India Induction Cooktop Market Report: Trends, Growth and Forecast (2026-2032)

By Product Type (Free-Standing (Portable), Integrated (Built-in)), By Application (Household, Commercial), By Style (Multi-element, Single-element), By Number of Burners / Cooking Zones (Single Burner, 2 Burners, 3 Burners, 4 Burners), By Price Range (Low / Economy, Mid-Range, Premium), By Control Type (Touch Control, Knob / Manual Control), By Sales Channel (Retail Offline (Direct Sale, Hypermarkets/Supermarkets, Specialty Stores), Retail Online (Direct Sale, E-Commerce)), By End User / Household Type (Individual Households, Apartments / Urban Homes, Hotels, Restaurants & Cafes (HoReCa)), By Region (North, East, West, South) ... Read more

|

Major Players

|

India Induction Cooktop Market Statistics and Insights, 2026

- Market Size Statistics

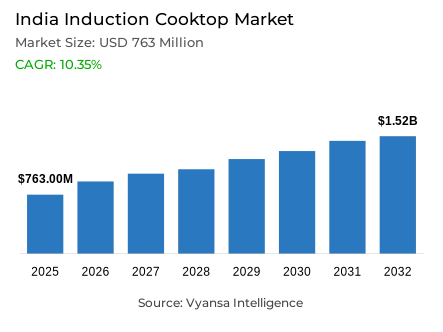

- Induction cooktop market size in India was valued at USD 763 million in 2025 and is estimated at USD 842 Million in 2026.

- The market size is expected to grow to USD 1.52 billion by 2032.

- Market to register a CAGR of around 10.35% during 2026-32.

- Product Type Shares

- Free-standing (portable) grabbed market share of 90%.

- Competition

- More than 10 companies are actively engaged in producing induction cooktop in India.

- Top 5 companies acquired around 65% of the market share.

- Usha International Ltd., V-Guard Industries Ltd., iBELL India, TTK Prestige Ltd., Versuni India Home Solutions Ltd. etc., are few of the top companies.

- Application

- Household grabbed 75% of the market.

India Induction Cooktop Market Outlook

The India Induction Cooktop Market was valued at USD 763 million in 2025 and is projected to grow from USD 842 million in 2026 to USD 1.52 billion by 2032, reflecting a CAGR of 10.35% during the forecast period. The policy push towards electric cooking and the development of national electricity infrastructure is a major contributor to market growth. According to a Government of India energy update (June 2025), power shortages decline to 0.1% in 2024-25, compared with 4.2% in 2013-14, while more than 2.8 crore households have been newly connected to the electricity grid. Such advances enhance the viability of electric cooking devices like induction cooktops in urban and semi-urban homes.

Programmes supported by the government are also promoting the shift to e-cooking solutions. The National Efficient Cooking Programme is an initiative by the Energy Efficiency Services Limited (EESL) to distribute induction cooktops and increase the popularity of electric cooking technologies among the population. These efforts can be used to launch induction cooking as a viable and energy-efficient option in the wider clean-energy transformation in India.

Within the product landscape, free‑standing (portable) induction cooktops account for 90% of the market. These models are still popular due to their ease of installation, portability, and applicability in a broad variety of residential environments. Their plug-and-use nature enables the end users to embrace electric cooking without altering their current kitchen infrastructure.

From an application perspective, household usage represents 75% of the market. Induction cooktops are usually bought in residential kitchens where families appreciate quick heating, convenience, and easy maintenance. With the increasing use of rooftop solar and the increasing awareness of energy efficient appliances, induction cooktops will have a better chance to gain momentum as a component of modern, electricity based cooking solutions in Indian households.

India Induction Cooktop Market Growth Driver

Policy-Led Electrification Strengthens the Shift to E-Cooking

The growing policy emphasis on electric cooking is a key driver of the induction cooktops demand in India. With the availability of electricity and the stability of power supply, households are increasingly becoming able to use electric appliances in their daily cooking activities. This transition is advantageous to induction cooktops because they heat faster, have more precise temperature control, and are cleaner to operate than traditional cooking methods.

