India Cooking Appliances Market Report: Trends, Growth and Forecast (2026-2032)

By Product Type (Large Cooking Appliances (Free-standing Large Cooking Appliances, Hobs, Ovens, Cooker Hoods, Range Cookers, Others), Small Cooking Appliances (Coffee Machines, Coffee Mills, Air Fryers, Electric Grills, Electric Steamers, Free-standing Hobs, Kettles, Others)), By Installation / Structure (Built-in, Freestanding / Countertop), By End User (Residential / Household, Commercial), By Sales Channel (Retail Online (Direct Sale, E-Commerce), Retail Offline (Direct Sale, Hypermarkets/Supermarkets, Specialty Stores)), By Region (North, East, West, South) ... Read more

|

Major Players

|

India Cooking Appliances Market Statistics and Insights, 2026

- Market Size Statistics

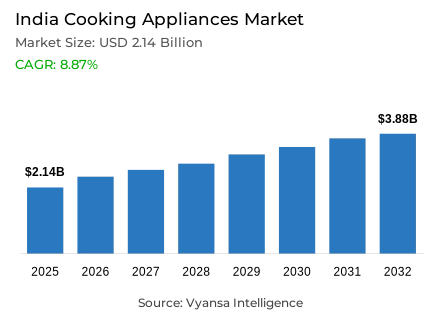

- Cooking appliances market size in India was valued at USD 2.14 billion in 2025 and is estimated at USD 2.6 Billion in 2026.

- The market size is expected to grow to USD 3.88 billion by 2032.

- Market to register a CAGR of around 8.87% during 2026-32.

- Product Type Shares

- Small cooking appliances grabbed market share of 60%.

- Competition

- More than 10 companies are actively engaged in producing cooking appliances in India.

- Top 5 companies acquired around 60% of the market share.

- LG Electronics India Limited, Panasonic Life Solutions India Private Limited, Pigeon Appliances Private Limited, TTK Prestige Limited, Versuni etc., are few of the top companies.

- Installation / Structure

- Freestanding / countertop grabbed 85% of the market.

India Cooking Appliances Market Outlook

The India Cooking Appliances Market was valued at USD 2.14 billion in 2025 and is projected to grow from USD 2.6 billion in 2026 to USD 3.88 billion by 2032, reflecting a CAGR of 8.87% during the forecast period. The gradual increase in clean cooking infrastructure and the increased availability of modern energy sources to Indian households are strong indicators of market growth. According to NITI Aayog, 100% of households now have electricity access, while the share of households using clean cooking fuels (LPG and PNG) increases to 96.35% in 2024, compared with 92.02% in 2020.

These infrastructural developments provide favourable conditions to both first-time appliance adoption and replacement demand. The growth of fuel distribution also strengthens the end user base of cooking appliances. As of 1 January 2026, the Petroleum Planning and Analysis Cell (PPAC) reports 3321.1 lakh active domestic LPG connections, and 15896515 domestic PNG connections as of 31 October 2025. With the increasing number of households moving to organized fuel systems, the demand of gas stoves, induction hobs, microwave ovens, and other contemporary cooking appliances is increasing in both urban and semi-urban areas. Within the product landscape, Small Cooking Appliances account for 60% of the market.

These miniature appliances are very popular due to their convenience, affordability, and versatility in daily cooking. Induction cooktops, microwave ovens, and small countertop cooking appliances are products that are increasingly becoming part of the modern kitchen where space optimisation and energy efficiency are becoming increasingly important in the buying decision.

Market structure is also influenced by installation preferences. Freestanding or countertop appliances hold 85% of the market, reflecting the strong demand for portable and easy‑to‑install cooking solutions. These appliances are not permanent and do not need any structural changes and can be used in both owned and rented houses. The India cooking appliances market is projected to experience a consistent growth up to 2032 as the digital retail and energy-efficiency awareness keeps growing.

India Cooking Appliances Market Growth DriverClean Cooking Access Keeps Core Demand Expanding

The ever-growing modern cooking infrastructure is one of the major drivers of the Indian cooking appliances market. Government programs that support the use of clean cooking energy have significantly increased access to electricity and modern fuels by households. This infrastructural growth strengthens the foundation of appliance adoption, as households are becoming more reliant on formal energy systems that serve modern cooking appliances.

