India Ultrafiltration Market Report: Trends, Growth and Forecast (2026-2032)

By Membrane Material (Polymeric Membranes (Polyvinylidene Fluoride, Polyethersulfone, Polysulfone, Polyacrylonitrile, Polyvinyl Chloride, Others), Ceramic Membranes), By Module Type (Hollow Fiber, Tubular, Plate & Frame, Spiral Wound, Others), By System Type (Pressurized Ultrafiltration Systems, Submerged Ultrafiltration Systems), By Application (Municipal Water Treatment, Municipal Wastewater Treatment, Industrial Process Water Treatment, Wastewater Reuse & Recycling, Desalination Pre-treatment, Food & Beverage Processing, Biopharmaceutical & Pharmaceutical Processing, Chemical & Petrochemical Processing, Others), By End-Use Industry (Municipal, Food & Beverage, Pharmaceutical & Biotechnology, Chemical & Petrochemical, Power Generation, Oil & Gas, Electronics & Semiconductor, Pulp & Paper, Textile, Others), By Sales Channel (Retail Online (Company Websites, E-Commerce Marketplaces, Online Distributor Portals, Online RFQ/Quotation Platforms), Retail Offline (Authorized Distributors, Dealers & Retail Stores, System Integrators, Direct Sales)), By Region (North, East, West, South) ... Read more

|

Major Players

|

India Ultrafiltration Market Statistics and Insights, 2026

- Market Size Statistics

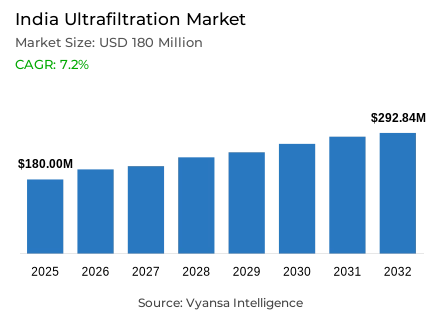

- Ultrafiltration market size in India was valued at USD 180 million in 2025 and is estimated at USD 192.96 million in 2026.

- The market size is expected to grow to USD 292.84 million by 2032.

- Market to register a CAGR of around 7.2% during 2026-32.

- Membrane Material Shares

- Polymeric membranes grabbed market share of 85%.

- Competition

- More than 10 companies are actively engaged in producing ultrafiltration in India.

- Top 5 companies acquired around 10% of the market share.

- DuPont Water Solutions, Veolia Water Technologies, Pall Corporation, Thermax, Ion Exchange India etc., are few of the top companies.

- Application

- Municipal water treatment grabbed 30% of the market.

India Ultrafiltration Market Outlook

The India ultrafiltration market was valued at USD 180 million in 2025 and is projected to advance from USD 192.96 million in 2026 to USD 292.84 million by 2032, registering a CAGR of 7.2% across the forecast period. This sustained and institutionally anchored expansion reflects a structurally sound growth environment within the broader India membrane filtration industry, where large-scale public water infrastructure investment, accelerating urban treatment capacity additions, and strengthening wastewater management requirements are collectively driving consistent and long-cycle procurement demand for advanced membrane filtration systems across municipal and industrial applications throughout the country. Growth is not demand-volatile but infrastructure-led, anchored in policy-backed programmes that are systematically expanding the scale and technical sophistication of India's water treatment network.

Material preference within the Indian market is defined by the commanding position of Polymeric Membranes, which account for approximately 85% of the membrane material segment. This dominant concentration reflects the deeply embedded and practically motivated preference among Indian utilities and industrial operators for polymeric ultrafiltration membranes India that combine cost-effective procurement economics, broad application adaptability, and the installation scalability required to serve the large treatment volumes characteristic of India's expanding public infrastructure programmes. As procurement decisions remain guided by deployment practicality and lifecycle cost efficiency, polymeric formats continue to attract the most commercially dependable and volume-consistent demand across the national membrane material landscape.

Application demand is led by Municipal Water Treatment, which commands approximately 30% of the overall application segment. This position reflects the sustained and institutionally embedded importance of urban and civic treatment requirements as the most significant and recurring revenue-generating end-use base for ultrafiltration technology across India. As drinking water expansion programmes scale and regulatory compliance expectations around treatment quality tighten, municipal water treatment India applications are generating the most stable and high-volume equipment procurement and installation demand within the national market structure.

Taken together, these structural demand characteristics define a clear and commercially dependable expansion pathway through 2032. Polymeric membrane leadership, municipal application dominance, and the institutional depth of India's water infrastructure investment programmes collectively establish an ultrafiltration market that is infrastructure-responsive, policy-supported, and well-positioned to benefit from the country's continuing commitment to expanding safe water access and wastewater management capacity throughout the forecast period.

