Israel Sleep Aids Market Report: Trends, Growth and Forecast (2026-2032)

By Product (Single Ingredient (Doxylamine Succinate, Diphenhydramine, Melatonin), Combination Ingredient (Diphenhydramine + Acetaminophen, Other Antihistamine-Based Combinations), Herbal & Traditional Sleep Aids (Valerian root, Passionflower, Chamomile, Kava, Multi-Herbal Sleep Blends)), By Sleep Disorder (Insomnia, Sleep Apnea, Restless Legs Syndrome, Narcolepsy, Sleep Walking, Others), By Age Group (Young to Mid Adults (25-44 Years), Middle-Aged Adults (45-64 Years), Geriatric Population (65+ Years)), By Sales Channel (Retail Online, Retail Offline), By End User (Homecare/Individual Consumers, Hospitals, Sleep Centers & Clinics), By Formulation (Tablets, Gummies, Capsules, Liquid, Sublingual) ... Read more

|

Major Players

|

Israel Sleep Aids Market Statistics and Insights, 2026

- Market Size Statistics

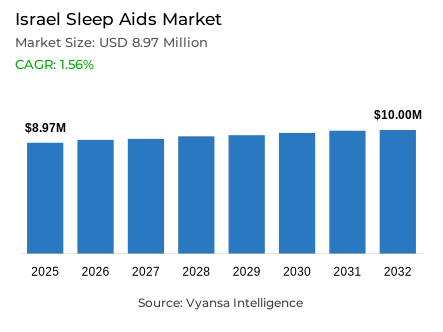

- Sleep aids market size in Israel was estimated at USD 8.97 million in 2025

- The market size is expected to grow to USD 10 million by 2032.

- Market to register a CAGR of around 1.56% during 2026-32.

- Product Shares

- Single ingredient grabbed market share of 45%.

- Competition

- More than 5 companies are actively engaged in producing sleep aids in Israel.

- Top 5 companies acquired around 90% of the market share.

- Trima Israel Pharmaceutical Products Maabarot Ltd, Chemipal Ltd, Super-Pharm (Israel) Ltd, Neopharm (Israel) 1996 Ltd, CTS Chemical Industries Ltd etc., are few of the top companies.

- Sales channel

- Retail offline grabbed 60% of the market.

Israel Sleep Aids Market Outlook

The Israel sleep aids market is shaped by sustained geopolitical stress and demographic ageing dynamics. The market is valued at USD 8.97 million in 2025 and is projected to reach USD 10 million by 2032, reflecting a CAGR of 1.56%. Persistent psychological strain linked to prolonged regional instability continues to elevate sleep disturbance prevalence, while an ageing population sustains baseline demand for gentler, non-habit-forming support products.

Single-Ingredient products lead with 45% market share, supported by demand for clarity and controlled usage. However, herbal and traditional positioning is gaining traction as health-conscious end users increasingly favor natural formulations. Melatonin remains relevant but is influenced by regulatory positioning, which encourages certain demographics to seek alternatives or explore international retail online channels.

Retail Offline channels account for 60% of market distribution, with pharmacies acting as trusted intermediaries. Cost sensitivity remains a structural constraint, particularly following the VAT increase to 18% in 2025, which intensifies price awareness across income groups.

Looking ahead, growth will remain moderate but structurally supported. As long as mental well-being remains under pressure, demand for accessible, clean-label, short-term sleep support will persist. Brands that combine affordability, transparent formulation, and pharmacist-backed credibility will be best positioned to sustain relevance through 2032.

Israel Sleep Aids Market Growth DriverConflict-Related Stress Sustains Elevated Short-Term Sleep Demand

Ongoing security tensions continue to exert measurable psychological pressure across Israel, reinforcing structural demand for accessible sleep-support solutions. According to the Ministry of Health, data released in November 2025 indicate that 83% of teenagers have experienced emotional distress since 7 October. This elevated stress environment translates into higher prevalence of sleep-onset difficulties and interrupted sleep cycles across households.

In this context, pharmacies remain a critical access point for non-prescription sleep aids that provide short-term symptomatic relief. Persistent uncertainty sustains category relevance, even as households moderate discretionary expenditure. Immediate availability and perceived safety are central to purchase decisions, particularly for temporary use during acute stress periods.

