Indonesia Diagnostic Labs Market Report: Trends, Growth and Forecast (2026-2032)

By Lab Type (Single/Independent Laboratories, Hospital-based Laboratories, Physician Office Laboratories, Others), By Testing Services (Physiological Function Testing, General & Clinical Testing, Esoteric Testing, Specialized Testing, Non-invasive Prenatal Testing, COVID-19 Testing, Others), By Disease (Cardiology, Oncology, Neurology, Orthopedics, Gastroenterology, Gynecology, Odontology, Others), By Revenue Source (Healthcare Plan, Out-of-Pocket, Public System), By Test Type (Pathology, Radiology), By End User (Referrals, Walk-ins, Corporate Clients), By Region (Sumatra, Java, Kalimantan, Sulawesi, Others) ... Read more

|

Major Players

|

Indonesia Diagnostic Labs Market Statistics and Insights, 2026

- Market Size Statistics

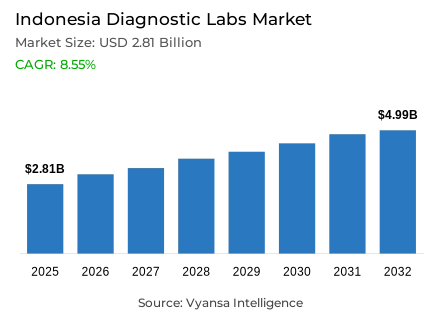

- Diagnostic labs market size in Indonesia was estimated at USD 2.81 billion in 2025.

- The market size is expected to grow to USD 4.99 billion by 2032.

- Market to register a CAGR of around 8.55% during 2026-32.

- Lab Type Shares

- Hospital-based laboratories grabbed market share of 55%.

- Competition

- Diagnostic labs in Indonesia is currently being catered to by more than 10 companies.

- Top 5 companies acquired around 65% of the market share.

- PT Indec Diagnostics, Ultra Medica Clinic Surabaya, PT Prima Medika Laboratories, PT Kimia Farma Diagnostika, PT Prodia Diacro Laboratories etc., are few of the top companies.

- Testing Services

- General & clinical testing grabbed 50% of the market.

Indonesia Diagnostic Labs Market Outlook

Indonesia diagnostic labs market is poised for substantial expansion over the forecast period, with the market valued at USD 2.81 billion in 2025 and projected to reach USD 4.99 billion by 2032. The market is expected to register a robust CAGR of around 8.55% during 2026-32, driven by the near-universal reach of the national health insurance scheme (JKN) covering approximately 95% of the population. This extensive insurance coverage has reduced out-of-pocket health expenditures to just 27.5% of total health spending, enabling previously underserved populations to access diagnostic services without financial constraints. The expansion has directly translated into increased patient visits and laboratory test orders, as routine procedures like blood work and disease screenings now fall under insurance reimbursement, fueling sustained demand growth across the country.

The diagnostic labs dynamics are shaped by significant infrastructure challenges alongside promising technological advancements. While healthcare facilities face suboptimal laboratory capacity, logistical constraints, and inadequate staff training—particularly in rural areas where test results can take over a week—the sector is simultaneously embracing digital transformation. The health ministry's establishment of a joint AI laboratory in 2026 and strategic plans for domestic production of molecular rapid-test kits demonstrate Indonesia's commitment to modernizing diagnostic capabilities. International support, including a $25 million Pandemic Fund grant awarded in 2024, provides crucial resources for upgrading laboratory networks and establishing integrated One Health systems linking human and animal health facilities.

The market structure is dominated by hospital-based laboratories, accounting for around 55% of the country's total testing capacity. These laboratories, being an integral part of large hospital networks, have access to better equipment, larger patient bases, and a wide range of testing capabilities, making them the primary force behind Indonesia's diagnostic landscape. The remaining 45% is accounted for by freestanding laboratories, private pathology centers, and smaller public health facilities that usually perform routine testing with relatively smaller patient bases.

