pump Inhibitors), Laxatives, Motion Sickness Remedies), By Age Group (Children & Adolescents (01-17 years), Adults (18-65 years), Geriatric (65+ years)), By Sales Channel (Retail Online, Retail Offline (Hospitals, Clinics, Pharmacies)) ... Read more

|

Major Players

|

Kenya Digestive Remedies Market Statistics and Insights, 2026

- Market Size Statistics

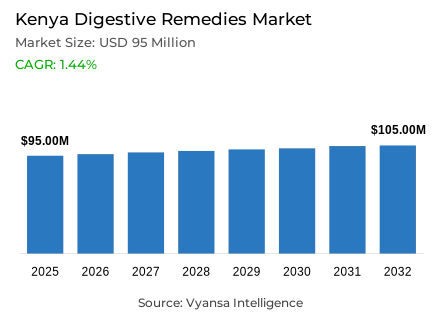

- Digestive remedies market size in Kenya was valued at USD 95 million in 2025 and is estimated at USD 96 Million in 2026.

- The market size is expected to grow to USD 105 million by 2032.

- Market to register a CAGR of around 1.44% during 2026-32.

- Product Type Shares

- Indigestion & heartburn remedies grabbed market share of 80%.

- Competition

- More than 10 companies are actively engaged in producing digestive remedies in Kenya.

- Top 5 companies acquired around 55% of the market share.

- Aspen Pharmacare Holdings Ltd, Beximco Pharmaceuticals Ltd, Boehringer Ingelheim Pharma GmbH & Co KG, GSK Consumer Healthcare, Glenmark Pharmaceuticals Ltd etc., are few of the top companies.

- Sales Channel

- Retail offline grabbed 95% of the market.

Kenya Digestive Remedies Market Outlook

The Kenya digestive remedies market size was valued at USD 95 million in 2025 and is projected to grow from USD 96 million in 2026 to USD 105 million by 2032, exhibiting a CAGR of around 1.44% during the forecast period. Growth remains modest but steady as everyday stomach-related illnesses and self-care practices continue to support demand for over-the-counter digestive treatments across the country.

Public-health conditions remain an important factor supporting the use of digestive remedies. Kenya’s Ministry of Water reports that access to improved water services reaches 74% in FY 2024/25, while safely managed sanitation reaches 40.9%, leaving a significant portion of the population exposed to sanitation gaps. WHO also states that diarrhoea often results from lack of safe drinking water, adequate sanitation, and hygiene. Within the product mix, indigestion and heartburn remedies hold about 80% of the share, reflecting the frequent need for fast relief from common stomach discomfort in daily life.

Purchasing behaviour continues to be affected by affordability for consumers when they are purchasing digestive remedies. According to the KNBS, inflation was running at 4.5% as of December 2025, and prices of food and non-alcoholic beverages have increased year on year by 7.8%. Additionally, the Ministry of Health has reported that it is making a concerted effort to reduce the prices of medicines in Kenya by providing savings up to 60% for selected essential medicines as part of an initiative called the Kenya–Pfizer Accord. Due to these changing economic conditions, many buyers are looking for low cost, quick relief options rather than premium branded products and, therefore, the category is increasingly sensitive to price fluctuations.

Most of the distribution is conducted through physical retail channels. Approximately 95% of sales are generated through off-line retail channels; therefore, consumers will continue to purchase their treatment from a pharmacy, chemist, or nearby store as these are the most convenient and fastest ways to access treatment when they have an acute health issue such as diarrhoea, nausea, or acid reflux. In addition, the government has announced plans to increase local pharmaceutical manufacturing to 50% (currently at 20%) between 2025 and 2030 through the Kenya local manufacturing strategy. This will provide new opportunities to enhance the availability and affordability of digestive remedies through improved domestic supplies and greater access to essential medicines.

Kenya Digestive Remedies Market Growth DriverSanitation Gaps Keep Diarrhoeal Care in Focus

A key driver for digestive remedies in Kenya is the continued burden of water and sanitation linked stomach illness. Kenya’s Ministry of Water reports that access to improved water services reaches 74% in FY 2024/25, while safely managed sanitation reaches 40.9%. This still leaves a large part of the population exposed to hygiene and sanitation gaps. WHO also states that diarrhoea mostly results from lack of safe drinking water, adequate sanitation, and hygiene.