This transition is strengthened by government efforts. A Government of India energy note (June 2025) reports that power shortages decline to 0.1% in 2024–25, compared with 4.2% in 2013–14, while more than 2.8 crore households have been connected to the electricity grid. Also, according to Energy Efficiency Services Limited (EESL), the National Efficient Cooking Programme is aimed at providing induction cooktops and encouraging the use of electric cooking. These electricity infrastructure and policy improvements are enhancing the base of induction cooktop use in Indian households.

India Induction Cooktop Market Challenge

Deep LPG Dependence Keeps Switching Barriers High

One of the major threats facing the India induction cooktop market is the fact that the market has been accustomed to the use of LPG as the main cooking fuel. Numerous families still use gas stoves as they are already part of everyday cooking and kitchen designs. Consequently, induction cooktops are often employed as an addition to LPG-based cooking systems, but not as a replacement.

The official data on fuel distribution points to the magnitude of LPG consumption. According to the Petroleum Planning and Analysis Cell (PPAC), the oil marketing companies in the public sector have 32.89 crore active domestic LPG customers as of 1 January 2025. Pradhan Mantri Ujjwala Yojana (PMUY) programme alone has benefited approximately 10.33 crore beneficiaries. end user switching to electric cooking is slow with such a huge installed LPG base. This high reliance on LPG still makes it difficult to fully migrate to induction-based cooking in most households.

Unlock Market Intelligence

Explore the market potential with our data-driven report

India Induction Cooktop Market Trend

Energy-Efficiency Positioning Becomes More Visible

The concept of energy efficiency is gaining more significance in the purchase of induction cooktops. Customers are becoming more conscious of the amount of electricity they use and the cost of running their homes, which is pushing manufacturers to focus on efficiency features, smart controls, and optimised heating technologies in their product lines.

National efficiency standards support this change. According to the Bureau of Energy Efficiency (BEE), its Standards and Labelling programme now includes 34 categories of appliances and equipment, and Induction Hob is one of the voluntary appliances. The induction cooking equipment included in the programme promotes more efficient comparisons between products. With end users becoming more aware of their electricity consumption and long-term operating expenses, energy-efficient performance is becoming a major product attribute that brands are emphasizing.

India Induction Cooktop Market Opportunity

Rooftop Solar Expands the Addressable Use Case

The growth of residential rooftop solar systems is a major opportunity to induction cooktop in India. With the households producing electricity using solar systems, electric cooking appliances will be more appealing since they can be used with self-generated renewable energy.

The magnitude of this opportunity is depicted through government programmes. According to a Government of India energy update (June 2025), the PM Surya Ghar programme has 50.03 lakh applications and serves 11.88 lakh households as of April 2025. As more households install rooftop solar systems, end users are becoming more interested in less grid reliance and less electricity bills. Induction cooktops can be easily incorporated into this shift, enabling households to incorporate cooking devices into larger energy-efficient home systems.

Unlock Market Intelligence

Explore the market potential with our data-driven report

India Induction Cooktop Market Segmentation Analysis

By Product Type

- Free-Standing (Portable)

- Integrated (Built-in)

The segment with the highest share under Product Type is Free‑standing (Portable) Induction Cooktops, accounting for 90% of the market. This leadership is indicative of the high appropriateness of portable models to the Indian households where flexibility and ease of installation are key factors of purchase.

Induction cooktops are portable and need minimum installation and can be operated by just plugging them into an electrical socket. This is why they are perfect in rental houses, hostels, small kitchens, and temporary cooking systems. They are also portable and therefore end users can use them as additional appliances when preparing their meals during peak times or when they want to cook something fast. Portable induction cooktops are the most popular type of product in the market because they are convenient and do not need structural changes in the kitchen.

By Application

- Household

- Commercial

Under Application, the Household segment accounts for approximately 75% of the market. This leadership indicates the high position of induction cooktops in domestic cooking. These appliances are used by families to prepare quick meals, reheat food, and cook small portions more efficiently and conveniently.