Israel Sleep Aids Market ChallengeVAT and Cost Pressure Weakens Discretionary Purchase Frequency

Rising indirect taxation is increasing cost pressure on over-the-counter sleep aids. According to the Government of Israel, the value-added tax rate stands at 18% effective 1 January 2025. This upward adjustment contributes directly to higher retail shelf prices across pharmacy channels.

Combined with broader economic slowdown linked to prolonged conflict conditions, higher VAT amplifies household price sensitivity. End users may delay purchases, reduce frequency of use, or revert to low-cost home-prepared remedies. The category therefore faces margin constraints and softer repeat purchasing behavior, particularly among lower-income groups.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Israel Sleep Aids Market TrendPrescription Constraints Push Cross-Border Online Sourcing

Domestic retail limitations are increasingly bypassed through international etail online platforms. End users seeking melatonin or herbal sleep solutions are turning to cross-border retail online sources, diversifying brand exposure beyond traditional pharmacy shelves. This behavior redistributes part of category demand outside local retail infrastructure.

Clinical positioning also influences purchasing patterns. The European Medicines Agency notes that prolonged-release melatonin product Circadin was evaluated in 681 patients aged 55 years and above with primary insomnia. This age-specific framing reinforces melatonin’s association with older adults, while younger consumers increasingly experiment with packaged herbal alternatives aligned with lifestyle-oriented wellness narratives.

Israel Sleep Aids Market OpportunityDeepening Natural Health Preferences Open a Clear Runway for Herbal Variants

Heightened caution toward synthetic sleep medications creates runway for herbal and traditional formulations. Brands can expand packaged botanical portfolios positioned as routine-compatible and non-habit-forming alternatives to conventional sedatives. Convenient delivery systems provide structured substitutes for home-prepared remedies while maintaining natural credibility.

Global health patterns support this trajectory. In December 2025, the World Health Organization reported that nearly 90% of Member States indicate 40% to 90% of their populations use traditional medicine. This widespread familiarity strengthens acceptance of herbal sleep aids and supports premium positioning for plant-based formulations within Israel’s pharmacy-based retail environment.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Israel Sleep Aids Market Segmentation Analysis

By Product

- Single Ingredient

- Combination Ingredient

- Herbal & Traditional Sleep Aids

The segment with highest market share under Product is Single-Ingredient formulations account for 45% of total market share, positioning them as the dominant segment. This leadership reflects end-user preference for straightforward solutions that are easy to understand, dose, and integrate into short-term coping routines during stress-related sleep disturbance. Predictability of effect and clarity of active content are particularly valued by first-time purchasers seeking a controlled entry into the category.

Single-ingredient formats also align with broader caution around dependency and over-medication. In a market shaped by psychological strain and heightened sensitivity toward pharmaceutical intensity, simplified positioning facilitates quicker purchase decisions at the pharmacy shelf. Clear labeling and limited formulation complexity reinforce trust, making this segment the default option in a competitive environment where reassurance and transparency are central to brand selection.

By Sales Channel

- Retail Online

- Retail Offline

Retail Offline holds 60% of total market share and remains the primary distribution channel for sleep aid products in Israel. This dominance is driven by the reactive nature of purchasing behavior, where demand is often triggered by acute insomnia episodes or anxiety-related sleep disruption. Physical pharmacies provide immediate access, professional reassurance, and on-the-spot product comparison, which are critical in health-sensitive categories.

Offline retail also benefits from entrenched purchasing habits and trust in pharmacist guidance. In-store consultation reduces perceived risk related to side effects or dependency concerns and supports short-term usage decisions. Although cross-border retail online purchasing is expanding—particularly for products with local regulatory constraints—physical stores continue to anchor category sales due to speed, familiarity, and perceived reliability.

List of Companies Covered in Israel Sleep Aids Market

The companies listed below are highly influential in the Israel sleep aids market, with a significant market share and a strong impact on industry developments.