General and Clinical Testing is the single largest service segment, accounting for around 50% of the country's total testing volume. This service segment encompasses high-volume routine tests such as complete blood counts, blood chemistry analyses, and urinalyses, which are used as primary diagnostic aids in all healthcare settings. Specialized testing services, encompassing medical imaging, pathology, genetic analyses, and advanced molecular testing, together account for the other 50% of the country's total testing volume, reflecting the balanced market composition between routine and specialized types of diagnostic tests.

Indonesia Diagnostic Labs Market Growth DriverExpanding Universal Health Coverage Drives Diagnostic Demand

The national health insurance scheme (JKN) in Indonesia has reached a near-universal coverage of over 260 million people or about 95% of the population by December 2023. This broadening of the insurance coverage has essentially changed the accessibility of healthcare, decreasing out-of-pocket health spending to only 27.5% of total health spending. The radical reduction of financial obstacles has enabled hitherto underserved groups to access medical diagnostics via government-funded healthcare systems, thus establishing a major change in healthcare utilisation trends throughout the archipelago.

The growth of insurance cover has had a direct impact of increasing the number of patients visiting the healthcare centers and the number of laboratory test requests in the healthcare centers across Indonesia. Regular diagnostic tests such as blood tests, screening of diseases, and monitoring of chronic conditions are now under insurance reimbursement, thus eliminating cost-related barriers to patients seeking medical attention. This increased accessibility promotes prompt testing of infectious and chronic diseases, which will promote long-term development of diagnostic laboratory use in the country. There is an increasing demand of laboratory services by healthcare providers as insured patients are actively seeking preventive and diagnostic tests that were once unaffordable.

Indonesia Diagnostic Labs Market ChallengeInfrastructure Deficiencies Constrain Market Growth

The diagnostic laboratory industry in Indonesia is faced with a major infrastructure problem that limits the capacity of service delivery in the market. Laboratory capacity, logistical issues, and lack of staff training are cited by healthcare facilities as the main operational challenges. Many community labs do not have sophisticated diagnostic tools and skilled technologists to conduct a full testing panel in their localities. Lack of quality control and insufficient training programmes also worsen the capacity of laboratories to provide precise and timely results, which introduces bottlenecks in the diagnostic process and restricts the range of tests that can be performed.

These capacity constraints are aggravated by geographic differences, where rural and remote areas face especially severe restrictions. Outlying diagnostic samples are often transported to other island-based laboratories, which leads to turnaround times of more than one week on critical test results. These long waits and disproportionate distribution of infrastructure lead to slower diagnosis and initiation of treatment in peripheral areas, which negatively impacts patient outcomes. The infrastructure disparity highlights the necessity of urgent laboratory improvements, equipment funding, and extensive training programmes in underserved communities to create equal diagnostic opportunities across the country.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Indonesia Diagnostic Labs Market TrendDigital Health Integration and AI-Powered Diagnostics Emerge

Indonesia is also embracing the use of modern digital technologies to modernise its diagnostic services by engaging in strategic international partnerships. The Ministry of Health opened a joint laboratory in 2026 focused on the application of artificial intelligence in medical diagnostics, which is an indication of a significant investment in technological development. This project focuses on the implementation of AI-based analytics and mobile health systems to improve the early disease detection and patient management systems. Indonesian health authorities are developing advanced ability to identify diseases and optimise treatment in a short time by combining artificial intelligence with genomics data and clinical information.

The digital revolution is specifically applied to molecular diagnostics and imaging technologies, with a specific focus on high-burden diseases like tuberculosis. Authorities are working on AI-based imaging analysis systems and fast-test solutions to speed up the diagnosis process by a large margin. Strategic plans also involve the development of domestic production of molecular rapid-test kits, which will minimize reliance on imported diagnostic supplies. These projects are indicative of a larger trend of digital health solutions and indigenous innovation in laboratory testing, which places Indonesia in a position to utilize the latest technologies to achieve better population health outcomes and diagnostic efficiency.