India Ultrafiltration Market Growth Driver

National Water Infrastructure Programmes Mechanically Expand Treatment System Procurement

India's large-scale and policy-backed public water infrastructure expansion is generating direct, recurring, and commercially significant demand for advanced drinking water ultrafiltration India systems by progressively raising the filtration capacity, treatment quality, and operational reliability requirements of an expanding national water delivery network. As per data published by the Press Information Bureau of India, more than 15.57 crore rural households representing 80.38% of all rural households had tap water supply connections by 31 March 2025 under the Jal Jeevan Mission, confirming that the scale of piped water network expansion is mechanically increasing demand for treatment systems capable of delivering adequate filtration capacity, consistent feed-water conditioning, and dependable quality management across a continuously widening distribution infrastructure.

Urban infrastructure investment reinforces this demand driver with a separate and equally substantial layer of municipal treatment capacity addition. According to statistics released by the Press Information Bureau of India, AMRUT 2.0 had approved 10,647 million litres per day of water treatment plant capacity and 6,739 million litres per day of sewage treatment plant capacity by 2025, confirming that new treatment assets are being sanctioned at a scale that creates sustained and multi-year procurement demand for compact UF water treatment systems India capable of improving turbidity control, pathogen removal, and downstream process reliability within newly commissioned and upgraded public treatment facilities across India's major urban centres.

India Ultrafiltration Market Challenge

Groundwater Stress Elevates Treatment Complexity and Operational Cost

Rising groundwater extraction pressure and the progressive deterioration of raw water source quality across stressed aquifer zones are creating a structurally significant and technically demanding challenge for ultrafiltration system operators and membrane suppliers managing deployment performance across India's increasingly variable source-water environment. Based on data from the Press Information Bureau of India, India's total annual groundwater extraction reached 247.22 billion cubic metres in 2025 with a national groundwater extraction stage of 60.63%, confirming that extraction demand is already placing meaningful pressure on aquifer systems in ways that worsen raw water quality consistency, increase particulate and dissolved contaminant loads, and elevate membrane fouling risk and pretreatment requirements across industrial water filtration India and municipal treatment deployments in affected regions.

The geographic concentration of this challenge within formally classified stressed assessment units adds further operational and procurement complexity for treatment system providers operating across India's diverse hydrological landscape. As indicated by authoritative sources at the Press Information Bureau of India, 730 assessment units representing 10.80% of the country's total were classified as over-exploited in 2025 while a further 758 units representing 11.21% were classified as semi-critical, confirming that a significant proportion of India's groundwater-dependent treatment catchments are experiencing conditions that increase technical entry barriers, raise operating cost, and shift procurement preference toward higher-quality and more operationally resilient low-fouling UF membranes India capable of maintaining consistent treatment performance under challenging and variable source-water conditions.

Unlock Market Intelligence

Explore the market potential with our data-driven report

India Ultrafiltration Market Trend

SCADA Integration Is Reshaping Ultrafiltration System Design and Deployment Standards

A well-defined and commercially consequential structural trend is reshaping how water and wastewater treatment infrastructure is designed and operated across India, as the systematic integration of digital monitoring and supervisory control technology into public utility projects progressively elevates the performance expectations placed on treatment systems including IoT-enabled water filtration India and automated membrane filtration installations throughout the national infrastructure network. Evidence drawn from public data released by the Press Information Bureau of India confirms that 1,487 water supply projects under AMRUT 2.0 had been approved with SCADA technology by 2025, alongside large-scale water and sewage treatment capacity additions, confirming that digitally supervised operations are becoming a standard rather than a premium feature expectation within India's evolving public utility infrastructure investment framework.

The practical field-level implementation of this trend is already demonstrably active across commissioned projects within the AMRUT 2.0 programme. In line with findings from the Press Information Bureau of India, 230 water supply projects and 146 sewerage projects had been implemented with SCADA technology under the programme, confirming that automation-integrated treatment infrastructure is moving from approval to operational reality at meaningful scale. For automated UF systems India suppliers, this digital infrastructure transition creates a commercially significant revenue pathway through performance-tracked and automation-ready ultrafiltration systems that support stable treated-water output, faster response to quality fluctuations, and improved lifecycle performance management within digitally supervised utility operating environments.

India Ultrafiltration Market Opportunity

Treated Wastewater Reuse Policy Creates a Structurally New and Expanding Demand Layer

The formalisation and active policy promotion of treated wastewater reuse across India is creating a commercially significant and structurally additive opportunity for ultrafiltration technology providers by establishing a second and independently growing demand layer for membrane-based polishing treatment that operates alongside and independently from conventional freshwater treatment procurement cycles. As per official figures from the Press Information Bureau of India, AMRUT 2.0 had already approved 2,093 million litres per day of sewage treatment capacity specifically designated for recycle and reuse applications by 2025, confirming that municipal wastewater reuse India is being institutionalised within national infrastructure investment programmes at a scale that generates direct and sustained procurement demand for membrane filtration systems capable of meeting the tighter effluent quality standards required for non-potable and reclaimed water distribution.

