Italy Sleep Aids Market Report: Trends, Growth and Forecast (2026-2032)

By Product (Single Ingredient (Doxylamine Succinate, Diphenhydramine, Melatonin), Combination Ingredient (Diphenhydramine + Acetaminophen, Other Antihistamine-Based Combinations), Herbal & Traditional Sleep Aids (Valerian root, Passionflower, Chamomile, Kava, Multi-Herbal Sleep Blends)), By Sleep Disorder (Insomnia, Sleep Apnea, Restless Legs Syndrome, Narcolepsy, Sleep Walking, Others), By Age Group (Young to Mid Adults (25-44 Years), Middle-Aged Adults (45-64 Years), Geriatric Population (65+ Years)), By Sales Channel (Retail Online, Retail Offline), By End User (Homecare/Individual Consumers, Hospitals, Sleep Centers & Clinics), By Formulation (Tablets, Gummies, Capsules, Liquid, Sublingual) ... Read more

|

Major Players

|

Italy Sleep Aids Market Statistics and Insights, 2026

- Market Size Statistics

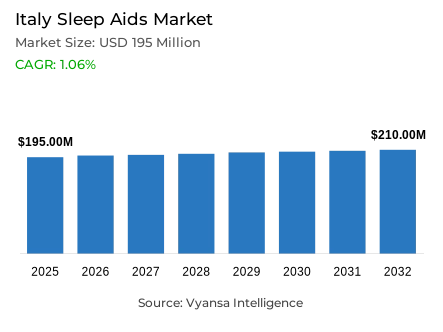

- Sleep aids market size in Italy was estimated at USD 195 million in 2025.

- The market size is expected to grow to USD 210 million by 2032.

- Market to register a CAGR of around 1.06% during 2026-32.

- Product Shares

- Herbal & traditional sleep aids grabbed market share of 40%.

- Competition

- More than 15 companies are actively engaged in producing sleep aids in Italy.

- Top 5 companies acquired around 40% of the market share.

- Uriach Italy Srl, ESI Srl, Carepharm Srl, Procter & Gamble Italia SpA, Opella Healthcare Italy Srl etc., are few of the top companies.

- Sales channel

- Retail offline grabbed 70% of the market.

Italy Sleep Aids Market Outlook

The Italy sleep aids market has entered a stabilization phase following the elevated demand observed during pandemic years. The market is valued at USD 195 million in 2025 and projected to reach USD 210 million in 2032, registering a CAGR of 1.06%. While post-pandemic normalization and economic caution have moderated recent sales momentum, structural awareness of sleep health remains higher than pre-2020 levels.

Herbal and Traditional Sleep Aids maintain a 40% share of the category. Although melatonin continues to regulate sleep-cycle positioning, consumer preference is gradually shifting toward botanicals such as valerian, chamomile, and lemon balm, perceived as safer and less invasive. Leading brands including Vicks ZzzQuil and Novanight sustain visibility through format innovation, particularly gummies and oral sprays.

Retail Offline channels account for 70% of total sales, underscoring the enduring importance of pharmacy-based trust. Demographic ageing remains a structural opportunity, as sleep disturbance prevalence increases among older adults. Women also represent a significant target group due to higher incidence of hormone-related sleep challenges.

Future category resilience will depend on effective alignment with preventive wellness trends. As consumers adopt relaxation practices and lifestyle adjustments alongside product use, growth opportunities will likely emerge through targeted segmentation strategies addressing specific needs, including menopause-related sleep disruption and digitally driven fatigue patterns.

Italy Sleep Aids Market Growth DriverAgeing Demographics Expand Structural Need for Sleep Support

Italy’s ageing population continues to expand the structurally vulnerable base for sleep-related disorders, including insomnia and nocturnal awakenings. According to the Italian National Institute of Statistics, individuals aged 65 years and above account for 24.3% of the total population, while the median age has reached 46.6 years, reflecting a mature demographic profile with elevated chronic care needs.

This demographic dynamic sustains steady engagement with sleep-support products that are framed as non-stimulating and suitable for routine home use. Older end users demonstrate preference for familiar retail channels and simplified dosing formats, reinforcing the ongoing relevance of melatonin-based and plant-derived solutions. As post-pandemic sleep awareness remains structurally higher, ageing acts as a long-term demand stabiliser independent of short-term economic cycles.