This directly supports demand for diarrhoeal remedies, oral rehydration products, and other quick digestive treatments, especially where stomach infections spread easily and self-care is common. In Kenya, digestive remedies therefore remain closely tied to everyday public-health conditions, not just occasional lifestyle discomfort.

Kenya Digestive Remedies Market ChallengeTight Budgets Hold Back Premium Product Uptake

A major challenge for digestive remedies in Kenya is strong consumer price sensitivity. KNBS reports that annual inflation stands at 4.5% in December 2025, while food and non-alcoholic beverage prices rise 7.8% year on year. At the same time, the Ministry of Health says Kenya is working to cut medicine costs, including savings of up to 60% on selected essential medicines under the Kenya–Pfizer Accord. This shows how important affordability remains in healthcare buying.

For digestive remedies, this means many buyers focus on low-cost and immediate-relief options rather than premium or imported brands. The pressure is strongest in OTC categories, where consumers often buy only what they need at the moment and avoid higher-ticket purchases unless symptoms feel serious.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Kenya Digestive Remedies Market TrendNatural Digestive Care Gains Formal Backing

A clear trend in Kenya is the growing acceptance of natural and integrative care. Kenya's Health Ministry launches new forum on traditional medicine. In February 2026, the Ministry of Health launches the East Africa Forum on traditional, complementary, and integrative Medicine where it reports that millions of East Africans use traditional and complementary medicine as part of their everyday healthcare. The Ministry also refers to Kenya's alignment with the World Health Organization's (WHO) traditional medicine strategy 2025-2034 (the WHO as a reference to a timeline, plan for development of such services), which advocates for safe and evidence-based use of traditional and complementary medicine in the healthcare system.

The launch of the East Africa Forum on Traditional Medicine, and the Kenyan government’s commitments to the WHO’s Traditional Medicine Strategy, enhance the positioning of herbal and nature-based digestive support products in the marketplace. This is significant in terms of digestive health specifically since consumers are looking for solutions that are more gentle and holistic for symptoms like bloating, gas, and abdominal discomfort. This is creating an increasing degree of evolution from informal use of herbal digestive remedies to more formalized recognition and support in the marketplace for herbal products used to support digestive health.

Kenya Digestive Remedies Market OpportunityLocal Manufacturing Opens Room for Affordable Expansion

A strong opportunity in Kenya comes from the push to make medicines more locally available and affordable. The Ministry of Health says the government wants to increase local manufacturing of essential medicines from 20% to 50%, and it is using the Kenya Local Manufacturing Strategy 2025–2030 to scale production. The Ministry also says the Kenya–Pfizer Accord gives access to over 140 medicines on a not-for-profit basis, with some treatments priced far lower than before.

For digestive remedies, this creates room for wider reach of local and generic OTC products in a very price-sensitive market. Better local supply can improve product availability, support more competitive pricing, and help brands target everyday digestive complaints with more affordable offerings.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Kenya Digestive Remedies Market Segmentation Analysis

By Product Type

- Paediatric Digestive Remedies

- Paediatric Diarrhoeal Remedies

- Paediatric Indigestion & Heartburn Remedies

- Paediatric Laxatives

- Paediatric Motion Sickness Remedies

- Diarrhoeal Remedies

- IBS Treatments

- Indigestion & Heartburn Remedies

- Antacids

- Antiflatulents

- Digestive Enzymes

- H2 Blockers

- Proton Pump Inhibitors

- Laxatives

- Motion Sickness Remedies

The segment has the highest share around product type under indigestion & heartburn remedies, with about 80% of the market. This segment leads because indigestion, acid reflux, and heartburn are among the most frequent stomach complaints in daily life. They are closely linked with changing eating habits, convenience food consumption, and the need for quick symptom relief, which keeps this category highly relevant in both urban and peri-urban demand.

Its lead also reflects practical buying behaviour. Consumers usually look for products that act fast, are easy to use, and are available in affordable packs. Because indigestion and heartburn remedies solve common day-to-day discomfort rather than rare conditions, they attract a wider consumer base than the other digestive product categories.

By Sales Channel

- Retail Online

- Retail Offline

- Hospitals

- Clinics

- Pharmacies

The segment has the highest share around sales channel under retail offline, with about 95% of the market. This dominance is also logical due to the fact that digestive products are nearly always bought for immediate relief. Consumers tend to prefer purchasing their products from pharmacies, chemists, and local stores when they suddenly have symptoms of heartburn, diarrhoea, nausea or stomach pain and require treatment on the same day.

