Italy Digestive Remedies Market Report: Trends, Growth and Forecast (2026-2032)

By Product Type (Paediatric Digestive Remedies (Paediatric Diarrhoeal Remedies, Paediatric Indigestion & Heartburn Remedies, Paediatric Laxatives, Paediatric Motion Sickness Remedies), Diarrhoeal Remedies, IBS Treatments, Indigestion & Heartburn Remedies (Antacids, Antiflatulents, Digestive Enzymes, H2 Blockers, Proton Pump Inhibitors), Laxatives, Motion Sickness Remedies), By Age Group (Children & Adolescents (01-17 years), Adults (18-65 years), Geriatric (65+ years)), By Sales Channel (Retail Online, Retail Offline (Hospitals, Clinics, Pharmacies)) ... Read more

|

Major Players

|

Italy Digestive Remedies Market Statistics and Insights, 2026

- Market Size Statistics

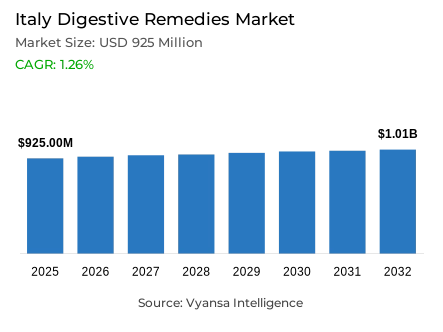

- Digestive remedies market size in Italy was valued at USD 925 million in 2025 and is estimated at USD 937 Million in 2026.

- The market size is expected to grow to USD 1.01 billion by 2032.

- Market to register a CAGR of around 1.26% during 2026-32.

- Product Type Shares

- Indigestion & heartburn remedies grabbed market share of 54%.

- Competition

- More than 20 companies are actively engaged in producing digestive remedies in Italy.

- Top 5 companies acquired around 35% of the market share.

- Bayer SpA, Haleon Italy Srl, ESI Srl, Opella Healthcare Italy Srl, Aboca SpA etc., are few of the top companies.

- Sales Channel

- Retail offline grabbed 85% of the market.

Italy Digestive Remedies Market Outlook

The Italy digestive remedies market size was valued at USD 925 million in 2025 and is projected to grow from USD 937 million in 2026 to USD 1.01 billion by 2032, exhibiting a CAGR of around 1.26% during the forecast period. Growth remains supported by demographic factors and lifestyle patterns that continue to keep digestive discomfort common across the population. The ageing population and active tourism flows both contribute to recurring demand for digestive relief products.

Ageing remains a structural factor supporting demand for digestive remedies in everyday self-care. In its 2025 Annual Report, Italian National Institute of Statistics (ISTAT) projects life expectancy to be 83.4 years as of 2024, with 1/4 of the population over age 65 and 4.6 million people over age 80; these demographics will increase the likelihood of people experiencing constipation, acid reflux, and other gastrointestinal issues. Of total sales, indigestion and acid reflux medications represent approximately 54 % of sales, indicating there is a large need for quick relief from acid and reflux.

However, purchasing patterns are strongly influenced by consumers' spending behaviours. In 2024, the Italian Medicines Agency (AIFA) expects citizens to spend EUR 10.2 billion of their own money on pharmaceutical products, with approximately 29.2% of the total amount spent on pharmaceuticals being purchases made by the consumer. As a result, the ISTAT has projected that inflation will continue at about 1.6% annually in February 2026, leading consumers to be careful about how they will spend their money on over-the-counter (OTC) products. This environment limits higher value growth potential for premium digestive remedy products, as consumers look to compare prices and choose cheaper alternatives to premium-priced products.

Currently, the distribution of digestive remedies is heavily reliant on traditional pharmacy and retail store entities. Approximately 85% of all sales of digestive remedies are made through retail entities, which speaks to the need for immediate access and provided professional advice by pharmacy professionals for consumers who are purchasing digestive remedies for their acid reflux symptoms, constipation, diarrhoea, or motion sickness type symptoms Tourism activity also reinforces category demand, as tourist arrivals rise by 4.5% in 2024 with 6 million additional arrivals and overnight stays increase by 4.2%, supporting continued use of digestive remedies linked to travel, irregular meals, and on-the-go symptom management.