Indonesia Diagnostic Labs Market OpportunityGlobal Partnerships Create Laboratory Expansion

Indonesia has received significant foreign funding to enhance its diagnostic laboratory facilities within the global health security systems. In 2024, the Pandemic Fund granted US $25 million to Indonesia to support the improvement of surveillance systems and laboratory networks, with further co-financing agreements. The funding opportunity aims to support pandemic preparedness by implementing a One Health approach that combines human and animal health surveillance, which will establish a strong base to expand laboratory systems and capacity building in various sectors in the future.

The funded programs focus on strategic laboratory network development and capacity enhancement projects. The major activities involve the development of an integrated One Health Laboratory Network between human and animal health facilities, modernization of laboratory equipment and referral systems, building of modern sample storage facilities, and creation of new diagnostic testing facilities. Detailed staff training programmes on biosafety measures and quality management systems are also key elements of this investment. These international collaborations and investments offer huge potentials to the Indonesian diagnostic laboratories to improve technical capacity, increase service coverage, and resilience to emerging health threats.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Indonesia Diagnostic Labs Market Segmentation Analysis

By Lab Type

- Single/Independent Laboratories

- Hospital-based Laboratories

- Physician Office Laboratories

- Others

Hospital-based laboratories currently hold the leading market share in the Indonesia diagnostic labs market, accounting for about 55% of the country's total testing capacity. These labs are established within large hospital networks and offer comprehensive clinical testing services to inpatients and outpatients. Their association with large hospital networks gives them access to sophisticated diagnostic equipment, larger patient volumes, and broader testing capabilities compared to other types of laboratories. This allows hospital-based labs to be the driving force behind Indonesia's diagnostic testing market, processing more than half of the total diagnostic tests conducted in the country.

The other 45% of the total testing capacity in the Indonesia diagnostic labs market is accounted for by standalone labs, private pathology centers, and smaller public health facilities. These types of laboratories are known to perform standard testing procedures and handle relatively smaller patient volumes per laboratory. Although these laboratory types make a significant contribution to the diagnostic testing market, their smaller size and reduced testing capabilities make them less dominant compared to hospital-based labs. The significantly high dominance of hospital-based labs in the Indonesia diagnostic labs market can be attributed to the country's hospital-based healthcare delivery system, where diagnostic testing is largely centralized within large hospital networks.

By Testing Services

- Physiological Function Testing

- General & Clinical Testing

- Esoteric Testing

- Specialized Testing

- Non-invasive Prenatal Testing

- COVID-19 Testing

- Others

General and Clinical Testing is the largest market segment in the Indonesia diagnostic labs market, accounting for around 50% of the total share of testing. This major market segment includes high-volume general clinical laboratory tests such as complete blood counts, comprehensive blood chemistry analyses, and urinalyses ordered by general practitioners and hospital-based physicians. The broad-based demand for these basic diagnostic tests in all types of healthcare facilities and patient populations fuels the high volume that defines this market segment. These general clinical tests are basic diagnostic tools used for general health evaluations, chronic disease monitoring, and acute illness assessments, which explains their major market share.

Specialized testing services, taken together, account for the remaining 50% of the total diagnostic activity, including medical imaging studies such as X-rays and CT scans, and pathology services such as tissue biopsies, genetic analyses, and advanced molecular testing. Although each of these specialized testing services is an important component of contemporary diagnostic medicine, especially medical imaging studies for comprehensive disease diagnosis, they are individually smaller market segments than general clinical testing. The fragmented nature of specialized testing services into several distinct market segments, along with their lower testing rates and higher levels of complexity, defines their combined but distributed market share. The adaptability and high demand for general clinical testing establish this market segment as the major player in the Indonesia diagnostic labs market.

List of Companies Covered in Indonesia Diagnostic Labs Market

The companies listed below are highly influential in the Indonesia diagnostic labs market, with a significant market share and a strong impact on industry developments.