- Trima Israel Pharmaceutical Products Maabarot Ltd

- Chemipal Ltd

- Super-Pharm (Israel) Ltd

- Neopharm (Israel) 1996 Ltd

- CTS Chemical Industries Ltd

- Perrigo Israel Pharmaceuticals Ltd

- Sam-On Pharmaceuticals Chemicals Ltd

Competitive Landscape

Israel sleep aids market is led by herbal/traditional brands, with Nerven Dragees holding the top value position as consumers shift toward gentler, plant-based solutions amid heightened anxiety linked to the Israel-Hamas war. Demand is further supported by an ageing population seeking alternatives to prescription hypnotics perceived as harmful for long-term use. While melatonin benefits from its natural image, regulatory restrictions limit domestic OTC availability, driving cross-border online purchases and creating leakage from local retail. Competitive intensity remains moderate, with pharmacies as the primary channel. Key differentiation opportunities include clinically validated herbal formulations, senior-targeted positioning, stress-relief and trauma-support blends, and value-tier offerings to mitigate potential VAT-driven price sensitivity.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Israel Sleep Aids Market Policies, Regulations, and Standards

- Israel Sleep Aids Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Israel Sleep Aids Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product

- Single Ingredient- Market Insights and Forecast 2022-2032, USD Million

- Doxylamine Succinate- Market Insights and Forecast 2022-2032, USD Million

- Diphenhydramine- Market Insights and Forecast 2022-2032, USD Million

- Melatonin- Market Insights and Forecast 2022-2032, USD Million

- Combination Ingredient- Market Insights and Forecast 2022-2032, USD Million

- Diphenhydramine + Acetaminophen- Market Insights and Forecast 2022-2032, USD Million

- Other Antihistamine-Based Combinations- Market Insights and Forecast 2022-2032, USD Million

- Herbal & Traditional Sleep Aids- Market Insights and Forecast 2022-2032, USD Million

- Valerian root- Market Insights and Forecast 2022-2032, USD Million

- Passionflower- Market Insights and Forecast 2022-2032, USD Million

- Chamomile- Market Insights and Forecast 2022-2032, USD Million

- Kava- Market Insights and Forecast 2022-2032, USD Million

- Multi-Herbal Sleep Blends- Market Insights and Forecast 2022-2032, USD Million

- Single Ingredient- Market Insights and Forecast 2022-2032, USD Million

- By Sleep Disorder

- Insomnia- Market Insights and Forecast 2022-2032, USD Million

- Sleep Apnea- Market Insights and Forecast 2022-2032, USD Million

- Restless Legs Syndrome- Market Insights and Forecast 2022-2032, USD Million

- Narcolepsy- Market Insights and Forecast 2022-2032, USD Million

- Sleep Walking- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Age Group

- Young to Mid Adults (25-44 Years)- Market Insights and Forecast 2022-2032, USD Million

- Middle-Aged Adults (45-64 Years)- Market Insights and Forecast 2022-2032, USD Million

- Geriatric Population (65+ Years)- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- By End User

- Homecare/Individual Consumers- Market Insights and Forecast 2022-2032, USD Million

- Hospitals- Market Insights and Forecast 2022-2032, USD Million

- Sleep Centers & Clinics- Market Insights and Forecast 2022-2032, USD Million

- By Formulation

- Tablets- Market Insights and Forecast 2022-2032, USD Million

- Gummies- Market Insights and Forecast 2022-2032, USD Million

- Capsules- Market Insights and Forecast 2022-2032, USD Million

- Liquid- Market Insights and Forecast 2022-2032, USD Million

- Sublingual- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Product

- Market Size & Growth Outlook

- Israel Single Ingredient Sleep Aids Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Sleep Disorder- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Formulation- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Israel Combination Ingredient Sleep Aids Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Sleep Disorder- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Formulation- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Israel Herbal & Traditional Sleep Aids Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Sleep Disorder- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Formulation- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Neopharm (Israel) 1996 Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- CTS Chemical Industries Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Perrigo Israel Pharmaceuticals Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Sam-On Pharmaceuticals Chemicals Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Trima Israel Pharmaceutical Products Maabarot Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Chemipal Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Super-Pharm (Israel) Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Neopharm (Israel) 1996 Ltd

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product |

|

| By Sleep Disorder |

|

| By Age Group |

|

| By Sales Channel |

|

| By End User |

|

| By Formulation |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.