India Diagnostic Labs Market Report: Trends, Growth and Forecast (2026-2032)

By Lab Type (Single/Independent Laboratories, Hospital-based Laboratories, Physician Office Laboratories, Others), By Testing Services (Physiological Function Testing, General & Clinical Testing, Esoteric Testing, Specialized Testing, Non-invasive Prenatal Testing, COVID-19 Testing, Others), By Disease (Cardiology, Oncology, Neurology, Orthopedics, Gastroenterology, Gynecology, Odontology, Others), By Revenue Source (Healthcare Plan, Out-of-Pocket, Public System), By Test Type (Pathology, Radiology), By End User (Referrals, Walk-ins, Corporate Clients), By Sector (Urban, Rural), By Region (North, East, West, South) ... Read more

|

Major Players

|

India Diagnostic Labs Market Statistics and Insights, 2026

- Market Size Statistics

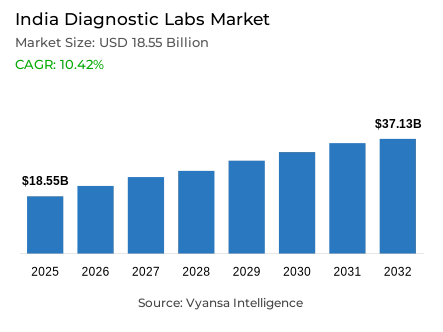

- Diagnostic labs market size in India was estimated at USD 18.55 billion in 2025.

- The market size is expected to grow to USD 37.13 billion by 2032.

- Market to register a CAGR of around 10.42% during 2026-32.

- Lab Type Shares

- Single/independent laboratories grabbed market share of 55%.

- Competition

- Diagnostic labs in India is currently being catered to by more than 10 companies.

- Top 5 companies acquired around 45% of the market share.

- Vijaya Diagnostic Centre Pvt. Ltd., Max Healthcare Institute Limited, Apollo Hospitals Enterprise Ltd., Dr. Lal PathLabs Limited, Agilus Diagnostic Limited etc., are few of the top companies.

- Testing Services

- General & clinical testing grabbed 45% of the market.

India Diagnostic Labs Market Outlook

The market of diagnostic laboratories in India is set to experience a healthy growth in the next few years. The market is projected to grow to over US$37.13 billion by 2032, with a high CAGR of about 10.42% in 2026-32, with a valuation of US 18.55 billion in 2025. This growth is supported by higher government expenditure on healthcare, with the Union Budget 2026-27 spending Rs.1,06,530.42 crore on health and family welfare, which is almost 10% higher than the previous year. The PM-ABHIM scheme has experienced an impressive 67.66% budget growth to Rs.4,770 crore, which has directly empowered the public health laboratories and increased testing infrastructure throughout the country.

One of the significant changes that are altering the market is the increase in preventive and precision testing. Indians are also choosing proactive health screening more than waiting until they experience symptoms. Preventive health tests increased by about 30% each year in 2025, with specialised tests like gut-health panels increasing by 47% and oncogenomic testing volumes growing by 16%. This change is being led by urban youth and middle-class populations, who are consistently choosing wellness packages to track conditions like diabetes and cardiovascular disease at an early stage.

The market faces serious access challenges despite the promising growth. Geographic barriers are still significant with about 70% of Indians living in rural and small towns. The low health insurance coverage (approximately 59%) and the low outpatient diagnostic coverage (less than 0.1) force millions of people to pay out of pocket, which discourages prompt testing. However, there are enormous opportunities in tier-2 and tier-3 cities, and the volume of diagnostics increases in these areas about 25% per year, as opposed to only 10% in metropolitan areas. These smaller cities already provide about 40% of total revenue.

The market is very fragmented with single/independent labs controlling about 55% of the market share of the 300,000 plus diagnostic centres in the country. The most common services are general and clinical testing (45%) which includes routine blood tests, urine tests, and simple imaging that is the foundation of medical diagnostics in all patient groups.

