Japan Diagnostic Labs Market Report: Trends, Growth and Forecast (2026-2032)

By Lab Type (Single/Independent Laboratories, Hospital-based Laboratories, Physician Office Laboratories, Others), By Testing Services (Physiological Function Testing, General & Clinical Testing, Esoteric Testing, Specialized Testing, Non-invasive Prenatal Testing, COVID-19 Testing, Others), By Disease (Cardiology, Oncology, Neurology, Orthopedics, Gastroenterology, Gynecology, Odontology, Others), By Revenue Source (Healthcare Plan, Out-of-Pocket, Public System), By Test Type (Pathology, Radiology), By End User (Referrals, Walk-ins, Corporate Clients) ... Read more

|

Major Players

|

Japan Diagnostic Labs Market Statistics and Insights, 2026

- Market Size Statistics

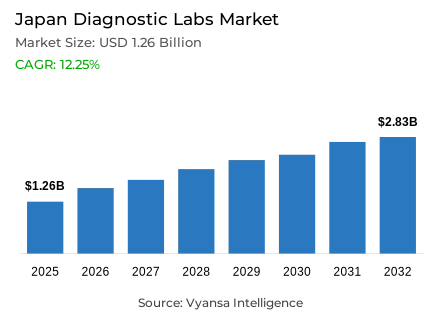

- Diagnostic labs market size in Japan was estimated at USD 1.26 billion in 2025.

- The market size is expected to grow to USD 2.83 billion by 2032.

- Market to register a CAGR of around 12.25% during 2026-32.

- Lab Type Shares

- Hospital-based laboratories grabbed market share of 50%.

- Competition

- Diagnostic labs in Japan is currently being catered to by more than 5 companies.

- Top 5 companies acquired around 70% of the market share.

- BML Inc., Forest Japan Medical Centre, H.U. Group, Miraca Holdings Inc., Eurofins Scientific (Genetic Lab) etc., are few of the top companies.

- Testing Services

- General & clinical testing grabbed 40% of the market.

Japan Diagnostic Labs Market Outlook

The diagnostic laboratories market in Japan is estimated at USD 1.26 billion in 2025 and is expected to be USD 2.83 billion in 2032 with a healthy CAGR of 12.25% in 2026-32. The main factor behind this strong growth is the aging population in the country, with the citizens aged 65 years and above constituting 29.3% of the total population. The geriatric population generates a long-term need of regular monitoring tests such as HbA1c, lipid profiles, kidney and liver function tests, and coagulation tests in hospitals, clinics, and long-term care centers. With the growing number of patients needing continuous monitoring to manage chronic diseases, and not a single diagnostic event, laboratories are becoming more concerned with rapid turnaround times and full automation to facilitate timely clinical decision-making.

The market is dominated by hospital-based labs with a 50% share, as they are essential in emergency care, inpatient monitoring, and time-sensitive tests where immediate results have a direct effect on patient outcomes. Their smooth connection with electronic health records and direct connection with ordering clinicians are of great benefit in sample prioritisation and critical value alerts. In the meantime, the testing services segment is dominated by general and clinical testing services with a 40% market share, including the basic diagnostic panels of complete blood counts, glucose levels, and electrolyte panels that constitute the core of daily medical practice.

The labor market has been experiencing a serious workforce problem because the working-age population (15-64 years) in Japan constitutes only 59.6% of the demographic composition, which poses a stiff competition to qualified laboratory technologists. Laboratories are speeding up investments in automation and workflow standardisation to overcome staffing limitations. Also, digital transformation is on the rise, and 28.4 million people are projected to be using My Number Cards to verify health-insurance by March 2025, allowing laboratories to minimize manual data-entry errors and enhance operational efficiency.

The high-rate scaling of cancer genomic testing, as demonstrated by 121,489 registered patients in the national C-CAT repository as of December 2025, offers promising growth opportunities to labs that can handle complex molecular processes and specialised quality needs.

Japan Diagnostic Labs Market Growth Driver

Demographic Aging Drives Sustained Diagnostic Demand

The diagnostic laboratories in Japan have a steady demand due to the aging population in the country, with the population aged 65 and older constituting 29.3% of the total population as of 1 October 2024. This demographic reality translates into elevated volumes of regular monitoring tests, such as HbA1c, lipid tests, kidney and liver tests, electrolytes, CRP, and coagulation tests, in hospitals, clinics, and long-term care centers. The elderly patients need regular monitoring of chronic illnesses, medication safety assessments, and pre-procedure examinations, which form a base of repeat test volumes that form the basis of market stability.