Italy Sleep Aids Market ChallengeReimbursement Pathways and Budget Caution Divert OTC Spend

Household financial caution and public reimbursement structures influence purchasing behavior. Eurostat reports Italy’s harmonised inflation rate at 2.0% in April 2025, indicating moderated but persistent consumer price sensitivity. Discretionary health spending, including OTC sleep aids, is increasingly evaluated against perceived value.

Meanwhile, the Organisation for Economic Co-operation and Development notes that 73% of Italy’s total health expenditure is financed through compulsory prepayment schemes. This systemic funding structure makes reimbursed prescription options financially attractive compared with out-of-pocket OTC purchases. The resulting demand shift intensifies competition on retail shelves and contributes to consolidation pressure among smaller players.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Italy Sleep Aids Market TrendDigital Wellness Routines Reduce Reliance on Traditional Aids

Digital engagement is transforming preventive health behaviors in Italy. According to the Italian National Institute of Statistics, 86.2% of households had internet access in 2024, while 81.9% of individuals aged six and above used the internet within the three months preceding the survey. Among households composed entirely of older individuals, access reached 60.6%, indicating narrowing digital gaps.

This widespread connectivity supports the adoption of guided relaxation content, structured bedtime applications, and lifestyle-tracking tools that integrate with product-based sleep solutions. Consequently, demand is gradually favoring accessible formats such as oral sprays and gummies, which align more closely with wellness positioning than traditional pharmaceutical tablets.

Italy Sleep Aids Market OpportunityCBD Safety Benchmarks Enable Premium, Compliant Formulation White Space

Regulatory clarification around cannabidiol (CBD) establishes a structured foundation for premium sleep formulations. In February 2026, the European Food Safety Authority set a temporary safe intake of proximately 2 milligrams per day, equivalent to approximately 2 milligrams daily for a 70-kilogram adult, while noting ongoing scientific data gaps.

This benchmark allows clearer dosing guidance and responsible product development in a category sensitive to dependency concerns and melatonin dosage limits. Premium combination formulations incorporating CBD with botanicals can target defined segments, including hormone-related sleep disturbance or circadian rhythm fatigue. Clear compliance and pharmacist-supported distribution enhance credibility, particularly within pharmacy-based retail environments.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Italy Sleep Aids Market Segmentation Analysis

By Product

- Single Ingredient

- Combination Ingredient

- Herbal & Traditional Sleep Aids

Herbal and Traditional Sleep Aids represent the leading product type, holding approximately 40% market share. This dominance aligns with end-user preference for solutions perceived as less pharmacologically aggressive and more suitable for regular use. Concerns around next-day drowsiness and long-term dependence continue to influence purchasing decisions, reinforcing the appeal of plant-based positioning.

Familiar botanicals such as chamomile, valerian, and lemon balm lower barriers to first trial and encourage repeat purchases across broad demographic groups. While melatonin remains a core active ingredient within major brand portfolios, differentiation increasingly occurs through botanical combinations and user-friendly delivery systems such as gummies and oral sprays. Natural-led formulations therefore remain central to category innovation and competitive positioning.

By Sales Channel

- Retail Online

- Retail Offline

Retail Offline holds approximately 70% market share and remains the dominant purchasing channel for sleep aids in Italy. Pharmacies and related retail outlets play a decisive role in shaping end-user choice through professional counselling, reassurance, and immediate product access—particularly important for health issues perceived as personal or sensitive.

Offline leadership is reinforced by the tendency of end users to compare OTC options with reimbursed prescription alternatives, creating demand for pharmacist guidance. Shelf visibility, trusted store formats, and long-standing brand recognition provide established players with competitive advantage, while smaller entrants face increasing consolidation pressure in a stabilizing market environment.

List of Companies Covered in Italy Sleep Aids Market

The companies listed below are highly influential in the Italy sleep aids market, with a significant market share and a strong impact on industry developments.