India Diagnostic Labs Market Growth Driver

Government Investment and Healthcare Infrastructure Enhancement

Diagnostics in India is directly supported by the policy focus on healthcare financing. In the 2026-27 Union Budget, the Ministry of Health and Family Welfare has been allocated budget of Rs. 1,06,530.42 crore and this is an increment of about 10% of the Revised Estimates FY 2025-26. This enriched population expenditure strengthens hospitals and public health programmes that habitually rely on laboratory screening to make treatment decisions, standby disease surveillance, and screening..

In the same budgetary framework, the expenditure on PM-ABHIM is 4,770 crores in the BE 2026-27, which is a significant 67.66 crores higher than the Revised Estimates of FY 2025-26 (Rs.2,845 crores). Its strategic emphasis on the growth of integrated public health laboratories and related infrastructure greatly enhances the reach and capacity of testing, thus contributing to a more standardised provision of diagnostics throughout the ecosystem and strengthening the pillars of market expansion.

India Diagnostic Labs Market Challenge

Geographic Disparities and Insurance Coverage Limitations

Although the market in India is growing rapidly, the diagnostic-lab market is experiencing significant challenges in equitable access. The rural and small-town populations (comprising about 70% of Indians) face considerable obstacles to diagnostic services. A 2025 study pointed out that such regions tend to have no close labs and experts, and patients have to travel long distances or even skip necessary tests. This extreme urban-rural disparity leads to late diagnosis of illnesses in hinterlands, which essentially compromises health outcomes and causes significant inefficiencies in service delivery.

The other important limitation is the low penetration of health insurance, which means that millions of people have to cover tests themselves. Less than half of Indian families (about 41%) have any health-insurance cover. In addition, outpatient diagnostics is rarely insured; outpatient policy coverage is less than 0.1 in India. As a result, regular check-ups and screening are costly to the end users, which actively discourages the use of preventive measures and timely check-ups among the population groups.

Unlock Market Intelligence

Explore the market potential with our data-driven report

India Diagnostic Labs Market Trend

Preventive Healthcare Adoption and Precision Medicine Integration

Another significant trend that is transforming the diagnostic-lab market in India is the increased preventive and precision testing. There is a growing preference among end users to undergo proactive health screenings instead of waiting to experience the symptoms. Preventive health tests increased by about 30% annually in 2025, as people became more aware of the importance of early detection of diseases like diabetes and cardiovascular disease. This change is being propelled by urban youth and middle-class end users who are often using wellness packages to track metabolic health, cardiac risk profiles and nutritional status, thus representing a paradigm shift in healthcare-seeking behaviour.

Specialised and advanced testing is also taking off in this paradigm. The number of people seeking lifestyle-related diagnostics like gut-health panels increased by 47% in 2025 due to the sedentary lifestyle and the recommendation of early intervention by physicians. Oncology tests, on the same note, showed consistent growth—oncogenomic testing volumes grew 16% with quicker turnaround times on results. These trends suggest a more general shift towards data-driven, personalised care, as diagnostic providers are broadening their test menus to incorporate genetic screenings and high-end molecular diagnostics.

India Diagnostic Labs Market Opportunity

Semi-Urban Market Penetration and Regional Expansion Potential

The opportunity to expand the diagnostic services to the tier-2 and tier-3 cities in India is a significant opportunity to the market players. Smaller towns have long been underserved, and the demand in these regions is increasing at a high rate. According to industry leaders, the volume of diagnostic tests in tier-2/3 cities is increasing by about 25% per year—much higher than the 10% per year increase in metropolitan areas. These towns already generate about 40% of total diagnostics revenue, which will grow as providers enter deeper into semi-urban markets.