The aging patient mix essentially changes the priorities of laboratories to focus on the episodic diagnostic events to the continuous monitoring of the patient during long-term care paths. This development increases the strategic value of fast turnaround times, full automation platforms and standardized sample-handling procedures that allow clinicians to make timely treatment changes in routine care environments. By maximising these capabilities, laboratories can be in a position to facilitate the effective management of polypharmacy risks and avoidable complications in geriatric populations, thus increasing their value proposition in integrated care delivery models.

Japan Diagnostic Labs Market Challenge

Labor Market Constraints Challenge Operational Capacity

The workforce pressure is increasing on clinical laboratories because the working-age population (15-64 years) in Japan amounts to 73,728 thousand people, which is 59.6% of the demographic composition of the country as of 1 October 2024. This reduced labour pool has a direct limiting effect on the supply of trained technologists needed to prepare samples, operate the analyzers, validate results, and report critically- needed especially in STAT protocols and overnight shift cover. The small pool of candidates increases the competition among qualified staff in all facilities, increasing the cost of recruitment and prolonging the hiring process, at the same time making it more susceptible to service disruptions.

These personnel limitations pose operational weaknesses that are reflected in long turnaround times during periods of high demand, high overtime needs, and increased burnout risks among the available staff. Laboratories react by increasing investments in automation technologies, workflow standardisation projects, and selective outsourcing agreements to reduce reliance on manual processes. But these adaptations also require stricter quality-control measures, well-established escalation policies, and extensive retention programmes to ensure service continuity and avoid the loss of talented employees in a more competitive job market.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Japan Diagnostic Labs Market Trend

Digital Health Infrastructure Transforms Administrative Workflows

The Japanese healthcare system is undergoing a faster digitalisation of patient identification and insurance verification procedures, with 28.4 million people using My Number Cards as health-insurance identification by March 2025. This increasing usage is an indicator of increased patient acceptance of digital check-in processes and electronic eligibility confirmation systems in hospitals and clinics. The transition to identity-based verification is a radical change in the administrative processes, as paper-based operations are replaced by integrated digital routes that simplify the process of patient registration and data management.

In the case of diagnostic laboratories, this digital infrastructure transformation allows more accurate patient identification procedures and easier electronic connectivity between test ordering and delivery of results. Registration information obtained via digital verification systems minimizes manual data-entry needs and related transcription errors, and consent-based information sharing enables cleaner interfaces between laboratory information systems, barcode workflows, and compliance audit trails. Labs that actively match their technical infrastructure and operational workflows to these new digital standards achieve competitive advantages in the form of lower rates of clerical errors, shorter result-reporting cycles, and greater integration with larger healthcare IT ecosystems.

Japan Diagnostic Labs Market Opportunity

Genomic Medicine Expansion Creates Specialized Service Opportunities

Genomic testing of cancer is rapidly scaling in the Japanese healthcare environment, creating growing opportunities to laboratories that can handle complex molecular processes and high-quality standards. The national Cancer Genomic Information Management Centre (C‑CAT) repository reported 121,489 registered cancer gene panel testing data as at 31 December 2025, showing the rapidly growing collection of real-world genomic data to aid variant interpretation and therapy-matching decisions. This trend indicates a wider use of precision oncology methods in hospital networks and specialised cancer centres that aim to individualize treatment plans.

Labs located to provide end-to-end genomic testing services, including specialised tissue processing, next-generation sequencing services, bioinformatics analysis pipelines, and clinically actionable reporting, can develop preferred partner relationships with growing oncology programmes. In addition to the core testing capabilities, market opportunities are advanced sample logistics networks, reflex testing protocols to sequential analysis, and data governance frameworks that meet the standards of the public sector but allow the use of research. The barriers to entry posed by the complexity and specialised expertise needed to provide high-quality genomic services provide natural barriers to entry that defend market positions of laboratories that have invested in the required technology, personnel, and quality infrastructure.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Japan Diagnostic Labs Market Segmentation Analysis

By Lab Type

- Single/Independent Laboratories

- Hospital-based Laboratories

- Physician Office Laboratories

- Others

Hospital-based laboratories command the dominant position in the Japan diagnostic labs market by lab type segmentation, holding a 50% market share that reflects their essential role in acute care delivery. This leadership stems from hospitals' fundamental requirement for on-site testing capabilities supporting emergency presentations, inpatient monitoring protocols, surgical preparation, and time-critical clinical decisions where rapid results directly impact patient outcomes. Hospital laboratories maintain comprehensive testing capabilities spanning chemistry, hematology, microbiology, and blood bank services, enabling immediate response to diverse clinical needs without external dependencies that would compromise care quality or patient safety.