- Uriach Italy Srl

- ESI Srl

- Carepharm Srl

- Procter & Gamble Italia SpA

- Opella Healthcare Italy Srl

- Vemedia Pharma Italia Srl

- Aboca SpA

- Humana Italia SpA

- Nathura SpA

- Neuraxpharm Italy SpA

Competitive Landscape

Italy sleep aids market is characterised by post-pandemic normalisation and consolidation, with Procter & Gamble’s Vicks ZzzQuil and Opella Healthcare’s Novanight leading through strong brand equity, R&D investment, and appealing formats such as gummies and sprays. Melatonin remains the core active ingredient across most leading brands, though Aboca differentiates with melatonin-free herbal formulations, reflecting rising consumer preference for chamomile, valerian, lemon balm, and other plant-based solutions perceived as gentler. Smaller pandemic-era entrants are exiting amid intensified competition and softer demand, while reimbursed prescription products pose indirect competition to OTC options during economic strain. Future differentiation lies in senior-focused solutions, women-specific formulations, gamer and remote-worker targeting, and preventive wellness positioning that integrates sleep into broader holistic health routines.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Italy Sleep Aids Market Policies, Regulations, and Standards

- Italy Sleep Aids Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Italy Sleep Aids Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product

- Single Ingredient- Market Insights and Forecast 2022-2032, USD Million

- Doxylamine Succinate- Market Insights and Forecast 2022-2032, USD Million

- Diphenhydramine- Market Insights and Forecast 2022-2032, USD Million

- Melatonin- Market Insights and Forecast 2022-2032, USD Million

- Combination Ingredient- Market Insights and Forecast 2022-2032, USD Million

- Diphenhydramine + Acetaminophen- Market Insights and Forecast 2022-2032, USD Million

- Other Antihistamine-Based Combinations- Market Insights and Forecast 2022-2032, USD Million

- Herbal & Traditional Sleep Aids- Market Insights and Forecast 2022-2032, USD Million

- Valerian root- Market Insights and Forecast 2022-2032, USD Million

- Passionflower- Market Insights and Forecast 2022-2032, USD Million

- Chamomile- Market Insights and Forecast 2022-2032, USD Million

- Kava- Market Insights and Forecast 2022-2032, USD Million

- Multi-Herbal Sleep Blends- Market Insights and Forecast 2022-2032, USD Million

- Single Ingredient- Market Insights and Forecast 2022-2032, USD Million

- By Sleep Disorder

- Insomnia- Market Insights and Forecast 2022-2032, USD Million

- Sleep Apnea- Market Insights and Forecast 2022-2032, USD Million

- Restless Legs Syndrome- Market Insights and Forecast 2022-2032, USD Million

- Narcolepsy- Market Insights and Forecast 2022-2032, USD Million

- Sleep Walking- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Age Group

- Young to Mid Adults (25-44 Years)- Market Insights and Forecast 2022-2032, USD Million

- Middle-Aged Adults (45-64 Years)- Market Insights and Forecast 2022-2032, USD Million

- Geriatric Population (65+ Years)- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- By End User

- Homecare/Individual Consumers- Market Insights and Forecast 2022-2032, USD Million

- Hospitals- Market Insights and Forecast 2022-2032, USD Million

- Sleep Centers & Clinics- Market Insights and Forecast 2022-2032, USD Million

- By Formulation

- Tablets- Market Insights and Forecast 2022-2032, USD Million

- Gummies- Market Insights and Forecast 2022-2032, USD Million

- Capsules- Market Insights and Forecast 2022-2032, USD Million

- Liquid- Market Insights and Forecast 2022-2032, USD Million

- Sublingual- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Product

- Market Size & Growth Outlook

- Italy Single Ingredient Sleep Aids Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Sleep Disorder- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Formulation- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Italy Combination Ingredient Sleep Aids Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Sleep Disorder- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Formulation- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Italy Herbal & Traditional Sleep Aids Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Sleep Disorder- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Formulation- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Procter & Gamble Italia SpA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Opella Healthcare Italy Srl

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Vemedia Pharma Italia Srl

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Aboca SpA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Humana Italia SpA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Uriach Italy Srl

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- ESI Srl

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Carepharm Srl

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Nathura SpA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Neuraxpharm Italy SpA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Procter & Gamble Italia SpA

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product |

|

| By Sleep Disorder |

|

| By Age Group |

|

| By Sales Channel |

|

| By End User |

|

| By Formulation |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.