Laboratory chains and hospital networks are actively increasing their presence in these areas. Public-private partnerships have enabled the presence of diagnostic chains in over 50% of the underdeveloped aspirational districts in India. Agilus and Metropolis companies earn significant revenue shares in smaller cities and are building dozens of new laboratories and collection centres in those locations. It is worth noting that the end users in the tier-2/3 cities are willing to pay premiums to quality diagnostics because of the historically limited choices, which opens up significant growth opportunities.

Unlock Market Intelligence

Explore the market potential with our data-driven report

India Diagnostic Labs Market Segmentation Analysis

By Lab Type

- Single/Independent Laboratories

- Hospital-based Laboratories

- Physician Office Laboratories

- Others

The single/independent laboratories segment holds the highest share under lab types, accounting for approximately 55% of the India diagnostic labs market. Thousands of small stand-alone pathology laboratories and clinics serve local communities, far outnumbering corporate chains or hospital-based facilities. India is home to over 300,000 diagnostic laboratories nationwide, with unorganized independent centers constituting the bulk of this landscape. This dominance of standalone laboratories highlights the market's fragmented nature, where numerous local establishments cater to neighborhood demand for blood tests and imaging services.

Such independent laboratories thrive by offering accessible, low-cost services, particularly in semi-urban and rural areas. While top-tier hospital laboratories and national chains provide specialized testing, single-location laboratories ensure basic diagnostic coverage across the country. However, this structure presents standardization challenges-only a small fraction of these laboratories are accredited-though ongoing quality improvement efforts aim to bring consistency. The predominance of independent laboratories underscores their essential role in delivering everyday diagnostic services throughout India.

By Testing Services

- Physiological Function Testing

- General & Clinical Testing

- Esoteric Testing

- Specialized Testing

- Non-invasive Prenatal Testing

- COVID-19 Testing

- Others

Under the testing service type, general & routine clinical testing forms the largest segment of the India diagnostic labs market, with an estimated share of approximately 45%. These encompass common blood tests, urine analyses, basic imaging procedures (X-rays/ultrasounds), and other standard pathology examinations-the foundation of most medical diagnoses. Such general testing services account for roughly half of all diagnostic spending, underscoring their critical role in healthcare delivery. Physicians rely extensively on these routine tests for initial patient assessments and ongoing monitoring of chronic conditions like diabetes and hypertension.

The broad demand for general and clinical testing is driven by its necessity across all end user groups. From annual health check-ups and pre-employment screenings to managing chronic diseases, basic laboratory tests remain in constant use. They are relatively affordable and widely available, making them the first touchpoint for medical care in many areas. India's push toward preventive healthcare means more individuals are proactively obtaining routine panels. Overall, the dominance of general clinical testing reflects its indispensability in detecting common ailments and guiding timely treatment.

List of Companies Covered in India Diagnostic Labs Market

The companies listed below are highly influential in the India diagnostic labs market, with a significant market share and a strong impact on industry developments.

- Vijaya Diagnostic Centre Pvt. Ltd.

- Max Healthcare Institute Limited

- Apollo Hospitals Enterprise Ltd.

- Dr. Lal PathLabs Limited

- Agilus Diagnostic Limited

- Metropolis Healthcare Ltd.

- Medcis PathLabs

- Thyrocare Technologies Limited

- Redcliffe Life Diagnostics Private Limited

- Lucid Medical Diagnostics Pvt Ltd.

Market News & Updates

- Dr. Lal PathLabs Limited, 2025:

Dr. Lal PathLabs publicly communicated strategic expansion initiatives with plans to open 15–20 new labs in underserved Tier-2 and Tier-3 Indian cities during FY25, underlining its push to broaden diagnostic accessibility and scale service offerings within the domestic diagnostics market.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. India Diagnostic Labs Market Policies, Regulations, and Standards

4. India Diagnostic Labs Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. India Diagnostic Labs Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in USD Million