Offline retail outlets are also likely to remain strong, as a large number of Kenyan consumers are still very price-sensitive and generally purchase drugs in small quantities. Physical outlets are also much easier for consumers to compare when they are making decisions at the point of purchase, allowing them to quickly determine the least expensive acceptable alternative. Therefore, offline retail remains the primary sales channel for digestive products, especially where consumers place more value on urgency and affordability than on having to wait for fulfilment.

List of Companies Covered in Kenya Digestive Remedies Market

The companies listed below are highly influential in the Kenya digestive remedies market, with a significant market share and a strong impact on industry developments.

- Aspen Pharmacare Holdings Ltd

- Beximco Pharmaceuticals Ltd

- Boehringer Ingelheim Pharma GmbH & Co KG

- GSK Consumer Healthcare

- Glenmark Pharmaceuticals Ltd

- Prisma Pharmaceuticals Ltd

- Cheplapharm Arzneimittel GmbH

- Reckitt Benckiser East Africa Ltd

- Aventis SA

Competitive Landscape

In 2025, the competitive landscape of digestive remedies in Kenya shows moderate concentration, with GSK Consumer Healthcare leading the market with a 23.2% retail value share, followed by Glenmark Pharmaceuticals Ltd at 14.3%. GSK Consumer Healthcare benefits from strong brand recognition and the popularity of well-known products such as Eno, which is widely used to relieve indigestion, heartburn and acid reflux. Glenmark Pharmaceuticals also holds a notable position through its portfolio of gastrointestinal treatments targeting common digestive conditions. Demand for digestive remedies in Kenya is supported by modern lifestyles characterised by unhealthy diets, rising consumption of processed and fast foods, sedentary habits and high stress levels, all of which contribute to increasing cases of digestive disorders. The ageing population is also supporting demand for treatments addressing indigestion, reflux and constipation. At the same time, growing consumer interest in natural and herbal remedies, including products containing ingredients such as charcoal, turmeric and ginger, is shaping market trends. Price sensitivity remains high, encouraging the growth of local and generic brands, while the prevalence of diarrhoeal diseases in areas with poor sanitation continues to sustain demand for affordable over-the-counter digestive treatments.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Kenya Digestive Remedies Market Policies, Regulations, and Standards

- Kenya Digestive Remedies Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Kenya Digestive Remedies Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product Type

- Paediatric Digestive Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Diarrhoeal Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Indigestion & Heartburn Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Laxatives- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Motion Sickness Remedies- Market Insights and Forecast 2022-2032, USD Million

- Diarrhoeal Remedies- Market Insights and Forecast 2022-2032, USD Million

- IBS Treatments- Market Insights and Forecast 2022-2032, USD Million

- Indigestion & Heartburn Remedies- Market Insights and Forecast 2022-2032, USD Million

- Antacids- Market Insights and Forecast 2022-2032, USD Million

- Antiflatulents- Market Insights and Forecast 2022-2032, USD Million

- Digestive Enzymes- Market Insights and Forecast 2022-2032, USD Million

- H2 Blockers- Market Insights and Forecast 2022-2032, USD Million

- Proton Pump Inhibitors- Market Insights and Forecast 2022-2032, USD Million

- Laxatives- Market Insights and Forecast 2022-2032, USD Million

- Motion Sickness Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Digestive Remedies- Market Insights and Forecast 2022-2032, USD Million

- By Age Group

- Children & Adolescents (01-17 years)- Market Insights and Forecast 2022-2032, USD Million

- Adults (18-65 years)- Market Insights and Forecast 2022-2032, USD Million

- Geriatric (65+ years)- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- Hospitals- Market Insights and Forecast 2022-2032, USD Million

- Clinics- Market Insights and Forecast 2022-2032, USD Million

- Pharmacies- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Product Type

- Market Size & Growth Outlook

- Kenya Paediatric Digestive Remedies Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Kenya Diarrhoeal Remedies Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Kenya IBS Treatments Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Kenya Indigestion & Heartburn Remedies Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Kenya Laxatives Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Kenya Motion Sickness Remedies Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- GSK Consumer Healthcare

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Glenmark Pharmaceuticals Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Prisma Pharmaceuticals Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Cheplapharm Arzneimittel GmbH

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Reckitt Benckiser East Africa Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Aspen Pharmacare Holdings Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Beximco Pharmaceuticals Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Boehringer Ingelheim Pharma GmbH & Co KG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Aventis SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Atco Laboratories Pvt Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- GSK Consumer Healthcare

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Age Group |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.