The integration advantages inherent to hospital-based operations strengthen their market position through direct connectivity with ordering clinicians and electronic health record systems. This seamless integration facilitates sophisticated sample prioritization logic, efficient repeat testing workflows, and immediate critical value notification protocols under unified governance frameworks. While independent and standalone laboratories serve important roles managing overflow volumes and providing convenient collection access for routine testing, hospital facilities remain the anchoring infrastructure for high-acuity diagnostic services and time-sensitive testing where proximity to clinical decision-makers creates irreplaceable value in care delivery pathways.

By Testing Services

- Physiological Function Testing

- General & Clinical Testing

- Esoteric Testing

- Specialized Testing

- Non-invasive Prenatal Testing

- COVID-19 Testing

- Others

General and clinical testing services hold the leading position within the testing services segmentation, capturing 40% of the market through their fundamental role in everyday clinical practice. This category encompasses the core diagnostic panels that form the foundation of medical evaluation: complete blood counts, glucose measurements, liver and kidney function assessments, lipid profiles, electrolyte panels, and urinalysis. Clinicians rely on these standardized tests for initial patient evaluations, chronic disease monitoring programs, treatment follow-ups, and routine health maintenance screenings, generating consistent high-volume demand that drives laboratory utilization patterns across all care settings.

The standardized nature and frequent repetition of general clinical testing panels shift competitive dynamics toward operational excellence in throughput capacity, analytical accuracy, and reporting speed rather than specialized interpretive expertise. Laboratories optimize these workflows through batch processing strategies, comprehensive automation platforms, and clearly defined reference ranges that enable clinicians to track patient trends over time with confidence. While advanced services including molecular diagnostics, anatomic pathology support, and specialty immunology contribute important value in complex clinical scenarios, general and clinical testing remains the workhorse category that anchors overall laboratory revenue streams and establishes the baseline service expectations that end users require from diagnostic providers.

List of Companies Covered in Japan Diagnostic Labs Market

The companies listed below are highly influential in the Japan diagnostic labs market, with a significant market share and a strong impact on industry developments.

- BML Inc.

- Forest Japan Medical Centre

- H.U. Group

- Miraca Holdings Inc.

- Eurofins Scientific (Genetic Lab)

Market News & Updates

- H.U. Group Holdings Inc., 2025:

H.U. Group Holdings, a leading Japanese clinical testing and diagnostics provider (also the parent of Fujirebio), announced in June 2025 that its subsidiary Fujirebio Diagnostics, Inc. acquired Plasma Services Group, Inc., strengthening its access to biological raw materials used in in-vitro diagnostics; it also expanded its assay portfolio with new CSF biomarker tests such as the Lumipulse G pTau217 for RUO research applications, demonstrating continued investment in advanced diagnostic technologies and global service capabilities.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. Japan Diagnostic Labs Market Policies, Regulations, and Standards

4. Japan Diagnostic Labs Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. Japan Diagnostic Labs Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in USD Million

5.2. Market Segmentation & Growth Outlook

5.2.1.By Lab Type

5.2.1.1. Single/Independent Laboratories- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Hospital-based Laboratories- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3. Physician Office Laboratories- Market Insights and Forecast 2022-2032, USD Million

5.2.1.4. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Testing Services

5.2.2.1. Physiological Function Testing- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. General & Clinical Testing- Market Insights and Forecast 2022-2032, USD Million

5.2.2.3. Esoteric Testing- Market Insights and Forecast 2022-2032, USD Million

5.2.2.4. Specialized Testing- Market Insights and Forecast 2022-2032, USD Million

5.2.2.5. Non-invasive Prenatal Testing- Market Insights and Forecast 2022-2032, USD Million

5.2.2.6. COVID-19 Testing- Market Insights and Forecast 2022-2032, USD Million

5.2.2.7. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Disease

5.2.3.1. Cardiology- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Oncology- Market Insights and Forecast 2022-2032, USD Million