5.2. Market Segmentation & Growth Outlook

5.2.1.By Lab Type

5.2.1.1. Single/Independent Laboratories- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Hospital-based Laboratories- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3. Physician Office Laboratories- Market Insights and Forecast 2022-2032, USD Million

5.2.1.4. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Testing Services

5.2.2.1. Physiological Function Testing- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. General & Clinical Testing- Market Insights and Forecast 2022-2032, USD Million

5.2.2.3. Esoteric Testing- Market Insights and Forecast 2022-2032, USD Million

5.2.2.4. Specialized Testing- Market Insights and Forecast 2022-2032, USD Million

5.2.2.5. Non-invasive Prenatal Testing- Market Insights and Forecast 2022-2032, USD Million

5.2.2.6. COVID-19 Testing- Market Insights and Forecast 2022-2032, USD Million

5.2.2.7. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Disease

5.2.3.1. Cardiology- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Oncology- Market Insights and Forecast 2022-2032, USD Million

5.2.3.3. Neurology- Market Insights and Forecast 2022-2032, USD Million

5.2.3.4. Orthopedics- Market Insights and Forecast 2022-2032, USD Million

5.2.3.5. Gastroenterology- Market Insights and Forecast 2022-2032, USD Million

5.2.3.6. Gynecology- Market Insights and Forecast 2022-2032, USD Million

5.2.3.7. Odontology- Market Insights and Forecast 2022-2032, USD Million

5.2.3.8. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Revenue Source

5.2.4.1. Healthcare Plan- Market Insights and Forecast 2022-2032, USD Million

5.2.4.2. Out-of-Pocket- Market Insights and Forecast 2022-2032, USD Million

5.2.4.3. Public System- Market Insights and Forecast 2022-2032, USD Million

5.2.5.By Test Type

5.2.5.1. Pathology- Market Insights and Forecast 2022-2032, USD Million

5.2.5.2. Radiology- Market Insights and Forecast 2022-2032, USD Million

5.2.6.By End User

5.2.6.1. Referrals- Market Insights and Forecast 2022-2032, USD Million

5.2.6.2. Walk-ins- Market Insights and Forecast 2022-2032, USD Million

5.2.6.3. Corporate Clients- Market Insights and Forecast 2022-2032, USD Million

5.2.7.By Sector

5.2.7.1. Urban- Market Insights and Forecast 2022-2032, USD Million

5.2.7.2. Rural- Market Insights and Forecast 2022-2032, USD Million

5.2.8.By Region

5.2.8.1. North- Market Insights and Forecast 2022-2032, USD Million

5.2.8.2. East- Market Insights and Forecast 2022-2032, USD Million

5.2.8.3. West- Market Insights and Forecast 2022-2032, USD Million

5.2.8.4. South- Market Insights and Forecast 2022-2032, USD Million

5.2.9.By Competitors

5.2.9.1. Competition Characteristics

5.2.9.2. Market Share & Analysis

6. India Single/Independent Laboratories Market Statistics, 2022-2032

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in USD Million

6.2. Market Segmentation & Growth Outlook

6.2.1.By Testing Services- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Disease- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By Revenue Source- Market Insights and Forecast 2022-2032, USD Million

6.2.4.By Test Type- Market Insights and Forecast 2022-2032, USD Million

6.2.5.By End User- Market Insights and Forecast 2022-2032, USD Million

6.2.6.By Sector- Market Insights and Forecast 2022-2032, USD Million

6.2.7.By Region- Market Insights and Forecast 2022-2032, USD Million

7. India Hospital-based Laboratories Market Statistics, 2022-2032

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in USD Million

7.2. Market Segmentation & Growth Outlook

7.2.1.By Testing Services- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Disease- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By Revenue Source- Market Insights and Forecast 2022-2032, USD Million