The commercial scope of this opportunity is expanding further as national policy engagement with treated wastewater reuse broadens beyond conventional irrigation and industrial cooling applications into higher-value and more technically demanding end uses. Data compiled from internationally recognised public authorities at NITI Aayog confirms that a national workshop on the reuse of treated wastewater held in November 2025 highlighted common quality standards, wider utilisation frameworks, and the specific role of treated water in meeting emerging demands including data centre cooling requirements, confirming that water reuse solutions India policy is actively creating new institutional demand contexts for advanced membrane polishing treatment. For ultrafiltration system providers, this expanding reuse policy landscape represents a commercially durable growth opportunity that links membrane treatment demand to India's future industrial and urban water security priorities throughout the forecast period.

Unlock Market Intelligence

Explore the market potential with our data-driven report

India Ultrafiltration Market Segmentation Analysis

By Membrane Material

- Polymeric Membranes

- Polyvinylidene Fluoride

- Polyethersulfone

- Polysulfone

- Polyacrylonitrile

- Polyvinyl Chloride

- Others

- Ceramic Membranes

Polymeric Membranes command the highest share within the membrane material category at approximately 85%, reflecting overwhelming and broadly distributed procurement preference for membrane filtration systems India formats that deliver cost-effective deployment economics, broad application adaptability, and the installation scalability required to serve the large treatment volumes characteristic of India's expanding public and industrial water infrastructure. Indian utilities and industrial operators consistently select polymeric configurations because they combine adequate and proven treatment performance with well-understood procurement economics, widely available domestic and international supplier networks, and demonstrated scalability across both large municipal treatment plant installations and smaller distributed system deployments. Its commanding market position confirms that deployment cost efficiency, operational practicality, and broad application compatibility remain the most commercially durable procurement criteria within the India ultrafiltration membrane material landscape.

Its sustained dominance also reflects a wider market dynamic in which the established performance track record, competitive pricing, and broad technical familiarity of polymeric membrane systems create durable procurement confidence among Indian utility and industrial buyers who prioritise practical operational outcomes over material specification innovation. Polymeric membranes maintain their overwhelming market lead across India because they serve the full spectrum of treatment application requirements at accessible total system cost levels, support strong domestic supply chain depth, and benefit from extensive operator experience within both municipal and industrial treatment communities. As high-flux ultrafiltration membranes India and advanced low-fouling formulations enhance polymeric performance, this segment is expected to retain its anchor position throughout the forecast period.

By Application

- Municipal Water Treatment

- Municipal Wastewater Treatment

- Industrial Process Water Treatment

- Wastewater Reuse & Recycling

- Desalination Pre-treatment

- Food & Beverage Processing

- Biopharmaceutical & Pharmaceutical Processing

- Chemical & Petrochemical Processing

- Others

Municipal Water Treatment commands the highest share within the application category at approximately 30%, establishing public utility infrastructure as the most commercially significant and volume-generating end-use context for ultrafiltration technology across India. Municipal utilities and civic treatment operators consistently prioritise ultrafiltration for applications requiring dependable large-volume contaminant removal, consistent treatment quality performance under variable source-water conditions, and operational reliability across the high-throughput treatment trains characteristic of India's urban water supply infrastructure, with water reuse filtration India and direct potable treatment applications both contributing to the commercial depth of this segment across national and state-level programme procurement. Its leading position confirms that public infrastructure investment scale, rising regulatory quality expectations, and the need for technically reliable treatment capacity expansion are the primary demand drivers within the India ultrafiltration application landscape.

Its continued commercial leadership is expected to deepen through the forecast period as Jal Jeevan Mission network expansion, AMRUT 2.0 treatment capacity additions, and wastewater reuse programme implementation collectively sustain and broaden municipal procurement demand for membrane filtration systems at an institutionally backed pace that is structurally insulated from the demand volatility that affects more commercially cyclical industrial application segments. As sustainable water treatment India objectives continue to shape national infrastructure investment priorities, municipal water treatment is expected to retain and strengthen its position as the most strategically significant application category within the India ultrafiltration market through 2032.

List of Companies Covered in India Ultrafiltration Market

The companies listed below are highly influential in the India ultrafiltration market, with a significant market share and a strong impact on industry developments.