Italy Digestive Remedies Market Growth DriverAgeing Population Sustains Everyday Relief Demand

A key driver for digestive remedies in Italy is the country’s ageing population. ISTAT’s 2025 Annual Report states that life expectancy at birth reaches 83.4 years, one quarter of residents are aged 65 or above, and the number of people aged over 80 is almost 4.6 million. This older consumer base is more exposed to constipation, reflux, dyspepsia, and other recurring digestive discomforts.

This demographic profile keeps demand steady for laxatives and antacids, especially products used for frequent or age-related digestive complaints. As older consumers manage multiple long-term conditions and regular medicine intake, digestive relief products remain relevant in daily self-care. That makes ageing a strong structural demand driver for the category in Italy.

Italy Digestive Remedies Market ChallengeHigh Personal Healthcare Spend Keeps Buyers Cautious

A major challenge for digestive remedies in Italy is consumer price sensitivity in self-medication. AIFA reports that citizens’ out-of-pocket pharmaceutical expenditure reaches EUR 10.2 billion in 2024, while 29.2% of medicine consumption is privately purchased. At the same time, ISTAT states that Italy’s consumer price index rises 1.6% year on year in February 2026. This keeps many households careful about non-essential OTC spending.

For digestive remedies, this caution can slow the uptake of higher-priced or premium-positioned products, especially in repeat-use categories such as laxatives and antacids. Consumers are more likely to compare prices, postpone purchases, or choose lower-cost alternatives when symptoms are manageable. As a result, affordability remains a real challenge for brands trying to grow value through innovation.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Italy Digestive Remedies Market TrendTargeted and Gentler Solutions Gain More Attention

In Italy, there is a noticeable shift towards more specific and easier to tolerate products for treating digestive health. According to AIFA, gastrointestinal and metabolism-related products are projected to be the second most consumed type of drug in 2024 with 296 daily doses per 1,000 residents, but are also expected to be the third highest in terms of sales at €3.5 billion. The average NHS cost of providing care for patients within this area will be €59.30 (5.1% increase from 2021).

The robust base of treatments supports a movement towards products created to address specific symptoms such as refluxing and "gentle" acting digestive health products. As consumers continue to seek out effective yet less aggressive treatment options for stomach and bowel issues when relieving symptoms of their digestive systems, we will see continued growth in these categories of targeted/mild digestive products.

Italy Digestive Remedies Market OpportunityTourism Creates More Travel-Linked Digestive Needs

A strong opportunity for digestive remedies in Italy comes from active tourism flows. ISTAT reports that in 2024, tourist arrivals rise by 4.5% with 6 million additional arrivals, while overnight stays increase by 4.2% with 19 million more presences. In the second quarter of 2025, arrivals grow another 1.1% and presences rise 4.7%, with foreign flows up 2.7% in arrivals and 5.9% in presences.

This creates room for motion sickness remedies, antacids, and diarrhoeal products, as travel often brings nausea, irregular meals, richer food intake, and stomach discomfort. It also supports easy-to-carry and quick-use formats that match travel behaviour. As tourism remains strong, brands have a good opportunity to connect digestive relief with travel convenience and immediate symptom management.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Italy Digestive Remedies Market Segmentation Analysis

By Product Type

- Paediatric Digestive Remedies

- Paediatric Diarrhoeal Remedies

- Paediatric Indigestion & Heartburn Remedies

- Paediatric Laxatives

- Paediatric Motion Sickness Remedies

- Diarrhoeal Remedies

- IBS Treatments

- Indigestion & Heartburn Remedies

- Antacids

- Antiflatulents

- Digestive Enzymes

- H2 Blockers

- Proton Pump Inhibitors

- Laxatives

- Motion Sickness Remedies

The segment has the highest share around product type under indigestion & heartburn remedies, with about 54% of the market. This segment leads because acidity, reflux, and indigestion are common digestive complaints that usually need quick and easy OTC relief. Strong consumer familiarity and the need for immediate symptom control also help this category stay ahead in Italy.

Its leadership is also supported by the broader medicine-use pattern in the country. AIFA states that gastrointestinal and metabolic drugs rank second in consumption in 2024 at 296 daily doses per 1,000 inhabitants and third in expenditure at EUR 3.5 billion. This large treatment base supports the dominance of indigestion and heartburn remedies within digestive care.