7.2.4.By Test Type- Market Insights and Forecast 2022-2032, USD Million

7.2.5.By End User- Market Insights and Forecast 2022-2032, USD Million

7.2.6.By Sector- Market Insights and Forecast 2022-2032, USD Million

7.2.7.By Region- Market Insights and Forecast 2022-2032, USD Million

8. India Physician Office Laboratories Market Statistics, 2022-2032

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in USD Million

8.2. Market Segmentation & Growth Outlook

8.2.1.By Testing Services- Market Insights and Forecast 2022-2032, USD Million

8.2.2.By Disease- Market Insights and Forecast 2022-2032, USD Million

8.2.3.By Revenue Source- Market Insights and Forecast 2022-2032, USD Million

8.2.4.By Test Type- Market Insights and Forecast 2022-2032, USD Million

8.2.5.By End User- Market Insights and Forecast 2022-2032, USD Million

8.2.6.By Sector- Market Insights and Forecast 2022-2032, USD Million

8.2.7.By Region- Market Insights and Forecast 2022-2032, USD Million

9. Competitive Outlook

9.1. Company Profiles

9.1.1.Dr. Lal PathLabs Limited

9.1.1.1. Business Description

9.1.1.2. Service Portfolio

9.1.1.3. Collaborations & Alliances

9.1.1.4. Recent Developments

9.1.1.5. Financial Details

9.1.1.6. Others

9.1.2.Agilus Diagnostic Limited

9.1.2.1. Business Description

9.1.2.2. Service Portfolio

9.1.2.3. Collaborations & Alliances

9.1.2.4. Recent Developments

9.1.2.5. Financial Details

9.1.2.6. Others

9.1.3.Metropolis Healthcare Ltd.

9.1.3.1. Business Description

9.1.3.2. Service Portfolio

9.1.3.3. Collaborations & Alliances

9.1.3.4. Recent Developments

9.1.3.5. Financial Details

9.1.3.6. Others

9.1.4.Medcis PathLabs

9.1.4.1. Business Description

9.1.4.2. Service Portfolio

9.1.4.3. Collaborations & Alliances

9.1.4.4. Recent Developments

9.1.4.5. Financial Details

9.1.4.6. Others

9.1.5.Thyrocare Technologies Limited

9.1.5.1. Business Description

9.1.5.2. Service Portfolio

9.1.5.3. Collaborations & Alliances

9.1.5.4. Recent Developments

9.1.5.5. Financial Details

9.1.5.6. Others

9.1.6.Vijaya Diagnostic Centre Pvt. Ltd.

9.1.6.1. Business Description

9.1.6.2. Service Portfolio

9.1.6.3. Collaborations & Alliances

9.1.6.4. Recent Developments

9.1.6.5. Financial Details

9.1.6.6. Others

9.1.7.Max Healthcare Institute Limited

9.1.7.1. Business Description

9.1.7.2. Service Portfolio

9.1.7.3. Collaborations & Alliances

9.1.7.4. Recent Developments

9.1.7.5. Financial Details

9.1.7.6. Others

9.1.8.Apollo Hospitals Enterprise Ltd.

9.1.8.1. Business Description

9.1.8.2. Service Portfolio

9.1.8.3. Collaborations & Alliances

9.1.8.4. Recent Developments

9.1.8.5. Financial Details

9.1.8.6. Others

9.1.9.Redcliffe Life Diagnostics Private Limited

9.1.9.1. Business Description

9.1.9.2. Service Portfolio

9.1.9.3. Collaborations & Alliances

9.1.9.4. Recent Developments

9.1.9.5. Financial Details

9.1.9.6. Others

9.1.10. Lucid Medical Diagnostics Pvt Ltd.

9.1.10.1. Business Description

9.1.10.2. Service Portfolio

9.1.10.3. Collaborations & Alliances

9.1.10.4. Recent Developments

9.1.10.5. Financial Details

9.1.10.6. Others

10. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Lab Type |

|

| By Testing Services |

|

| By Disease |

|

| By Revenue Source |

|

| By Test Type |

|

| By End User |

|

| By Sector |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.