The domestic market is also very robust since the induction cooktops are safe and easy to maintain as opposed to the traditional gas stoves. The cooking surface is smooth and easy to clean and the appliance minimizes the risks of open flames. Such advantages make induction cooktops especially appealing in contemporary urban apartments and nuclear family houses. Consequently, residential kitchens still constitute the biggest market base of induction cooktops in India.

List of Companies Covered in India Induction Cooktop Market

The companies listed below are highly influential in the India induction cooktop market, with a significant market share and a strong impact on industry developments.

- Usha International Ltd.

- V-Guard Industries Ltd.

- iBELL India

- TTK Prestige Ltd.

- Versuni India Home Solutions Ltd.

- Bajaj Electricals Ltd.

- Pigeon (Stovekraft Ltd.)

- Butterfly Gandhimathi Appliances Ltd.

- Glen Appliances Pvt. Ltd.

- Orient Electric Ltd.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- India Induction Cooktop Market Policies, Regulations, and Standards

- India Induction Cooktop Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- India Induction Cooktop Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product Type

- Free-Standing (Portable)- Market Insights and Forecast 2022-2032, USD Million

- Integrated (Built-in)- Market Insights and Forecast 2022-2032, USD Million

- By Application

- Household- Market Insights and Forecast 2022-2032, USD Million

- Commercial- Market Insights and Forecast 2022-2032, USD Million

- By Style

- Multi-element- Market Insights and Forecast 2022-2032, USD Million

- Single-element- Market Insights and Forecast 2022-2032, USD Million

- By Number of Burners / Cooking Zones

- Single Burner- Market Insights and Forecast 2022-2032, USD Million

- 2 Burners- Market Insights and Forecast 2022-2032, USD Million

- 3 Burners- Market Insights and Forecast 2022-2032, USD Million

- 4 Burners- Market Insights and Forecast 2022-2032, USD Million

- By Price Range

- Low / Economy- Market Insights and Forecast 2022-2032, USD Million

- Mid-Range- Market Insights and Forecast 2022-2032, USD Million

- Premium- Market Insights and Forecast 2022-2032, USD Million

- By Control Type

- Touch Control- Market Insights and Forecast 2022-2032, USD Million

- Knob / Manual Control- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- Direct Sale- Market Insights and Forecast 2022-2032, USD Million

- Hypermarkets/Supermarkets- Market Insights and Forecast 2022-2032, USD Million

- Specialty Stores- Market Insights and Forecast 2022-2032, USD Million

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- Direct Sale- Market Insights and Forecast 2022-2032, USD Million

- E-Commerce- Market Insights and Forecast 2022-2032, USD Million

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- By End User / Household Type

- Individual Households- Market Insights and Forecast 2022-2032, USD Million

- Apartments / Urban Homes- Market Insights and Forecast 2022-2032, USD Million

- Hotels, Restaurants & Cafes (HoReCa)- Market Insights and Forecast 2022-2032, USD Million

- By Region

- North

- East

- West

- South

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Product Type

- Market Size & Growth Outlook

- India Free-Standing (Portable) Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Style- Market Insights and Forecast 2022-2032, USD Million

- By Number of Burners / Cooking Zones- Market Insights and Forecast 2022-2032, USD Million

- By Price Range- Market Insights and Forecast 2022-2032, USD Million

- By Control Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By End User / Household Type- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Integrated (Built-in) Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Style- Market Insights and Forecast 2022-2032, USD Million

- By Number of Burners / Cooking Zones- Market Insights and Forecast 2022-2032, USD Million

- By Price Range- Market Insights and Forecast 2022-2032, USD Million

- By Control Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By End User / Household Type- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- TTK Prestige Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Versuni India Home Solutions Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Bajaj Electricals Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Pigeon (Stovekraft Ltd.)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Butterfly Gandhimathi Appliances Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Usha International Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- V-Guard Industries Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- iBELL India

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Glen Appliances Pvt. Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Orient Electric Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- TTK Prestige Ltd.

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Application |

|

| By Style |

|

| By Number of Burners / Cooking Zones |

|

| By Price Range |

|

| By Control Type |

|

| By Sales Channel |

|

| By End User / Household Type |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.