According to NITI Aayog, 100% of households in India possess electricity access, while the availability of clean cooking fuel rises to 96.35% of households in 2024, compared with 92.02% in 2020. This trend is further supported by the growth of LPG and PNG networks. According to the Petroleum Planning and Analysis Cell (PPAC), there are 3321.1 lakh active domestic LPG connections and 15896515 domestic PNG connections as of January 2026 and October 2025, respectively. With the increasing number of households moving to organized clean-fuel networks, first-time appliance purchases and replacement demand remain the drivers of market growth in the country.

India Cooking Appliances Market ChallengeUneven Clean-Cooking Adoption Limits Full-Penetration Potential

Although there has been a significant change in cooking infrastructure, modern cooking access in India is not fully universal yet. Although the adoption of clean fuels has been growing at a very high rate, some households are still not part of the formal LPG or PNG ecosystem. This disparity restricts the homogenous adoption of modern cooking appliances in the nation. Data from NITI Aayog indicate that 96.35% of households have access to clean cooking fuel in 2024, implying that a residual segment of the population still relies on alternative cooking methods.

This disproportionate access has an impact on the adoption of appliances since most of the modern cooking appliances require a stable power supply or a stable fuel network to be used consistently. As a result, the market has been characterized by differences in the penetration of appliances in various regions and income groups. As long as clean-cooking infrastructure is not completely universalized, appliance manufacturers will still struggle to attain evenly spread market growth.

Unlock Market Intelligence

Explore the market potential with our data-driven report

India Cooking Appliances Market TrendEnergy Efficiency Moves Closer to Purchase Decisions

In India, energy efficiency is gradually becoming a critical determinant in the purchase of cooking appliances. With the increased consciousness of households about the use of electricity and the cost of operation, buyers are starting to consider appliances based not only on price and features but also on the long-term energy performance. National efficiency programmes support this shift. According to the Bureau of Energy Efficiency (BEE), its Standards and Labeling programme now includes 34 categories of appliances and equipment, such as cooking appliances like microwave ovens and induction hobs.

Standardized energy-efficiency labelling helps end users to compare appliances in terms of electricity consumption and efficiency. Consequently, manufacturers are increasingly emphasizing energy-saving technology and efficiency ratings, which strengthens an increasing end user preference towards appliances that offer performance and reduced long-term operating costs.

India Cooking Appliances Market OpportunityDigital Reach Opens Wider Direct-to-Consumer Access

The digital connectivity is opening up new avenues to the cooking appliance brands to access end users in India. The online platforms offer increased product exposure and allow customers to compare specifications, prices, and reviews prior to making a purchase decision. This change is especially beneficial to small cooking devices that can be easily sold and shipped via e-commerce platforms. The growing digital infrastructure in India increases this opportunity. The Telecom Regulatory Authority of India (TRAI) estimates 1028.61 million internet subscribers and 1007.35 million broadband subscribers in the country as of December 2025.

This vast networked population enables the appliance brands to access end users outside the conventional retail channels. Online platforms allow businesses to conduct promotions, offer product demonstrations, and establish closer direct-to-end user relationships. With online discovery and purchase steadily growing, online platforms are emerging as a more significant growth channel to cooking appliance manufacturers.

Unlock Market Intelligence

Explore the market potential with our data-driven report

India Cooking Appliances Market Segmentation Analysis

By Product Type

- Large Cooking Appliances

- Free-standing Large Cooking Appliances

- Hobs

- Ovens

- Cooker Hoods

- Range Cookers

- Others

- Small Cooking Appliances

- Coffee Machines

- Coffee Mills

- Air Fryers

- Electric Grills

- Electric Steamers

- Free-standing Hobs

- Kettles

- Others

The segment with the highest share under Product Type is Small Cooking Appliances, accounting for 60% of the market. This leadership is based on the high demand of small and multi-purpose cooking solutions that address daily kitchen requirements. The popularity of small appliances is due to their convenience and flexibility and the fact that they do not need as much investment as large built-in kitchen appliances. The appliances also enjoy the advantage of high replacement rates and common usage in homes.

Induction cooktops, microwave ovens, and portable cooking devices are products that are usually used in daily cooking. Their small size allows them to be easily fitted in the contemporary kitchen, especially in urban houses where space is the most important factor. Small cooking appliances remain the product mix in the Indian cooking appliances market due to their affordability, portability, and the ability to be used in a variety of cooking styles.

By Installation / Structure

- Built-in

- Freestanding / Countertop

Under Installation / Structure, Freestanding or Countertop appliances account for approximately 85% of the market. This leading role is an indication of the convenience and adaptability of appliances that can be conveniently stacked on kitchen counters without the need to install them permanently. Free-standing appliances are especially appealing in the markets where a large number of households are inclined to portable and ready-to-use solutions.