- DuPont Water Solutions

- Veolia Water Technologies

- Pall Corporation

- Thermax

- Ion Exchange India

- VA Tech WABAG

- QUA Group

- Aquatech

- Toray

- Pentair X-Flow

Market News & Updates

- QUA Group, 2026:

QUA deployed Q-SEP 8012 outside-in hollow-fibre ultrafiltration membranes for a 20 MLD TTRO plant serving a State Industrial Development Corporation in Southern India. The system delivered 562 m³/hr permeate flow per phase and reduced TDS from 1,300 ppm to below 150 ppm. The project supports treated-water availability for industrial operations

- VA Tech WABAG, 2025:

WABAG’s 40 MLD Ghaziabad TTRO plant in Uttar Pradesh received the Distinction Award in the Water Reuse Project of the Year category at the Global Water Awards 2025. The facility uses disc filtration, ultrafiltration, and reverse osmosis to convert municipal wastewater into industrial-grade water for Sahibabad Industrial Estate.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- India Ultrafiltration Market Policies, Regulations, and Standards

- India Ultrafiltration Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- India Ultrafiltration Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Membrane Material

- Polymeric Membranes- Market Insights and Forecast 2022-2032, USD Million

- Polyvinylidene Fluoride- Market Insights and Forecast 2022-2032, USD Million

- Polyethersulfone- Market Insights and Forecast 2022-2032, USD Million

- Polysulfone- Market Insights and Forecast 2022-2032, USD Million

- Polyacrylonitrile- Market Insights and Forecast 2022-2032, USD Million

- Polyvinyl Chloride- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Ceramic Membranes- Market Insights and Forecast 2022-2032, USD Million

- Polymeric Membranes- Market Insights and Forecast 2022-2032, USD Million

- By Module Type

- Hollow Fiber- Market Insights and Forecast 2022-2032, USD Million

- Tubular- Market Insights and Forecast 2022-2032, USD Million

- Plate & Frame- Market Insights and Forecast 2022-2032, USD Million

- Spiral Wound- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By System Type

- Pressurized Ultrafiltration Systems- Market Insights and Forecast 2022-2032, USD Million

- Submerged Ultrafiltration Systems- Market Insights and Forecast 2022-2032, USD Million

- By Application

- Municipal Water Treatment- Market Insights and Forecast 2022-2032, USD Million

- Municipal Wastewater Treatment- Market Insights and Forecast 2022-2032, USD Million

- Industrial Process Water Treatment- Market Insights and Forecast 2022-2032, USD Million

- Wastewater Reuse & Recycling- Market Insights and Forecast 2022-2032, USD Million

- Desalination Pre-treatment- Market Insights and Forecast 2022-2032, USD Million

- Food & Beverage Processing- Market Insights and Forecast 2022-2032, USD Million

- Biopharmaceutical & Pharmaceutical Processing- Market Insights and Forecast 2022-2032, USD Million

- Chemical & Petrochemical Processing- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By End-Use Industry

- Municipal- Market Insights and Forecast 2022-2032, USD Million

- Food & Beverage- Market Insights and Forecast 2022-2032, USD Million

- Pharmaceutical & Biotechnology- Market Insights and Forecast 2022-2032, USD Million

- Chemical & Petrochemical- Market Insights and Forecast 2022-2032, USD Million

- Power Generation- Market Insights and Forecast 2022-2032, USD Million

- Oil & Gas- Market Insights and Forecast 2022-2032, USD Million

- Electronics & Semiconductor- Market Insights and Forecast 2022-2032, USD Million

- Pulp & Paper- Market Insights and Forecast 2022-2032, USD Million

- Textile- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- Company Websites- Market Insights and Forecast 2022-2032, USD Million

- E-Commerce Marketplaces- Market Insights and Forecast 2022-2032, USD Million

- Online Distributor Portals- Market Insights and Forecast 2022-2032, USD Million

- Online RFQ/Quotation Platforms- Market Insights and Forecast 2022-2032, USD Million

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- Authorized Distributors- Market Insights and Forecast 2022-2032, USD Million

- Dealers & Retail Stores- Market Insights and Forecast 2022-2032, USD Million

- System Integrators- Market Insights and Forecast 2022-2032, USD Million

- Direct Sales- Market Insights and Forecast 2022-2032, USD Million

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- By Region

- North- Market Insights and Forecast 2022-2032, USD Million

- East- Market Insights and Forecast 2022-2032, USD Million

- West- Market Insights and Forecast 2022-2032, USD Million

- South- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Membrane Material

- Market Size & Growth Outlook

- India Polymeric Membranes Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Module Type- Market Insights and Forecast 2022-2032, USD Million

- By System Type- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By End-Use Industry- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Ceramic Membranes Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Module Type- Market Insights and Forecast 2022-2032, USD Million

- By System Type- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By End-Use Industry- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Thermax

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Ion Exchange India

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- VA Tech WABAG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- QUA Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Aquatech

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- DuPont Water Solutions

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Veolia Water Technologies

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Pall Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Toray

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Pentair X-Flow

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Thermax

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Membrane Material |

|

| By Module Type |

|

| By System Type |

|

| By Application |

|

| By End-Use Industry |

|

| By Sales Channel |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.