5.2.3.3. Neurology- Market Insights and Forecast 2022-2032, USD Million

5.2.3.4. Orthopedics- Market Insights and Forecast 2022-2032, USD Million

5.2.3.5. Gastroenterology- Market Insights and Forecast 2022-2032, USD Million

5.2.3.6. Gynecology- Market Insights and Forecast 2022-2032, USD Million

5.2.3.7. Odontology- Market Insights and Forecast 2022-2032, USD Million

5.2.3.8. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Revenue Source

5.2.4.1. Healthcare Plan- Market Insights and Forecast 2022-2032, USD Million

5.2.4.2. Out-of-Pocket- Market Insights and Forecast 2022-2032, USD Million

5.2.4.3. Public System- Market Insights and Forecast 2022-2032, USD Million

5.2.5.By Test Type

5.2.5.1. Pathology- Market Insights and Forecast 2022-2032, USD Million

5.2.5.2. Radiology- Market Insights and Forecast 2022-2032, USD Million

5.2.6.By End User

5.2.6.1. Referrals- Market Insights and Forecast 2022-2032, USD Million

5.2.6.2. Walk-ins- Market Insights and Forecast 2022-2032, USD Million

5.2.6.3. Corporate Clients- Market Insights and Forecast 2022-2032, USD Million

5.2.7.By Competitors

5.2.7.1. Competition Characteristics

5.2.7.2. Market Share & Analysis

6. Japan Single/Independent Laboratories Market Statistics, 2022-2032

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in USD Million

6.2. Market Segmentation & Growth Outlook

6.2.1.By Testing Services- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Disease- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By Revenue Source- Market Insights and Forecast 2022-2032, USD Million

6.2.4.By Test Type- Market Insights and Forecast 2022-2032, USD Million

6.2.5.By End User- Market Insights and Forecast 2022-2032, USD Million

7. Japan Hospital-based Laboratories Market Statistics, 2022-2032

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in USD Million

7.2. Market Segmentation & Growth Outlook

7.2.1.By Testing Services- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Disease- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By Revenue Source- Market Insights and Forecast 2022-2032, USD Million

7.2.4.By Test Type- Market Insights and Forecast 2022-2032, USD Million

7.2.5.By End User- Market Insights and Forecast 2022-2032, USD Million

8. Japan Physician Office Laboratories Market Statistics, 2022-2032

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in USD Million

8.2. Market Segmentation & Growth Outlook

8.2.1.By Testing Services- Market Insights and Forecast 2022-2032, USD Million

8.2.2.By Disease- Market Insights and Forecast 2022-2032, USD Million

8.2.3.By Revenue Source- Market Insights and Forecast 2022-2032, USD Million

8.2.4.By Test Type- Market Insights and Forecast 2022-2032, USD Million

8.2.5.By End User- Market Insights and Forecast 2022-2032, USD Million

9. Competitive Outlook

9.1. Company Profiles

9.1.1.Miraca Holdings Inc.

9.1.1.1. Business Description

9.1.1.2. Service Portfolio

9.1.1.3. Collaborations & Alliances

9.1.1.4. Recent Developments

9.1.1.5. Financial Details

9.1.1.6. Others

9.1.2.Eurofins Scientific (Genetic Lab)

9.1.2.1. Business Description

9.1.2.2. Service Portfolio

9.1.2.3. Collaborations & Alliances

9.1.2.4. Recent Developments

9.1.2.5. Financial Details

9.1.2.6. Others

9.1.3.BML Inc.

9.1.3.1. Business Description

9.1.3.2. Service Portfolio

9.1.3.3. Collaborations & Alliances

9.1.3.4. Recent Developments

9.1.3.5. Financial Details

9.1.3.6. Others

9.1.4.Forest Japan Medical Centre

9.1.4.1. Business Description

9.1.4.2. Service Portfolio

9.1.4.3. Collaborations & Alliances

9.1.4.4. Recent Developments

9.1.4.5. Financial Details

9.1.4.6. Others

9.1.5.H.U. Group

9.1.5.1. Business Description

9.1.5.2. Service Portfolio

9.1.5.3. Collaborations & Alliances

9.1.5.4. Recent Developments

9.1.5.5. Financial Details

9.1.5.6. Others

10. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Lab Type |

|

| By Testing Services |

|

| By Disease |

|

| By Revenue Source |

|

| By Test Type |

|

| By End User |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.