These appliances are easily portable, have minimum set up and do not entail extra renovation and installation expenses. This renders them appropriate in both owned and rental housing settings. The fact that these appliances can be used as soon as they are bought increases their attractiveness to a wide end user market. As a result, freestanding and countertop models still occupy the biggest portion of the Indian cooking appliances market, which is backed by their convenience and availability.

List of Companies Covered in India Cooking Appliances Market

The companies listed below are highly influential in the India cooking appliances market, with a significant market share and a strong impact on industry developments.

- LG Electronics India Limited

- Panasonic Life Solutions India Private Limited

- Pigeon Appliances Private Limited

- TTK Prestige Limited

- Versuni

- Bajaj Electricals Limited

- Butterfly Gandhimathi Appliances Limited

- Glen Appliances Private Limited

- Franke Faber India Private Limited

- Elica PB India Private Limited

Market News & Updates

- LG Electronics India Limited, 2025:

LG unveiled its Essential Series in October 2025 as a “Made for India” appliance lineup, including a Convertible Oven with Indian Auto Cook menus for dishes such as paneer, ghee, and dal, plus Air Fry and Convection modes. This is important for the India cooking appliances market because it combines localized cooking presets with healthier, multifunctional cooking formats, helping broaden adoption of modern ovens among Indian households.

- Glen Appliances Private Limited, 2025:

Glen introduced its Built-in Microwave with Convection Jog Wheel Control 25L (MO-674CONBL) with the official product page showing “Item available from: Oct 2025.” The model adds convection cooking, grill capability, auto-cook menus, and a built-in premium format for modular kitchens. This is a meaningful update for the India cooking appliances market because it strengthens demand in built-in cooking formats where aesthetics, multi-function cooking, and compact kitchen integration are becoming more important.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- India Cooking Appliances Market Policies, Regulations, and Standards

- India Cooking Appliances Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- India Cooking Appliances Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product Type

- Large Cooking Appliances- Market Insights and Forecast 2022-2032, USD Million

- Free-standing Large Cooking Appliances- Market Insights and Forecast 2022-2032, USD Million

- Hobs- Market Insights and Forecast 2022-2032, USD Million

- Ovens- Market Insights and Forecast 2022-2032, USD Million

- Cooker Hoods- Market Insights and Forecast 2022-2032, USD Million

- Range Cookers- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Small Cooking Appliances- Market Insights and Forecast 2022-2032, USD Million

- Coffee Machines- Market Insights and Forecast 2022-2032, USD Million

- Coffee Mills- Market Insights and Forecast 2022-2032, USD Million

- Air Fryers- Market Insights and Forecast 2022-2032, USD Million

- Electric Grills- Market Insights and Forecast 2022-2032, USD Million

- Electric Steamers- Market Insights and Forecast 2022-2032, USD Million

- Free-standing Hobs- Market Insights and Forecast 2022-2032, USD Million

- Kettles- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Large Cooking Appliances- Market Insights and Forecast 2022-2032, USD Million

- By Installation / Structure

- Built-in- Market Insights and Forecast 2022-2032, USD Million

- Freestanding / Countertop- Market Insights and Forecast 2022-2032, USD Million

- By End User

- Residential / Household- Market Insights and Forecast 2022-2032, USD Million

- Commercial- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- Direct Sale- Market Insights and Forecast 2022-2032, USD Million

- E-Commerce- Market Insights and Forecast 2022-2032, USD Million

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- Direct Sale- Market Insights and Forecast 2022-2032, USD Million

- Hypermarkets/Supermarkets- Market Insights and Forecast 2022-2032, USD Million

- Specialty Stores- Market Insights and Forecast 2022-2032, USD Million

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- By Region

- North

- East

- West

- South

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Product Type

- Market Size & Growth Outlook

- India Large Cooking Appliances Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- Product Type- Market Insights and Forecast 2022-2032, USD Million

- By Installation / Structure- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Distribution Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Small Cooking Appliances Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- Product Type- Market Insights and Forecast 2022-2032, USD Million

- By Installation / Structure- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Distribution Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- TTK Prestige Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Versuni

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Bajaj Electricals Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Butterfly Gandhimathi Appliances Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Glen Appliances Private Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- LG Electronics India Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Panasonic Life Solutions India Private Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Pigeon Appliances Private Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Franke Faber India Private Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Elica PB India Private Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- TTK Prestige Limited

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Installation / Structure |

|

| By End User |

|

| By Sales Channel |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.