By Sales Channel

- Retail Online

- Retail Offline

- Hospitals

- Clinics

- Pharmacies

The segment has the highest share around sales channel under retail offline, with about 85% of the market. This dominance remains logical because digestive remedies are often bought for immediate use. Consumers usually prefer pharmacies and physical stores when they need fast relief from acidity, constipation, diarrhoea, bloating, or motion-related discomfort.

This pattern is supported by AIFA’s 2024 medicine-use data. In Italy, nearly 2 billion medicine packages are dispensed in public and private local care, while citizens’ out-of-pocket pharmaceutical spending reaches EUR 10.2 billion. These figures show how important local physical purchase points remain for self-care categories. That is why retail offline continues to lead digestive remedies sales in the country.

List of Companies Covered in Italy Digestive Remedies Market

The companies listed below are highly influential in the Italy digestive remedies market, with a significant market share and a strong impact on industry developments.

- Bayer SpA

- Haleon Italy Srl

- ESI Srl

- Opella Healthcare Italy Srl

- Aboca SpA

- Johnson & Johnson SpA

- Reckitt Benckiser Healthcare Italia SpA

- Alfasigma SpA

- Societa Prodotti Antibiotici SpA

- Medical Pharma Srl

Competitive Landscape

In 2025, the competitive landscape of digestive remedies in Italy was moderately fragmented, with Opella Healthcare Italy Srl leading the market with a 14.3% retail value share, followed by Aboca SpA at 6.1%. Opella Healthcare benefits from strong demand for well-established brands such as Dulcolax and Dulcosoft in the laxatives category, supported by growing consumer preference for gentler osmotic products based on macrogol. Aboca SpA maintains a notable position through its focus on natural and herbal digestive solutions, which aligns with the increasing consumer preference for plant-based and holistic health products. Demand for digestive remedies in Italy continues to be supported by the ageing population, sedentary lifestyles associated with remote work, and rising stress levels that contribute to digestive issues such as constipation, reflux and irritable bowel syndrome. However, the category also faces growing competition from fibre supplements, probiotics and other natural preventive solutions, as many Italian consumers are increasingly adopting healthier diets and focusing on gut health and lifestyle changes to prevent digestive problems rather than relying solely on traditional remedies.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Italy Digestive Remedies Market Policies, Regulations, and Standards

- Italy Digestive Remedies Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Italy Digestive Remedies Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product Type

- Paediatric Digestive Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Diarrhoeal Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Indigestion & Heartburn Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Laxatives- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Motion Sickness Remedies- Market Insights and Forecast 2022-2032, USD Million

- Diarrhoeal Remedies- Market Insights and Forecast 2022-2032, USD Million

- IBS Treatments- Market Insights and Forecast 2022-2032, USD Million

- Indigestion & Heartburn Remedies- Market Insights and Forecast 2022-2032, USD Million

- Antacids- Market Insights and Forecast 2022-2032, USD Million

- Antiflatulents- Market Insights and Forecast 2022-2032, USD Million

- Digestive Enzymes- Market Insights and Forecast 2022-2032, USD Million

- H2 Blockers- Market Insights and Forecast 2022-2032, USD Million

- Proton Pump Inhibitors- Market Insights and Forecast 2022-2032, USD Million

- Laxatives- Market Insights and Forecast 2022-2032, USD Million

- Motion Sickness Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Digestive Remedies- Market Insights and Forecast 2022-2032, USD Million

- By Age Group

- Children & Adolescents (01-17 years)- Market Insights and Forecast 2022-2032, USD Million

- Adults (18-65 years)- Market Insights and Forecast 2022-2032, USD Million

- Geriatric (65+ years)- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- Hospitals- Market Insights and Forecast 2022-2032, USD Million

- Clinics- Market Insights and Forecast 2022-2032, USD Million

- Pharmacies- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Product Type

- Market Size & Growth Outlook

- Italy Paediatric Digestive Remedies Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Italy Diarrhoeal Remedies Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Italy IBS Treatments Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Italy Indigestion & Heartburn Remedies Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Italy Laxatives Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Italy Motion Sickness Remedies Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Opella Healthcare Italy Srl

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Aboca SpA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Johnson & Johnson SpA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Reckitt Benckiser Healthcare Italia SpA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Alfasigma SpA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Bayer SpA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Haleon Italy Srl

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- ESI Srl

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Societa Prodotti Antibiotici SpA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Medical Pharma Srl

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Opella Healthcare Italy Srl

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Age Group |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.