- PT Indec Diagnostics

- Ultra Medica Clinic Surabaya

- PT Prima Medika Laboratories

- PT Kimia Farma Diagnostika

- PT Prodia Diacro Laboratories

- Laboratorium Klinik CITO Indraprasta Semarang

- Bio Medika Kelapa Gading

- Laboratorium Parahita Diagnostic Center

- ABC Central Clinical Laboratory

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Indonesia Diagnostic Labs Market Policies, Regulations, and Standards

- Indonesia Diagnostic Labs Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Indonesia Diagnostic Labs Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Lab Type

- Single/Independent Laboratories- Market Insights and Forecast 2022-2032, USD Million

- Hospital-based Laboratories- Market Insights and Forecast 2022-2032, USD Million

- Physician Office Laboratories- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Testing Services

- Physiological Function Testing- Market Insights and Forecast 2022-2032, USD Million

- General & Clinical Testing- Market Insights and Forecast 2022-2032, USD Million

- Esoteric Testing- Market Insights and Forecast 2022-2032, USD Million

- Specialized Testing- Market Insights and Forecast 2022-2032, USD Million

- Non-invasive Prenatal Testing- Market Insights and Forecast 2022-2032, USD Million

- COVID-19 Testing- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Disease

- Cardiology- Market Insights and Forecast 2022-2032, USD Million

- Oncology- Market Insights and Forecast 2022-2032, USD Million

- Neurology- Market Insights and Forecast 2022-2032, USD Million

- Orthopedics- Market Insights and Forecast 2022-2032, USD Million

- Gastroenterology- Market Insights and Forecast 2022-2032, USD Million

- Gynecology- Market Insights and Forecast 2022-2032, USD Million

- Odontology- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Revenue Source

- Healthcare Plan- Market Insights and Forecast 2022-2032, USD Million

- Out-of-Pocket- Market Insights and Forecast 2022-2032, USD Million

- Public System- Market Insights and Forecast 2022-2032, USD Million

- By Test Type

- Pathology- Market Insights and Forecast 2022-2032, USD Million

- Radiology- Market Insights and Forecast 2022-2032, USD Million

- By End User

- Referrals- Market Insights and Forecast 2022-2032, USD Million

- Walk-ins- Market Insights and Forecast 2022-2032, USD Million

- Corporate Clients- Market Insights and Forecast 2022-2032, USD Million

- By Region

- Sumatra

- Java

- Kalimantan

- Sulawesi

- Others

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Lab Type

- Market Size & Growth Outlook

- Indonesia Single/Independent Laboratories Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Testing Services- Market Insights and Forecast 2022-2032, USD Million

- By Disease- Market Insights and Forecast 2022-2032, USD Million

- By Revenue Source- Market Insights and Forecast 2022-2032, USD Million

- By Test Type- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Indonesia Hospital-based Laboratories Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Testing Services- Market Insights and Forecast 2022-2032, USD Million

- By Disease- Market Insights and Forecast 2022-2032, USD Million

- By Revenue Source- Market Insights and Forecast 2022-2032, USD Million

- By Test Type- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Indonesia Physician Office Laboratories Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Testing Services- Market Insights and Forecast 2022-2032, USD Million

- By Disease- Market Insights and Forecast 2022-2032, USD Million

- By Revenue Source- Market Insights and Forecast 2022-2032, USD Million

- By Test Type- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- PT Kimia Farma Diagnostika

- Business Description

- Service Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- PT Prodia Diacro Laboratories

- Business Description

- Service Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Laboratorium Klinik CITO Indraprasta Semarang

- Business Description

- Service Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Bio Medika Kelapa Gading

- Business Description

- Service Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Laboratorium Parahita Diagnostic Center

- Business Description

- Service Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- PT Indec Diagnostics

- Business Description

- Service Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Ultra Medica Clinic Surabaya

- Business Description

- Service Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- PT Prima Medika Laboratories

- Business Description

- Service Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- ABC Central Clinical Laboratory

- Business Description

- Service Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- PT Kimia Farma Diagnostika

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Lab Type |

|

| By Testing Services |

|

| By Disease |

|

| By Revenue Source |

|

| By Test Type |

|

| By End User |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.